BDX - Best New Idea For 2023: Innovate

Summary

- Today, VATE costs under $3 but is a bargain beneath $4.

- Their infrastructure business alone is worth $1.

- Life Sciences offers $15-$20 of embedded optionality.

It's rare to uncover a single investment in the new economy that's best-in-class.

To find a company that has multiple best-in-class assets is extraordinary.

- Avie Glazer, Innovate Chairman

Innovate

Innovate ( VATE ) is a holding company for a rando hodgepodge of independent non-cross collateralized assets. The wide-ranging assets include a large Infrastructure services business called DBM Global, a Life Sciences segment called Pansend, and a Spectrum business comprising local broadcast stations, and various smaller on-balance sheet assets. While ordinarily I'm drawn to companies with a clear area of focus, the messiness of Innovate Corp.'s history and holdings piqued my interest. VATE could be worth as much as $15-$20 per share and much of that value could be unlocked in 2023. Their DBM Global business provides downside protection through predictable cash flow that covers the parent company debt stack, while the Spectrum business essentially pays for itself. The Pansend Life Sciences platform has misunderstood and underfollowed assets with upside catalysts in 2023.

{kind=link}

Let's take a deeper look at Innovate Corp.'s three businesses: Infrastructure, Spectrum and Life Sciences.

Infrastructure

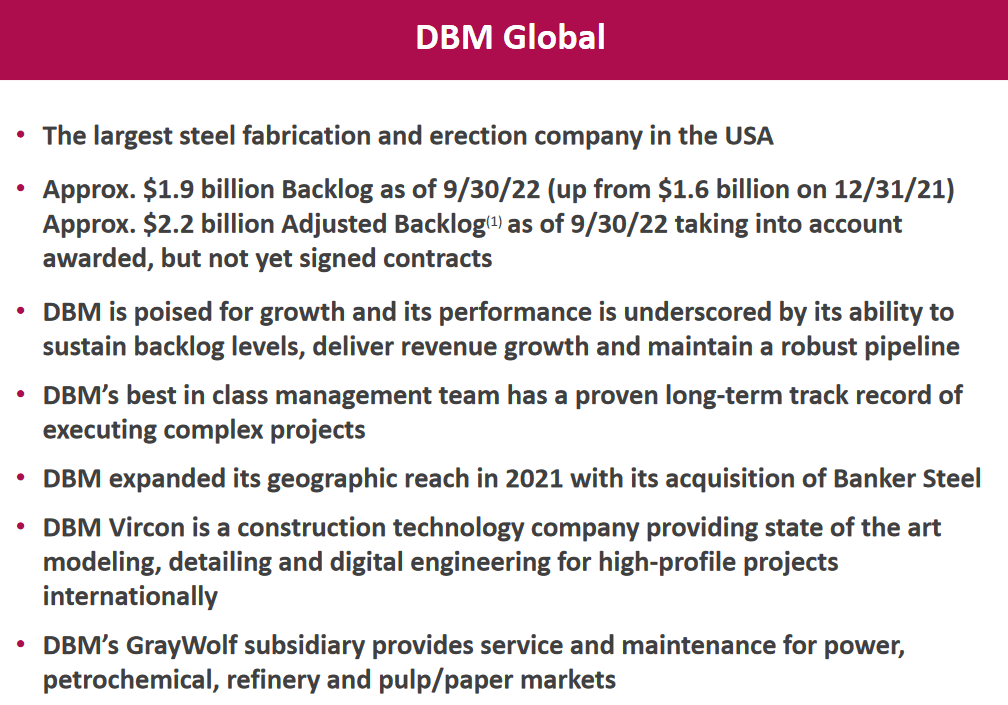

- DBM Global is the largest fabrication and erection company in US.

- Its valuation covers VATE's debt stack.

- Record-high project backlog provides insight into next 18-24 months of revenue and earnings.

DBM offers construction services on large-scale complex commercial, industrial, and infrastructure projects ranging from large infrastructure projects (e.g.: JFK Airport New Terminal One) and office complexes (e.g.: Apple global HQ, JP Morgan Chase global HQ) to large stadiums (e.g.: SOFI Stadium, LA Clippers Arena). It makes up most of VATE's current market cap.

