BRBR - BellRing Brands: Rating Downgrade To Hold While Monitoring FY24 Growth Situation

2023-06-28 07:54:14 ET

Summary

- BellRing Brands' products continue to see sales growth with strong industry demand for ready-to-drink protein shakes.

- I would pay attention to capacity and COGS developments to determine if FY24 growth will continue to see double digits.

- Valuation is now at 25x NTM P/E, which I expect to contract back to mean.

Investment thesis

Premier Protein and Dymatize are two of BellRing Brands' ( BRBR ) most prominent products. RTD (ready-to-drink) protein shakes are the backbone of Premier Protein, and they're formulated to provide a lot of protein for not a lot of calories. Dymatize protein powder and sports nutrition is designed specifically for athletes who want to perform better. During the most recent earnings call, management increased their earnings forecast for the second consecutive quarter and reported encouraging data regarding the company's progress toward expanding its capacity. All in all, the business has executed just as expected, and the stock price has reflected my price target quicker than I expected. With the stock now priced at 25x NTM PE, I am downgrading my buy rating to a hold. Nonetheless, I maintain an optimistic outlook on the company and anticipate the emergence of yet another buying opportunity.

Industry demand remains strong

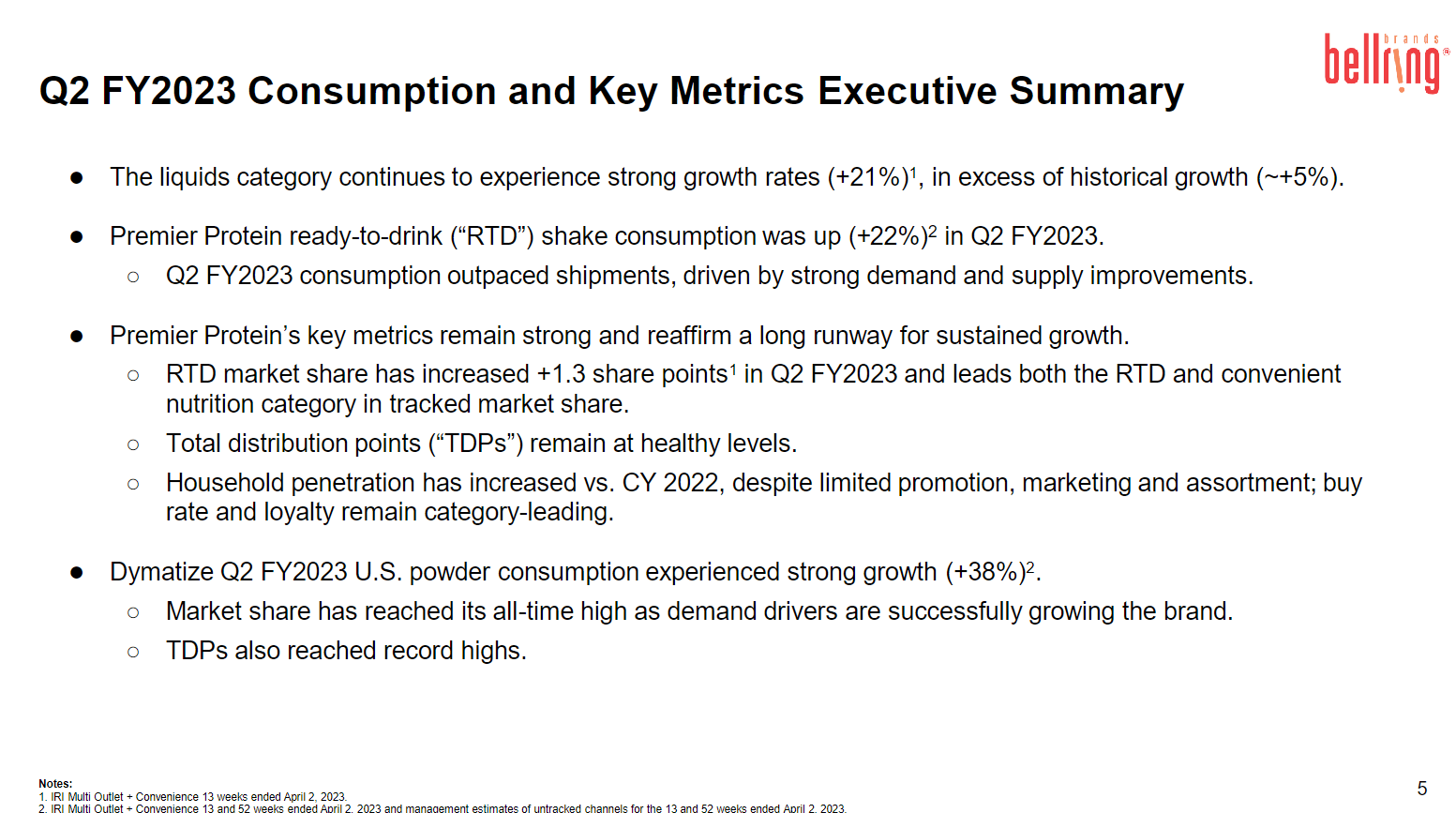

Industry-wide, the RTD protein shakes category saw continued strength, increasing by 21%, which is faster than the 15% increase seen over the previous 12 months and significantly higher than the 5% increase seen on average over the past few years. Since there is no compelling reason to expect that the underlying demand trend will change, I take this as a sign that the underlying demand is doing well and that demand will continue to be strong. If inflation or high interest rate would impact demand, we should already see it happening in the numbers. This is great news for BRBR, as the company is showing signs of expanding its market share thanks to rising demand (Retail sales of Premier and Dymatize have increased by 21.9% and 38.3%, respectively, across all distribution channels).

{kind=link}

Key brands sales remain strong

Beginning with Premier, the brand is riding high, with net sales growth for the brand reaching its highest in over 18 months thanks to strong volume gains and price benefit. However, I feel it important to point out that pricing has been a key factor in the expansion (20% of the 26% growth is pricing). On the positive side, the price increase has offset significant cost inflation. However, on the negative side, it also means that this performance is unlikely to repeat itself again in FY24 as BRBR laps a tough comp next year. I'm worried that the headline growth will decelerate dramatically, which will send the stock plummeting. That said, since Premier consumption exceeded shipments in the second quarter, it is possible that volume growth will quicken as retailers stock up to meet strong seasonal demand and boost TDPs. The recovery of distribution for Premier flavors that were discontinued in 2022 thanks to the addition of incremental capacity may also be a driver of volume growth in FY24. This should cushion the impact of loss of pricing tailwind in FY24.

