BSY - Bentley Systems: Strong Infrastructure Investment And AI Solution Demand Boosting Growth

2023-12-13 09:38:14 ET

Summary

- BSY has shown robust financial performance, with growing revenue and levered free cash flows, and a decreasing debt/equity ratio.

- BSY's partnership with BP and acquisition of Blyncsy are set to strengthen its market position and enhance its capabilities in the AI segment.

- Strong demand in infrastructure investment and engineering resource gap will bolster BSY's growth outlook.

- In terms of comparable valuation, BSY outperformed competitors in terms of net income margin, and its current forward EV/Sales are in line with historical trends.

Synopsis

Bentley Systems (BSY) is a technology company that specialize in infrastructure engineering software solutions, offering a variety of services including cloud infrastructure, artificial intelligence, and digital twin technology to enhance the efficiency and productivity of engineering and construction projects.

In this post, I am recommending a buy rating for BSY. My rating recommendation is driven by a few factors. Firstly, its past and 3Q23 financial results have been very robust. Revenue and levered free cash flows are growing, while the debt/equity ratio is decreasing. In addition, BP's partnership with BSY has demonstrated the trustworthiness and strength of its software solution, and I believe this will further strengthen BSY's market position. Lastly, AI has been identified as a key solution for the engineering resource gap, and BSY's acquisition of Blyncsy will bolster its strength in the AI segment.

Assessing Past Financial Performance: How Did It Fare?

BSY's historical revenue growth has been very robust. Since 2019, it has been growing and accelerated until 2021 to approximately 20.4%. In 2022, although it did slow down to about 14%, it was still above its 5-year revenue CAGR of approximately 9.7%. On an absolute basis, it's clear that BSY's revenue has been consistently growing since 2018. For 2023 and 2024, the market expects BSY to continue growing as well. Overall, BSY's revenue trend is looking very strong.

{kind=link}

In terms of BSY's levered free cash flow [LFCF] growth, it is also looking very strong. In 2018, it was zero, but within a short span of four years, it has grown to approximately $230 million. For its trailing twelve months [TTM], it has already accumulated approximately $325 million. Additionally, BSY's four-year median LFCF margin is around 25%, significantly higher than the sector median of 8.24%. In fact, it is about three times higher than the sector median, which is very encouraging. For each dollar of revenue, BSY is able to generate better returns for equity holders.

Author's Chart Seeking Alpha

Moving onto its debt, at first glance, it might seem worrisome. In 2021, there was a spike in the debt level, primarily due to the acquisition of Seequent in March of that year. Following that acquisition, the debt-to-equity [D/E] ratio has gradually decreased, with the TTM at approximately 235%. Although the D/E ratio is quite high, the net interest expense as a percentage of revenue is, in fact, negligible and is on a downward trend. Therefore, I do not expect interest to significantly erode its net income margin.

