BERY - Berry Global: Changes In Capital Allocation Gives Hope To Shareholders

2023-09-15 07:41:55 ET

Summary

- Berry Global operates in the stable and countercyclical plastic packaging sector.

- The company has been trading at a chronic, well-deserved undervaluation compared to the sector due to shareholder-unfriendly capital allocation.

- Three activist funds have decided to change the course of BERY, and a turnaround situation seems feasible.

Investment Thesis

Berry Global (BERY) operates in a relatively stable sector that is typically resilient to economic crises. However, historically, it has suffered from chronic undervaluation compared to the multiples at which its peers and the sector as a whole trade. As a result, various activist funds have addressed letters to the board, seeking to unlock Berry's value and narrow this valuation gap.

After years of attempting to alter the company's trajectory, it appears that Berry Global is now taking activist funds' input into account. This could potentially trigger a turnaround in which the market begins to improve BERY's valuation. In this article, we will analyze if a fundamental change has really occurred in the company and assess whether the company's shares might present an investment opportunity.

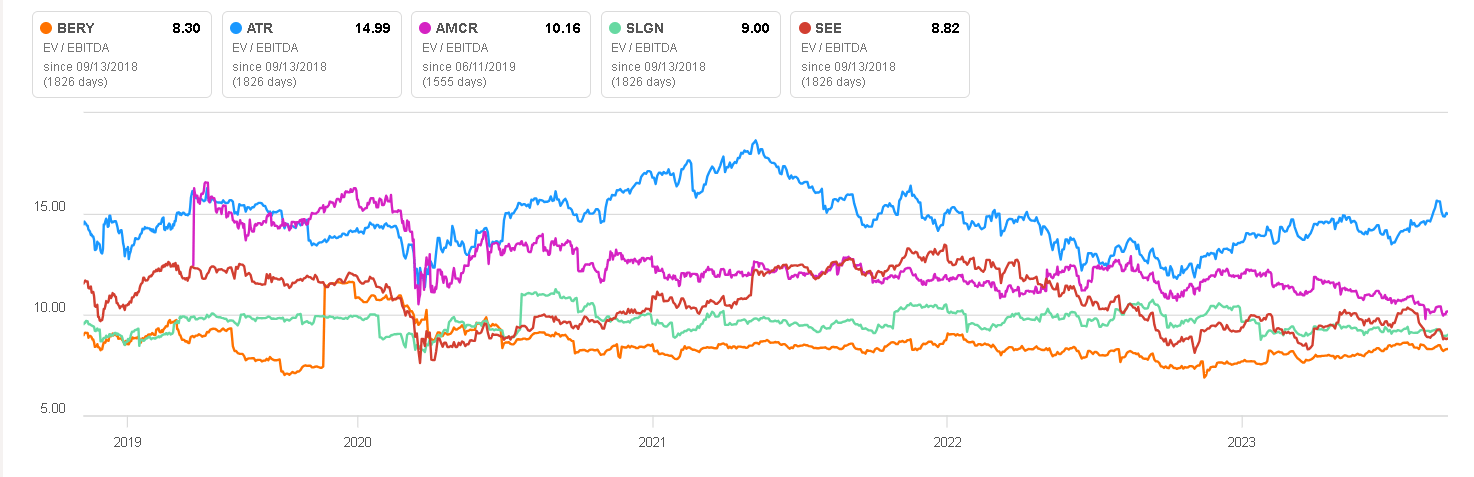

Valuation Difference (Seeking Alpha)

{kind=link}

Business Overview

Berry Global is a packaging manufacturer with a global presence. These products are usually sold to very stable sectors such as healthcare, personal care, and food and beverage.

