SFTBY - Berkshire Grey: This Go-Private Transaction Makes Sense

2023-03-28 12:36:04 ET

Summary

- Shares of Berkshire Grey roared higher, closing up after news broke that the company had agreed to sell itself to SoftBank Group.

- The all-cash transaction may make a lot of investors in the business unhappy, but it's a wise move in my view.

- Despite a history of strong sales growth and a sizable market opportunity, Berkshire Grey has a history of profit and cash flow issues.

March 27th proved to be a rather big day for shareholders of Berkshire Grey ( BGRY ). Although many investors are likely unhappy at this time, those who bought in on the cheap are almost certainly rejoicing. This is because shares of the company, while still trading significantly below their 52-week high mark, closed up 20.2% after news broke that the business had agreed to be acquired by SoftBank Group ( SFTBY ) ( SFTBF ) in a go-private transaction valuing it at about $375 million. There almost certainly exists a large portion of shareholders in the company who are unhappy with this development, likely because they believe that the deal materially undervalues the business. While I understand the sentiment, I believe that, on the whole, this development is a positive for investors and should be viewed optimistically. It takes a highly speculative company that has a history of significant losses and cash outflows, and produces a guaranteed price at which investors are effectively cashing out. While this does eliminate further upside, I believe that the guaranteed payout is logical. This is not to say that I would recommend the stock from here. Based on the modest amount of upside that's left on the table, combined with how inherently risky Berkshire Grey is, I would say that now might be the time for investors to cash out.

A look at the deal

According to the press release issued by Berkshire Grey, the company has agreed to be absorbed by SoftBank Group in a deal valuing it at $1.40 per share, all of which will be payable in cash. This represents a roughly 24% premium over the closing price of the stock on March 24th, which was the last trading day prior to the date of the announcement. In all, it values the enterprise at $375 million and will remove it as a publicly traded company from the market. This will give SoftBank Group the ability to take the business, further grow it, and, hopefully, turn it profitable, with a significant amount of potential upside on the table if all goes well. But of course, it also shoulders them with the burden of the transaction and will likely require years of additional massive investments in order to make the company a truly viable operation.

For those who are not familiar with Berkshire Grey, a brief discussion of its operations is in order. The management team at the company describes the business as an IER, or Intelligent Enterprise Robotics, company that focuses on developing and selling AI-enabled robotic solutions that help with supply chain activities. In essence, the company is building robots that assist with e-commerce, retail, and other similar activities, with core functions including the picking of items in warehouses, the sorting of items, and the movement of items. The goal of the company seems to be to replace warehouses full of employees with warehouses full of automated machines that can perform the work instead.

Over the years, the company has established for itself a portfolio of 170 patents, with another 325 patents that are pending. Instead of just focusing on the machines themselves, the company also emphasizes the software side of things. The software in question touches on things like vision and scene understanding, motion planning, haptics and interference testing, intelligent placement, and more. As of early November of last year, the company boasted $104 million in backlog, with around $250 million of orders. Customers include major companies such as FedEx ( FDX ), Walmart ( WMT ), Target ( TGT ), and more. During the 2021 fiscal year, its largest customer was Target. That retailer comprised 32% of the company's revenue, with the top four largest customers making up 77% of sales.

This is a good thing for shareholders

Generally speaking, I am skeptical of mergers and acquisitions. Often, especially when you are making a deal during turbulent market conditions, I believe that the company that's selling out does not get enough of a return to justify the move. But this is not always the case. Sometimes, I think the deal makes perfect sense or may even be generous to the shareholders of the company that's selling out. Frankly, I believe that Berkshire Grey is an example of the latter scenario.

