KHC - Berkshire Hathaway: Tempered Expectations

Summary

- FY22 operating earnings were good but were challenged by struggles at GEICO and the slowdown in consumer goods.

- The pace of share repurchases in 2022 dropped to $7.9 billion from 27.1 billion in 2021.

- Berkshire has fallen 5% in the last 6 weeks while Apple has risen 10%, bringing price/book down to the 1.38x level.

- My outlook for Berkshire's FY23 has results coming in around the same levels as FY22.

- The choice to add new investment money to Treasuries or Berkshire is a much harder decision now versus in the past.

Berkshire Hathaway ( BRK.A ) ( BRK.B ) just reported Q4 and full year results and released their annual report . It contained Buffett's usual wisdom, including this whopper of a quote regarding share repurchases:

When you are told that all repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, you are listening to either an economic illiterate or a silver-tongued demagogue (characters that are not mutually exclusive).

I'm happy that repurchases are still a focus, even though their pace slowed considerably this year. After spending my Saturday morning reading the Berkshire report, which has become a yearly tradition for me, here are my takeaways from Berkshire's 2022 and thoughts on the year ahead.

Q4 and Full Year Results

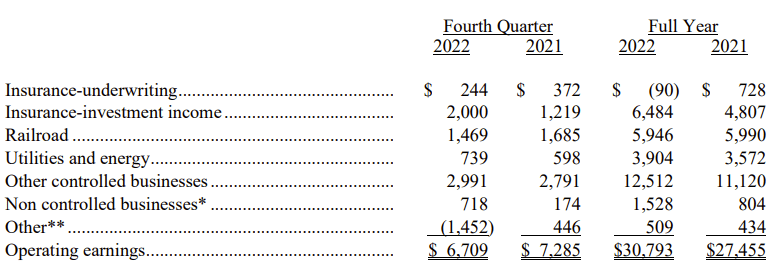

Q4 and 2022 results were a mixed bag. We can ignore the headlines about Q4 being down year over year as this was mainly driven by FX rates. But the full year operating results do show some challenges with the current environment, with many segments decelerating into the 2nd half of the year and Berkshire warning 2023 results will be lower.

{kind=link}

Insurance-underwriting is weaker than it appears. GEICO lost $1.9 billion in 2022 on higher claims. The segment showing an underwriting profit was due to Berkshire Hathaway Reinsurance having its first winning year since 2016, with a $1.4 billion dollar underwriting profit, almost entirely from Property/Casualty jumping $1.5 billion to a $2.2 billion underwriting gain. From 2017-2021, BH Reinsurance lost a cumulative $9.8 billion , so this was an unusually good year for the business.

Insurance-investment income is benefitting from both higher dividends and interest rates. Dividends increased 19%, just short of a $1 billion increase. Interest income jumped 186% to $1.7 billion from just $600 million last year. This will likely jump about ~$1.5 billion again in 2023 from higher interest rates.

Railroad was flat year over year. Volumes were down 5.8% driven primarily by consumer products being down 8.3%. Berkshire made up most of this volume loss through higher fuel surcharges.

This business was decelerating toward the end of the year, and the latest intermodal and carload report is down 9% so far in 2023.

Utilities and Energy was a bright spot, up 7.5% in total. The energy businesses themselves were up 14.6%, driven by strength in natural gas pipelines and Other Energy (a mix of businesses including renewables.) Overall results were dragged down by Berkshire Hathaway HomeServices (yes, this business is owned by BHE) which saw earnings drop from $387 million in 2021 to $100 just million in 2022.

Other Controlled Businesses which includes PCC, Lubrizol, IMC and many others, had a strong year, up 9.7%. This was mostly driven by the Manufacturing side (+13.6%) versus Service/Retail (+7%.)

Inside Manufacturing, building products (+41.3%) offset weakness in consumer products (-23%.) This strength in building products will likely be short lived, and Berkshire warns earnings will likely decline from current levels in 2023.

Consumer products was weak, and was only held up by RV maker Forest River. But this strength was almost entirely in the first half of the year, and Berkshire warns will also weaken in 2023.

Inside Service/Retail, Services, including the aviation businesses were strong (+14%) offsetting weakness in retail (-4.7%). Most of retail is BH Automotive, which was impacted by the automotive supply chain issues. We hopefully will see an improvement in Retail this year as the automotive industry recovers.

Non Controlled Business and Other is the category that includes equity method earnings and FX fluctuations from non-US denominated Berkshire debt. It was up 64% over last year, but in truth, this is not nearly as strong as it looks.

Of the $2 billion, $1.3 billion were FX gains. Also starting in Q4, Berkshire began to include Occidental's ( OXY ) earnings here, which added $258 million year over year.

Bright spots were Kraft Heinz ( KHC ) earnings (up $233 million) and Pilot (up $267 million.) Berkshire acquired an additional 41.4% interest in Pilot on January 31, 2023 and became the majority owner, so this will move spots into Controlled Businesses and we'll have more information on this business going forward.