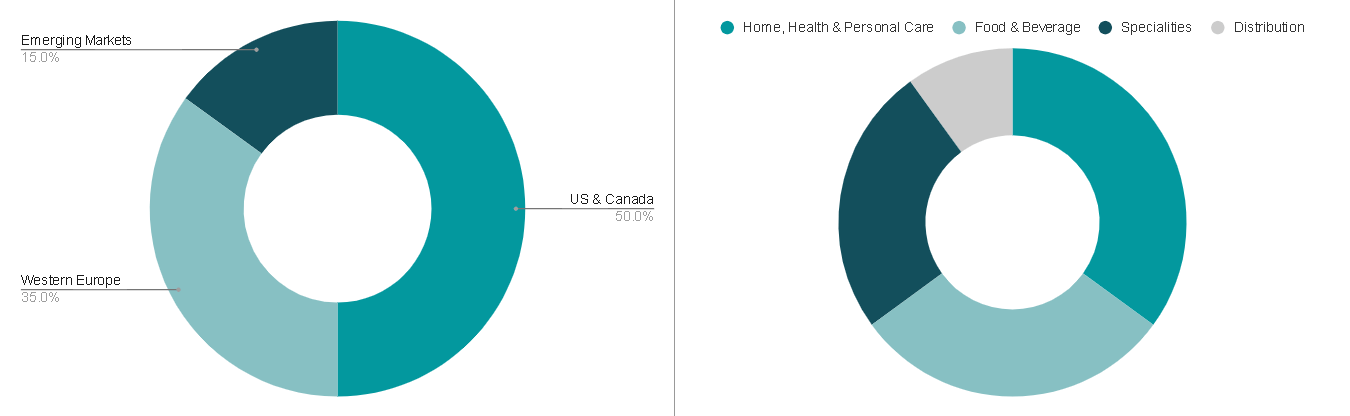

Revenues are greatly diversified geographically and by end market.

Sales Diversification (Author's Representation)

