WHITF - Bet On Dirty Energy: Whitehaven Coal

2023-10-29 08:14:51 ET

Summary

- Whitehaven is an undisputable leader in its peer group. It achieved 82% free cash flow yields at 4.2% CAPEX/Revenue. These numbers mean the company has abundant firepower for expansion.

- Acquiring BMA assets will transform Whitehaven into a metallurgical coal leader. New mines will increase the company's resource base by 75%. The recoverable reserves will grow by 29%.

- Whitehaven is a hidden gem. It offers excellent liquidity and solvency and, at the same time, realize double-digit ROI and ROE.

- Despite the company's qualities and generous dividends, Whitehaven has been trailing for twelve months. The company is deeply undervalued against its past metrics and regional peers.

Introduction

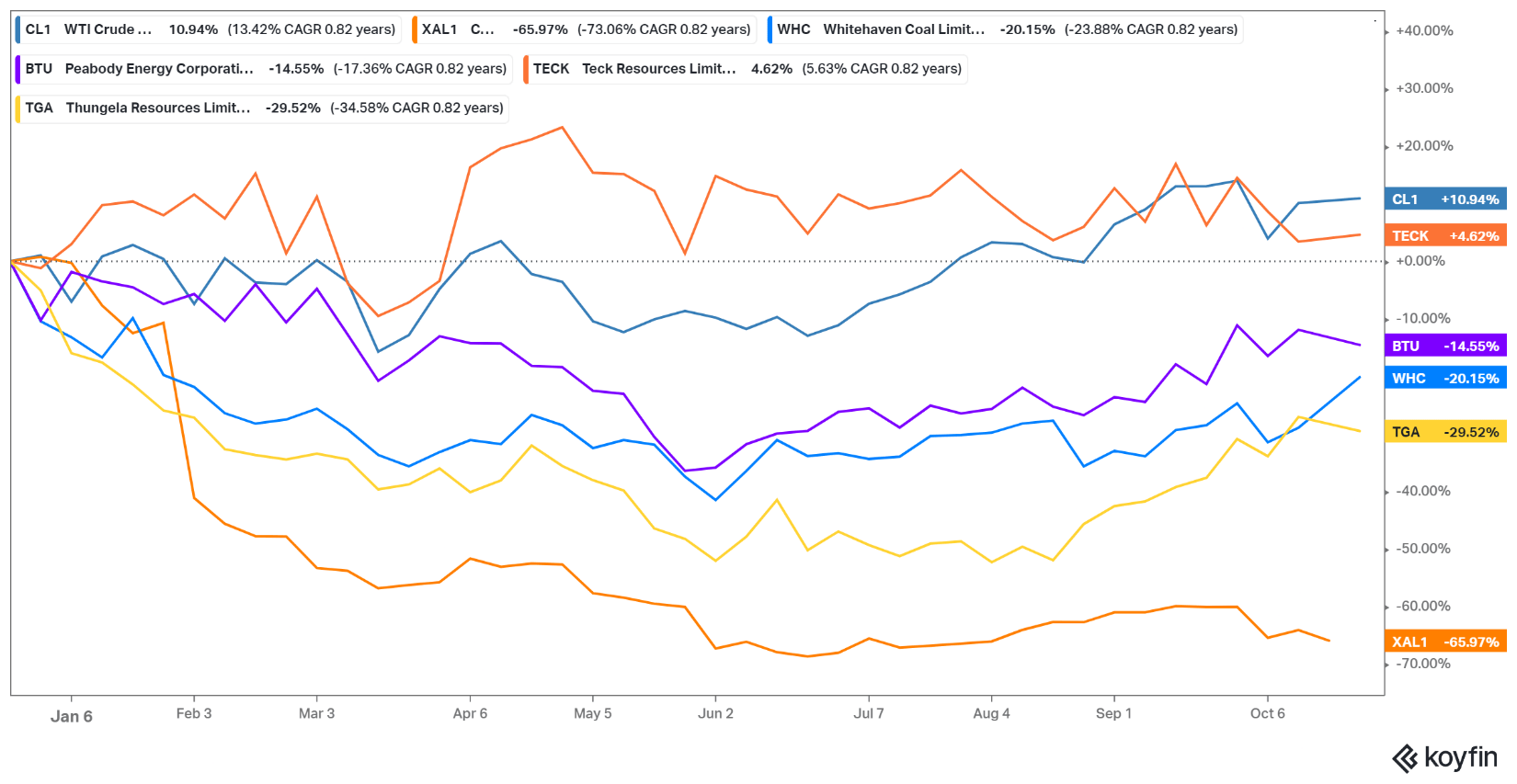

Coal stocks are lagging behind their uranium and fossil fuel counterparts. However, the picture is not that bad. Despite the low coal prices, the coal miners managed to maintain their standing, as seen in the image below:

{kind=link}

XAL1 (coal prices) had declined 65.9% YTD. However, coal miners performed adequately, given the coal prices. Thungela (TNGRF)[TGA], Whitehaven (WHITF), and Peabody ( BTU ) declined by 14 to 30%. I added Teck is not coal pure play, though it is one of the largest metallurgical coal producers moved sideways.

Whitehaven is among the top players in that game. Whitehaven announced its plans to acquire Daunia and Blackwater metallurgical mines from BMA ( BHP subsidiary ). Both mines will expand the company`s reserve base and push its assets LOM further, as seen in the chart below. Whitehaven will transform into one of the primary producers of metallurgical coal. The company offers a bulletproof balance sheet, exuberant profit multiples, and pays dividends. The company is deeply discounted against its peers and its past multiples.

Whitehaven at glance

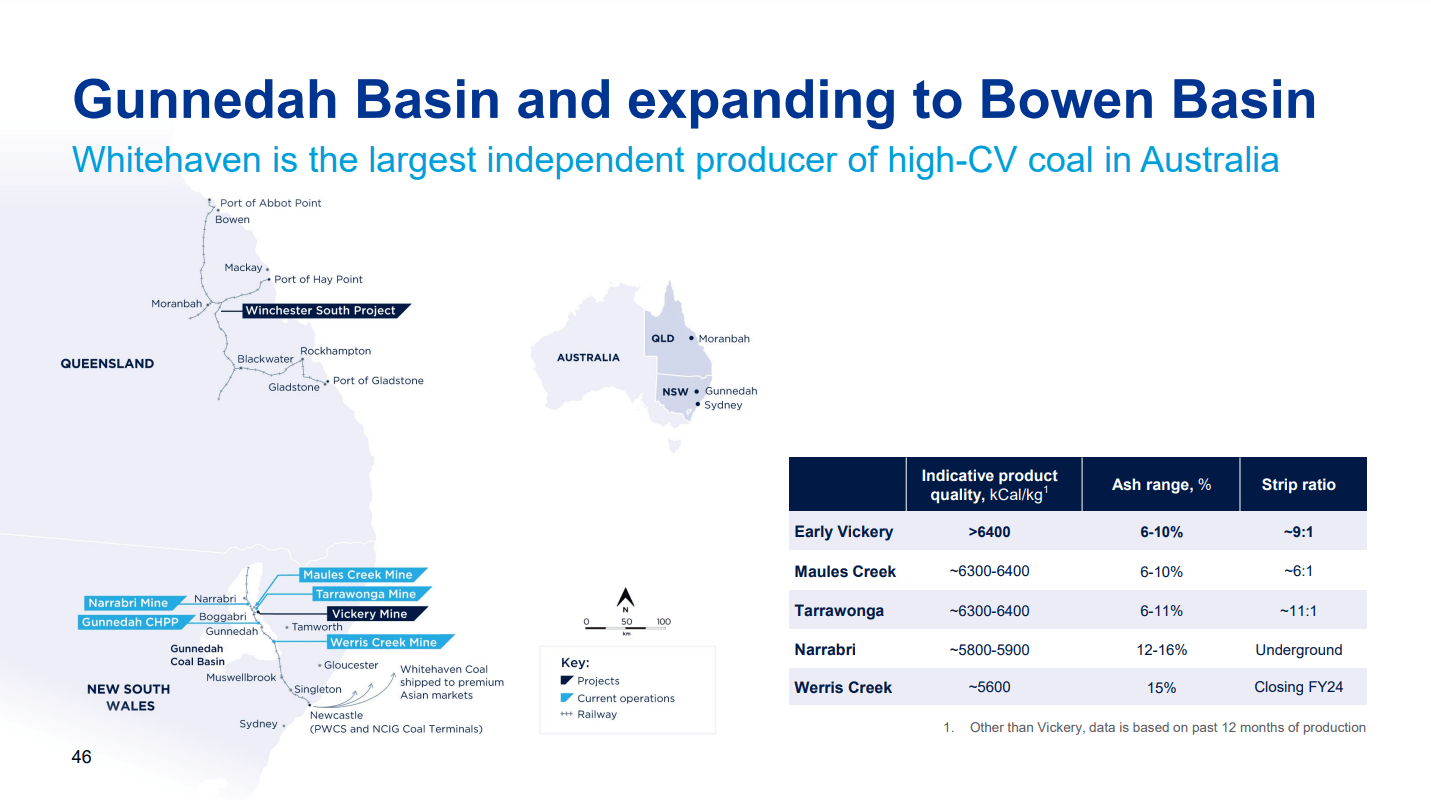

The focus today is on Whitehaven Coal. It is an Australian coal mining company. The image below from the last presentation shows the location of the company`s mines.

{kind=link}

The company has five operating mines:

- Narrabri

- Gunnedah

- Maules Creek

- Tarrawonga Mine

- Werris Creek

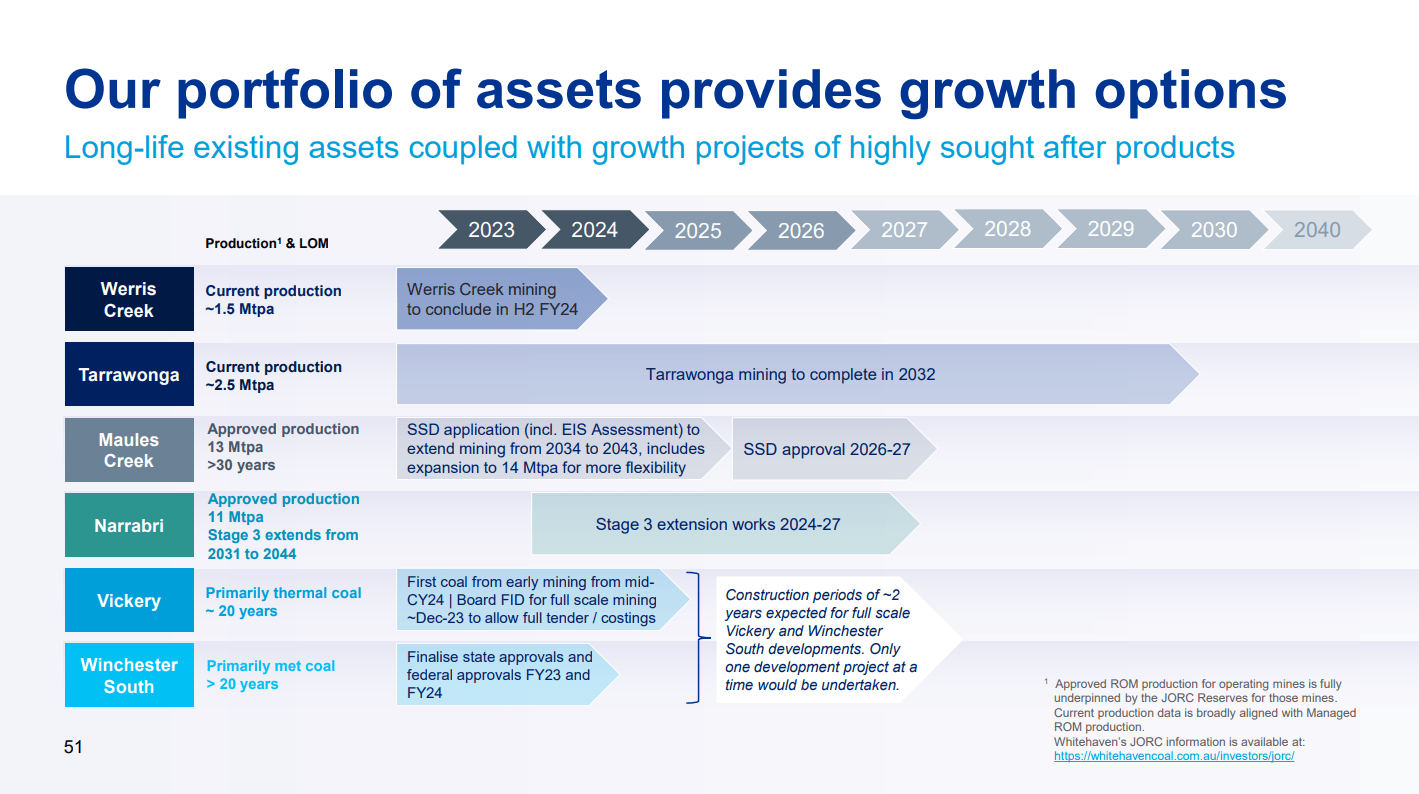

The company's assets include several developing mines: the Vickery, near Gunnedah, and Winchester South, in Queensland's Bowen Basin. The Vickery Extension Project is an underground mine planned to be constructed approximately 25km north of Gunnedah. Whitehaven's future projects are shown in the graphic below:

{kind=link}

In the long term, Whitehaven has sufficient reserves to expand its production. Its mines have a LOM of over ten years and produce 18.2 million tonnes annually. Plans for next year are for output to reach 18.7-20 million tonnes.

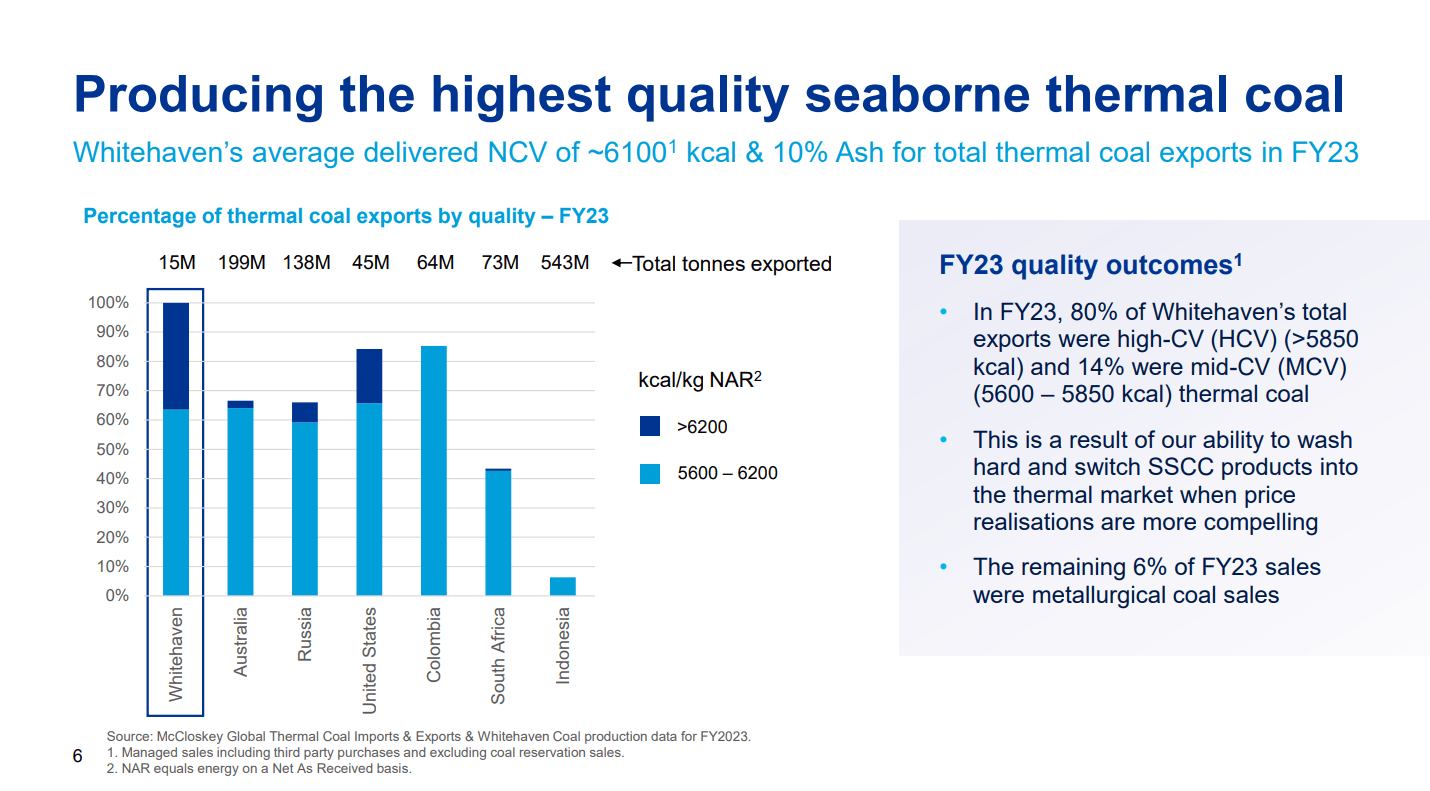

Whitehaven is among the highest-quality coal producers measured by Net As Received ((NAR)). This parameter accounts for the calories of energy contained in one kilogram of coal. The following graph shows that Australia produces some of the highest calorific value coal, and Whitehaven outperforms the national average.

