GEF - Berry Global Group: A Stellar Year And Weakening Financials Aren't Enough To Change My Stance

2023-07-18 13:21:42 ET

Summary

- Berry Global Group, a global supplier of packaging products, has seen a 25.1% increase in shares over the past 12 months, outperforming the S&P 500's 15.6% upside.

- Despite a year-over-year decline in revenue for H1 2023 due to a volume decline and decreased selling prices, the company's shares remain cheap compared to similar firms.

- The company plans to return $700 million to stockholders in 2023 through stock repurchases and dividends, and aims to grow distribution and achieve total returns of 10-15% annually.

What a difference a year can make! A little over a year ago, on July 8, 2022, I published an article wherein I discussed my very bullish thesis regarding Berry Global Group ( BERY ), an enterprise that operates as a global supplier of packaging products. I found myself drawn to the company because of the growth it was experiencing and the fact that shares of the enterprise were incredibly cheap. Recently, we have started to see a change in the performance of the firm. That might be causing some investors to become concerned. Given broader economic conditions, I definitely understand that. But even after seeing the company experience a blockbuster 12 months, I do believe that further upside is on the table.

A solid prospect still

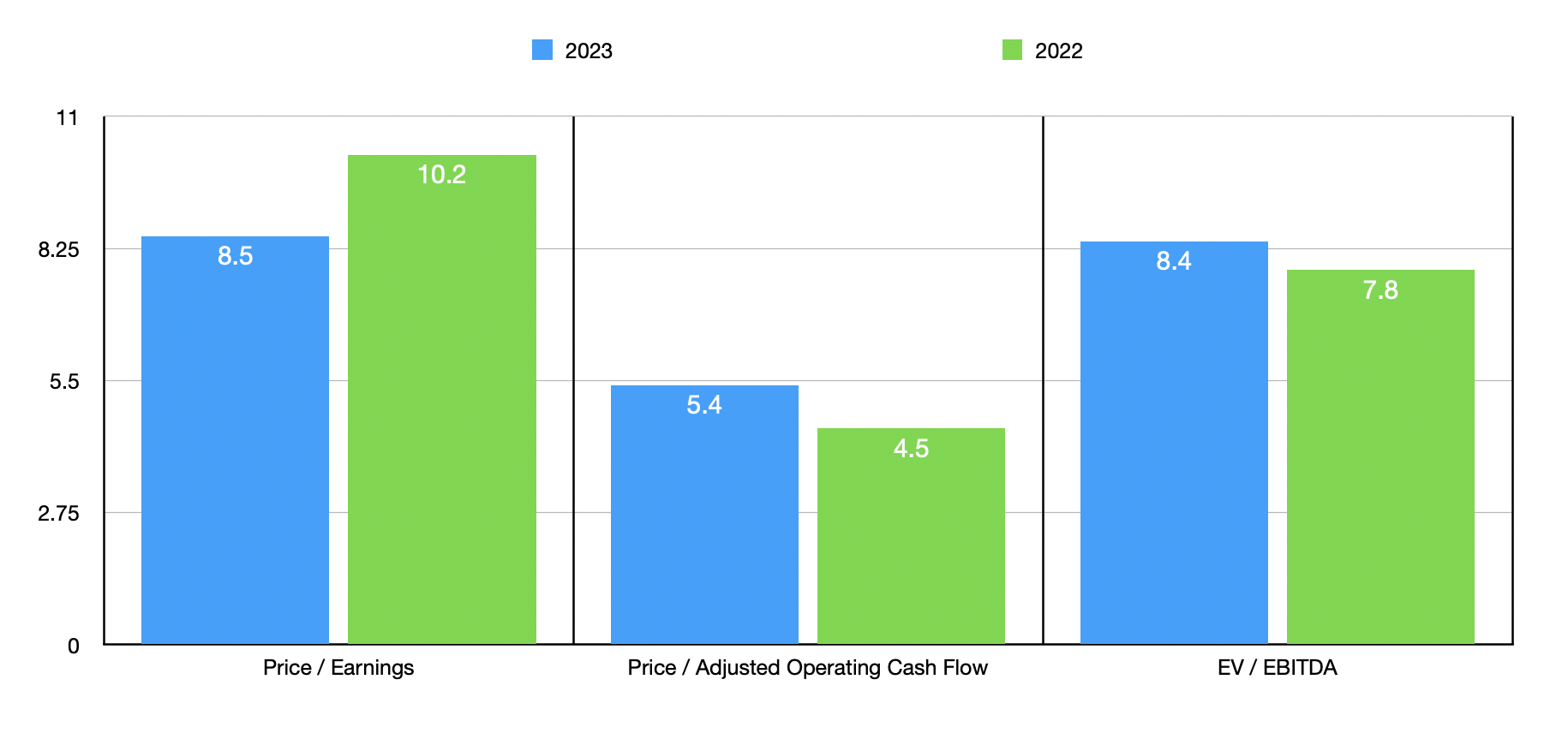

Over the past 12 months, the S&P 500 has seen a rather impressive 15.6% upside. That is remarkable considering just how painful certain parts of the past two years have been. But that upside pales in comparison to the 25.1% increase that shares of Berry Global Group experienced from the time I last wrote about it 12 months ago. Much of the upside the company has experienced was driven by robust financial performance, combined with the fact that shares of the company were quite cheap. On a forward basis, the firm was trading at a price to earnings multiple of 7.4. The forward price to adjusted operating cash flow multiple was 3.5, while the EV to EBITDA multiple was only 5.4.