{kind=link}

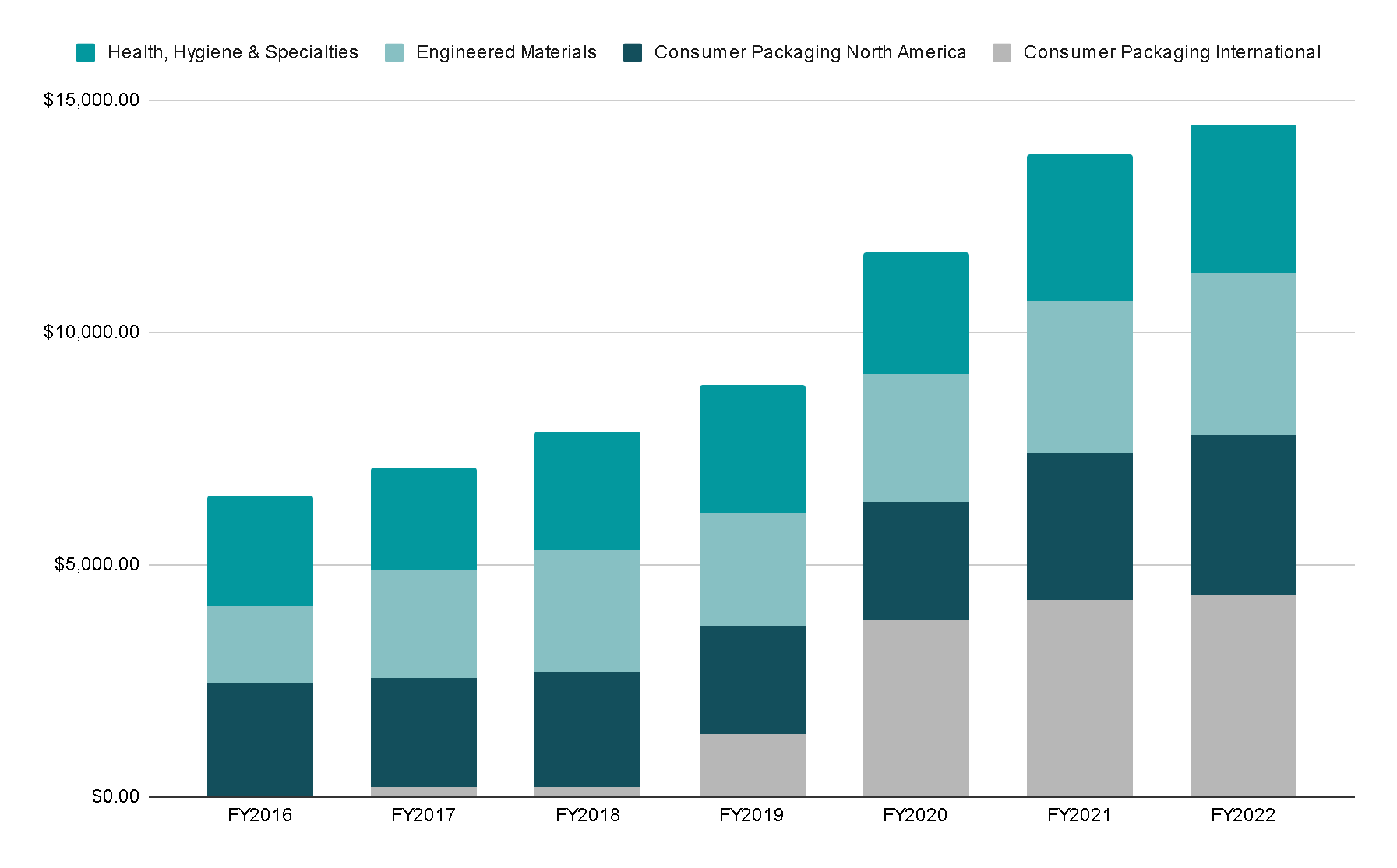

In addition to end market distribution, I would also like to briefly comment on the four main segments on which we could distinguish each Berry Global product. These are Consumer Packaging International, Consumer Packaging North America, Engineered Materials, and Health, Hygiene & Specialties.

Consumer Packaging International: This division specializes in producing rigid plastic products and primarily services to markets outside of North America. The product categories within this division encompass Closures and Dispensing Systems, Pharmaceutical Devices and Packaging, Containers and Technical Components.

In the fiscal year 2022, Consumer Packaging International contributed 30% to our total consolidated sales.

Consumer Packaging North America: This section specializes in producing rigid plastic products and predominantly serves markets in North America. This segment comprises product categories such as Containers and Pails, Foodservice, Closures, Bottles or Prescription Vials.

In the fiscal year 2022, Consumer Packaging North America represented 24% of our total consolidated sales.

Rigid Plastic Products (Berry Global)

Engineered Materials: The Engineered Materials division manufactures flexible plastic products primarily for markets in North America and Europe. This segment encompasses product categories such as Stretch and Shrink Films, Converter Films, Institutional Can Liners, Food and Consumer Films or Retail Bags.

In the fiscal year 2022, Engineered Materials contributed 24% to our total consolidated sales.

Flexible Plastic Products (Berry Global)

Health, Hygiene & Specialties: The Health, Hygiene & Specialties division specializes in producing non-woven and related products. Within this segment, there are product groups including Healthcare, Hygiene, Specialties, and Tapes.

In fiscal 2022, Health, Hygiene & Specialties represented 22% of our total consolidated sales.

Revenue per Segment (Author's Representation)

{kind=link}

All segments present very stable revenues that tend to be resilient due to diversification through such solid sectors as basic consumption or health care. Although it is worth mentioning that they mostly grow inorganically.

Another positive aspect of BERY's revenue is that EBIT margins are usually stable between 7 and 12% across all business lines. During 2021 and 2022 they fell, mainly due to inflation in raw materials and transportation costs, but even during covid-19 margins remained at their usual levels thanks to the recurring use of the products sold.

Plastic Consumption Isn't Over

Despite the bad reputation that plastic has, it is still one of the cheapest and most efficient ways to package products. For this reason, it is not surprising that the global plastic packaging market continues to expect growth of 4-5% annually for the next decade, especially in emerging markets, since it is difficult to achieve economic growth without access to such a cheap material. and reliable like plastic.

Marketsand Markets

What is true is that the market in general is turning towards more ecological alternatives to plastic, that is, variants made of plastic but that have biodegradable properties or with a lower percentage of this material. One of the most common alternatives is the lightweighting process , which is responsible for making the same product, but with fewer kilograms of plastic per unit. This is cheaper but it is also friendlier to the environment.

For example, during Q1 2023 the company announced that it has been delivering lightweight alternatives in the packaging of large companies such as Cola-Cola or a small consumer in Germany called Milchwerke Schwaben

We became the first plastic packaging manufacturer in Europe to supply the Coca-Cola company with a lightweight tethered closure for its carbonated soft drinks in PET bottles. The new tethered closure for Coca-Cola is designed to remain intact with the model, make it less likely to be littered and more likely to be recycled.

Or this example of the Q4 2022 conference call.

We also recently announced our launch of a new Mars jar for the well-known products such as M&Ms, SKITTLES and STARBURTS which will be lighter in weight and include 15% post-consumer resin.