FY23 Outlook

Normalizing for the difference in accounting treatment for Occidental, I expect FY23 results to be flat to down slightly from FY22.

On the positive, we'll see gains from the inclusion of Pilot and Alleghany, along with a ~$1.5 billion tailwind from interest rates.

For headwinds, FY22 results included a $1.26 billion FX gain. While the dollar may still go higher, I wouldn't include this as a base case. I also would not expect BH Reinsurance to repeat its 2022 performance. I do believe GEICO will improve, but the next few quarters might be rough. Overall, FY23 may show an underwriting loss.

Railroad will likely also show a decline in earnings through at least the first half of the year. Many of the other bright spots from FY22 will decrease in FY23 as discussed above. BH HomeServices could show a loss for the year.

I'd caution anyone trying to extrapolate the FY21 -> FY22 earnings growth into FY23 and thinking Berkshire will post $34-35 billion in Operating Earnings this year. I do not believe this will happen, and improving on FY22 results at all should be viewed as a win. This year we should temper our expectations as the inflationary environment is proving more challenging to Berkshire than I originally believed it would be.

Share Repurchases

In Q4, $2.6 billion was used to repurchase Berkshire shares, bringing the total for the year to ~$7.9 billion. This is a significant deceleration from 2021 when it repurchased $27.1 billion.

Berkshire Repurchases (TSOH Investment Research - used with permission)

Why the massive drop off? I can think of two reasons.

One, for much of the first half of last year, the stock just wasn't cheap.

Two, they did not have the available cash. At the end of September, Berkshire held $109 billion in cash, with the Alleghany purchase on tap. I know it sounds insane to claim a company with $100+ billion in cash "doesn't have enough" but it's true. Throughout its history, Berkshire has historically held a significant percentage of the float in cash and cash equivalents. I don't think this is changing either, as Buffett said the following in the 2022 Shareholder letter :

As for the future, Berkshire will always hold a boatload of cash and U.S. Treasury bills along with a wide array of businesses. We will also avoid behavior that could result in any uncomfortable cash needs at inconvenient times, including financial panics and unprecedented insurance losses. Our CEO will always be the Chief Risk Officer - a task it is irresponsible to delegate

I think the current risk of a financial panic is elevated. Maybe Buffett does, too.

I will be interested in seeing the repurchase behavior in Q1 of this year. Will Berkshire revert to a 2021 level of repurchases, or opt to earn 5% in treasuries with the ongoing cash flow?

My Hedge Call

In early January with shares at $318, I suggested that some investors may want to Hedge Berkshire stock , because I believed shares had become overheated and drifted above 1.5x book, a value it has not stayed at long in recent history.

I personally purchased a Jan24 $310 Put for $17, and a few days later sold a Jan24 $350 Call for $15. This past Friday, I sold the Put option for $22, leaving just the short call in place (which is now worth under $10.) While not a homerun trade, I think it ultimately was a pretty good call.

Berkshire indeed did not stay at that level very long. Despite Apple rallying 10% while the market was flat, Berkshire dropped 5%. My calculations for Price/Book now are at 1.38x versus 1.53x when I made the call. This was enough for me to sell the Puts, because ultimately, I want to continue owning Berkshire, and I want the time decay of options to work for me, not against me.

I will likely hold the call until expiration, because I'd be surprised if Berkshire rose above $360 (my current breakeven) by year end. At that level, I may consider selling it, tax consequences be darned.

Maybe I got lucky here, but I think my analysis was sound. If the broader market and Apple had dropped further, this trade would have been a home run.

Valuation always matters, even for Berkshire.

Conclusion - should investors allocate new money to Berkshire?

For years, Berkshire was an easy call to allocate money to for the "safe" portion of my portfolio - the portion that would have been occupied by governments bonds, if they yielded anything. I made this choice with eyes open, knowing I was sacrificing safety and that in a stress situation like 2020, Berkshire would still behave like a stock. I figured Berkshire would return 7%/year, versus 1% for intermediate term treasuries, so giving up 6% a year in return for the safety and optionality of holding treasuries was just too much for me to give up.

Right now, the choice is less clear. The one year treasury rate is above 5%, while Berkshire's "earnings yield" is around 4.5% and its free cash flow yield is less than that. Even giving 100% inclusion to the "look through" earnings of its equity book, Berkshire's earnings yield is in the mid 6% range since its major holdings like Coca-Cola ( KO ) and Apple ( AAPL ) also sport high PE ratios.

So while previously it was a "no brainer" to choose Berkshire over treasuries for many, right now the best choice really depends on the individual investor's situation - their risk tolerance, tax rates, time horizon, and how the current inflation personally impacts them. For investors that have fairly fixed expenses, and anyone with a fixed mortgage around 3%, the safety and optionality of 5% treasuries is appealing.

Whether it's more appealing than owning more Berkshire depends on the investor, but for now, I'm adding to treasuries and holding my Berkshire.

For further details see:

Berkshire Hathaway: Tempered Expectations