{kind=link}

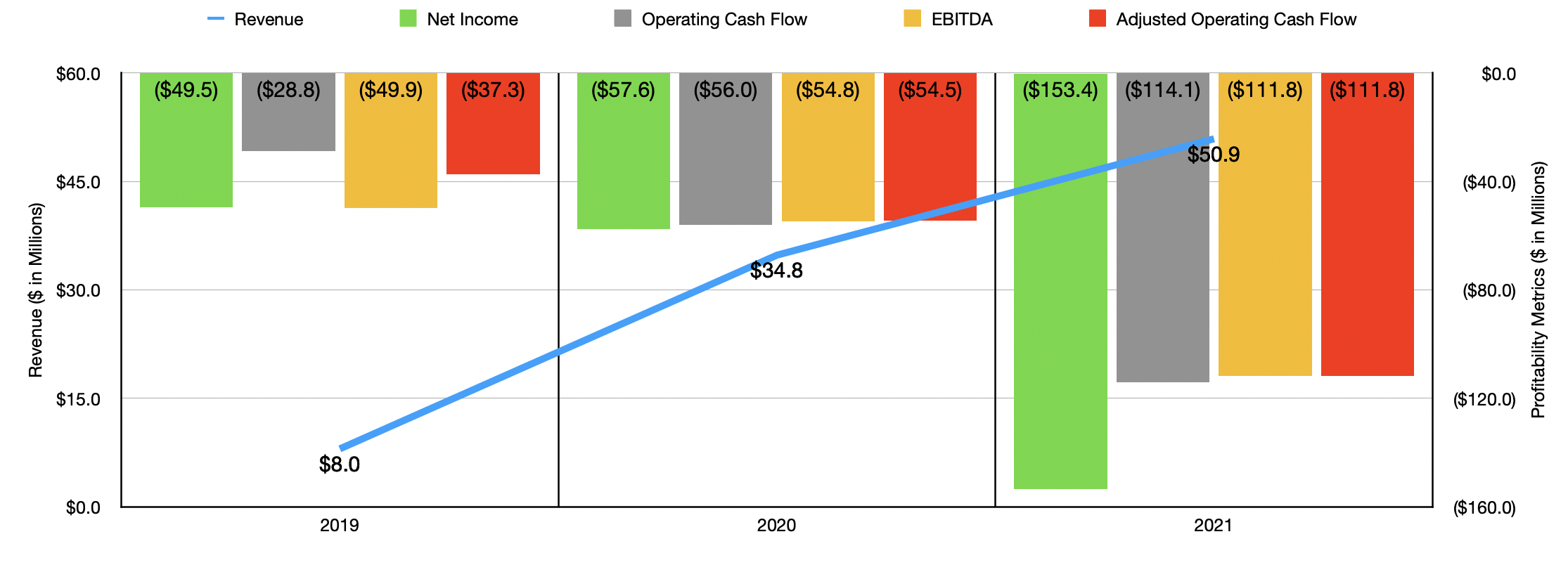

Looking at the fundamental data, growth-oriented investors might be perplexed about my statements. After all, Berkshire Grey has done well to grow itself over the past few years. The company went from generating revenue of only $8 million back in 2019 to generating revenue of $50.9 million in 2022. The surge in revenue from $34.8 million in 2020 to $50.9 million was driven largely by a rise in orders from its existing customers. Given the nature of the company, this is not a surprise. It has always historically exposed the firm to risk. But the fact that existing customers have largely stayed with it means that the company is doing something right.

This is not to say that everything has been great regarding the firm. Consider its bottom line results in recent years. Back in 2019, the company generated a net loss of $49.5 million. This loss ballooned to $153.4 million in 2021. Other profitability metrics looked very similar. Operating cash flow went from negative $28.8 million in 2019 to negative $114.1 million in 2021. If we adjust for changes in working capital, the picture doesn't look much different, with the metric turning from negative $37.3 million to negative $111.8 million. A similar trend can be seen when looking at EBITDA, which has gone from negative $49.9 million to negative $111.8 million.

