ARKK - Best Macro Pairs Trade Of 2023: Short ARKK And Long Healthcare

Summary

- The technology sector is highly cyclical and sensitive to interest rates, and the valuation for many companies is still overvalued; tech should continue to get clobbered during 2023.

- Inflation is still high; the fed is still hiking rates; the yield curve is still inverted, and macro trends are continuously unfavorable toward the technology sector, especially the software industry.

- We believe healthcare is the only undervalued non-correlated growth sector that will continuously do well during stagflation.

- SMID cap biotech's end buyers are big pharma with robust non-correlated cashflow and deep pockets; they need continued M&A to replenish their pipeline.

- Longing healthcare ETF and shorting ARKK as a hedge is an excellent strategy moving into 2023 to generate a negative beta portfolio that may outperform S&P500 during the stagflationary market conditions.

2022 played out exactly as we predicted with tech suffering and healthcare outperforming

As we predicted in our previous article early last February, the technology sector has underperformed the S&P500, and healthcare equities have outperformed the market. We expect this trend to continue further during 2023. After small and midcap tech getting totally obliterated, the generals of the software industry, including Tesla ( TSLA ), Apple ( AAPL ), Amazon (AMZ), Netflix ( NFLX ), and Facebook/Meta ( META ) are starting to follow the same trajectory, getting clobbered approaching near pandemic level. The biggest casualties of the low interest-rate induced bubble popping are Cathie Wood's Ark Innovation ETF ( ARKK ) and cryptocurrencies. As we warned our readers multiple times in my bearish article on cryptocurrencies, the king of cryptocurrency Bitcoin ( BTC-USD ) and Ethereum ( ETH-USD ), has almost lost 70%+ of their value within the last several months, and the end is nowhere in sight. The speculative bubble stocks and digital collectibles started collapsing when US Fed changed into a hawkish tone (November 2021) right after Jerome Powell got reappointed as Fed chairman . Things haven't changed since we wrote our previous article; inflation is still high, the fed is still hiking rates, the yield curve is still inverted, and macro is continuously unfavorable toward the technology sector.

Shorting tech and longing biotech would have yielded excellent risk-adjusted return beating S&P500 by a great margin.