While this is not unique to Berry Global, it does tell us that there is still demand for plastic in the future and that the company is in a good competitive position to supply this demand.

Key Ratios

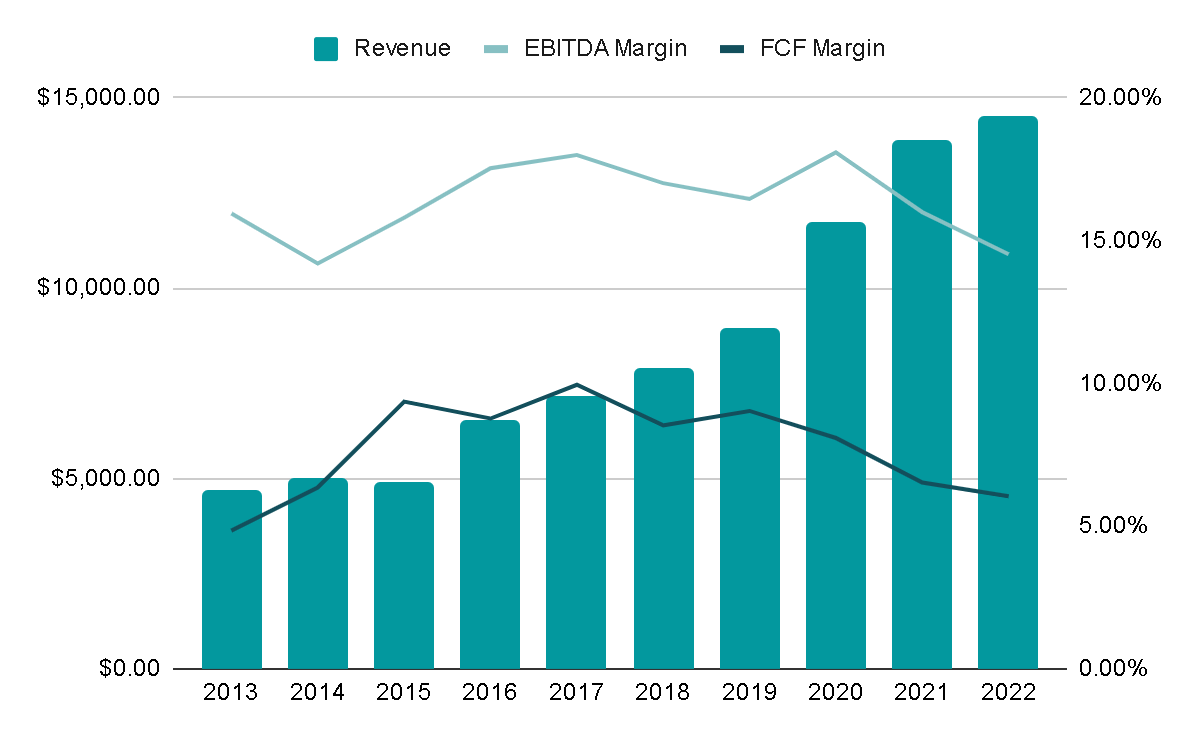

As I mentioned above, Berry's income is quite predictable. In fact, in the last decade they grew at a rate of 13% annually, although very little of this was organic (perhaps 1-2% annually).

This growth has been achieved while maintaining average EBITDA margins of 16% and almost 8% for Free Cash Flow. As a reference, during FY2022 the margins were 14.5% and 6% respectively, which shows us what I mentioned previously about how inflation and raw material costs have slightly affected profits.

Revenue and Margins (Author's Representation)