Author's Chart Author's Chart

Analysis Of BSY's 3Q23 Earnings Results

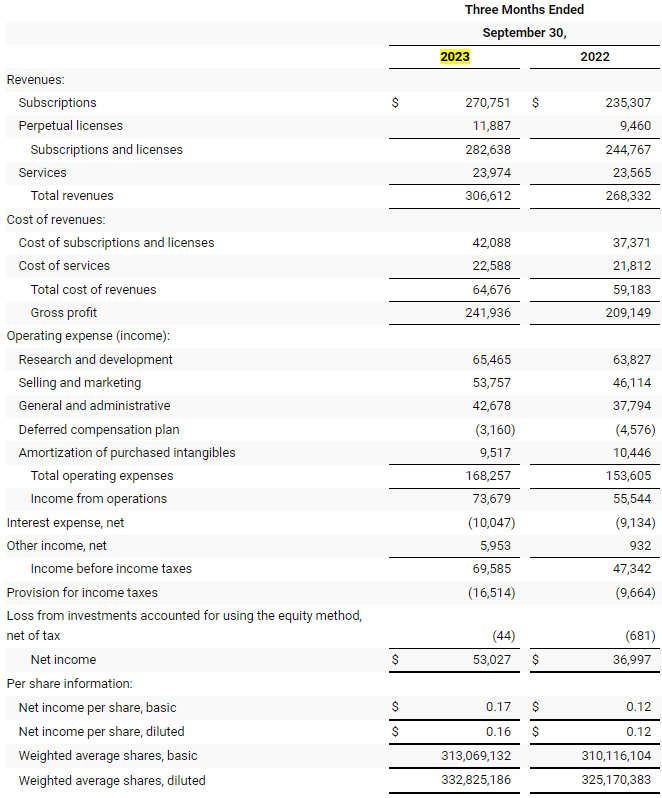

In my opinion, BSY reported strong 3Q23 financial results. In this quarter, total revenue grew by 14.3% year-over-year to approximately $306 million, up from 3Q22's approximately $268 million. Its revenue can be broken down into three segments: Subscription, Perpetual Licenses, and Services. Of these three, Subscription revenue forms the lion's share at approximately 88%, and this segment grew strongly by 15.1% year-over-year to approximately $270 million.

Another key metric I looked at is the annualized recurring revenue [ARR], which grew by 12.5% year-over-year. Solid ARR growth represents strong customer retention and loyalty. Such growth suggests that customers find value in BSY's offerings and are willing to continue paying for them over time, indicating the strength of the product. To further complement this, its net retention rate [NRR] was 110%. NRR measures the impact of upsells, cross-sells, downgrades, and churn. With NRR at 110%, it indicates that its revenue from existing customers is growing, which is also an indicator of strong product demand and strength.

In terms of profitability, BSY managed to grow its gross profit, operating income, and net income margins. The most notable improvements were in its operating and net income margins. In the quarter, the operating income margin improved from approximately 20% to about 24%, while the net income margin increased from around 14% to approximately 17%. Overall, it's encouraging to see that management is living up to their word regarding margin and cash flow improvements. Quote : "We are likewise steadily tracking to our planned annual gains in operating margins and cash flows".

Author's Chart BSY's Investor Relations

{kind=link}

{kind=link}

Boosting BSY's Growth Outlook Through BP Deployment Of BSY's Infrastructure Cloud

In early November 2023, BP plc (BP), reported that it had partnered with BSY for its infrastructure cloud services. This partnership includes BSY's AssetWise Reliability and AssetWise Asset Lifecycle Information Management solutions [ALIM]. These will be used to manage BP's project and operations engineering information, ensuring global asset integrity management.

In 2019, BP implemented ALIM as a Central Information Store [CIS] for certain projects with specific restrictions. Now, BP's projects, production, and manufacturing assets will be standardized with ALIM throughout. This standardization ensures smoother data migration, efficient workflows, and improved facilitation of BP's projects and operations.

By using AssetWise Reliability, BP will be able to enhance safety and risk management, increase availability, reduce maintenance costs, and fully optimize inspections. Originally, this implementation was only in the North Sea. This initial success has led to BP's commitment to rolling it out across 8 locations.

The net infrastructure value of this oil and gas supermajor is approximately $106 billion , ranking it at No. 33 under Bentley Infrastructure's top 500 owners. The expansion of BSY's suite of infrastructure solutions deepens its strong partnership with BP as BSY integrates its standardized solutions across BP's projects and operations. This reflects the trust and reliability placed in BSY's solutions by one of the oil and gas supermajors, thereby strengthening BSY's position in the infrastructure engineering software market.

Acquisition Of Blyncsy To Integrate Transformative Operations With AI

Blyncsy is an intelligent infrastructure solution provider that supports the day-to-day operations of transportation departments. This acquisition is an effort by BSY to widen its artificial intelligence [AI] services and boost BSY's iTwin Venture portfolio. BSY's iTwin Platform provides access to a large-scale dataset for visualization and insights into infrastructure assets, modeling high-grade 3D models through digital imagery and drone surveying. As mutually agreed in the acquisition deal, Blyncsy will implement the iTwin Platform, and BSY's iTwin will integrate Blyncsy's AI expertise into its digital twin ecosystem.

This will provide immersive visualization and insights for users, as Blyncsy has the technology to analyze imagery and identify issues in transportation networks. This enhances efficiency by reducing the need for costly and manual data mining. The key acquisition of an AI-powered transportation analytics firm is a strategic move to expand the iTwin Platform digital ecosystem and gain a competitive advantage in the rapidly growing AI market. It also forms a synergy that drives innovation in the infrastructure and construction technology industry.