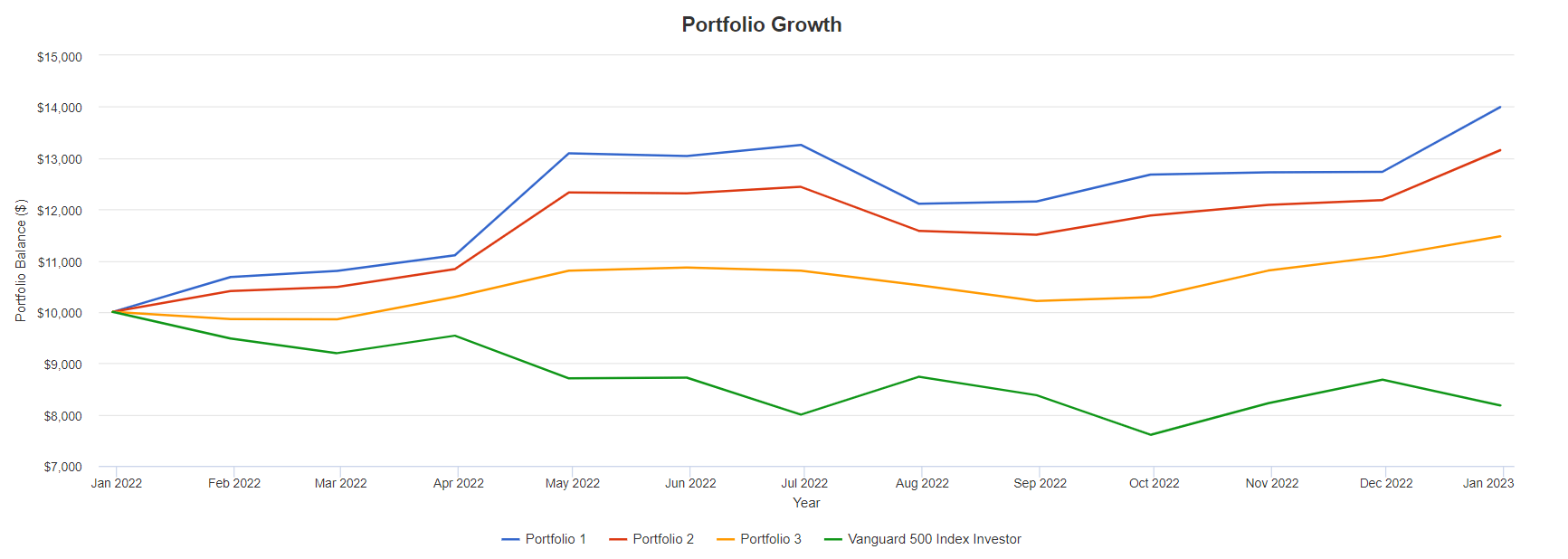

We have modeled our portfolio, going long healthcare through a widely held broad healthcare ETF and shorting ARKK as a hedge during 2022. We also adjusted the percentage of our short position to see how returns, market correlation, and the sharp ratio differs. Our three scenarios are i) portfolio 1: Long healthcare 50%, short ARKK 50%, ii) portfolio 2: long healthcare 60%, short ARKK 40%, and iii) portfolio 3: long healthcare 70%, short ARKK 30%.

{kind=link}

Biotechvalley portfolio back testing (Portfoliovisualizer)

{kind=link}

Biotechvalley portfolio back testing (Portfoliovisualizer)

The results were remarkable; all three portfolios returned 14-38% vs. S&P500 returning -18% during the same period, especially portfolio 3: long healthcare 70% and short ARKK 30% has created almost a market neutral (close to 0 market correlation). This correlates to 32%-57% market outperformance with a sharp ratio between 1.27 to 1.53.

{kind=link}

Biotechvalley portfolio back testing (Porfoliovisualizer)

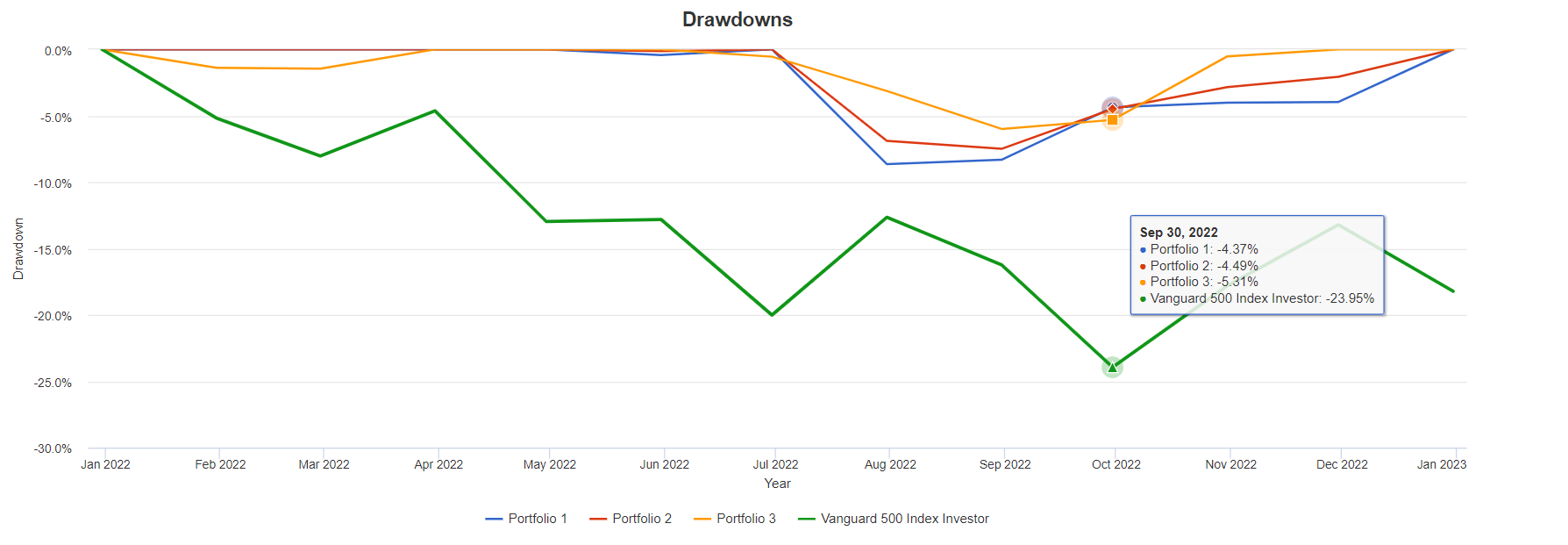

Another interesting point is that even though we had some remarkable bear market rallies in ARKK, the maximum drawdown levels of the model portfolio are extremely low, between 5-8% vs. -24% for S&P500 during last year as healthcare stocks also rallied offsetting the loss in the short side.

