BHE - Benchmark Electronics: Supply Chain Improvements Needed To Drive Cash Flow Generation

2023-06-13 05:06:14 ET

Summary

- Benchmark Electronics' valuation remains strong, with earnings, sales, and assets trading at significant discounts compared to the sector average.

- Q1 earnings showed growth in 70% of the company's portfolio, with medical and industrial segments expected to maintain double-digit growth in Q2.

- However, high inventory levels and negative cash flow generation have led to increased long-term debt, making it advisable to wait for Q2 earnings before investing.

Intro

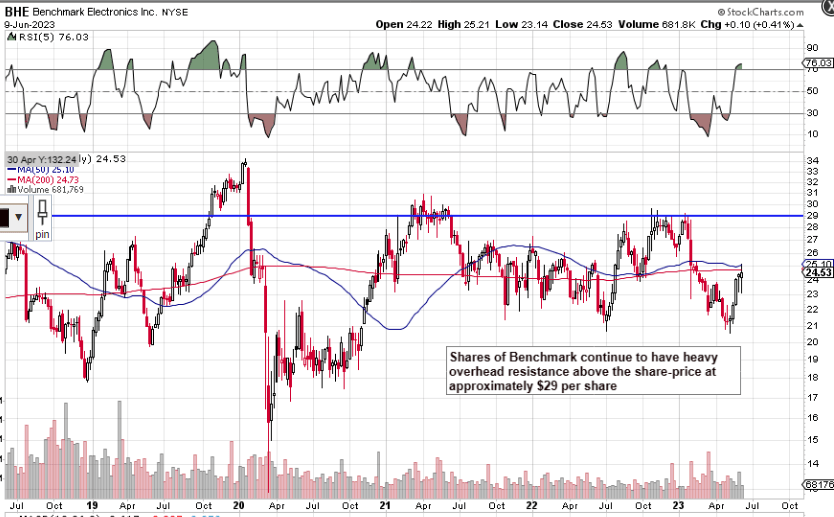

We wrote about Benchmark Electronics, Inc. ( BHE ) in August of last year when we were looking to put capital to work on a pending technical breakout. Earnings power at the time in BHE was accelerating which led us to believe that a breakout above overhead resistance was on the cards. As we see below, however, shares of Benchmark could not find the necessary momentum to punch above that $29 level with authority. This has resulted in the stock dropping close to 10% over the past 9+ months or so. Given, the S&P returned almost 8%, this is a sizable opportunity cost so we were fortunate that we did not buy the stock at that time irrespective of Benchmark's fundamentals which still continue to show underlying strength.

{kind=link}

The strongest calling card in Benchmark for us remains the valuation. In fact, across multiple valuation metrics, we can see that Benchmark's earnings, sales & assets are all trading for pennies on the dollar and at significant discounts to the sector in general. Furthermore, management continues to pay a dividend which currently equates to a forward yield of approximately 2.64%.

| Multiple |

| Benchmark Electronics |

| Sector Average |

| Price/Earnings |

| 12.58 |

| 25.15 |

| Price/Sales |

| 0.31 |

| 2.73 |

| Price/Book |

| 0.84 |

| 3.06 |

However, the Achilles heel of 'value investing' has always been the ability to time a respective investment. Although there were plenty of encouraging trends in the company's recent Q1 earnings report (which subsequently led to a sustained rally in the share price), we still maintain the 'timing' is off here with respect to putting money to work on the long side from a long-term perspective.

Q1 Earnings

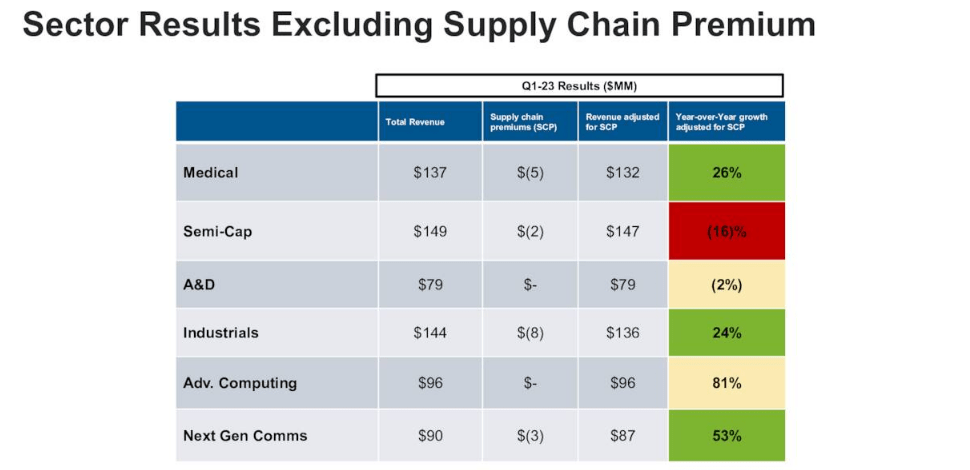

Although GAAP earnings of $0.35 missed the consensus estimate by a small margin, sales of almost $695 million beat consensus and also grew 9% over the same quarter of 12 months prior. Furthermore, company growth as we see below came from a number of sectors with only the 'Semi-cap' & 'A&D' segments reporting negative growth in the quarter. Suffice it to say, 70% of Benchmark's portfolio grew in the quarter which gives the company plenty of diversification in a difficult macro environment. 'Medical' as well as the 'Industrial' segment is expected to grow at a similar double-digit clip in Q2 and A&D is expected to go from a 2% negative growth rate in Q1 to positive growth in Q2. In fact, all segments barring the 'Semi Cap' are expected to remain firm despite the risk of some lumpiness concerning growth from quarter to quarter.

Benchmark Q1 Segment Growth Excluding Supply-Chain Premium (Seeking Alpha)

{kind=link}

Furthermore, it is encouraging to see investment behind the 'Semi-Cap' segment remaining strong as this demonstrates management's continued confidence in the fundamentals in this space. The company back in March of this year opened up a purpose-built ' Precision Technology' facility to meet the expected demand in the 'Semi-Cap' space going forward.

Cash Flow Concerns

Due to difficult ongoing trading conditions, however, it will be interesting to see if Benchmark can continue to invest aggressively whilst also keeping its balance sheet in check. Benchmark did not generate positive operating cash flow in Q1 (-$24.9 million) which resulted in management increasing its long-term debt position to almost $400 million. Suffice it to say, to ensure profitability can stay as elevated as possible on the income statement, management has begun to undergo expense controls to ensure investment can continue to be done even in a downcycle (such as the 'Semi-Cap segment in recent times).

The main driver behind Benchmark's cash crunch is its inventory which continues to rise ($778.1 million at the end of Q1). Now, the CFO believes free cash flow will still come in at approximately +$80 million in fiscal 2023 but a significant amount of inventory will need to be moved for this estimate to come to pass. Suffice it to say, companies which aim for sustained investment alongside aggressive cost-cutting can be difficult to achieve especially if trading conditions do not cooperate. This is why we recommend standing pat here at least until Benchmark's Q2 earnings numbers

Conclusion

To sum up, although Benchmark Electronics had plenty of segments that grew by strong double-digit percentages in Q1, high inventory levels and negative cash flow generation have led to the company drawing down more debt on the balance sheet. Let's see what Q2 brings. We look forward to continued coverage.

For further details see:

Benchmark Electronics: Supply Chain Improvements Needed To Drive Cash Flow Generation