{kind=link}

{kind=link}

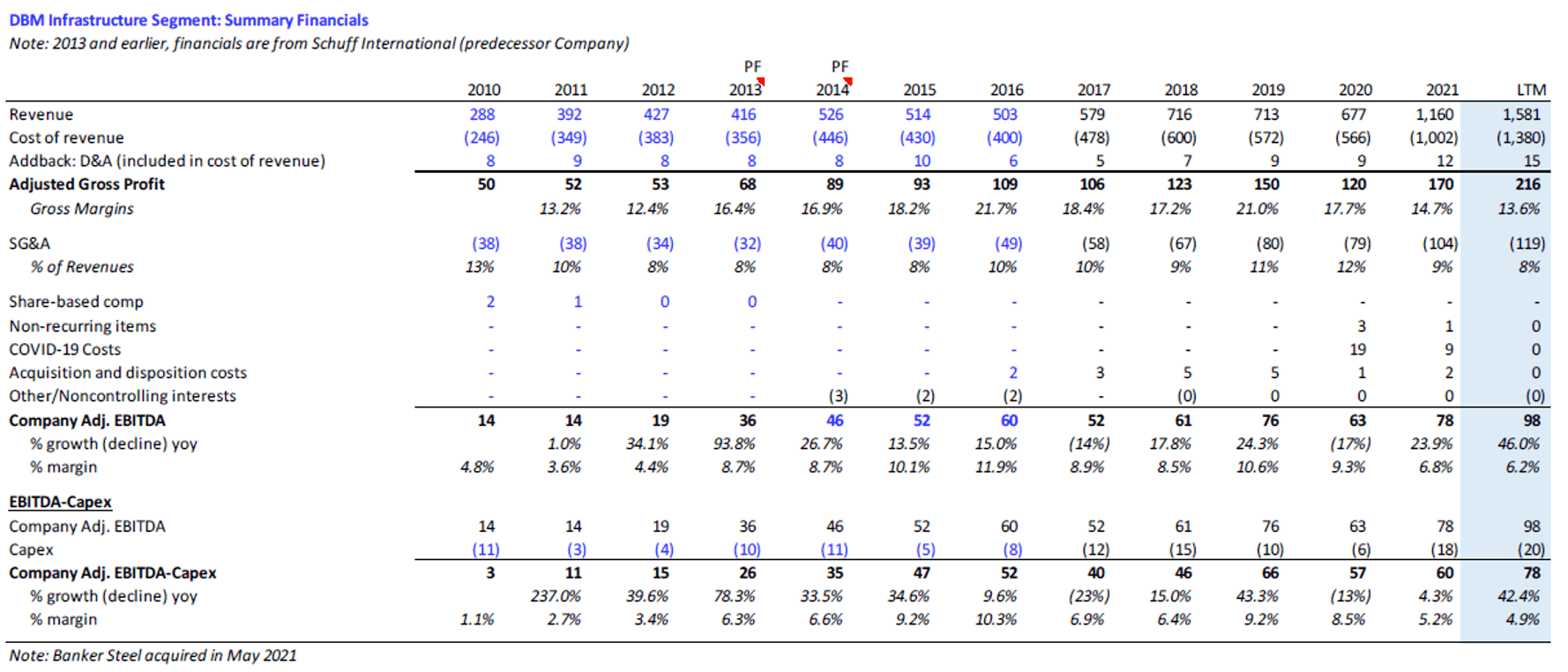

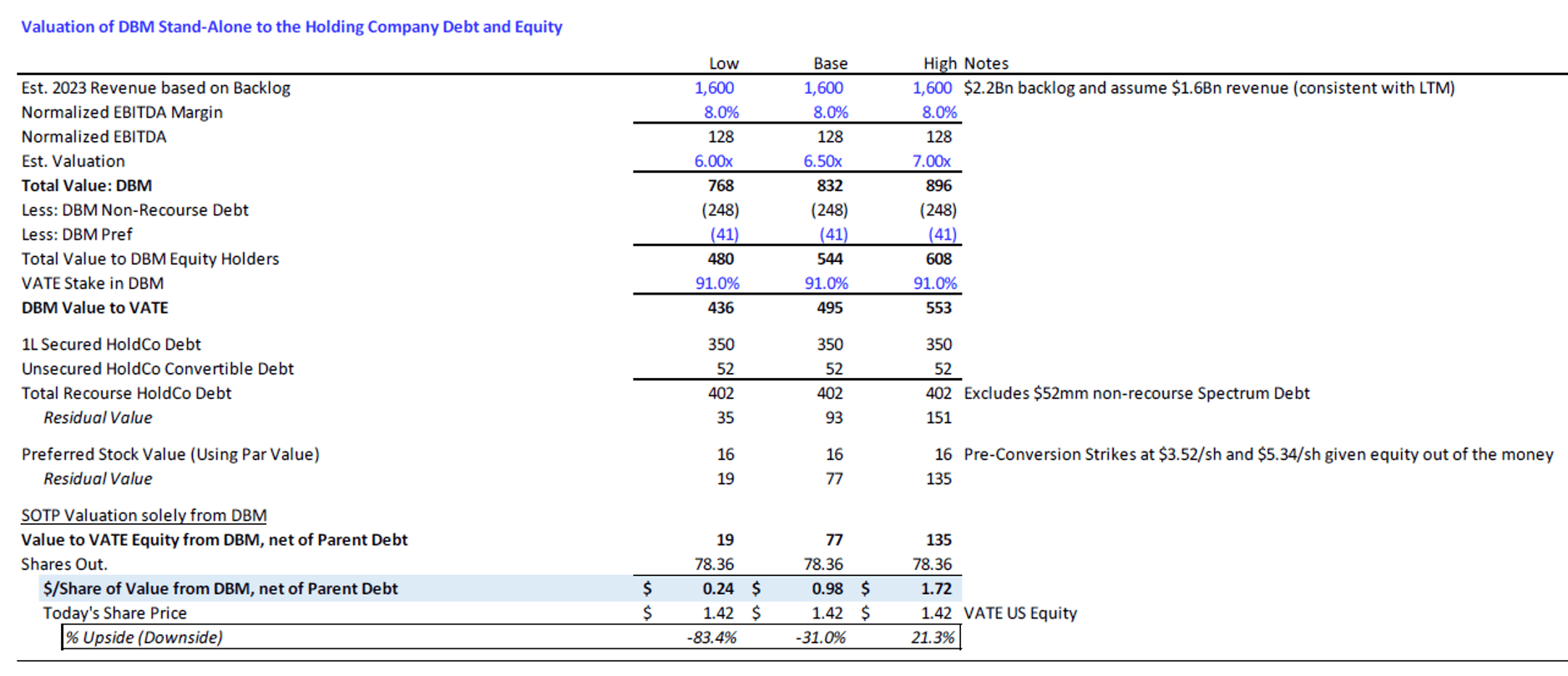

In addition to covering the debt stack, DBM Global offers another $1 or so of value for equity holders. This gives us some downside protection vs. a $1.29 share price as of this writing. DBM is worth a 6-7x EBITDA multiple, an 8% normalized EBITDA margin, and run-rate revenues of $1.6 billion. This EBITDA margin is below the average since 2015 of about 9.5%. The relatively modest EBITDA multiple has generated positive EBITDA-capex in every year over the past decade, with low capex intensity at only 1.3% of sales, and EBITDA-capex margins ranging between 5-10% of sales over a cycle. DBM is shifting to larger, more complex projects which could result in margins closer to 10%-11% as we saw in 2019-2020.

DBM requires a considerable working capital investment as their project backlog grows, generating a near-term liquidity drain. However, point of sale contract margins have normalized, justifying the return on investment, and the higher working capital balance has been offset by an increase in the DBM revolver secured by working capital assets. Conversely, if the project backlog were to decelerate in a US recession, the accompanying reduction in working capital should be cash flow generative.

In May 2021, DBM completed its acquisition of Banker Steel, giving it a full national presence from coast to coast in the US, a much bigger backlog, and additional operating synergies. DBM paid roughly 4.5x EBITDA for Banker Steel which was about half the size of DBM. DBM made an opportunistic purchase at a favorable price (announced in March 2021 during pandemic) from an existing private equity sponsor at the end of its investment life cycle, and therefore the Banker Steel acquisition multiple is not reflective of the pro forma valuation multiple warranted by DBM Global.