{kind=link}

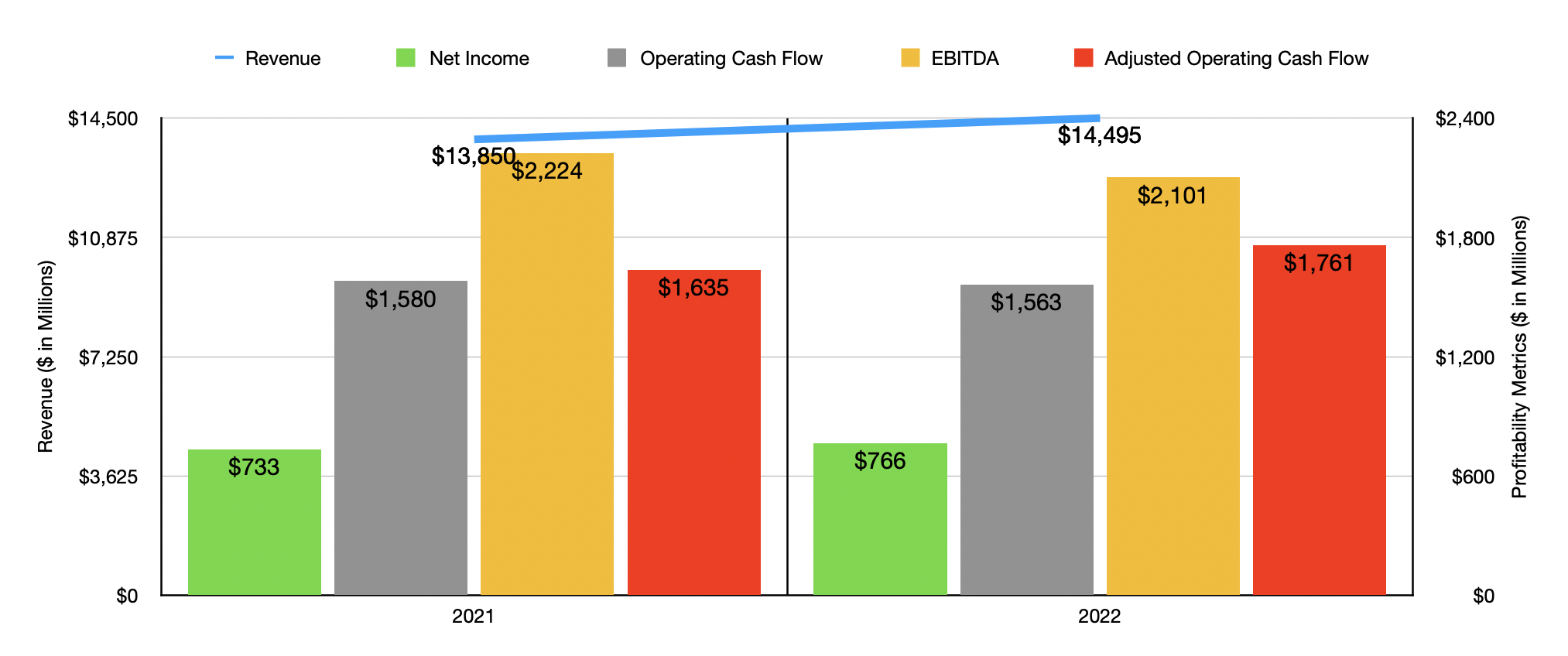

When you look at the 2022 fiscal year in its entirety, the picture for the business was quite nice. Revenue of $14.50 billion translated to a 4.7% increase over the $13.85 billion the company generated in 2021. This upside was in spite of the fact that the company sold off its rotational molding business that generated $146 million in revenue in 2021. The increase in sales, then, was driven largely by higher selling prices that helped the company to the tune of $1.65 billion. If this increase seems peculiar given the disparity in revenue between the two years, keep in mind that there are other factors at play when it comes to revenue. The company actually suffered from a 2% organic volume decline and was hit by the absence of an extra shipping day in 2021 that hurt sales by $131 million. But the biggest problem was a $420 million impact associated with unfavorable foreign currency fluctuations.

Bottom line results for the company were mixed year-over-year, but not bad. Net income of $766 million was higher than the $733 million reported for 2021. On the other hand, operating cash flow dipped from $1.58 billion to $1.56 billion. But if we adjust for changes in working capital, we would get an increase from $1.64 billion to $1.76 billion. Meanwhile, however, EBITDA for the company shrank from $2.22 billion to $2.10 billion.

