BERY - Berry Global: At 11% FCF Yield It Is A High Quality Bargain

2024-01-19 16:36:38 ET

Summary

- Berry Global is a turnaround story with a global leading position, resilient business model, and financial strength.

- The company has a diverse customer base and derives a significant portion of its sales from stable regions and businesses.

- Despite challenges such as declining volume and high input costs, Berry Global has managed to generate strong free cash flow and deploy capital effectively.

- My discounted cash flow analysis implies there is a 23% upside to be realized from the price of $65.15.

Investment Thesis

Berry Global ( BERY ) is a turnaround story. Over the past few years, the company has undergone a series of changes to its management and capital allocation strategy. The firm fits the bill for my investment philosophy due to its global leading position, resilient business model, and financial strength stemming from robust free cash flow generation and strong balance sheet.

Company Profile

BERY is a global provider of rigid products with 18,000 customers stemming from 38 countries. To name a few, McDonald's (MCD), P&G (PG), Coca-Cola (KO), L'Oreal (LRLCY), Johnson & Johnson (JNJ), and more. As you can see below, BERY serves developed and stable companies with predictable revenue streams. No customer constitute more than 5% of revenue and the top 10 customers only account for 15% of sales.

{kind=link}

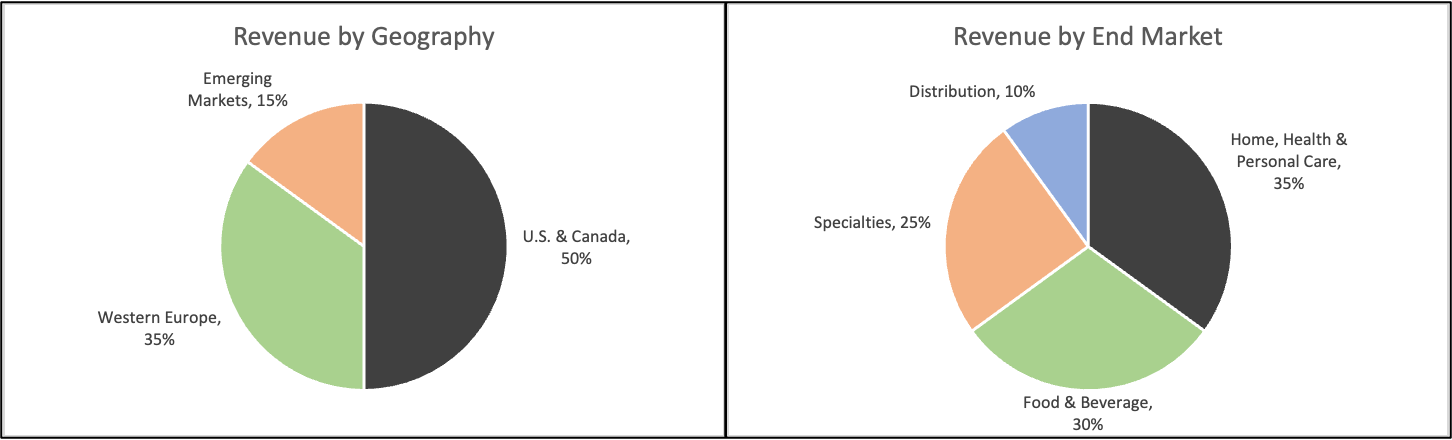

Not only is BERY does berry have a diversified customer base, but they are also well-diversified in terms of region and end markets. The company's exposure to emerging markets not only boosts future growth but can also offset any decline in developed regions such as Europe and North America.

{kind=link}

The Berry Global today is different from what it was five years ago. The firm had a poor capital allocation strategy, was highly leveraged, and was underperforming competitors in general. But a lot has changed since then, In February 2020, Canyon Capital which owned 7% of the company wrote a letter to BERY's management and in November 2021 another shareholder (Ancora Holdings) wrote another letter to the company.

Both letters pointed out that BERY was trading at a deep discount to peers, and to fix this management should start deleveraging the balance sheet, repurchase shares, sell some assets, and improve capital allocation as a whole (more on this later). In November of 2022, a capital allocation committee was formed and some changes to the board of directors have been implemented.

These changes include share buyback programs, initiating a dividend, and deleveraging the balance sheet. Additionally, Management appointed three new independent directors to the board.

Financial Strength

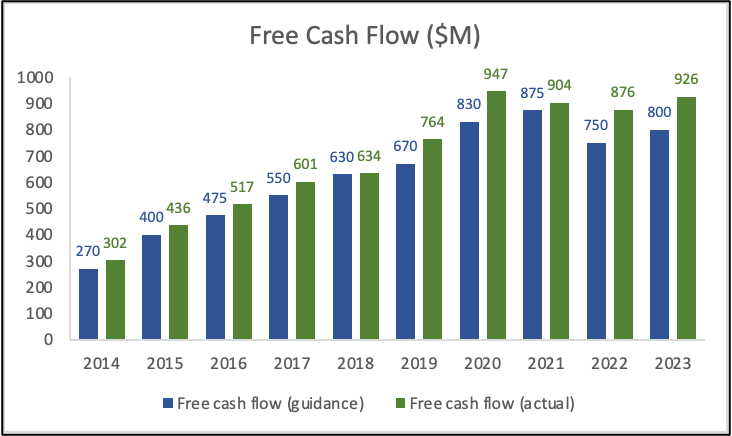

I believe BERY enjoys a strong financial position because of its strong cash flow generation and solid balance sheet. Aside from exceeding free cash flow guidance since 2014, BERY has been able to maintain a healthy FCF despite the volatility experienced in the past few years such as supply chain problems due to the pandemic and high input costs driven by inflation.