When DBM acquired Banker Steel, the pro forma backlog was $1.5 billion. However, given the success and integration of the team, the backlog today stands at $2.2 billion, giving DBM very strong medium-term foresight into revenue and free cash flow generation. Complex large-scale construction projects take 18-24 months to complete, so the pipeline provides earnings visibility through 2024. Operating results typically lag a recession given the contracted backlog, and any reduction in future backlog should generate cash flow as working capital is released.

DBM seeks to lock in commodity costs when it prices and signs a new contract, and its labor costs are generally subject to collective bargaining agreements that are fixed over certain time periods, limiting the risk of major cost overrun issues on construction projects in an inflationary environment. DBM's historical financials (including predecessor company financials and pro forma for Banker Steel) over the past decade indicate a well-managed company that has generated cash flow in every year, including during the COVID-19 pandemic in 2020, although EBITDA margins have varied from 5%-10% over the course of the business cycle and due to business mix with larger, more complex projects capturing higher margins.

Sell-side analysts focus on historically weak trailing EBITDA margins, further discounting their future projections based on expectations in a recession. This approach does not account for the time lag created by the project backlog. The weak EBITDA margins reported over the last several quarters resulted from the low-margin backlog contracted during the depths of the pandemic in 2020. Unsurprisingly the demand for capitalizing complex large-scale construction projects froze during the pandemic, forcing DBM to fill its project backlog with lower contracted margins that take 18-24 months to complete. The flip side of this is the roaring demand that surged upon the re-opening from the pandemic, resulting in a record backlog of $2.2 billion contracted at the high point of sale margins. Notably, in 2019 and 2020 when DBM had large and complex projects in its backlog, EBITDA margins ranged from 9%-11%. Mid-cycle normalized EBITDA margins are 8%-9%, with upside potential due to business mix scale and complexity.

The base case valuation uses an 8% EBITDA margin on a normalized basis which is beneath the 2015-2021 average of 9.5%, resulting in $128 million projected EBITDA for 2023.

{kind=link}

The market is overly focused on DBM Global's trailing earnings and trailing margins, which include notably below-market contracts entered into during the pandemic and rolling off by early 2023. If everything else at VATE goes horribly wrong, Infrastructure is what will salvage some value for shareholders.

Spectrum

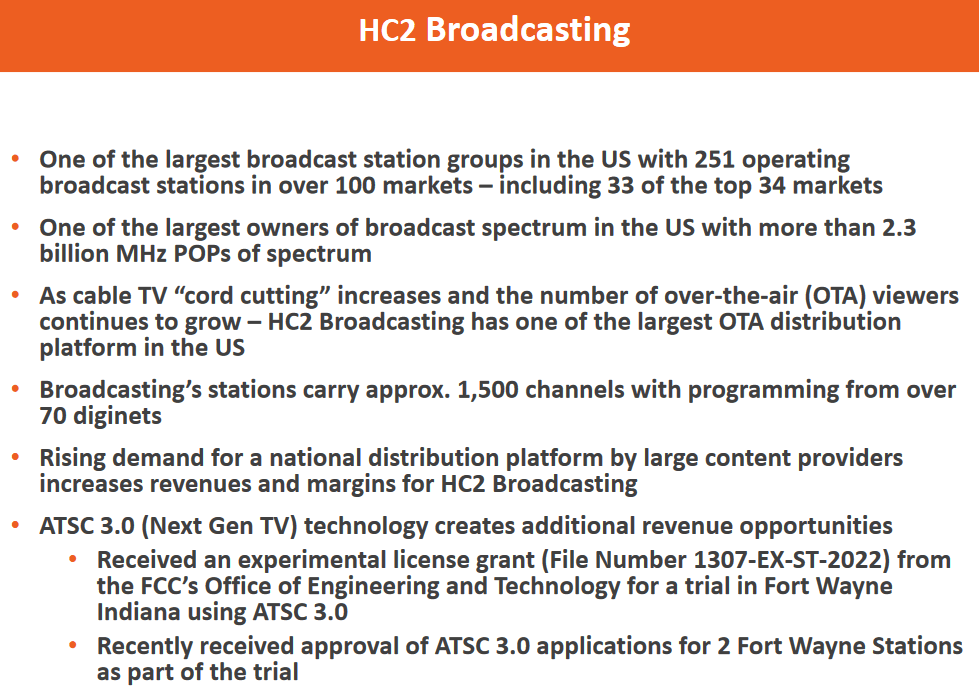

- One of the largest broadcasting groups in the US.

- Worth its cost; maybe more in a sale.

HC2 Broadcasting, representing VATE's Spectrum business, is one of the largest broadcast station groups in the US, as well as one of the largest owners of broadcast spectrum. With 251 local broadcast stations with 2.3 billion MHz POPs, HC2 offers upside optionality as a spectrum repurposing play. Conservatively, it is valued at cost. Spectrum-related debt is non-recourse to the parent company. Ultimately, this asset offers the most value to a strategic acquirer with the resources to develop and repurpose spectrum.

{kind=link}

Life Sciences

- Pansend Life Sciences is where there is real sizzle.

- MediBeacon's TGFR offers game-changing kidney monitoring; could receive FDA approval.

- R2's Glacial RX seeks a corner of the $22 billion global aesthetic dermatology market.

- BeneVir represents an embedded CVR, a wild card opportunity at no cost to valuation.

