BERY - Berry Global: Early Innings Of A Turnaround

2023-11-20 12:21:58 ET

Summary

- Berry Global Group has shown strong earnings and revenue growth, but its valuation has lagged its peers for years.

- The company is in the midst of a turnaround, having appointed a new CEO and a commitment to unlocking shareholder value.

- As Berry's operating results improve and its capital allocation strategy plays out, I anticipate institutional investors will take notice, driving share price appreciation over the long term.

- At $63 per share, the market is pricing in flat to declining FCF growth over the next decade, compared to Berry's 10-yr CAGR of 15%.

I first discovered Berry Global Group, Inc. ( BERY ) in 2021 while screening for high quality growth stocks. Berry screened unbelievably well for earnings growth and above average for revenue growth. The company is a cashflow machine.

I recall the stock looked cheap from a P/E perspective, trading at less than 10x. At first, I thought I found a diamond in the rough and was very excited.

Unfortunately, that changed after diving into Berry's balance sheet and cashflow statement, and after listening to the company's latest earnings call at the time.

What I learned was Berry liked to accumulate debt, and didn't appear all that concerned with creating shareholder value. Berry's market cap today is $7.4 billion, the same as it was back in 2017.

Fast forward to today, and all that has changed. In this article, I'll review why I think Berry Global is in the early innings of a turnaround which is likely to unlock meaningful value for patient shareholders.

Reader's Digest Overview

A previous author did a great job highlighting what Berry Global does, so I'll spare you the detail.

In short, the company manufactures and sells packaging products (mostly plastics) to numerous industries, including: health & beauty, food & beverage, and medical & pharmaceuticals.

In my opinion, Berry's operations are well diversified and anticyclical. Meaning, regardless of the macroeconomic environment, Berry is likely to make it through mostly unscathed.

Not to say the company wouldn't be impacted by a broad recession; it would. But I think it would weather the storm better than most due to its broad base of customers and diverse product mix.

Until recently, leadership at Berry was concerned with growing the company via acquisitions, hence the large and growing amount of debt on the balance sheet. Berry was less concerned with driving organic growth (i.e. growing revenue and earnings in the markets it already served), or creating value for shareholders.

In 2020, activist investors' frustrations finally bubbled over due to a prolonged disparity between Berry's stock price (in relation to its peers) and its financial performance.

What Did The Activists See?

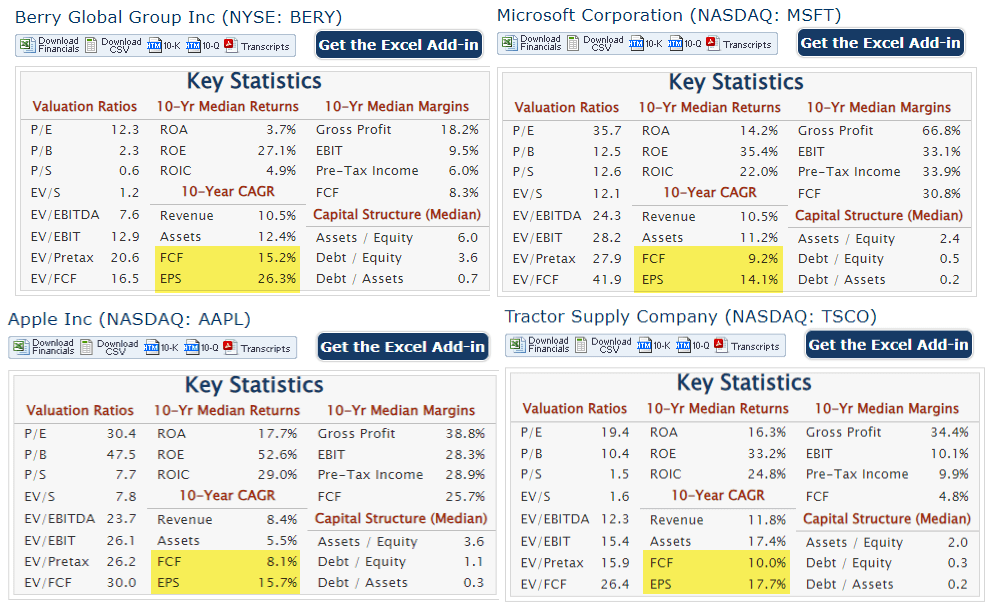

When you think of an earnings compounder, Berry Global probably isn't the first name that comes to mind. Apple ( AAPL ), yes. Microsoft ( MSFT ), of course. Tractor Supply ( TSCO ), sure.

These 3 companies have compounded earnings exceptionally well the past 10 years and shareholders have been rewarded handsomely.