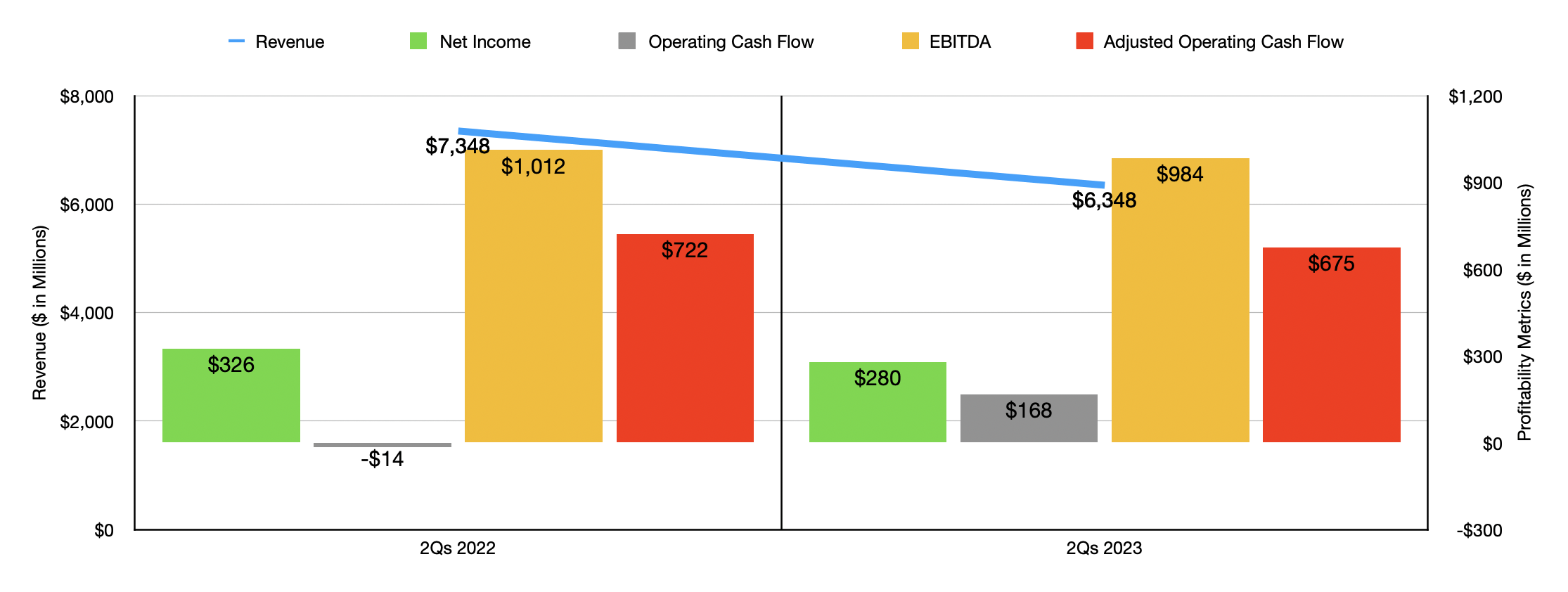

All things considered, these results were far from bad. In fact, they were really great. 2023, on the other hand, has proven to be a different animal entirely. Revenue of $6.35 billion translates to a year-over-year decline for the first half of the year compared to the same time last year of 13.6%. Management attributed this largely to a 6% volume decline and to decreased selling prices in the amount of $143 million. Foreign currency fluctuations hit the company to the tune of $80 million, while divestitures impacted the company to the tune of $42 million. Management was very clear about the cause of the volume decline. According to them, the market has experienced some softness and its customers are going through inventory destocking.

{kind=link}

Naturally, this would have profound implications for the company's bottom line. Net income during the first half of 2023 totaled $280 million. This was down significantly compared to the $326 million reported one year earlier. Operating cash flow did manage to go from negative $14 million to $168 million. But on an adjusted basis, it fell from $722 million to $675 million. Meanwhile, EBITDA for the company fell from $1.01 billion to $984 million.

Management has not provided any guidance when it comes to revenue for 2023. But given their expectations for the bottom line, I do think additional weakness is likely. Operating cash flow, for instance, is expected to come in at only between $1.4 billion and $1.5 billion. If we apply the same year-over-year change to EBITDA, we would get a reading of $1.95 billion for the year. Based on management's earnings per share guidance, net income should actually come in at a rather robust $925 million.

{kind=link}

In the chart above, you can see how shares are priced, using both data from 2022 and estimates for 2023. And in the table below, you can see how shares are priced using the 2022 figures compared to five similar enterprises. Using the price to earnings approach, only one of the companies was cheaper than Berry Global Group. When it comes to the price to operating cash flow approach, our prospect was the cheapest. And when it comes to the EV to EBITDA approach, only two of the five firms were cheaper than our target. This picture does not change much even if we use the estimates from 2023. Using the price to earnings approach, Berry Global Group ended up being the cheapest of the group. The same can be said when we use the price to operating cash flow approach. And when it comes to the EV to EBITDA approach, two of the five firms were cheaper than our target.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Berry Global Group |