{kind=link}

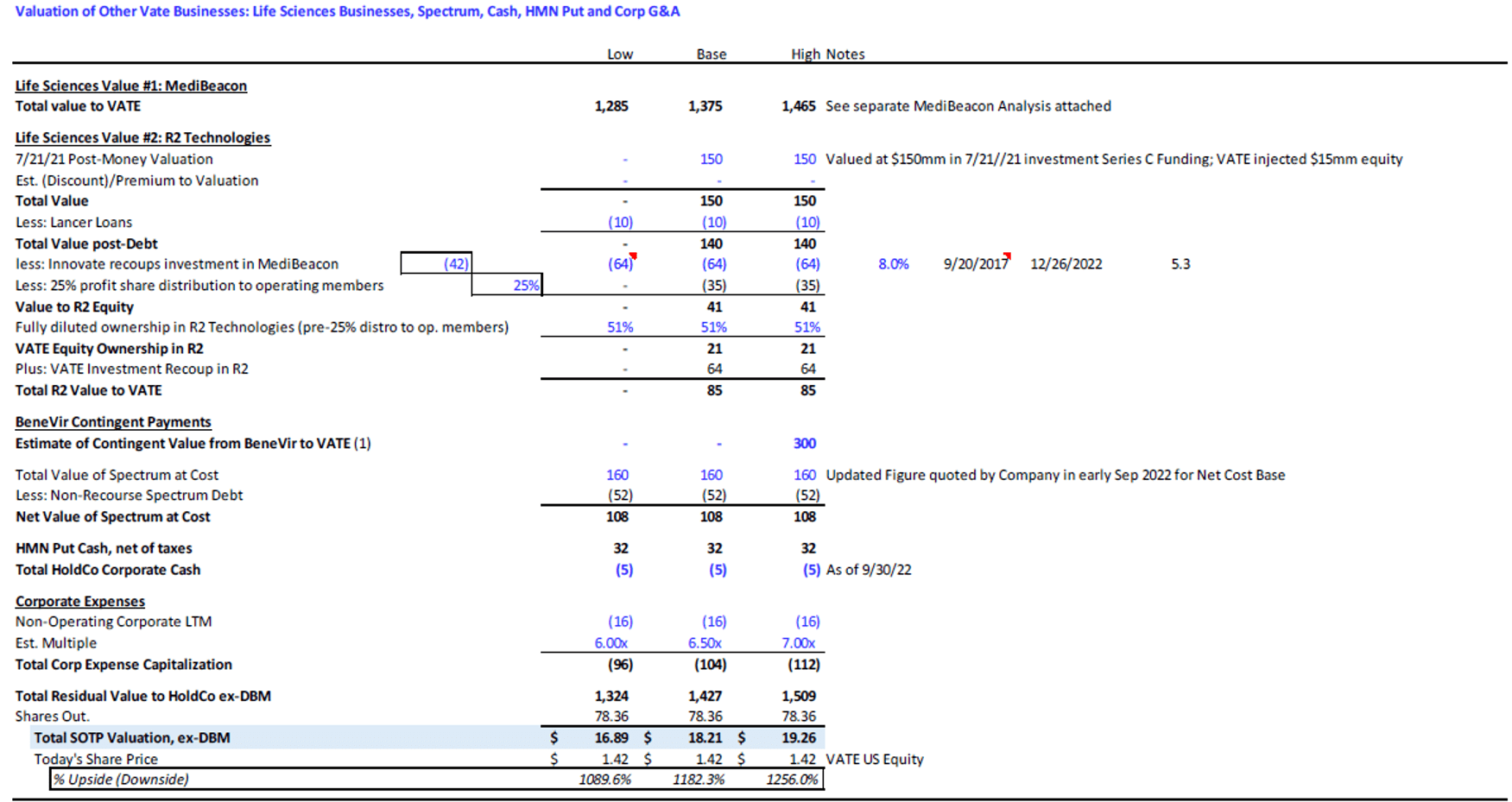

VATE's Life Sciences segment offers numerous upcoming shots on goal. It is compelling and misunderstood, most notably MediBeacon, which could be worth $16-$19 per share on its own . Value from each business is non-cross collateralized to the holding company. It comprises four investments. VATE owns 75% of Pansend's economic distributions after priority return of invested capital plus an 8% hurdle rate. Both MediBeacon and R2 Technologies could be worth significantly more than the market appreciates. A legacy CVR in BeneVir provides a little kicker to Pansend's value.

VATE

MediBeacon

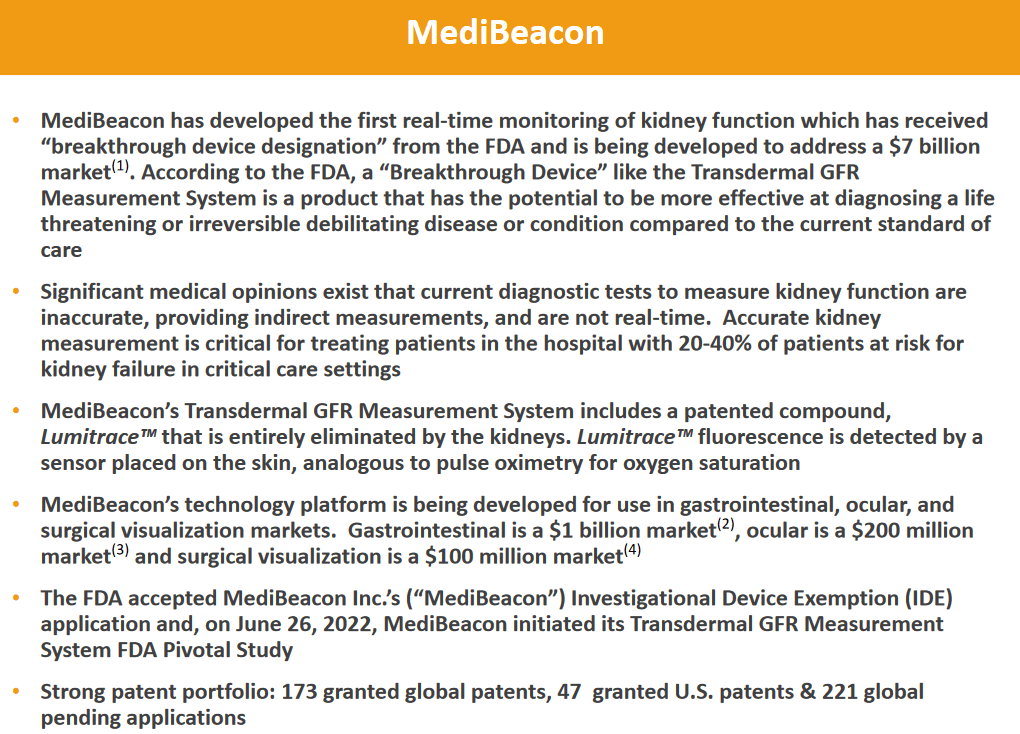

MediBeacon represents the biggest opportunity in Pansend's life sciences stable. MediBeacon's Transdermal Glomerular Filtration Rate ("TGFR") System is a non-invasive monitoring system for kidney function evaluation. Chronic kidney disease (CKD) affects over 850 million people worldwide. The TGFR System offers real-time kidney function monitoring by combining optical skin sensors with Lumitrace, a patented proprietary fluorescent tracer reagent administered intravenously. The results provide an additional vital sign for use in clinical diagnostics similar to an EKG for monitoring heart function.