{kind=link}

Biotechvalley portfolio back testing (PortfolioVisualizer)

Why do we expect the technology sector continuously deflate

The technology sector will further decline with more B:C and B:B customers cutting down on tech-related spending, impacting the demand side of the equation, as we have recently seen with Tesla's remarkable growth slowing down due to declining in demand . Furthermore, we expect many internet advertising-based businesses (Google, Meta, and Snap a few examples) to decline further with lesser consumer discretionary spending, and total advertising spending will have to decline. We reiterate our view around the technology sector from our previous article as things have not changed that much during the last 1 year, if not further aggravated.

Here is what we said last year:

Why we expect the technology sector to underperform during the last decade

Many growth investors will argue that Tech will grow faster (than healthcare and biotech) and justify the current valuation. We disagree with the point of view because of three reasons.

First, we are seeing a very high inflation rate (~7.5%) , and global central banks are slowly and steadily increasing interest rates. This will further put pressure on high P/E growth-sector companies (which are concentrated in the technology sector). As a result, investors will look more and more for value or defensive growth sectors that are reasonably priced; healthcare and biopharma is the best option. Unlike healthcare, the technology sector is more cyclical in nature - for example, during the recession, people will still spend money on drugs if they get sick, but many of them stop subscribing to Netflix ( NFLX ) and buy fewer products through Amazon ( AMZN ).

Second, bipartisan-backed antitrust push from major governments is capping the inorganic growth (M&A) of giant technology companies that drove S&P500 and NASDAQ during the last decade. There is increasingly more and more pushback on big tech acquiring smaller players. As such, many unprofitable technology companies with high valuations (Uber ( UBER ), DoorDash ( DASH ), Airbnb ( ABNB )) will continue to see the decline in their valuation and lower prospects of M&A, making it less attractive of an investment.

Thirdly, the headwind from the stagnating economy will likely be a tough environment for the technology sector to grow at the same speed to maintain its valuation. As the growth-rate declines and the discount rate increases (with the interest rate going up), the company's valuation is bound to come down to earth. Especially, many tech juggernauts, so-called FANGS, are facing more and more competition with each other (becoming a zero-sum game), and growth has been slowing down, as we have seen with Amazon and Facebook's (FB) painful collapse in share price after the disappointing earnings. B:C Companies like Facebook or Meta, which is a technically glorified marketing company, will have a hard time accessing and monetizing customers' data during the next decade, even though Metaverse becomes the next big thing. B:B companies (i.e., SAAS) may see decline in their pricing power as users cut down cost as the economy enters stagflation. In contrast, healthcare is, in a way, non-correlated to the general economy as people still need drugs and access to healthcare services even during the recession. For example, healthcare expenditure as a percentage of GDP has actually increased from 16.3% to 17.2% during the global financial crisis ( GFC ).

Source: Biotechvalley article

We expect continued growth in healthcare and biotech will be the fastest horse in the race

US healthcare spending has consistently grown (Peter G peterson foundation)

As shown in the chart above, even during numerous economic downturns, healthcare spending has consistently grown, which means key healthcare players, especially pharma has generated remarkable noncorrelated returns. With big pharma's R&D productivity in decline and with more patents expiring, we believe it is imperative for them to continue acquiring small biotech to replenish their pipeline, this will be the key factor driving pre-commercial SMID-cap biotech's performance during 2023.

Big pharma's war chest is full of dry powder

Big pharma is swimming in dry powder and waiting patiently to deploy it; according to an analyst from SVB Leerink, 18 large-cap and European pharmaceutical companies will have close to USD 500Bn of cash at hand by the end of 2022. Assuming small-mid cap biotech costs USD1B each, there is enough dry powder for 500 M&As. Furthermore, as big pharmaceutical companies' shares are appreciating due to sector rotation into value stocks, they will be able to raise more capital through the public market if they need to.

Big pharma is under dire need to replenish their pipeline

Worldwide total brand name prescription medications at risk from patent expiry are constantly increasing from USD16bn to close to USD28bn in 2026, according to Evaluate Pharma (page 22). This means that big pharmaceutical companies will see a high degree of revenue erosion as more copycat drugs enter the market after the patent expires. As such, there will be more pressure for those companies to aggressively acquire new clinical candidates that can plug the gap and replenish their declining pipeline.

Source: Biotechvalley article

With the COVID-19 vaccine windfall benefiting many big pharma companies (Pfizer ( PFE ), Moderna( MRNA ), AstraZeneca ( AZ )), they will start deploying their capital as deal momentum accelerates during 2023. We expect M&A activity to accelerate further with the in-person conference ongoing at the moment at the JP Morgan healthcare conference, which historically catalyzed many high-profile M&A deals that tend to prop up the biotech sector.