But would you believe me if I told you Berry outpaced them all? Well, it's true.

BERY Growth vs Market Darlings (quickfs.com)

{kind=link}

How can a company, having grown FCF and earnings at +15% for 10 years, have a 5-year average P/E of 10x? This is the question activist investors must've been asking themselves back in 2020.

The Turnaround

Feeling pressure from activist investors and shareholders in general, Berry took concrete, measured steps to unlock shareholder value. Since early 2022, some of these include:

- Appointment of a new CEO, Kevin Kwilinski

- Appointment of 3 new members to its Board of Directors, including a partner at Canyon Partners (one of the activist investors)

- Pausing/pulling back heavily on M&A activity

- Aggressively paying down debt to reduce net leverage to less than 3.5x, which it expects to accomplish by end of 2024

- Instituting a quarterly dividend, currently yielding 1.67%

- Opportunistically repurchasing shares

In my opinion, Berry has transitioned its priorities from "growth at any cost" to "unlocking long-term shareholder value." This is especially evident in the Q4 2023 and Full Year earnings presentation . There is slide after slide documenting Berry's shareholder-focused priorities which is highly encouraging.

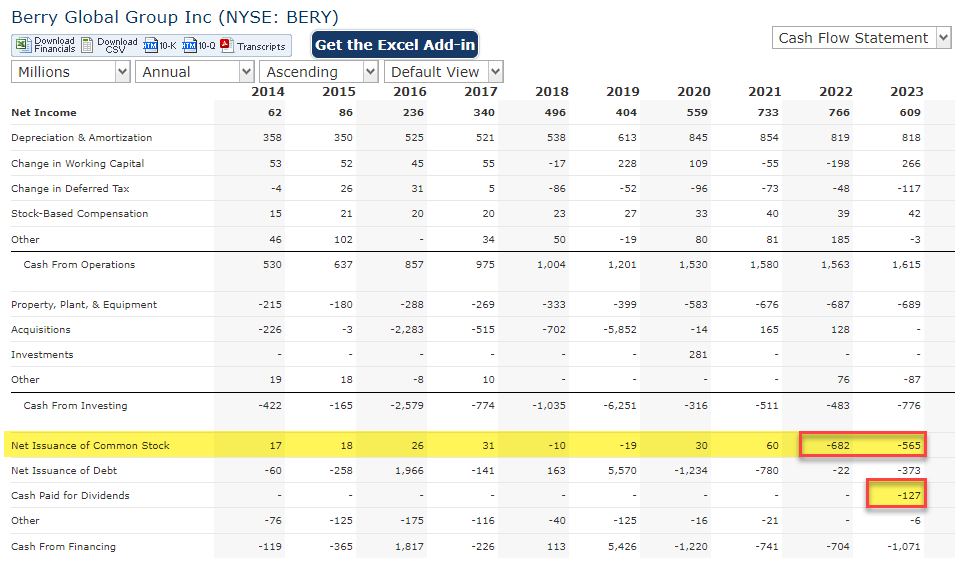

But words are fluff. Fortunately, Berry's actions aren't. In 2022 , Berry returned $709 million to shareholders via share buybacks. The trend continued in 2023, with $728 million returned to shareholders via a combination of share buybacks and dividends.

Coincidentally, this wasn't Berry's capital allocation strategy the previous 10 years as evidenced by its cashflow statement. Notice how the company had been slightly diluting shareholders with no dividend from 2014 to 2021? The past 2 years are a stark difference. To me, this indicates the turnaround effort is real.

BERY Cashflow Statement (quickfs.com)

{kind=link}

Valuation

Berry stock is up 18% since announcing Q4 2023 earnings with a current price near $63 per share. Even with the run up, shares still look to be undervalued.

Berry's non-GAAP forward P/E sits at 8.3x, compared to its 5-yr average of 10.2x. For 2024, the consensus non-GAAP EPS is $7.71. Assuming a reversion to the mean spurred by improving market sentiment due to Berry's turnaround efforts , that puts a fair value at $78.64 ($7.71 x 10.2x) representing 25% undervaluation.