The FDA granted MediBeacon a Breakthrough Device designation in October 2018, which allows the FDA to work with MediBeacon to expedite regulatory review and give more timely access to novel use technologies. For the past 30 years, a measure of the kidneys' ability to filter wastes, the glomerular filtration rate - GFR, could be determined only generally. The measured level of the protein creatinine in blood tests would be inputted into a regression equation based on various factors including age, gender, ethnicity, and body mass to estimate GFR. While this methodology generally works well in stable patient populations, it breaks down in acute care settings where patients have step-function declines in GFR due to comorbidities, creating a lag in patient assessment in the ICU. MediBeacon's TGFR device would allow for real-time monitoring of GFR in the acute care ICU setting, a potential game-changer in clinical diagnostics. In short, it's better. Other applications include measuring potential kidney damage from radiocontrast agents in cardiac catheterization, measuring perioperative kidney damage in cardiac surgery, monitoring kidney function and organ rejection in transplants, and delaying End Stage Renal Disease (ESRD) in Chronic Kidney Disease (CKD) patients.

Currently, MediBeacon is nearing completion of a Pivotal Study in the US and recently presented preliminary abstract results at the American Society of Nephrology Kidney Week in Nov 2022 that were extremely robust. After completion of the US Pivotal Study in the first quarter, look for the Premarket Approval - PMA - submission to the FDA and potential FDA approval by yearend.

MediBeacon entered into an exclusive commercialization partnership with Huadong Medicine (ticker 000963 CH), a publicly-listed Chinese pharmaceutical company with $11 billion market cap, relating to TGFR in Greater China in 2019, and Huadong invested $25 million equity capital in MediBeacon to date, plus non-dilutive advances against future royalties in Greater China. As of the second quarter of 2022, MediBeacon had 164 granted global patents, 46 granted US patents, and 212 global pending applications.

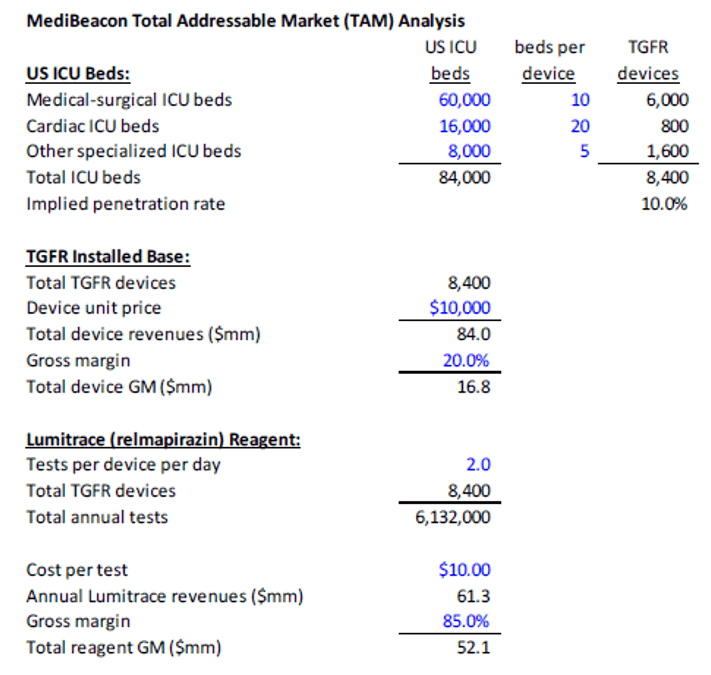

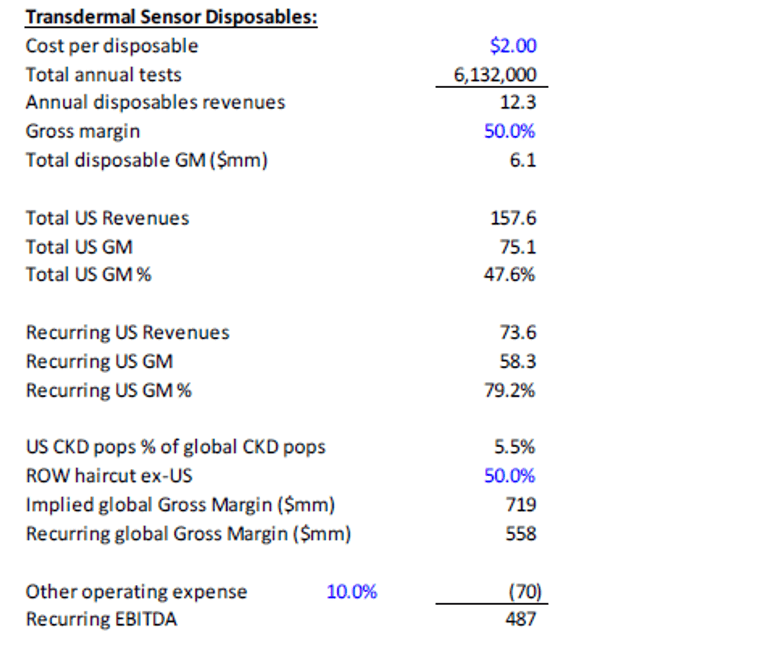

There's a significant global total addressable market for MediBeacon's TGFR device based solely on ICU applications. It will be a proprietary closed system razor/blade model where the majority of economics are derived from high-margin pull-through of Lumitrace reagent and disposable sensors. Given the annuity nature of reagent revenues and high margins, these business models typically warrant high valuations. For example, hospital clinical diagnostics company Becton Dickinson ( BDX ) trades at 17x forward EBITDA. The takeaway from the analysis below is that MediBeacon alone could be worth $16 to $19 per VATE share.