{kind=link}

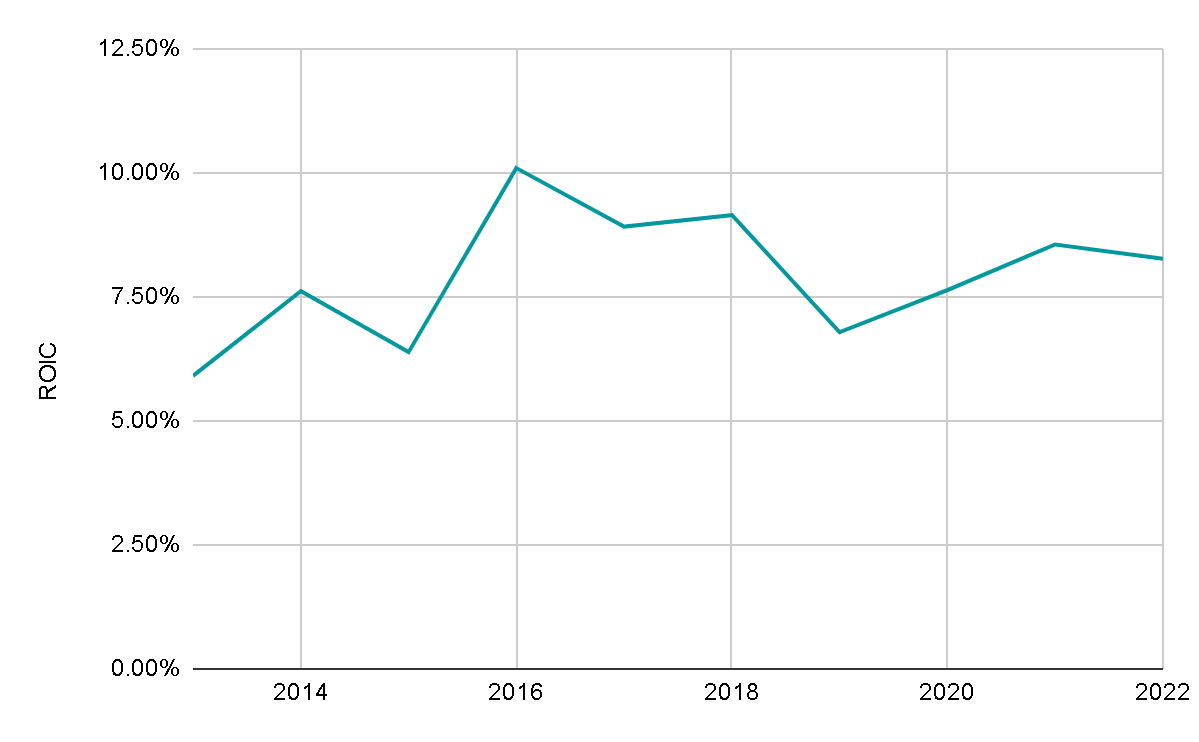

The ROIC is not exactly high, in fact it is usually around 8% which is much lower than the market average, however, I consider that this type of investment is more focused on receiving returns through dividends and share repurchases rather than by organic growth and returns on invested capital.

{kind=link}

Activist Investors

The important part of the thesis comes with the arrival of different activist investors, with the intention of improving the company's capital allocation.

The first of these was the American investment fund Canyon Capital in 2020 . Canyon sent a letter in which it commented that although the company's profits had grown in recent years, the share price had done nothing and there was value hidden in Berry due to poor capital allocation and proposed that the company should focus on reducing the level of leverage and M&A activities.