Examples of key biotech M&A during 2022 are listed below.

1. Amgen-Horizon

Amgen ’s recent $27.8 billion acquisition of the rare disease specialist Horizon Therapeutics takes this year’s top spot as the industry’s priciest buyout. This upsized deal lands Amgen a well-rounded portfolio of high-margin rare disease drugs, including the thyroid eye disease treatment Tepezza.

2. Pfizer-Biohaven

Pfizer ’s $11.6 billion buyout of Biohaven Pharma is the year’s second-largest M&A transaction in the industry. Through this mid-sized buyout, Pfizer gained the migraine drug Nurtec ODT, which is expected to play a vital role in the drugmaker’s battle against a slew of upcoming patent expires.

3. Pfizer-Global Blood Therapeutics

The year’s third priciest buyout is Pfizer’s $5.4 billion deal for the sickle cell disease specialist Global Blood Therapeutics . After winning a bidding war for Global Blood in August, Pfizer added the oral SCD drug Oxbryta to its diverse product portfolio.

Oxybryta is forecasted to surpass $1 billion in annual sales at its peak. However, this revenue prediction will depend on the commercial uptake of developing rival gene-edited therapies.

4. BMS-Turning Point

Bristol Myers Squibb ’s $4.1 billion buyout of Turning Point Therapeutics is the year’s fourth-largest buyout. This all-cash deal, announced last June, centered around the experimental lung cancer candidate, repotrectinib .

If approved, Wall Street estimated that repotrectinib should generate peak sales of more than $1 billion annually.

Repotrectinib, in turn, may play a vital role in the big pharma’s battle to minimize the impact of upcoming patent expires for the mega-blockbuster cancer therapy Opdivo and the blood thinner Eliquis (co-marketed with Pfizer).

5. Amgen-ChemoCentryx

Amgen’s $3.7 billion acquisition of the ChemoCentryx last August is this year’s fifth-largest deal. The impetus behind the transaction was ChemoCentryx’s FDA-approved anti-neutrophil cytoplasmic antibody-associated vasculitis drug, Tavneos.

Source: Biospace Article

For investors who want to speculate on potential big pharma M&A targets, here are the lists of potential high-quality biotechs that are top targets organized by FiercePharma.

Technology ETFs to short

We believe ARK innovation ETF is an excellent short as Cathie Wood is a remarkable manager who can pick an excellent stock to be short as most of her picks are i) non-cashflow positive companies, ii) overvalued companies with pie-in-the-sky valuation, iii) fails to predict earnings correctly, as we have seen with her piling into Coinbase ( COIN ), Tesla ( TSLA ), and Teledoc ( TDOC ) before lackluster earnings print. Other options would be shorting broad NASDAQ ETFs ( QQQ ), although there are many viable high-quality businesses on the NASDAQ100 that we would be hesitant to short.

Healthcare ETF to long

We maintain our previous recommendation around healthcare ETFs.

... for investors who don't have the expertise to pick individual stocks to buy a diversified broad biotech index like iShares Nasdaq Biotechnology ETF, SPDR S&P Biotech ETF (NYSEARCA: XBI ), First Trust NYSE Arca Biotechnology Index Fund ( FBT ), and VanEck Vectors Biotech ETF (NASDAQ: BBH ). We highlight that XBI includes more mid-cap (perhaps speculative companies such as ( BHVN ), ( CYTK ), ( TPTX ), and IBB includes safer big pharma/healthcare services (i.e., ( AMGN ), ( GILD ), ( BIIB ), ( REGN ), ( IQV ), ( VRTX ), ( ILMN )) with multiple approved candidates and solid cash flows. As such, if the market bounces, we view XBI may show a larger return, but down is also greater. We also like companies like Lonza ( OTCPK:LZAGY ) ( OTCPK:LZAGF ) (LONN), Samsung Biologics, WuXi Biologics ( OTCPK:WXXWY ) that are the key backbone to biotech/pharma R&D without any clinical risk (binary risk of stock going to zero if the trial fails). Other low-risk options would be going for drug royalties, Royalty Pharma ( RPRX ) and DRI Healthcare Trust (DHT.UN) may offer low-risk and non-correlated dividends for investors who want to avoid volatility. Tekla Healthcare has few actively managed funds available for investors interested in active stock picking. Source: Our previous article .

Risks

For further details see:

Best Macro Pairs Trade Of 2023: Short ARKK And Long Healthcare