{kind=link}

{kind=link}

{kind=link}

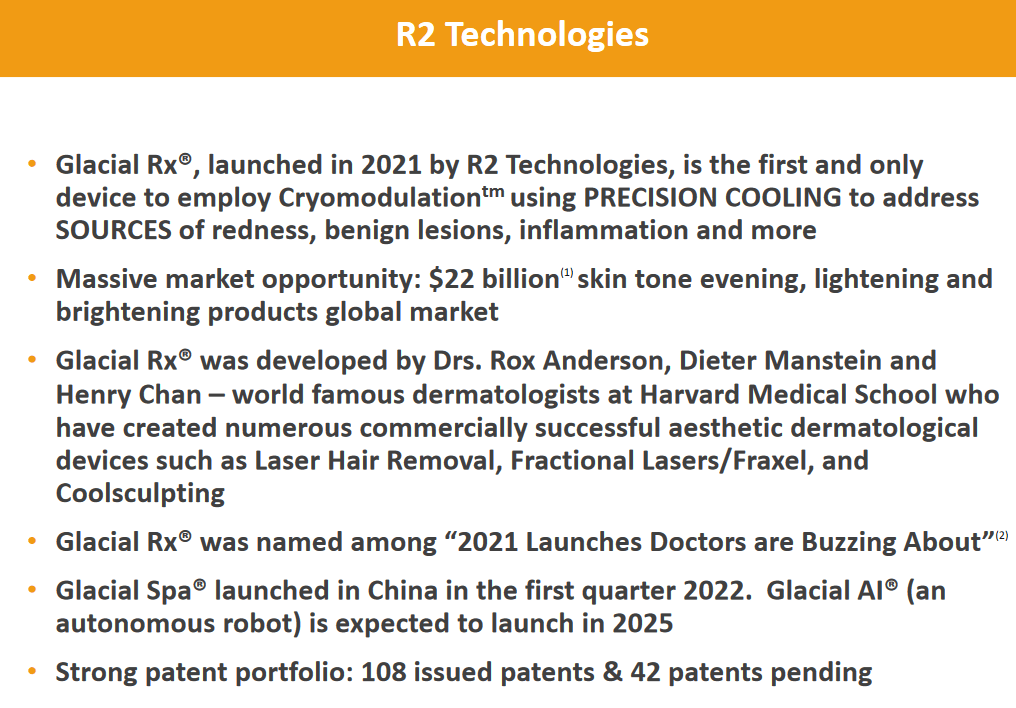

R2

In addition to MediBeacon, Pansend has majority ownership of R2 Technologies, an aesthetic dermatology company. R2's FDA-cleared device, the Glacial Rx platform, applies Cryomodulation (a patented cooling technology) to remove age spots, as well as lighten and brighten skin. Using a conservative valuation from R2's July 2021 post-money valuation of $150 million would place VATE's ownership stake around $85 million. But those numbers only tell a partial story.

R2 received FDA approval in September 2020, following Chinese government approval in June 2020. R2 commenced commercial sales of Glacial Rx devices in 2022 and shipped 215 Glacial devices to customers globally through the third quarter of 2022. Similar to MediBeacon, R2's main investment partner is Huadong Medicine, which has invested $30 million equity to date. As of the second quarter of 2022, R2 had 105 issued patents and 46 patents pending (numbers in slide below slightly newer). Glacial RX was developed by the same dermatologist team at Harvard Medical School that developed, took public in an IPO, and ultimately sold Zeltiq Aesthetics (CoolSculpting) to Allergan at about 7x revenues for $2.5 billion in 2017.

As these devices go to market, VATE could enjoy a substantial upside convexity in R2's value. Getting rid of age spots is the holy grail in aesthetic dermatology and represents a $22 billion global market opportunity. This could wildly overperform expectations.

{kind=link}

BeneVir

Finally, hidden in the folds of Pansend Life Sciences is a wild card stemming from the Company's 2018 sale of cancer immunotherapy startup BeneVir to Janssen Biotech (part of Johnson & Johnson JNJ)). The sale was for $140 million upfront cash plus contingent payments of up to $900 million based on achievement of certain regulatory and sales milestones. They include up to $250 million of gross payments for various regulatory approvals and up to $650 million of gross payments for certain revenue targets. Pansend owned 76% of BeneVir when it was sold, and VATE is eligible to receive 75% of the proceeds that Pansend receives from any of these contingent payments. Effectively, BeneVir represents an embedded contingent value right - CVR - within VATE. While it's safe to presume no value in the BeneVir CVR in a base case for VATE's valuation, it offers one more shot on goal.

{kind=link}

History

How the hell did we get here? Formerly known as HC2 Holdings, Inc., VATE is roughly 29% owned by Chairman of the Board, Avram Glazer and his Lancer Capital investment entity. Glazer began his involvement in VATE in 2020 after an activist campaign was launched by another shareholder against the prior CEO, Phil Falcone, alleging gross mismanagement and self-dealing at the company.

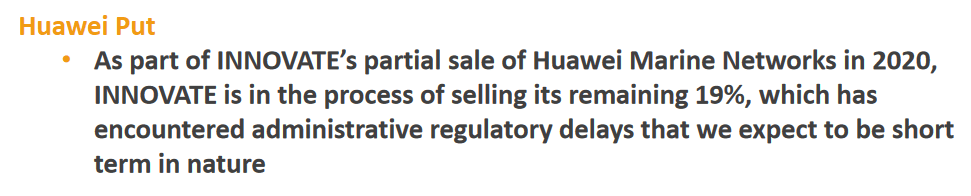

In June 2020, Falcone was removed from the HC2 board and exited the company after a successful dissident proxy fight (HC2 was subsequently renamed Innovate Corp. in Sep 2021). Since summer 2020, the company attempted to simplify an overly complex and poorly capitalized corporate and capital structure. They sold a 30% stake in Huawei Marine Networks ((HMN)) with a remaining put option for $32 million in net cash proceeds expected to be received in by the second quarter of 2023.

In November 2020, VATE faced liquidity pressures and had to issue a $65 million equity rights offering at a then deeply discounted price of $2.27 per share (well above today's stock price). Glazer/Lancer purchased over 50% of his current position through backstopping that rights offering. Glazer's overall cost basis based on 13D filings is about $2.78 per share, roughly double today's stock price.