{kind=link}

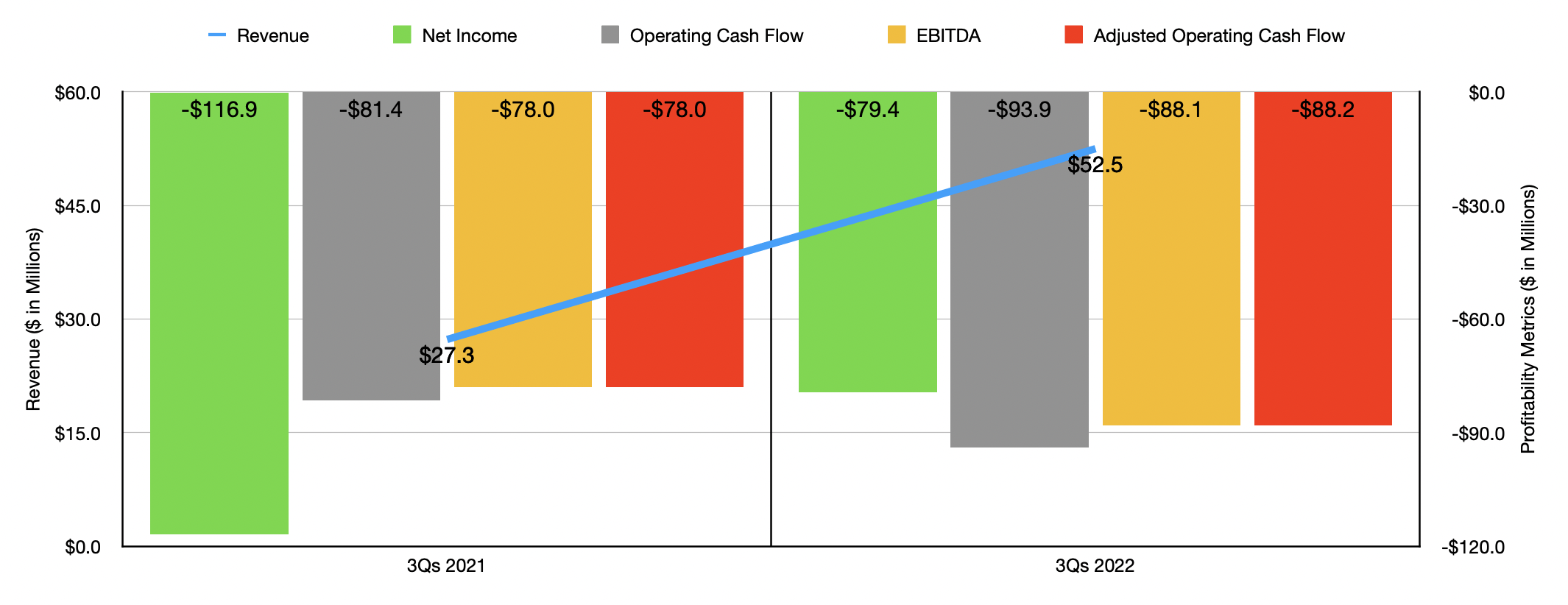

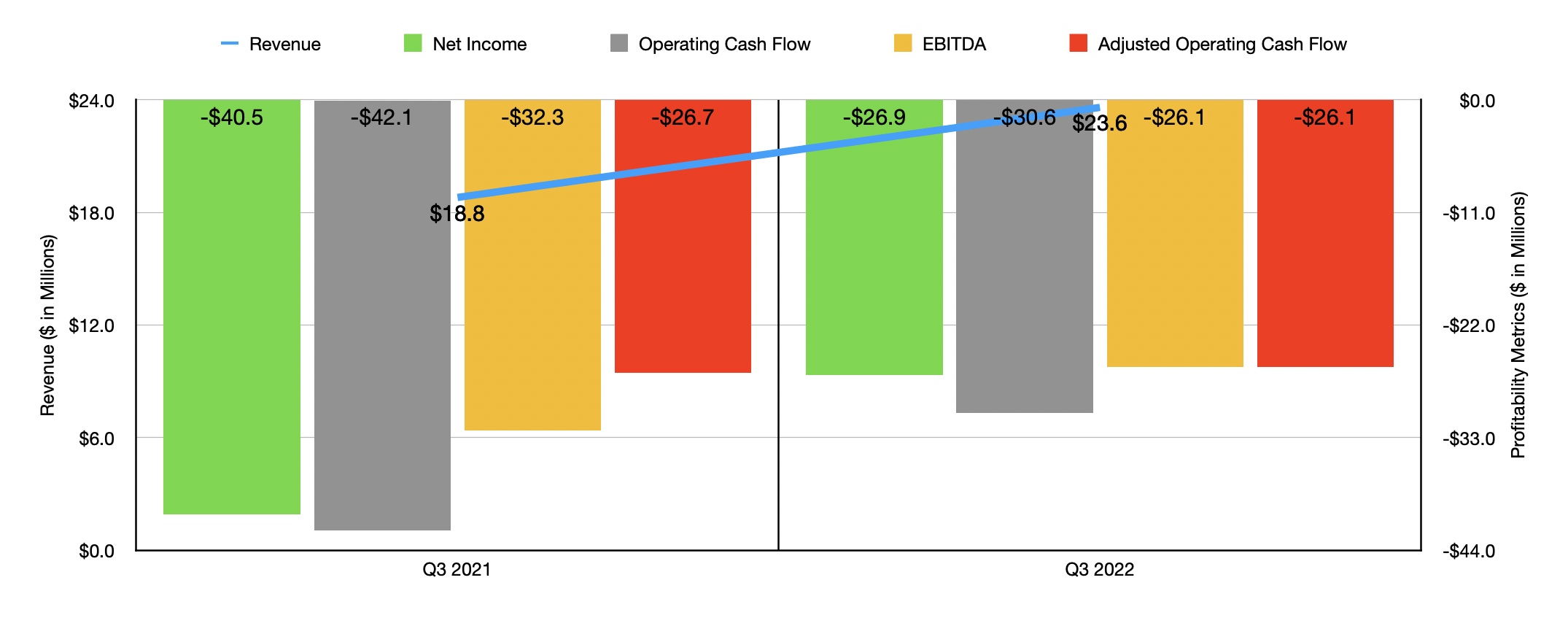

Where things really get interesting is when you look at the 2022 fiscal year. Growth for the company continued, with revenue in the first nine months hitting $52.5 million compared to the $27.3 million reported one year earlier. That's an increase of 92.3%. In addition to this, the company also managed to report an improvement in its bottom line. The net loss for the firm went from $116.9 million to $79.4 million. Though as the chart above illustrates, the cash flow data reported by management did worsen. But when you look at just the third quarter of the year, as shown below, you can see improvements on the bottom line across the board. A reduction in product and per-site deployment costs was instrumental in improving the company's gross profit margin. In addition to this, the firm saw its general and administrative costs improve drastically. For the third quarter of the year alone, these costs came out to only about 8% of sales. This compares to the roughly 44% of sales they accounted for one year earlier. The biggest contributor to this improvement, however, was a reduction in stock-based compensation, so it was non-cash in nature. At the same time, other costs for the business declined relative to revenue as well. Most notably, these were research and development expenses, and sales and marketing costs.

{kind=link}

Although it's great to see the bottom line for the company show signs of improvement, I don't believe that there is a realistic scenario where the company would have been worth more than what it agreed to be bought out for. In the table below, you can see a hypothetical range of trading multiples for the price to operating cash flow multiple and the EV to EBITDA multiple, with a low point of 10 and a high point of 30. You can see the amount of operating cash flow and EBITDA that the company would need to generate in order to be worth each of those multiples. Given the rapid growth that the company has seen, a multiple near the high end of this scale probably would not be unrealistic. But even in that case, the amount of cash flow that would need to be generated compared to the tremendous outflows seen for much of 2022 is a bridge too far in my opinion. This is especially true when you consider that the company is already showing signs of slowing growth. According to management, revenue for 2022 as a whole likely would have come in at between $65 million and $70 million. At the midpoint, that would be 32.6% higher than what was seen in 2021. By comparison, revenue growth from 2020 to 2021 was 46.3%, down from the 135% experienced from 2019 to 2020.

{kind=link}