{kind=link}

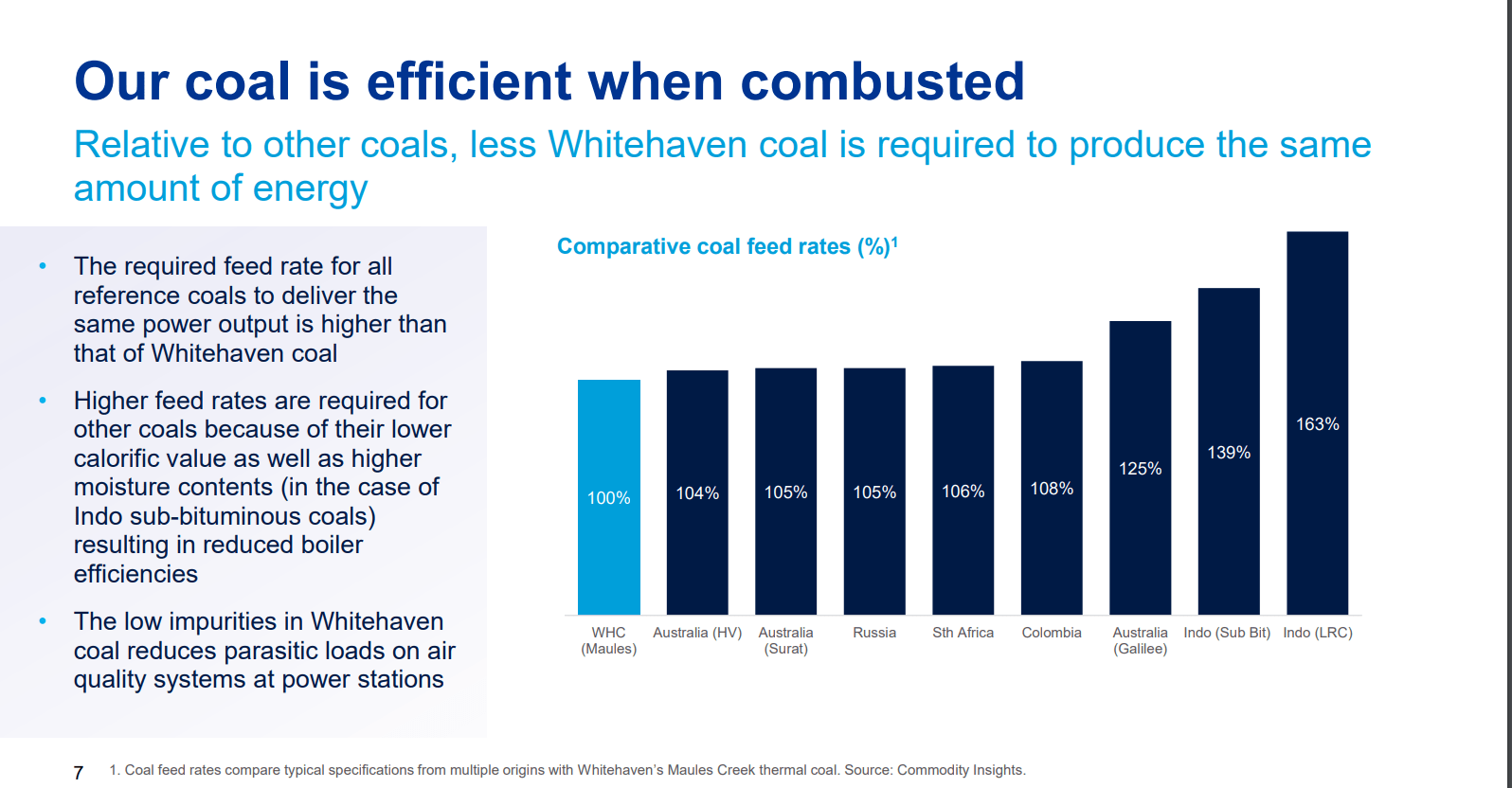

The coal caloric values are crucial for power plants and production facilities. The chart below compares various coal miners and leading coal mining countries.