VATE sold their Clean Energy subsidiary Beyond6 and their insurance business Continental Insurance Group. They refinanced expensive 11.5% Notes into 8.5% Notes termed out to a 2026 maturity. They acquired Banker Steel, a competitor to DBM, to add scale and cash flow to the infrastructure business, enabling runway for the Life Sciences business options to play out. These deals simplified the sum-of-the-parts story, leaving a large cash-flowing Infrastructure services business, a Life Sciences business that remains misunderstood, underfollowed and valuable, and a Spectrum broadcast business. In addition, the company termed out its capital structure at lower interest rates, allowing liquidity runway to realize step-function event catalysts in the Life Sciences segment in 2023. That's how we got here.

Pill

Expiration of the poison pill Tax Benefits Preservation Plan on March 31, 2023, will remove constraints on purchasing VATE stock and should improve liquidity in the shares. The company has a Tax Benefits Preservation Plan in place that was adopted on August 30, 2021, to protect the valuable NOLs and Section 163j interest limitations of the Company. This primarily includes the company's $165 million Federal NOLs and $223 million under Section 163((J)) limitation carryforwards as of the end of 2021. Under the Tax Benefits Preservation Plan, any person or group is deterred via a poison pill from acquiring beneficial ownership of 4.9% or more of VATE outstanding common stock to prevent a change of control that would jeopardize valuable tax attributes. The test for change of control is calculated on a three-year rolling basis under applicable regulation. Glazer applied to the Board of the company for a waiver of the Tax Benefits Preservation Plan to purchase an additional 3.3 million shares in May 2022, when VATE stock was at $2.40 per share. This request was subsequently denied by the Board. The Tax Benefits Preservation Plan will expire on March 31, 2023, by which time the rolling 3-year calculation for change of control purposes will exclude large legacy stock purchases by Glazer and another activist investor.

Red Devils

Glazer's family also owns a 60% economic stake in publicly listed soccer club Manchester United ( MANU ), the Red Devils. Avram Glazer personally owns 10.1% of the shares outstanding, which is about $375 million at today's market price based on a total market cap of $3.7 billion. In November 2022, MANU confirmed press reports that the team is exploring a sale in full or in part. Reports of sale prices for MANU have ranged from $4-7 billion. A potential monetization of his MANU stake would provide Glazer with a substantial cash windfall for redeployment, which may include acquiring more VATE shares or funding commercialization of MediBeacon's TGFR device.

Liquidity

Will VATE make it? Probably. Near-term liquidity appears tight, but the company should be able to get past their February 2023 interest payments without the need to raise dilutive capital (and if I'm wrong and they need it, I hope to provide it). The term structure of the debt stack (other than Spectrum debt which is non-recourse to VATE) has largely been termed out to 2026 maturity.

The company has various levers to tap additional liquidity including borrowing against working capital at DBM and incremental tax sharing payments from DBM to utilize consolidated tax NOLs offsetting taxable income. DBM's EBITDA margins should normalize to 8% over the coming quarters with high point of sales contracts and a robust backlog, further improving cash flow generation and easing liquidity constraints.

Additionally, VATE benefits from an expected inflow in the fourth quarter of 2022 or the first quarter of 2023 from a put option tied to the sale of its remaining legacy stake in undersea cable company Huawei Marine Networks ((HMN)), its 49% joint venture with Huawei Technologies, to Hengtong Optic-Electric (ticker 600487 CH). The first tranche sale of 30% closed in May 2020 and the remaining 19% interest is subject to a put option exercisable after Oct. 31, 2022. The company is actively asserting this put option and is awaiting certain China regulatory approvals to close the transaction and receive the net $32 million after-tax proceeds owed under this agreement. Payment of the February 2023 interest payments is not dependent upon the $32 million put obligation net cash proceeds from HMN, but receipt of such proceeds would further bolster liquidity. Once the company satisfies the February 2023 interest payments without requiring dilutive capital, we believe the bankruptcy/dilution overhang on VATE stock will lift, and market attention will refocus on the pending catalysts for MediBeacon.

{kind=link}

Catalysts

What's next? Key upcoming catalysts in 2023 primarily relate to the likely FDA approval of MediBeacon's Transdermal Glomerular Filtration Rate (TGFR) System, which could focus market attention on a groundbreaking novel use technology with a large global total addressable market. As a clinical diagnostics device, the TGFR System should not trigger lack of efficacy or safety concerns often raised in FDA reviews. This fact, coupled with the FDA Breakthrough Device designation and clinical use applications in acute care hospital ICUs, are likely to expedite FDA review and ultimate approval upon Premarket Approval ((PMA)) submission after completion of the US Pivotal Study in the first quarter of 2023. In addition, we could see a further commercialization ramp in R2's Glacial Rx device throughout 2023.

6 Milestones to Watch for in 2023

- By Q2: $32mm in HMN put obligation net cash proceeds likely received

- By Q2: MediBeacon TGFR US Pivotal Study likely completed and PMA submission to FDA

- By Q3: Tax Benefits Preservation Plan expires March 31, 2023, removing constraint on VATE stock purchases and increasing liquidity in shares

- Q2-4: Margins up at DBM after underpriced COVID-era contracts roll off

- Q3-4: MediBeacon likely gets FDA Approval for TGFR System

- Q1-4: Commercialization ramp of R2's Glacial Rx device

Value

Here's what actually matters. While DBM provides stable cash flows that anchor downside, there's highly convex upside from the Life Sciences segment, especially MediBeacon. A likely FDA approval could refocus the market on the large global total addressable market for the TGFR System, leading to a significant re-rating in VATE stock and potential monetization of MediBeacon.

The sum of the parts valuation including DBM Infrastructure, Life Sciences including MediBeacon and R2, and the Spectrum segment (based on historical acquisition cost net of non-recourse Spectrum debt) implies a value of $15-$20 per share. There are multiple independent non-cross-collateralized assets that may result in substantial residual value to VATE equity, providing multiple ways to win.

