BHE - Benchmark Electronics: Still Not In Buy Territory Post Q2 Earnings

2023-08-30 03:26:06 ET

Summary

- Benchmark Electronics' Q2 earnings beat normalized EPS estimates, but shares did not push on post the announcement.

- The company's earnings growth remains under pressure, despite positive operating cash flow for the first time in two years in Q2.

- Benchmark's leverage has increased significantly, leading to a low interest coverage ratio and a moderate outlook for profit growth.

Intro

We wrote about Benchmark Electronics, Inc. ( BHE ) back in June post the company's first-quarter numbers. Despite the very attractive valuation on offer in Benchmark at the time, we maintained our 'Hold' rating in the stock due to continued weakness in the semi-cap market and an elevated inventory position on the balance sheet, adversely affecting positive cash flow generation.

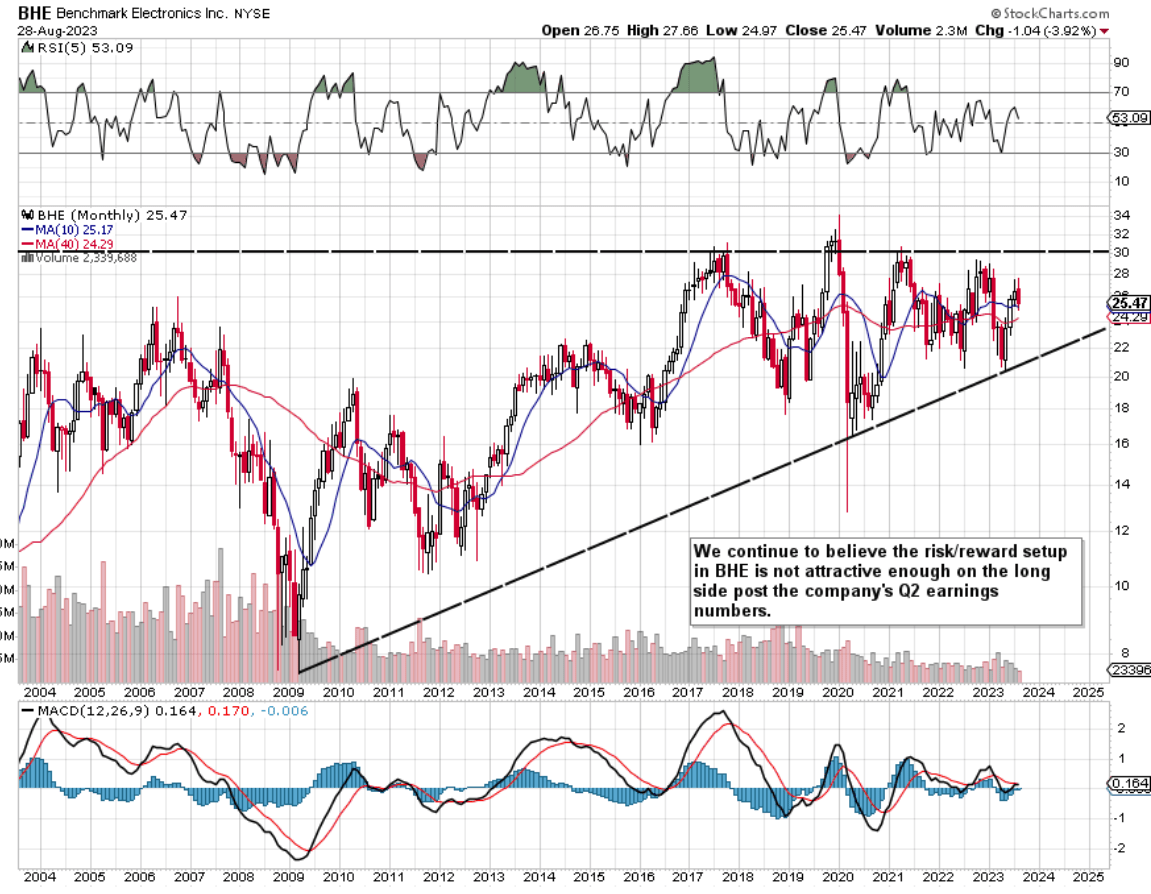

Although Benchmark Q2 GAAP earnings of $0.39 per share were in line with consensus and sales of $733+ million easily beating the top-line estimate, shares have failed to push on post the earnings announcement at the end of July. In fact, shares are only up just over 2% or $0.50 per share since we penned our most recent piece in early June. Suffice it to say, although BHE remains in a long-term bull market as we see below (through the stock's pattern of higher lows), shares have yet to take out significant overhead resistance of approximately $29 a share. Therefore, we are reiterating our 'Hold' rating in BHE as we believe consolidation will most likely continue for some time to come here.

{kind=link}

Q2 Earnings

Although the $733+ million top-line number for Q2 beat estimates handily as mentioned earlier, sales were most or less flat compared to the same period of 12 months prior. Furthermore, net profit of approximately $14 million was down by over $3 million (Where restructuring costs took their toll) compared to the second quarter of fiscal 2022. Suffice it to say, Benchmark's earnings growth remains under pressure despite the fact that the company finally printed a positive operating cash-flow print in Q2 (+$24.5 million) for the first time in two years.

