OXY - Berkshire Hathaway Q2'23 Earnings And Book Value Estimates - Where To From Here?

2023-07-13 14:35:06 ET

Summary

- Berkshire Hathaway has narrowed its underperformance to the S&P500 in Q2, largely due to the strength in Apple.

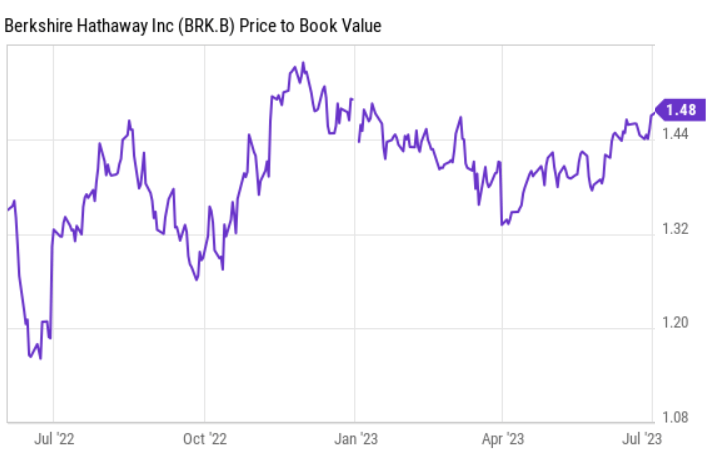

- Price/Book value at the end of Q2 was approximately 1.48x.

- Q2 operating earnings are expected to be around $10 billion, up 7.5% from last year.

- Berkshire's level of June repurchases should give a clue as to how Buffett feels about the current valuation.

After the 15% outperformance to the S&P500 in 2022 and lagging significantly after Q1, Berkshire Hathaway (BRK.A) (BRK.B) has narrowed its underperformance to the S&P500 to 6.5% in Q2.

The strength in Apple ( AAPL ) has a lot to do with this, as the majority of the market's gains this year have come from the rebound in big tech. Amazingly, ~90% of the S&P500's increase comes from the seven largest companies: Amazon ( AMZN ), Apple, Meta ( META ), Microsoft ( MSFT ), Nvidia ( NVDA ), Tesla ( TSLA ), and Alphabet ( GOOGL ). Viewed through this lens, Berkshire's performance, ex-Apple, has been on par with the bottom 493 companies in the S&P500.

Q2 Holdings Update

The value of Berkshire's investments in equity securities excluding Kraft Heinz ( KHC ) and Occidental ( OXY ) rose $37.5 billion, or 11.9% to $352.3 billion. Yet again, Apple ((AAPL)) was the big winner here.

Berkshire Top Holdings Q2 Valuation Change (Author)

From the $37.5 billion gain, after increasing the liability for future income taxes on the balance sheet as "income taxes, principally deferred" and subtracting 21%, we see a net book value gain of $29.6 billion for Q2.

Q2 Operating Earnings

Insurance underwriting will likely show ~$1 billion underwriting profit . The recovery at GEICO was faster than I expected in Q1, swinging from a $178 million loss in Q1-22 to a $703 million gain in Q1-23. Berkshire Primary and Reinsurance have also kept delivering underwriting profits in 2023. This almost certainly won't last, especially in this environment where float can generate 5% risk free, but let's enjoy it while we can!

Insurance investment income should come in around $ 2.5 billion , driven by higher short term interest rates and increased dividends. Higher rates as a tailwind is a nice change.

BNSF earnings should come in around $1.8 billion , a drop-off from the $2.2 billion in earnings from last year. In particular, Intermodal transport is down 17% year to date, likely due to a steep drop-off in trucking rates. When trucking rates are this inexpensive, a lot of loads can just be driven directly.

BHE should come in around $700 million, a bit down from last year. Berkshire Hathaway HomeServices will be the big drag year over year. Note, earnings from BHE have been particularly noisy lately. The big "miss" in Q1 here had to do with accruals related to the 2020 wildfires (likely this ruling against PacifiCorp) and not due to current operating performance. Further adjustments here could be expected.

Other Controlled Businesses containing dozens of companies like Precision Castparts, Lubrizol, Marmon, and other industrial businesses, now including Pilot , should be up year over year. Note this is not apples-to-apples and Pilot should add $250-300 million of this increase. The aviation and automotive businesses should be stronger, while Forest River should be weaker.

I'll estimate $ 3.5 billion in earnings from this group.

Non Controlled Businesses, defined as business where Berkshire has between a 20% and 50% ownership interest, which represents the interests in Occidental, Kraft-Heinz, and Berkadia. I'll estimate $500 million in earnings here , with Berkshire's larger OXY stake offsetting some of the weakness in results.

Other is now just a bucket for recording:

- Acquisition accounting expenses (-$202 million in Q1)

- Corporate interest expense before currency effects (-$64 million in Q1)

- Foreign currency exchange rate changes (-$17 million in Q1)

- "Other earnings", defined as Berkshire parent company investment income and corporate expenses, other intercompany interest income where the interest expense is included in earnings of the operating businesses and unallocated income taxes (+$172 million in Q1)

Since the dollar didn't move a lot during Q1, I'll estimate this group as flat.

In total, I expect Q2 operating earnings around $ 10 billion , up 7.5% from last years $9.3 billion.

Current Book Value

As reported in Berkshire's 2023 Q1 10-Q book value as of March 31, 2023 was $504.6 billion.

Adding the net gain of $29.6 billion from the equity investments to $10 billion in operating earnings, I project Q2-23 book value at $544.2 billion.

{kind=link}

Berkshire Price to Book Value (June 22-March 31 YCharts, April 1-June 30 Author estimates)

Berkshire's market cap as of June 30th was $745.9 billion. Dividing this by $504.6 billion yields a Price/Book Value of 1.48x for Q2.

2023 Outlook and Recommendations - Where to From Here?

Berks hire in 2023 is a microcosm of the market; its tech component is flying, while the industrial/financial/energy investments are flat to down. Without Apple, Berkshire might be flat this year after outperforming by 15% last year. I won't go too deep into Apple, as enough digital ink has been spilled over this topic already, but I believe its valuation is stretched, to put it mildly. It sports an earnings yield of a little over 3% with no growth (net income is down year over year, EPS is flat) with a business that is fully exposed to the consumer.

Berkshire itself is looking pricey again with a price/book at 1.48x, near the top of its recent historical range. The share price is at a 52-week high and only a few percentage points away from its all-time high. I don't believe Berkshire is in a bubble, but I'm not sure how much near term upside there is either.

I am very interested in seeing Berkshire's share repurchases for Q2, especially in June, as that will give a big clue on how Buffett and company think about the current share price.

I remain long, with a January 2024 $350 call still sold against my shares.

For further details see:

Berkshire Hathaway Q2'23 Earnings And Book Value Estimates - Where To From Here?