{kind=link}

Whitehaven extracts the most energy-efficient coal. As the graph states, the required feed rate for all reference coals to deliver the same power output is higher than that of Whitehaven coal.

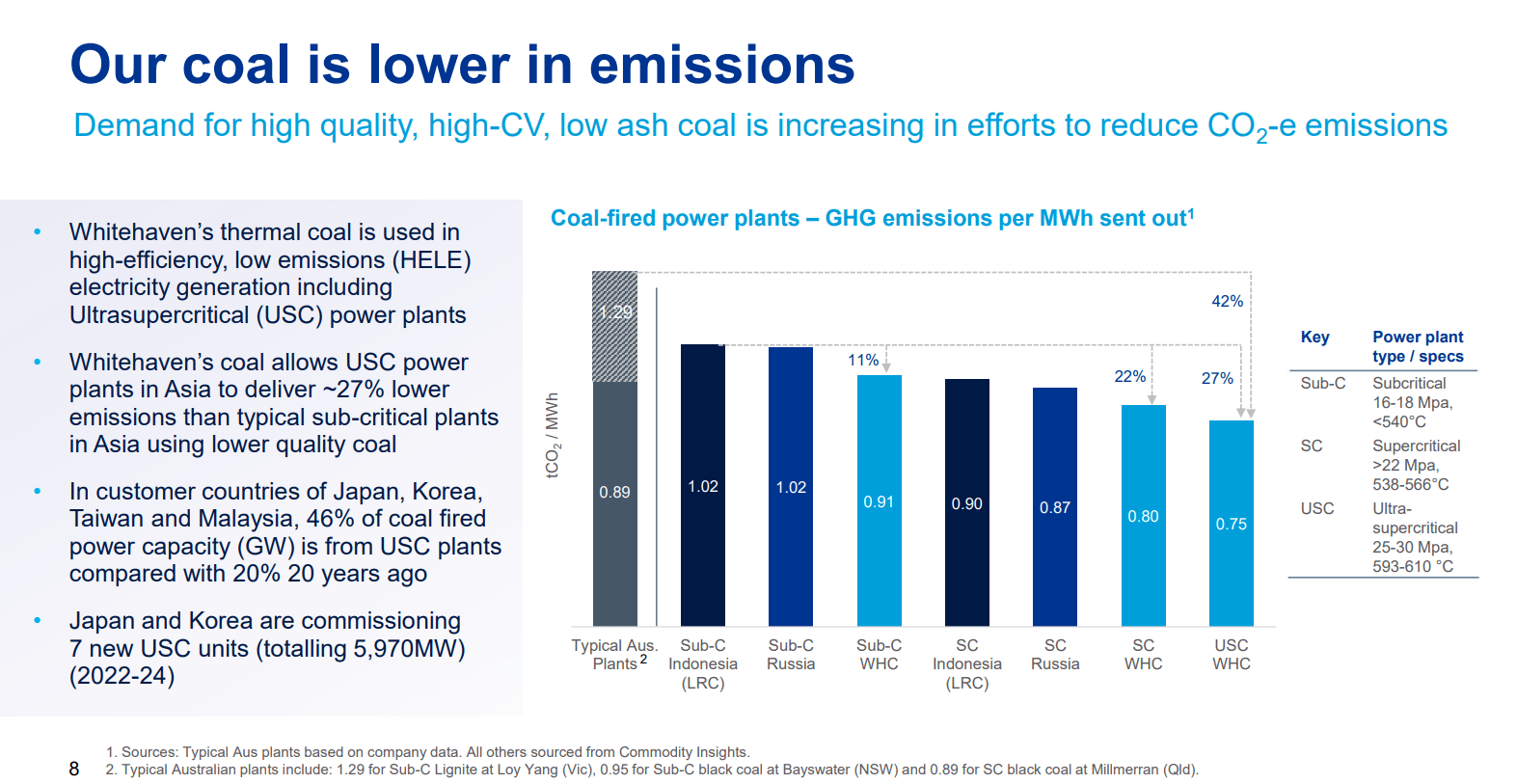

Another crucial metric is the CO2 emissions for various coal types. The chart below compares the most popular thermal coals and their tCO2/MWh.