AI As A Key Solution To Bridging The Infrastructure Investment Demand And Engineering Resource Gap

Based on the following chart , infrastructure demand has been accelerating since 2007 and the demand is expected to grow until 2037. This trend also ties with management's statement made during their Q&A session. Quote : "how much demand there is for infrastructure".

During the Q&A session, management also stated that there is a significant gap in engineering resource capacity, and this problem is on a global scale. One solution to fill this gap is to embrace and adopt digital technologies, especially technology with AI, as it increases the productivity and efficiency of engineers. Hence, it might be the solution to this gap.

I believe this complement very well with BSY's acquisition of Blyncsy, which I have discussed above. If the acquisition is successful, it will bolster the uptake of BSY's product offering by many engineering firms on a global scale.

{kind=link}

Comparable Valuation

BSY operates in the application software industry, specializing in software solutions. The three competitors I have listed below also operate in the same industry, and they provide software solutions as well.

In terms of market capitalization, which is a good proxy for company size, it's quite clear that BSY is larger than all of them. BSY has a market capitalization of approximately $15.880 billion, while the median market capitalization of its competitors is around $8.430 billion. In terms of size, BSY is 1.88x larger than them.

As a result of BSY's larger size, its forward revenue growth of 12.35% is lower than the competitors' median of 19.36%. I don't see this as a disadvantage, as larger companies tend to grow slower. Additionally, despite being 1.88x bigger, its growth is not significantly lagging behind its competitors.

On top of that, its gross margin of 78.92% is in line with the competitors' median of 78.98%. When it comes to net income margin, BSY clearly outshines its competitors. BSY's net income margin is 14.35%, while the median for its competitors is negative 12.57%.

Given its size, BSY's double-digit growth rate is still very commendable. Additionally, its net income margin is positive. Combining this with the strength and growth drivers of BSY I have discussed above, I believe its current forward EV/Sales of 14.17x is fair. Furthermore, its current forward EV/Sales is in line with its 5-year historical average, hence removing the possibility of overvaluation. The reason EV/Sales is used is due to its competitors' negative net income margins, which render P/E irrelevant.

The market revenue estimate for BSY is expected to reach $1.23 billion in 2023 and $1.37 billion in 2024. Given the growth outlook and financial strength of BSY discussed above, I believe these estimates are reliable. By applying its current EV/Sales to its 2024 revenue estimates, my 2024 price target is $56.87, representing an upside potential of approximately 12%. Additionally, my estimates are slightly lower than Wall Street's estimate, suggesting that my assumptions and estimations are quite conservative and in line with market's expectations.

Author's Valuation Seeking Alpha Seeking Alpha Seeking Alpha

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Risk Factor

Based on the chart I have compiled in relation to BSY's competitors, it's clear that BSY's D/E ratio is significantly higher than theirs. In the current uncertain inflationary environment, predicting the movement of interest rates is challenging. If interest rates start to rise, it will increase BSY's interest expenses, potentially contracting its net margins. In my valuation section, my argument for its EV/Sales is based on its superior net income margins. Should BSY's net income margin contract, its multiple might be under pressure, given that the general market credits its margins, not its growth, which is below the competitors' median.

Author's Chart

Conclusion

In conclusion, I am recommending a buy rating for BSY as my comparable valuation model suggests an upside potential of approximately 12%. When compared to its competitors, it clearly outperforms them in terms of net income margin but lags slightly behind in forward revenue growth. I attribute this lower growth to its size, as it is 1.88x larger than the median of its competitors.

When I dove deeper into its past and 3Q23 financial results, they showed a strong revenue and LFCF growth trend. On top of that, the D/E ratio has been decreasing. Overall, BSY's P&L and balance sheets look really healthy. Although it has a high D/E ratio, its net interest expense is actually quite low, hence posing no significant risk to its margins or liquidity.

Moving on, BP's partnership with BSY is expected to not just strengthen its growth outlook but also its position in the market, as BP is one of the biggest oil companies in the world. In addition, I believe BSY's acquisition of Blyncsy is a great move as it gives them access to the power of AI. Management stated that the current global engineering resource gap is driving demand for AI solutions. I believe this acquisition might open up new avenues for future growth.

For further details see:

Bentley Systems: Strong Infrastructure Investment And AI Solution Demand Boosting Growth