Those who are unhappy with this transaction will point out that the market opportunity that the company is playing in is massive. This is undeniably true. It is clear that the primary focus of the business is on e-commerce. That market was estimated to be worth $3.5 trillion in 2019. By 2026, it's forecasted to grow to $7.5 trillion, which translates to an 11.5% annualized growth rate. But the market niche that Berkshire Grey operates in specifically can be broken up into two much smaller fragments. The first, and larger, of the two is the warehouse labor market. According to management, this space is worth about $230 billion. The second fragment is the automated material handling space, which is worth around $56 billion.

As e-commerce grows, both of these are slated to expand as well. But this is not an easy market to play in. Not only will the company have to compete with other players, it will also need to compete with firms that might be its customers. Take Amazon ( AMZN ) as an example. Over a decade ago, the e-commerce giant acquired Kiva Systems, a producer of warehouse robots, for $775 million. Much more recently, in September of last year, the company announced the purchase of Cloostermans, a Belgian company that produces technology dedicated to the warehouse space. The terms of that deal were not disclosed. In order to cut down on costs, and make sure their needs are met in the most efficient way possible, other companies are likely to follow this path instead of relying on third parties for their needs. This is not pure speculation. Walmart, for instance, has also moved in this direction. Last year, the company acquired Alert Innovation, a company dedicated to developing fully autonomous bots that store, retrieve, and dispense orders in warehouses.

Takeaway

From all that I can see, Berkshire Grey’s decision to sell itself makes a great deal of sense. Although the company was growing at a nice clip, profits and cash flows were still an issue. The company had cash on hand, and it had means of getting some additional cash. It also benefited from the fact that it had no debt on its books. But given the current economic environment, there's no guarantee that it could get to cash flow neutrality in the foreseeable future. Though some investors are likely disappointed given that shares of the company were trading as high as $3.72 in the past year, I see this as a wise maneuver aimed at removing future risks from the company's investors. Given the fact that upside from the $1.37 per share that the company is currently trading for and the $1.40 per share price at which the company has agreed to be bought out for it's so small, and given the fundamental health of the business as a standalone entity, I would not consider this to be a great prospect. In fact, I would go so far as to rate the business a ‘sell’ at this time to reflect my view that shares will probably underperform the broader market moving forward.

For further details see:

Berkshire Grey: This Go-Private Transaction Makes Sense