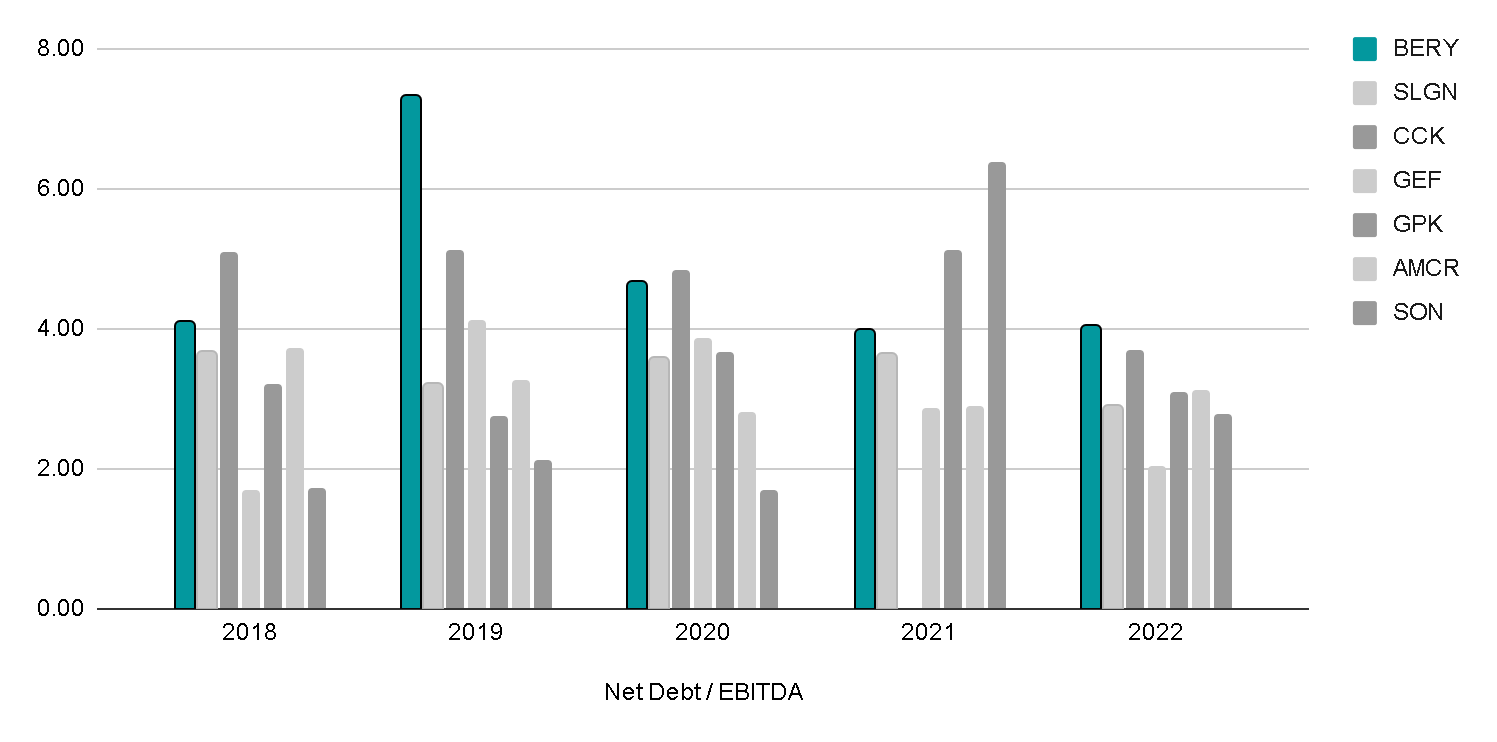

This had some truth, because in the years around 2020, Berry Global was one of the most indebted companies in the sector:

Net Debt vs Peers (Author's Representation)

{kind=link}

Despite this Berry's response was pretty poor and there was no change at all.

Subsequently, in November 2021, Ancora Holdings fund sent a letter to the board in which it proposed that the company should consider a total sale of the business and privatize it, since there was a constant undervaluation with its peers and it considered that the best way to solve it was through a large share buyback plan.

And after a few years of plastic and insistence, in November 2022 Berry Global finally announced an appointment of 3 new directors and the formation of a Capital Allocation Committee.

Capital Allocation

Based on this news, the question is: Is there really being a positive change according to what activist investors expected?

Well, to solve this question I would like to look at capital allocation:

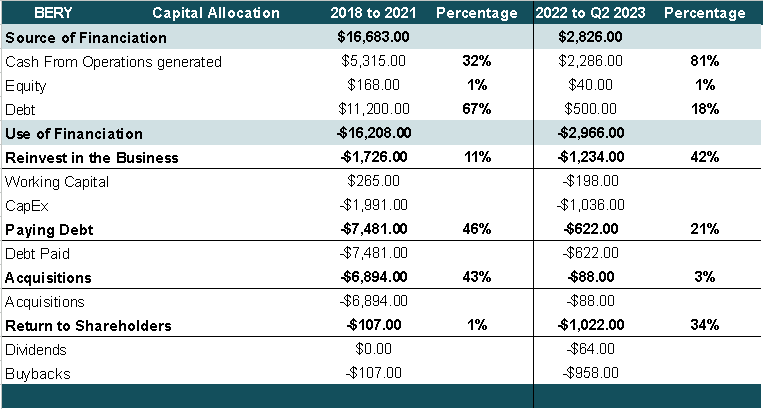

If we look at the 2018-2021 period (before the formation of the committee), capital allocation management focused on acquiring capital through debt and using it mostly to grow through acquisitions and pay off the acquired debt.

