BHE - Benchmark Electronics: Higher-Value Segments Show Signs Of Slowing Down

Summary

- Other than Aerospace & Defense, all of BHE's segments performed very well year-over-year.

- Supply constraints continue to weigh on the company, and if there are any surprises there, it should result in underperformance based upon management guidance.

- In the third quarter, its higher-value segments showed signs of slowing down, which if that continues, the share price of the company will take a hit.

Benchmark Electronics, Inc. ( BHE ) has had a great year in all its segments with the exception of Aerospace & Defense. Nonetheless, in the third quarter, its higher-value segments all showed signs of slowing down, even as its traditional segments outperformed.

The challenge for BHE is the traditional segments of Computing and Telco account for only 24 percent of total revenue, so the higher value segments, if they continue to slow down, will have a strong impact on the performance of the company in 2023.

With supply chain constraints being a major issue for the company, if it gets worse the company is going to come under a lot of pressure, but if it gets better-than-expected in the near term, it could surprise to the upside.

Taking into account the economic conditions as they stand today, I'm leaning toward supply constraints having a better chance of getting worse in the first half of 2023, with the probability of starting to ease in the second half.

In this article, we'll look at the implications of some of the numbers in its recent earnings report, especially as they relate to segment mix and pointing to things slowing down in the higher-value segments.

Some of the numbers

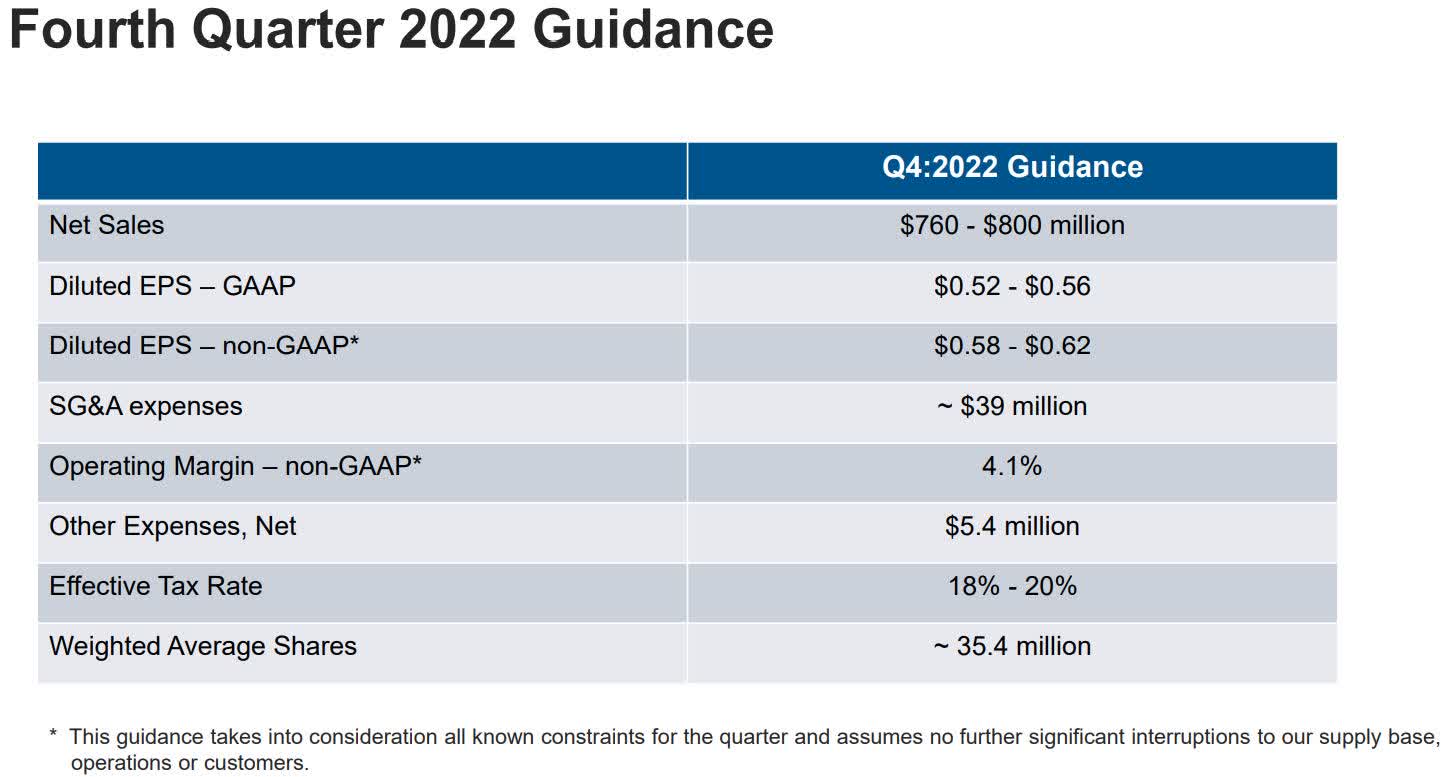

Revenue in the third quarter of 2022 was $772 million, up 35 percent from the $572 million in revenue generated in the third quarter of 2021. Cost of sales in the quarter was $705 million. Revenue guidance for the fourth quarter of 2022 was in a range of $760 million to $800 million.