As for Dymatize, all the growth is driven by pricing with modest volume decline. Sales appear to be low in volume, but this is because some products were phased out all at once, while sales rose organically due to increased brand investments. In fact, Dymatize's distribution continues to grow, as evidenced by their 157 TDPs, 51% ACV, and 38% quarterly increase in dollar consumption. However, I anticipate the same difficulty for the brand in FY24 when it needs to lap the high pricing comp in FY23.

What to monitor moving forward

My worry about volume growth in FY24 is being alleviated by the forthcoming increase of >20% in the production capacity of BRBR shakes. This would end the current capacity issues and enable BRBR to grow volume much faster than FY22/23. Gross margin expansion is another lever that I expect to soften the blow of reduced pricing tailwinds. I anticipate the cheaper inventory to reflect in the COGS line as BRBR cycles through its FIFO inventory, given that key inputs like the cost of milk and whey protein have decreased since the peak in FY22 due to Covid supply chain issue. BRBR's gross margin increased by almost 200 basis points in FY19 due to similar reasons, so there is a good precedent here to suggest it could happen again. Thus, while price increases are unlikely to contribute to FY24 top-line growth, volume gains enabled by capacity increases and gross margin expansion may still result in healthy growth at the gross profit line.

Valuation

My model suggests BRBR is worth $35.29, if it trades at 21x forward revenue multiple in FY24.

Model walkthrough:

- Revenue updated to reflect FY23 consensus estimates, and growth to be supported in FY24 given easing of supply constraint and margins to be stable due to gross margin expansion. Growth in FY25 to decelerate optically as BRBR lap a tough comp in FY24.

- To be conservative, I now expect BRBR forward PE to revert to mean of 21x forward PE.

Own model

Risks

Channel concentration

Retailers like Costco and Walmart see a high volume of BRBR sales. Negative publicity, decreased business, and customer defections stemming from these sources would be catastrophic for BRBR.

Conclusion

BRBR has performed as expected, with Premier Protein and Dymatize driving sales growth. The industry demand for RTD protein shakes remains strong, indicating continued market strength for BRBR. Looking ahead, the increase in production capacity and potential gross margin expansion provide optimism for volume growth and profitability in FY24. Despite the recent stock price increase, I am downgrading my rating to a hold, but I maintain an optimistic outlook and anticipate future buying opportunities for BRBR stock.

For further details see:

BellRing Brands: Rating Downgrade To Hold While Monitoring FY24 Growth Situation