While this wasn't necessarily a bad thing at all, as revenue and profit growth also helps share price growth, it also increased the risk perceived by the market as this was a company that consistently had a high leverage level.

And from 2022 to date, it can be seen that there was a radical change in capital allocation. In this period, 81% of the capital came from cash from operations and much less debt was acquired. In addition, M&A activity was almost completely paused and 30% of the capital began to be allocated to repurchase shares and pay dividends, something that was not done in previous years.

{kind=link}

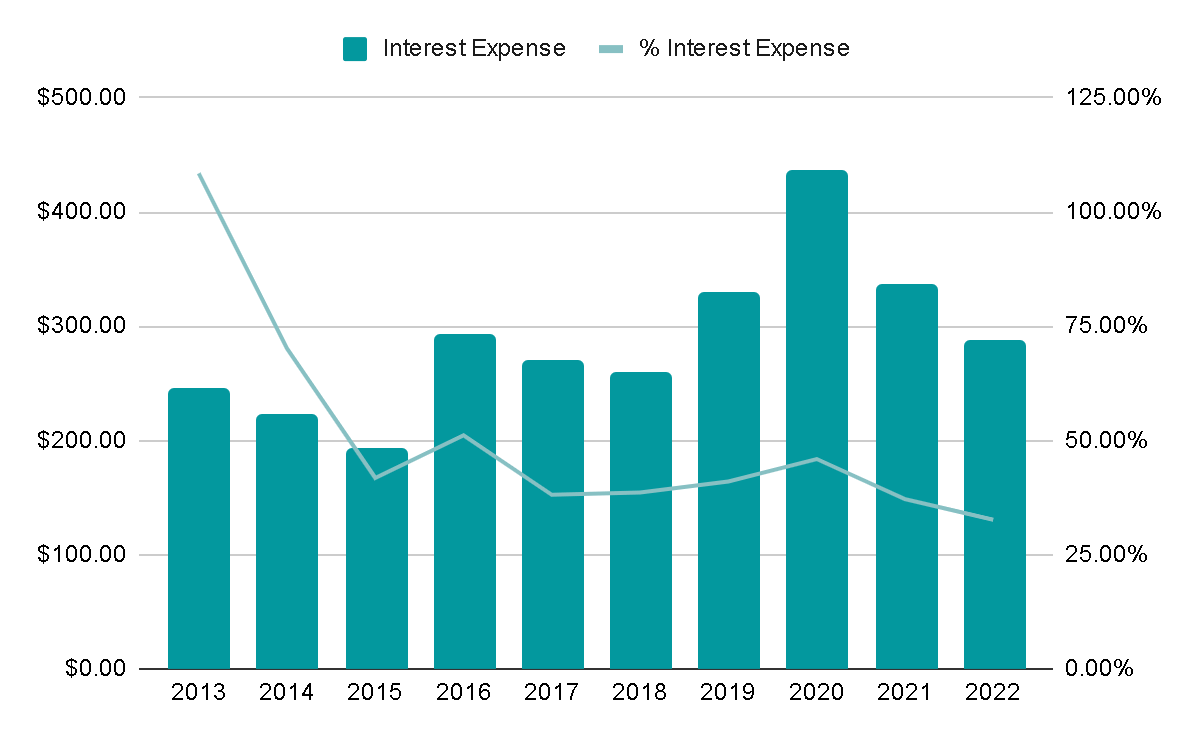

We can also see how interest expenses have been reduced and during FY2022 they represented only 32% of the Free Cash Flow, compared to 37% in FY2021 and the 44% average of the last decade.

Reducing debt and focusing on rewarding shareholders is an excellent way to unlock the hidden value that was in the company and make it trade at multiples close to or higher than its peers. Furthermore, it will be especially relevant in a macroeconomic environment with higher interest rates.

{kind=link}

Valuation

For the valuation, I want to employ a rather simple approach, as the great Charlie Munger once said: 'You don't need to know a man's weight to know that he's fat.'

