BRY - Berry Corporation: Q4 Should Benefit From A Full Quarter From Macpherson Assets

2023-11-24 04:32:30 ET

Summary

- Berry averaged 25,300 BOEPD in Q3 2023 production, along with generating $35 million in adjusted free cash flow.

- Berry's Macpherson acquisition may have contributed around 300 BOEPD in Q3 production with its mid-September close.

- Macpherson's production is expected to be 2,400 BOEPD in 2024, and this should meaningfully help Berry's Q4 2023 results as well.

- While Berry's operational performance has been good, the 2024 Brent strip has come down by $6 since I last looked at Berry.

Berry Corporation (BRY) reported solid Q3 2023 results , generating $35 million in adjusted free cash flow with its Macpherson acquisition only contributing a small amount during the quarter. The Macpherson acquisition closed in mid-September, so Berry's Q4 2023 results should involve increased free cash flow (compared to Q3 2023) and higher production despite Berry cutting back development spending at its legacy assets.

Berry's 2H 2023 results appear likely to be slightly better than I had previously anticipated . However, I am still trimming Berry's estimated value slightly (by around $0.25 per share) to a new range of $9.00 to $10.00 per share. This reflects weaker near-term Brent prices reducing Berry's projected free cash flow despite it having a substantial amount of hedges.

Q3 2023 Results

Berry reported 25,300 BOEPD (92% oil) in production during Q3 2023, which was 1% higher than its 1H 2023 production, although 2% lower than its Q2 2023 production. Berry only had $12 million in development capex in Q3 2023 (down from $21 million in Q2 2023) as it reduced activity to help pay for its Macpherson acquisition.

Berry's Q3 2023 results include a small amount of production from its Macpherson acquisition, which closed in mid-September . Without the Macpherson production, Berry's production would have been around 25,000 BOEPD instead.

I had previously modeled Berry's 2H 2023 production at 25,100 BOEPD based on its full-year guidance. Berry appears on track to end up a bit above that amount for the second half of the year. Berry's legacy production is likely to decline fairly substantially from the 25,000 BOEPD in Q3 2023 as Berry limits its development activities. This should be more than made up by a full quarter of production from the Macpherson assets, which are expected to produce 2,400 BOEPD in 2024, although current production was not disclosed.

The reduced capex budget allowed Berry to generate $35 million in adjusted free cash flow (after subtracting $9 million in fixed dividends) in Q3 2023. It also declared fixed and variable dividends totaling $0.21 per share related to the quarter.`

Berry's net operating expenses ended up at $28.20 per BOE in Q3 2023, which was slightly lower than I expected for the quarter. Berry appears capable of generating more than $35 million in adjusted free cash flow in Q4 2023 at current strip prices, excluding changes in working capital. This is helped by a full quarter of production from Macpherson.