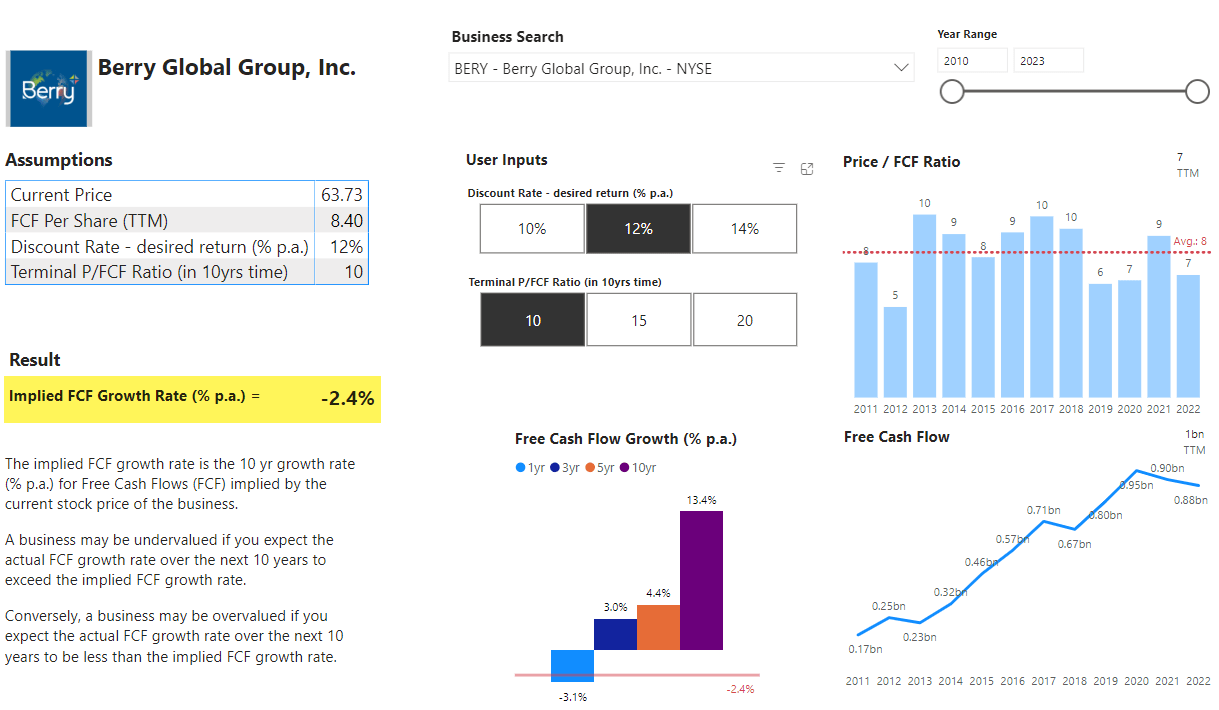

Similarly, the market is pricing in flat to declining FCF growth over the next 10 years. This is based on a reverse DCF calculation. For the calculation, I assumed a 12% discount rate and terminal P/FCF of 10x.

BERY Reverse DCF (stockinvestoriq.com)

{kind=link}

At $63 per share, the implied FCF growth rate is -2.4% annually . Reminder, Berry has grown FCF at a 15% CAGR the previous 10 years. The market appears to be extremely bearish with low expectations for Berry. With the bar so low, it seems like an opportunity.

Bear Case

Berry is a producer of plastic, which in light of the ESG movement, comes with a negative connotation. Environmentalists argue plastics are bad for the health of the planet and humanity. And with mounting pressure to invest in green, eco-friendly companies with strong ESG initiatives, institutional investors may shy away from a plastics maker like Berry Global.

To unlock value for shareholders, Berry needs big money, institutional investors to drive share appreciation. If Berry can't convince institutions it's an eco-friendly, sustainability-focused company (which I believe it is), no amount of dividends or share repurchases will move the needle on market cap.

Fortunately, Berry's new CEO Kevin Kwilinski is focused on exactly this, sustainability, as evidenced in its Q4 2023 earnings call:

I would say, the thoughts around growth and the opportunities, we have owned a very large opportunity around sustainability. And it isn't theoretical because the reality of the world we are in is -- Europe is quite a ways ahead of us. And we are operating in Europe -- and we are seeing where legislation is going and the opportunities it creates for new sorts of highly recyclable -- high recycled content, advanced recycle containing plastic products that the consumers want that fit within extended producer responsibilities and returnable, reusable options. And those drive very large opportunities for growth and share gain if we have products that are superior and differentiated.

Conclusion

Berry's story is no longer about growth, it's about execution and profitability. I don't expect double digit increases in revenue year after year. But 5-10% organic growth in EPS driven by product innovation and operating efficiencies, coupled with 5-10% growth via share repurchases, makes for a compelling opportunity. Not to mention the new dividend.

There's some inherent risk associated with Berry due to its core business as a plastics manufacturer, but management is environmentally and sustainability focused. I think it's a risk worth taking.

Plus, the market is sour on Berry, pricing shares well below its historical valuation multiples, and expecting no growth in FCF over the next decade. With a bar so low, it certainly appears easy to jump.

For further details see:

Berry Global: Early Innings Of A Turnaround