{kind=link}

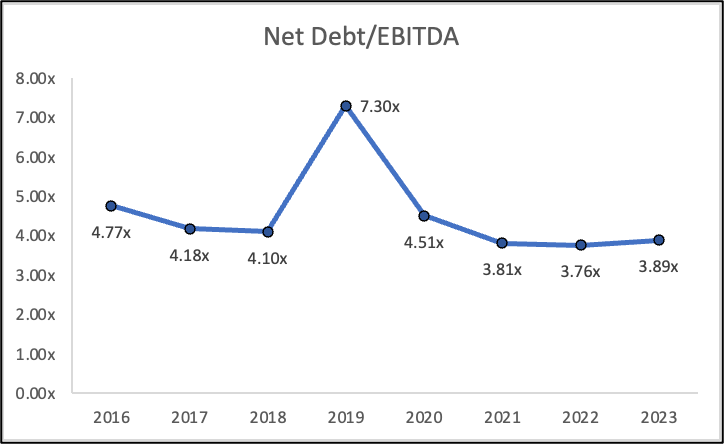

Even as volume declined and sales diminished by 13% in 2023, BERY managed to grow its free cash flow by 6%, which further proves the company's resiliency. As a result of the push from shareholders, the firm has modestly deleveraged the balance sheet, repurchased shares, and initiated a dividend.

{kind=link}

Moving on to the balance sheet, Looking at the company's working capital I can make an educated guess that the company has a low chance of running into liquidity issues because they are collecting cash from customers first before paying their suppliers. As you can see below, In 2023, it took Berry approximately 48 days to collect payment from customers and 59 days to pay suppliers.

These figures have improved over the past few years leading me to believe that management might have renegotiated its contracts. As the discrepancy grows large between the two, BERY can even use the cash collected to generate interest income. This could also help the company avoid running into any liquidity issues

{kind=link}

Recent Results

BERY recently wrapped up its fiscal year, and it was better than I expected. In FY2023 , sales decreased by 13%, primarily due to the pass-through of lower resin costs, a 6% volume decline, and an unfavorable $84 million impact from foreign currency changes. But despite lower revenue, the company was able to generate more free cash flow than last fiscal year (a 6% increase year over year).

Not only did FCF improve, but EBIT and EBITDA margins also experienced a jump of 60 and 150 bps, when excluding restructuring charges of course. The company allocated $728 million to shareholders while also paying back its debt. BERY repurchased nearly 8% of the shares outstanding for $601 million and paid a total of $127 million in dividends. Additionally, the firm recently increased its dividend by 10%.

All in all, I believe the company performed well despite the rising costs and currency impacts. The firm managed its finances pretty well; liquidity remained strong, cash was distributed to shareholders, and debt was reduced. Going forward, I believe BERY's robust free cash generation will continue to support its exemplary capital allocation strategy.

Valuation

As I'm writing this, the stock is sitting at $65.15. BERY is trading at a forward P/E of 8.65x the FY24 consensus of $7.62 and 7.76x the FY2025 consensus of $8.50. On a trailing free cash flow basis, the stock yields over 11.6% relative to its equity value.

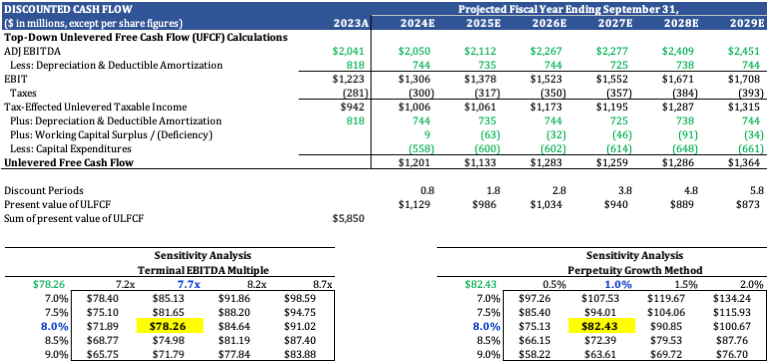

I used a discounted cash flow analysis to value Berry Global. Taking the average of both the exit and growth perpetuity methods, I arrived at an implied share price of $80.35. I assumed revenue would compound at an annual rate of 2.2% in line with inflation. I expect costs to normalize as they get passed on to consumers through price increases. I model COGS margin to stabilize around 80% and SG&A between 8 and 7% in the near future.

{kind=link}

I used a 1% growth rate for the perpetuity method because of the low growth in the industry and the 7.7x EV/EBITDA multiple, which is in line with the FWD and current multiple. I expect BERY to continue generating strong free cash flow and use it to pay down debt and reward shareholders.

Risks

Concerns that arise when considering investing in BERY are four, in my opinion. The first is for volume to continue to decline, which will lead to top-line pressure and perhaps free cash flow declines as well. The second is high input costs, given that BERY has a very thin margin business with a 15% EBITDA margin, 9.33% EBIT margin, and 18.24% gross margin. Thirdly is leverage; despite continued debt repayment, the balance sheet still carries a serious amount of debt, with approximately $6 billion maturing in 2026. Lastly, although diversification is a good thing, the company is exposed to currency fluctuations and that could lead to a few hits to sales as FY2023 proved.

Bottom line

The bottom line is that BERY is not a growth company; it is a consistent free cash flow-generating business with an improved capital allocation strategy. The company is also diversified in terms of customers and regions, which should offer some downside protection. My valuation implies a 23% return on the price of this writing ($65.15).

For further details see:

Berry Global: At 11% FCF Yield, It Is A High Quality Bargain