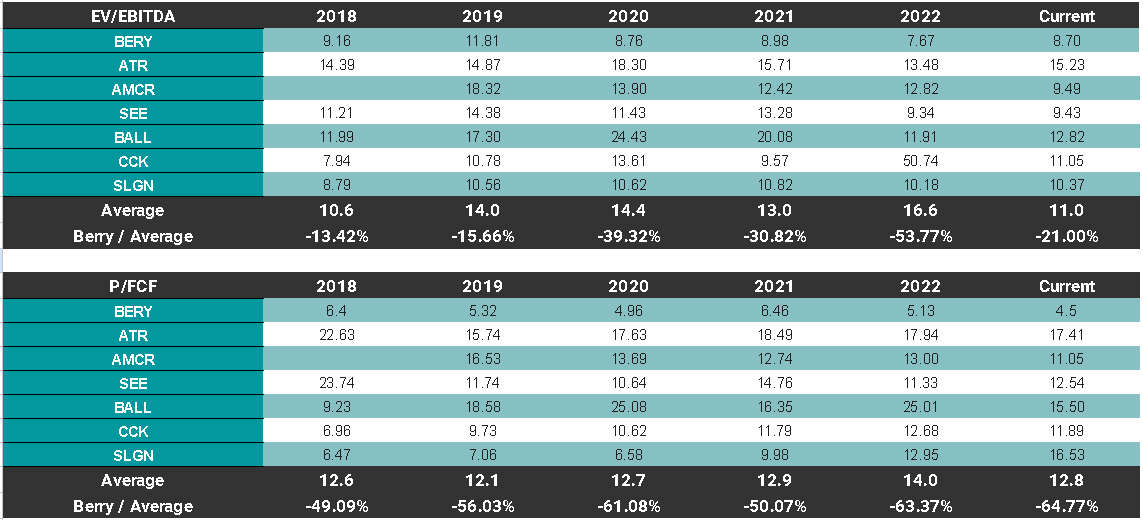

In the following table, we can observe Berry's valuation compared to its peers. Here, the undervaluation mentioned by the Canyon and Ancora funds becomes evident. While the average P/FCF in the rigid and flexible plastics sector is 12x, BERY has been trading at less than 5x for the past 5 years.

Valuation Metrics vs Peers (Author's Representation)

{kind=link}

Although in the past, there were reasons to justify this undervaluation, I believe that measures have currently been taken to benefit the financial strength of the company and, in turn, remunerate the shareholder, which should be reflected in the valuation thanks to a hypothetical optimism in the market and investors.

According to FY2023 guidance, management expects to generate $800M in Free Cash Flow this year and repurchase 8% of outstanding shares, bringing them to 122M shares. This would mean an FCF per share of $7 USD. If we were to apply the industry average of 12x P/FCF, Berry Global should be worth $85 USD today , which is 32% more than the $63 at which it is currently trading. Even with a P/FCF of only 10x, the current price would be $70 USD, 10% higher than current price.

All this is without counting the modest dividend yield of 1.6%

Final Thoughts

While this evaluation isn't exhaustive and relies on data and assumptions, it suggests that the stock's current price offers substantial value, trading at a significant discount compared to its peers, the sector, and the broader market average.

Does it merit a valuation on par with its competitors?

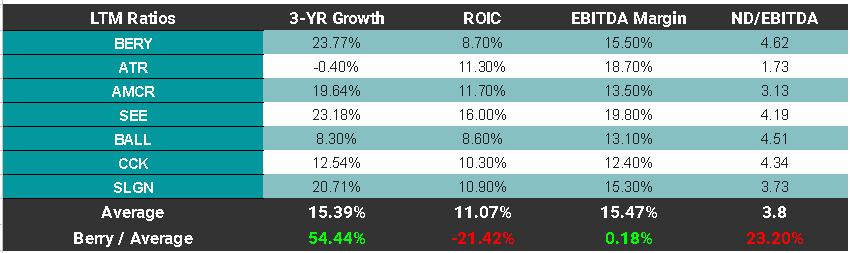

Based on its recent net income growth and EBITDA margin, the answer appears to be yes. However, when considering factors like ROIC and Net Debt/EBITDA, it's possible that the stock's undervaluation relative to the sector is justified. This is where the importance of reducing debt comes into play, a strategy the company has diligently pursued in recent months.

Comparison of Quality and Growth (Author's Representation)

{kind=link}

In my view, a turnaround seems plausible, potentially yielding favorable returns for shareholders. Therefore, I would recommend a ' buy ' rating, contingent on management's continued performance in line with their recent efforts.

For further details see:

Berry Global: Changes In Capital Allocation Gives Hope To Shareholders