{kind=link}

Whitehaven coal is used in high-efficiency/low-emission ((HELE)) plants. The power plants using such coal reduced their emissions by 27%.

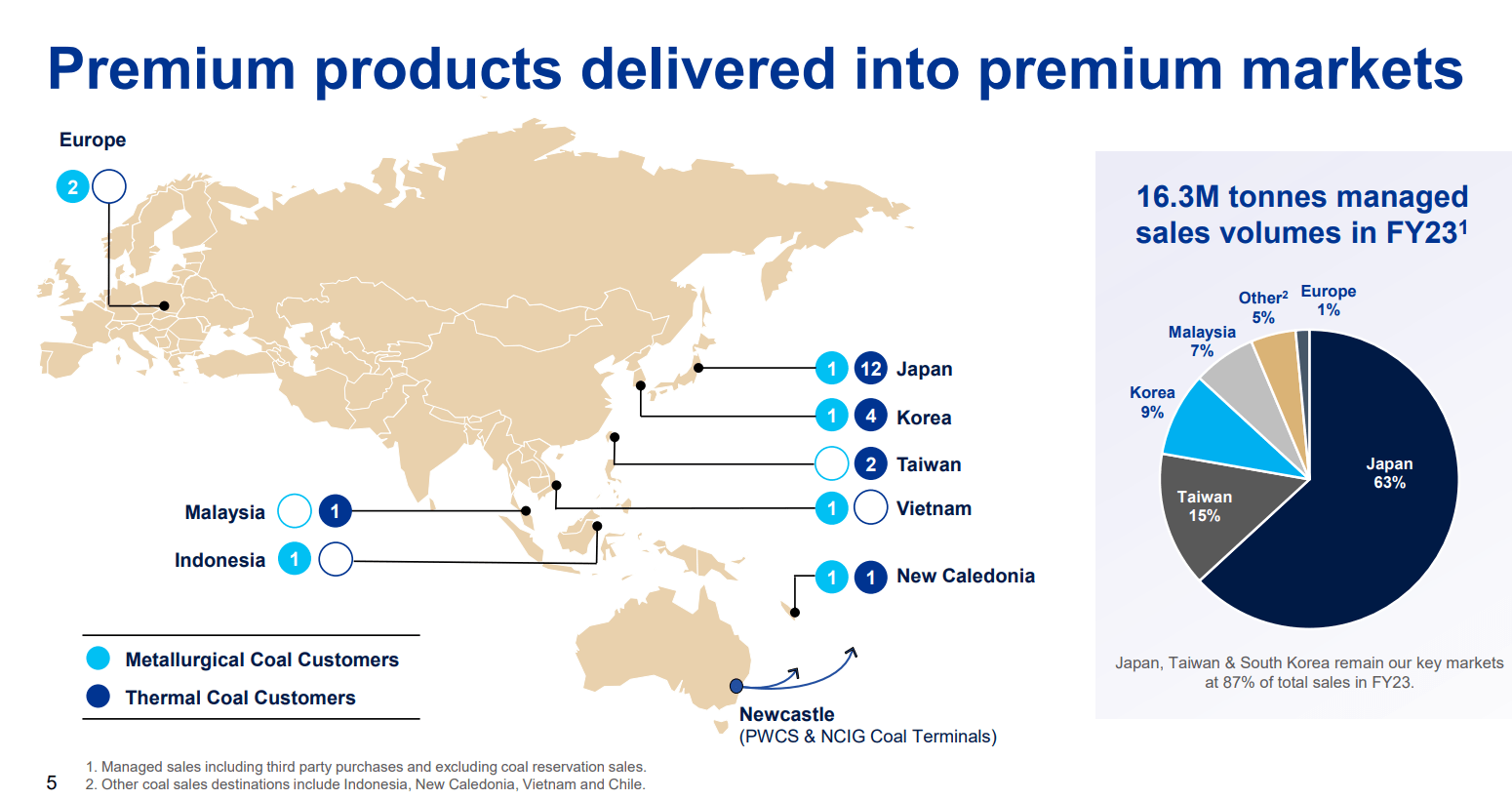

The main customers are Japan, Taiwan, and South Korea.