| 10.2 |

| 4.5 |

| 7.8 |

| Greif ( GEF ) |

| 9.6 |

| 5.7 |

| 7.1 |

| Crown Holdings ( CCK ) |

| 17.6 |

| 12.4 |

| 10.6 |

| Ranpak Holdings ( PACK ) |

| N/A |

| 20.9 |

| 20.7 |

| Silgan Holdings ( SLGN ) |

| 16.0 |

| 13.6 |

| 10.5 |

| Packaging Corporation of America ( PKG ) |

| 12.9 |

| 8.5 |

| 7.7 |

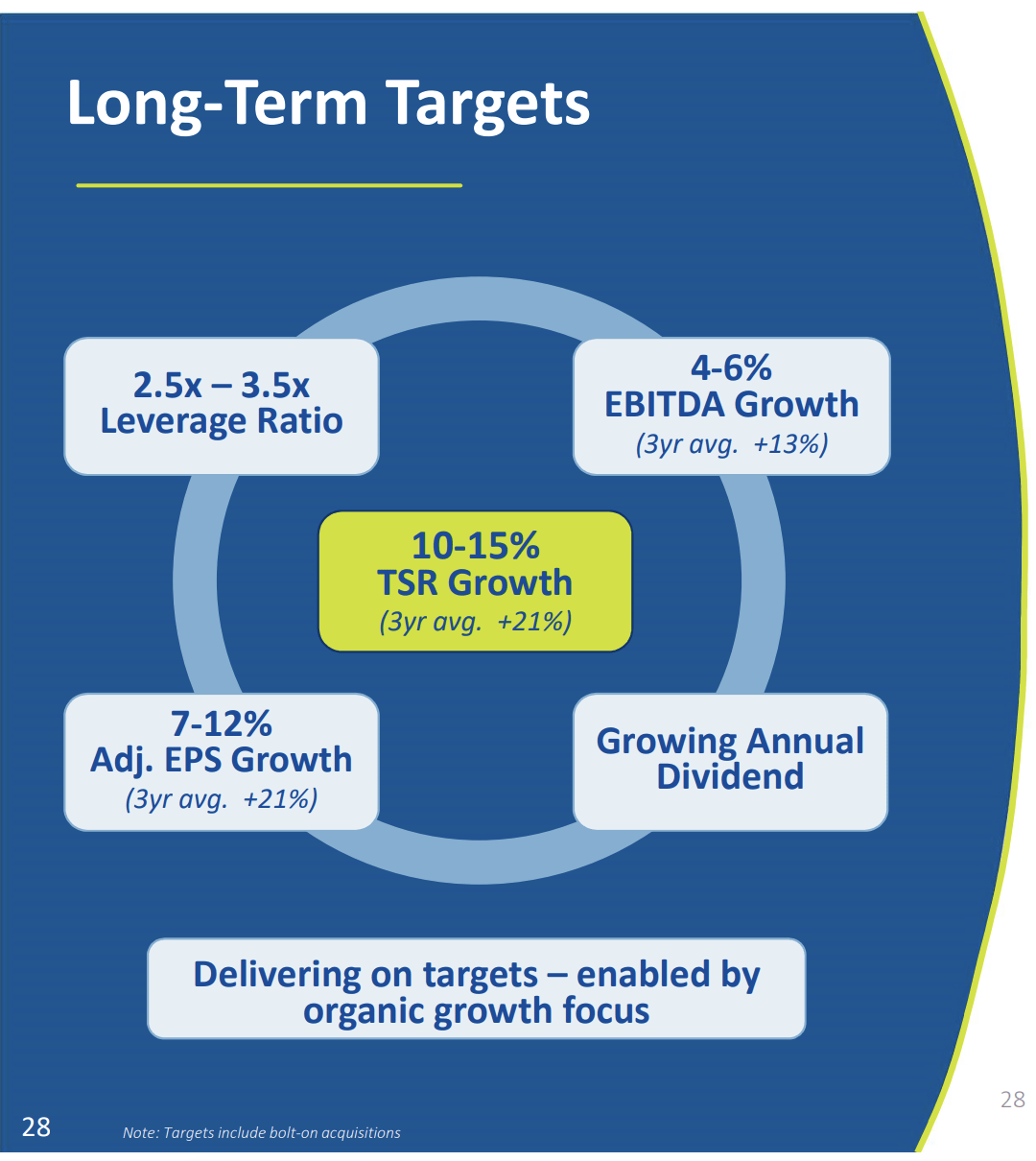

In addition to shares trading on the cheap, management is also dedicated to rewarding shareholders and focusing on long-term growth. The current expectation for 2023 is for the company to return $700 million to stockholders in the form of stock repurchases and dividends. And over the next few years, the expectation is for the company to get shareholders total returns of between 10% and 15% a year, with adjusted earnings per share climbing by between 7% and 12% while EBITDA should grow by between 4% and 6%. It's unclear if the company will continue to buy back stock during this time. But they did expressly say that their goal is to grow the firm's distribution moving forward.

{kind=link}

Takeaway

Even though we are experiencing a bit of weakness in this space, shares of Berry Global Group look cheap, both on an absolute basis and relative to similar firms. Long term, I have no doubt that the company will continue to grow. Along the way, the business is distributing large amounts of capital to its shareholders. While I would personally prefer that capital be reinvested into growth or allocated toward share repurchases and not dividends, any sort of return to investors is a net positive. Given all of these facts, I do believe that the 'strong buy' rating I assigned the company previously is still appropriate.

For further details see:

Berry Global Group: A Stellar Year And Weakening Financials Aren't Enough To Change My Stance