Therefore with $8.7 million being put to use for capex spending in the quarter, free cash flow amounted to +$15.8 million in Q2 this year. Although this may look like a change of trend on the surface with respect to profitability , management took out more debt in the quarter with long-term debt now surpassing $424 million on Benchmark's balance sheet. So, if we really want to get into comparables, we can say that long-term debt has increased by $162 million or 62% over the same period of 12 months prior.

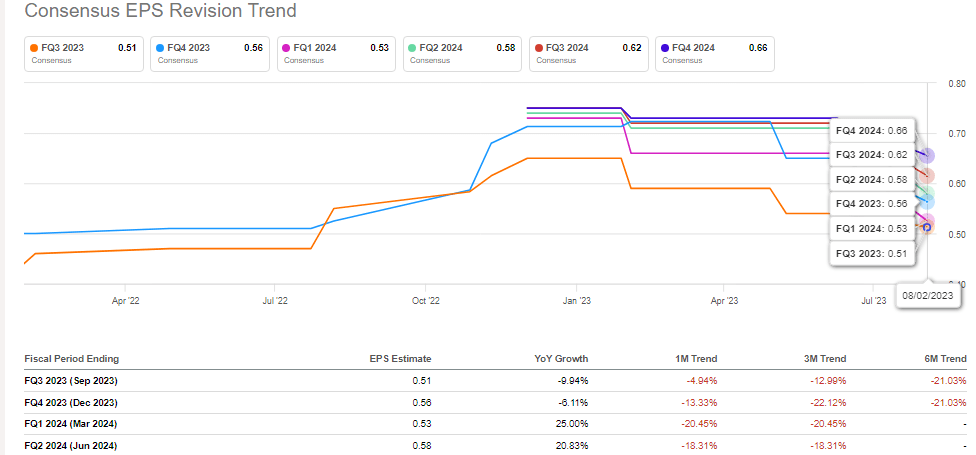

This in anyone's language has been a sizable increase and when we look at what consensus is expecting (with respect to forward-looking earnings growth), the growth in the company's leverage has been understandable. As we see below, sequential bottom-line growth (on average) is still expected of Benchmark going forward but revisions continue to get dialed down. Therefore, with inventory levels remaining stubbornly high and with a broader market recovery in the semi-cap space being continually pushed out over time, management does not want a cash crunch to develop; hence, the need for more leverage.

Benchmark Electronics Consensus EPS Revisions (Seeking Alpha)

{kind=link}

Leverage though as we know is a double-edged sword. To this point, Benchmark's interest coverage ratio in Q2 came in at a very low 3.34 where interest expense jumped to $8.3 million as a consequence of that extra balance sheet debt.

Moderate Outlook

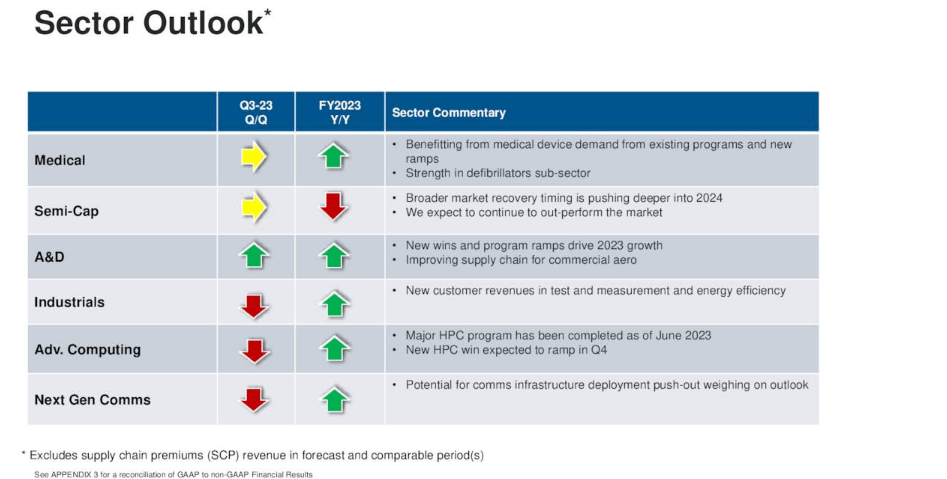

Now, when we look at Benchmark's six sectors (from a forward-looking demand perspective), we see that management is expecting growth in the 5 areas it sells into. However, when supply chain premiums are taken into account, we see that the bottom-line estimate for Benchmark for fiscal 2023 is just under the $2 per share mark (which would be a 5%+ bottom-line decrease over fiscal 2022 if realized). Top-line growth is one thing but if this growth is not transferring over to profit growth, the market may remain disinterested.

Furthermore, look at how three of Benchmark sectors (Industrials, Adv Computing & Next Gen Comms) are expected to perform over the near term (Specifically the third quarter). Sustained weakness in these areas as well as further stagflation in the Semi-Cap space will only put more pressure on the likes of Medical to keep the momentum going.

{kind=link}

Conclusion

To sum up, although Benchmark Electronics met the Q2 GAAP earnings estimate of $0.39 per share, recent trends point to the company's profitability remaining under pressure over upcoming quarters. There is no need to put capital to work here for the time being. We look forward to continued coverage.

For further details see:

Benchmark Electronics: Still Not In Buy Territory Post Q2 Earnings