Gross margin in the reporting period was 8.7 percent, down 70 basis points from gross margin of 9.4 percent year-over-year.

Operating margin in the third quarter was 3.3 percent, up 120 basis points from operating margin of 2.1 percent in the third quarter of 2021.

{kind=link}

Net income in the quarter was $18.8 million or $0.53 per diluted share, up over $10 million from net income of $8 million or $0.23 per share in the third quarter of 2021. Net income for the first nine months of 2022 was $47 million or $1.32 per diluted share, over double the $23.4 million in net income or $0.65 per share in the first nine months of 2021.

Free cash flow in the third quarter was negative $(40) million, up $8 million sequentially.

GAAP earnings per share in the fourth quarter is guided to be in a range of $0.52 to $0.56 per share.

At the end of the third quarter of 2022 the company had cash and cash equivalents of $247 million, down approximately $24 million from the cash and cash equivalents it held at the end of calendar 2021. Long-term debt stood at $296 million at the end of the reporting period, up from the $654 million in long-term debt at the end of calendar 2021.

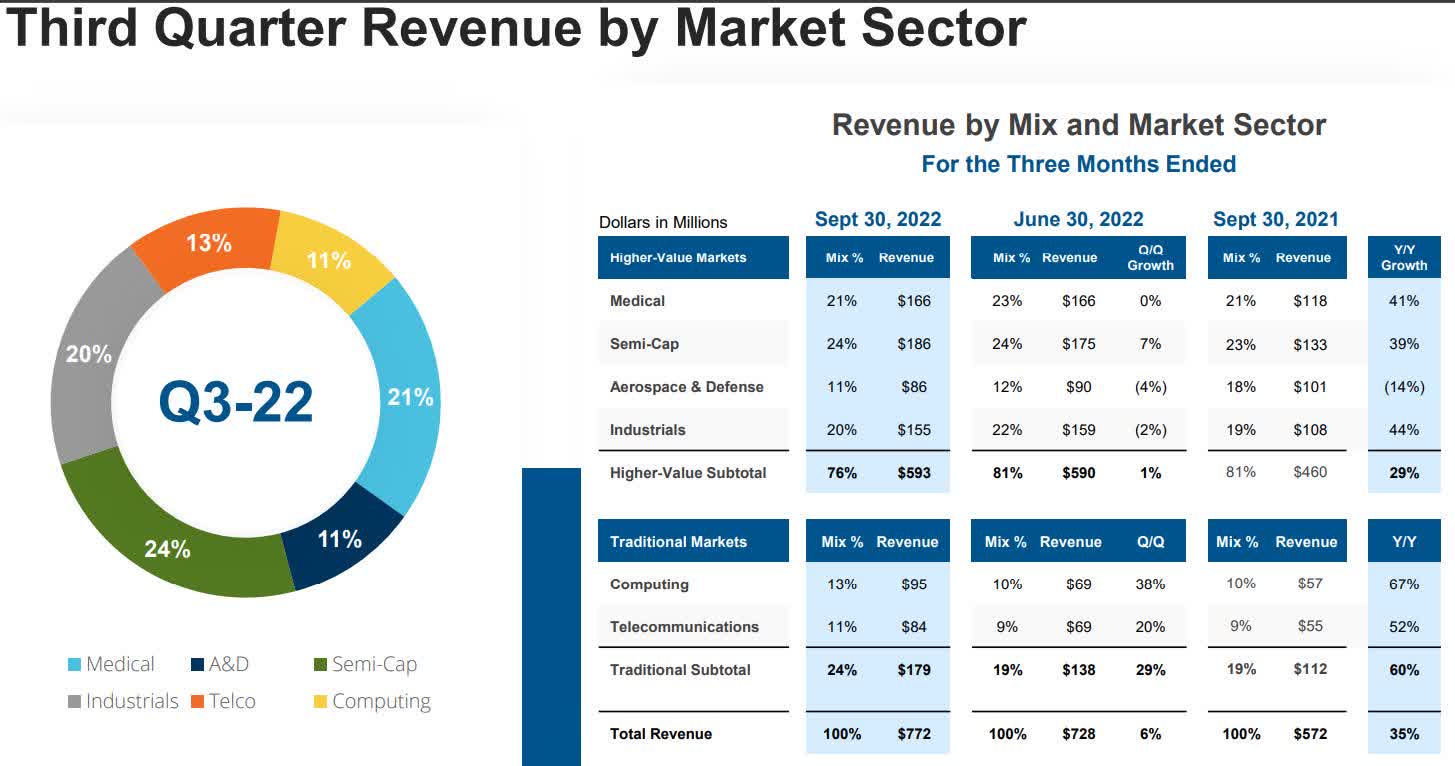

Revenue by mix

While BHE has had an excellent year across most of its segments, in the third quarter there were some signs of slowing down, which we'll have to watch in the fourth quarter and into 2023.

{kind=link}

On a percentage basis, Computing was the top segment for the company, generating revenue of $67 million, up 67 percent year-over-year. In the third quarter it accelerated, with revenue up 38 percent sequentially. Computing accounts for 13 percent of total revenue. The ramp up in high performance computing programs was the main catalyst in computing.

Next is Telco, which generated revenue of $84 million in the reporting period, up 52 percent year-over-year. It also had momentum in the third quarter, with revenue up 20 percent from the prior quarter. Telco accounts for 11 percent of total revenue. Strong demand and new broadband infrastructure starts were the impetus behind the strong performance.

Revenue for Industrials in the third quarter was $155 million, up 44 percent year-over-year. It slowed down in the third quarter, falling from $159 million sequentially, down 2 percent. The reason given for the decline was material constraints; something that could continue in the fourth quarter and early 2023. The tailwind from industrials over the last year came from infrastructure, LiDAR and products related to energy. Industrials account for 20 percent of overall.

In its Medical segment revenue in the reporting period was $166 million, up 41 percent year-over-year. That was flat sequentially. Medical accounts for 21 percent of total revenue as of the end of the third quarter of 2022. Growth for the last year came from getting more from its existing customers and new program starts.