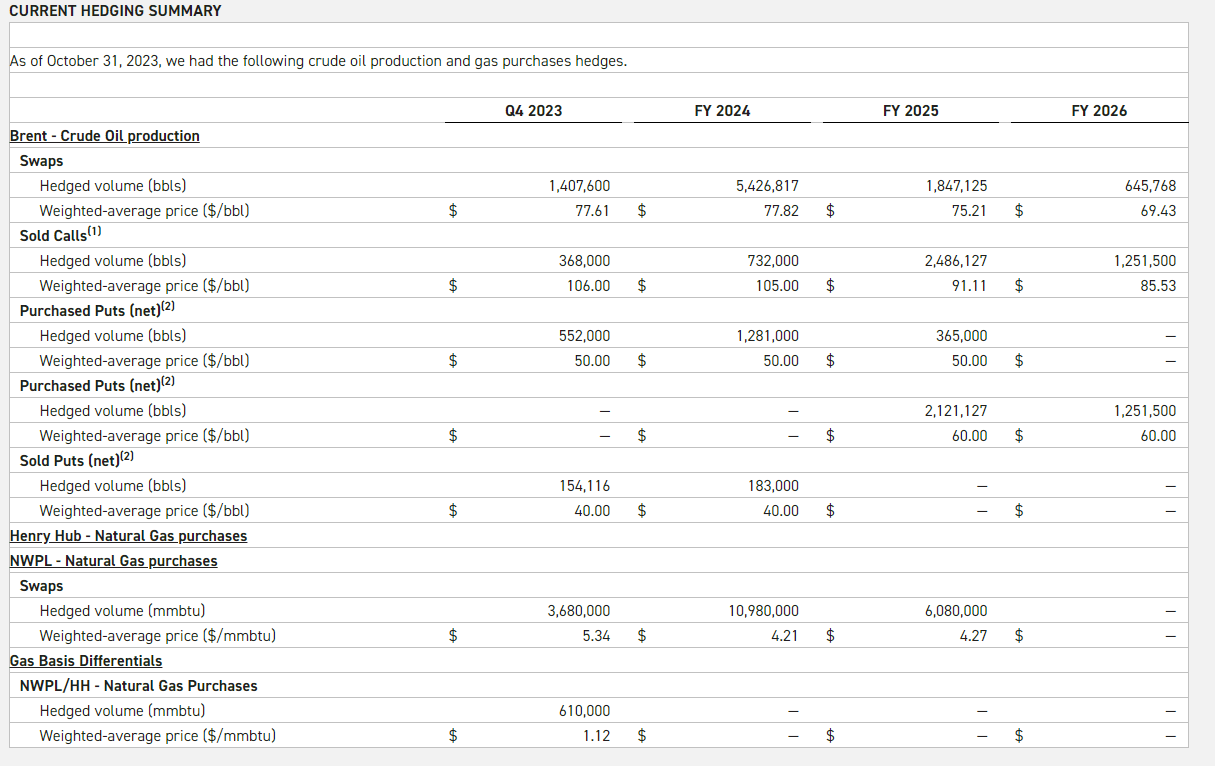

Adding Hedges

Berry has continued to add hedges. Since the end of July 2023, Berry added 2024 swaps covering 1.28 million barrels of oil at a Brent price of $83.30 per barrel. It also added 2025 swaps covering 1.095 million barrels of oil at $78.18 Brent and 2026 swaps covering 0.1585 million barrels of oil at $71.64 Brent. Berry also added 2026 collars covering another 0.779 million barrels of oil with a ceiling of $87.54 Brent and a floor of $60 Brent.

{kind=link}

At current strip these new hedges have around $4 million in positive value, while Berry's combined oil hedging position from 2024 to 2026 has around negative $24 million in value at current strip.

Berry has around 63% of its 2024 oil production (assuming flat production growth from 2H 2023 levels) hedged with swaps, but this goes down to 22% for 2025. Collars cover another 29% of Berry's 2025 oil production.

Estimated Value

My long-term estimate for Brent remains in the high-$70s ($78 to $79). The current 2024 strip for Brent is above that at approximately $81, but with backwardation the Brent strip declines to $77 in 2025 and down to $69.50 in 2028. The five-year average for Brent strip from 2024 to 2028 is a bit under $75.

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| Brent Strip |

| $81.00 |

| $77.00 |

| $74.00 |

| $71.50 |

| $69.50 |

Thus my long-term estimate is a few dollars above the current strip for the next five years.

When I last looked at Berry, near-term strip prices were a fair bit higher, with 2024 Brent strip being around $6 higher than now and 2025 and 2026 Brent strip being $3 to $4 higher than now.

Thus I am trimming my estimated value for Berry to $9.00 to $10.00 per share to reflect weaker near-term oil prices, despite hedges partially mitigating the impact of those weaker oil prices. I had previously assumed $87 Brent in 2024 and $78 to $79 Brent after 2024 when estimating Berry's value.

I have now moved to a flat $78 to $79 Brent price for my calculations, which is slightly below strip for 2024, but above strip after 2024.

Berry is performing fine operationally, but the $0.25 per share reduction in its estimated share price reflects the near-term impact of those lower oil prices on Berry's free cash flow. This is partially mitigated by Berry's production trending slightly higher than I had previously expected.

Conclusion

Berry has been performing decently operationally, with 2H 2023 production trending a bit higher than I had previously expected, while net operating expenses were slightly lower than modeled for Q3 2023. Berry generated $35 million in adjusted free cash flow in Q3 2023 and should be able to generate more than that in Q4 2023, excluding the impact of changes in working capital.

While there are operational positives for Berry, the weaker near-term Brent prices slightly lower its value despite my belief that longer-term Brent prices will still average in the high-$70s. As a result, I now estimate that Berry is worth $9 to $10 per share.

For further details see:

Berry Corporation: Q4 Should Benefit From A Full Quarter From Macpherson Assets