{kind=link}

{kind=link}

{kind=link}

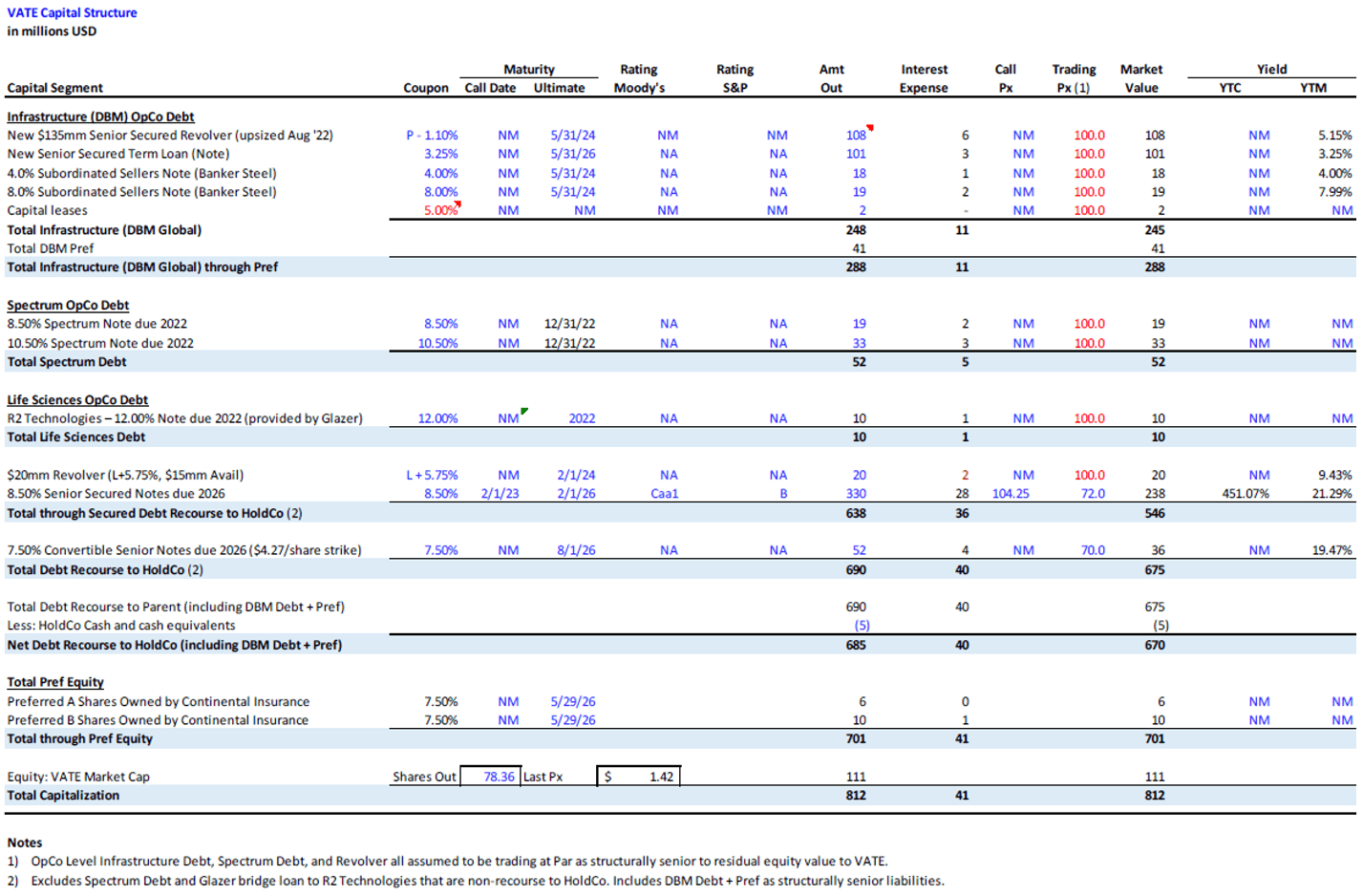

While VATE is leveraged on a consolidated basis, overlaying the corporate structure on the capital structure reveals that debt at the DBM Infrastructure business and the Spectrum business is non-recourse to the parent company, with virtually no debt at Life Sciences (other than a non-dilutive $10 million bridge loan from Glazer to fund commercialization ramp of Glacial Rx at R2), allowing for significant non-cross-collateralized asset value from MediBeacon and R2 to flow up to the parent holding company, affording multiple ways to win. $330 million 8.5% due 2026 First Lien Bonds at the parent holding company are currently quoted around 72 cents yielding 20%+, which is an attractive risk/reward given multiple avenues for residual value to flow up to the parent company. $50mm 7.5% due 2026 Unsecured Convertible Notes at the parent holding company are currently quoted around 70 cents, providing about an 11% current yield with a strike price of $4.27 per share. If either MediBeacon or R2 is successful, the convert strike will likely be in-the-money. While both the 1L Bond and Unsecured Convert are attractive paper, the best security at current prices is the VATE common equity given it is levered to the same risks yet benefits from much more upside.

{kind=link}

Caveat

Innovate is a leveraged equity with bonds trading at distressed prices implying that the common could be at risk. The long thesis is a variant view on what they're really worth, why, and when we could see their value revealed. All of the normal warnings apply to this, my best new idea for 2023. But it's entirely possible that the market is right and I'm wrong. It's even possible for this to go bankrupt, in theory as early as next quarter. I can't escape my own judgment but you can!

More likely, the idea works but the timing is off. If now isn't optimal (I think it is) then perhaps optimal is well into 2023 (maybe in a secondary). And maybe this one works for the bonds but not the stock. So I presented what I think (the common is a huge bargain and opportunity) and what I've done (buy a lot of it). While perhaps I'm wrong, you might be able to glean some value from it for other purposes - a bond investment, equity later/lower perhaps in new shares, or a cautionary tale to use when you teach your kids that they're better off in an index fund . Heck, you might even like this as a short idea (but that would require a far more dramatic caveat section to what would be a fabulously dangerous short!).

Conclusion

If you can buy VATE at or beneath $4 by early 2023, you can risk about $3 for a potential reward of at least $11. It is a leveraged equity, but that cuts both ways. Size accordingly. The infrastructure business is worth about $1 and can help avoid bankruptcy. MediBeacon, R2 Glacial Rx, and other Life Sciences opportunities are where you could make a multiple on your investment in 2023. At scale, they could be spun off to highlight their value. Discounting the varying ways for this to win or lose, it's probably worth closer to $8, a value that it could hit along the way to achieving its six 2023 milestones.

TL; DR

Buying VATE under $4 per share is StW's best new idea for 2023, and - we'll see what happens - just perhaps my best idea ever .

For further details see:

Best New Idea For 2023: Innovate