Semi-Cap revenues in the third quarter came in at $186 million, up 39 percent year-over-year and up 7 percent sequentially. Demand for "complex precision machining and large electromechanical assembly services" were attributed to the revenue growth in the segment. Semi-Cap accounts for 24 percent of total revenue.

Aerospace & Defense revenue was $86 million in the third quarter of 2022, down 14 percent year-over-year, and down 4 percent sequentially. The drop in revenue reportedly came from supply chain constraints, and again, that's probably going to continue on into 2023. A&D accounts for 11 percent of total revenue.

Interestingly, all of the higher-value markets of BHE slowed down in the third quarter, while its traditional markets took off. But with traditional markets only accounting for 24 percent of revenue combined (Computing and Telco), the higher-value segments have more impact on the performance of the company.

The story in the segment mix is its higher-value businesses are showing signs of slowing down. If that continues in the fourth quarter and into 2023, this could be a sign of trouble for the company.

{kind=link}

Guidance for the fourth quarter points to the probability that overall revenue is likely to be flat or slightly down. Any unforeseen supply chain constraints will almost certainly lower the numbers.

In the third quarter the supply chain premium was $74 million. While that was down $17 million sequentially, for full-year 2022 it was up $48 million. The direction supply chain constraints or easing go will probably determine the momentum of the company through the first half of 2023 at least.

Conclusion

In the fourth quarter, I think the company should be able to maintain momentum. After that, we'll get a much clearer picture of the impact from supply chain challenges and how rising interest rates and possibly a worsening economy have the performance of the company.

Just with supply chain itself there's a strong chance it'll hold back the potential growth of the company in the first half of 2023, and possibly longer if the recession goes deeper and longer.

On a quant basis, the company is strong in all but profitability, with valuation, growth, momentum and EPS revisions all rated at a B- or better. Based upon my thesis that the company is going to face some pretty strong headwinds in the first half of 2023, along with tough comps, I think its quant ratings are likely to come down some.

With the company outperforming the sector in most metrics , including a FWD GAAP P/E of 14.36 and a FWD P/S of a low 0.32, it's still going to remain a market leader in the sector.

Even so, I think the company's share price may be a little hefty at this time when measured against the headwinds it faces now and in the near future. I don't think it's going to fall off a cliff, but it could drop some until there's more clarity concerning the impact of supply constraints and whether or not its higher-value segments can maintain growth momentum.

For further details see:

Benchmark Electronics: Higher-Value Segments Show Signs Of Slowing Down