{kind=link}

The main markets in which Whitehaven operates are the Far East, excluding China. Over 60% of sales are made in Japan and 15% in Taiwan. The remaining is split between South Korea, Malaysia, and Singapore. The chart below shows the geographical distribution of revenue. Japan, Taiwan, and Malaysia are net importers of energy commodities and depend on regular and cheap coal imports from Australia. This makes switching suppliers an uphill task because the cost of delivery will rise due to transportation costs due to the greater distances involved. The latter also means longer delivery times.

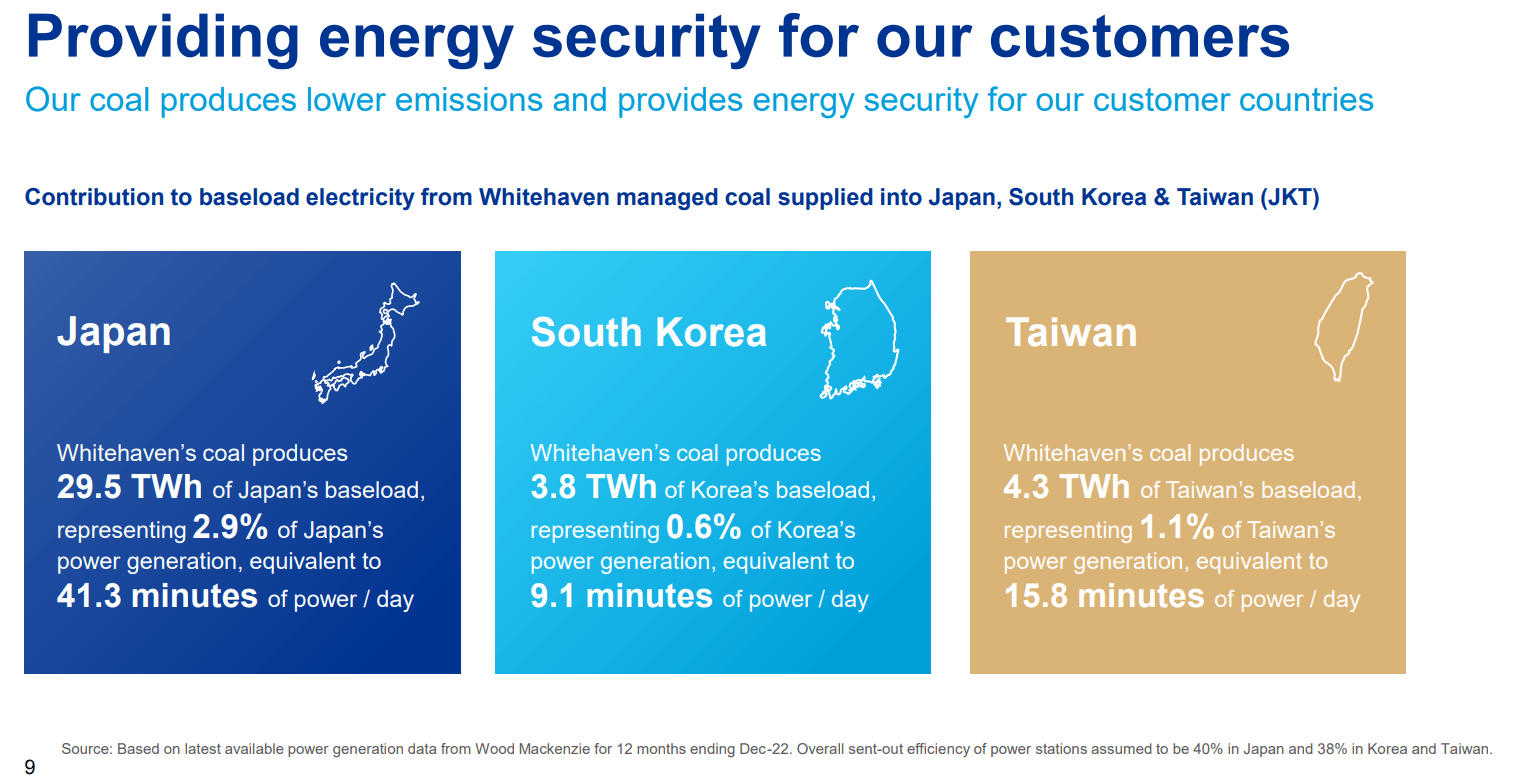

The importance of Whitehaven coal for its customers could be illustrated with the following chart:

{kind=link}

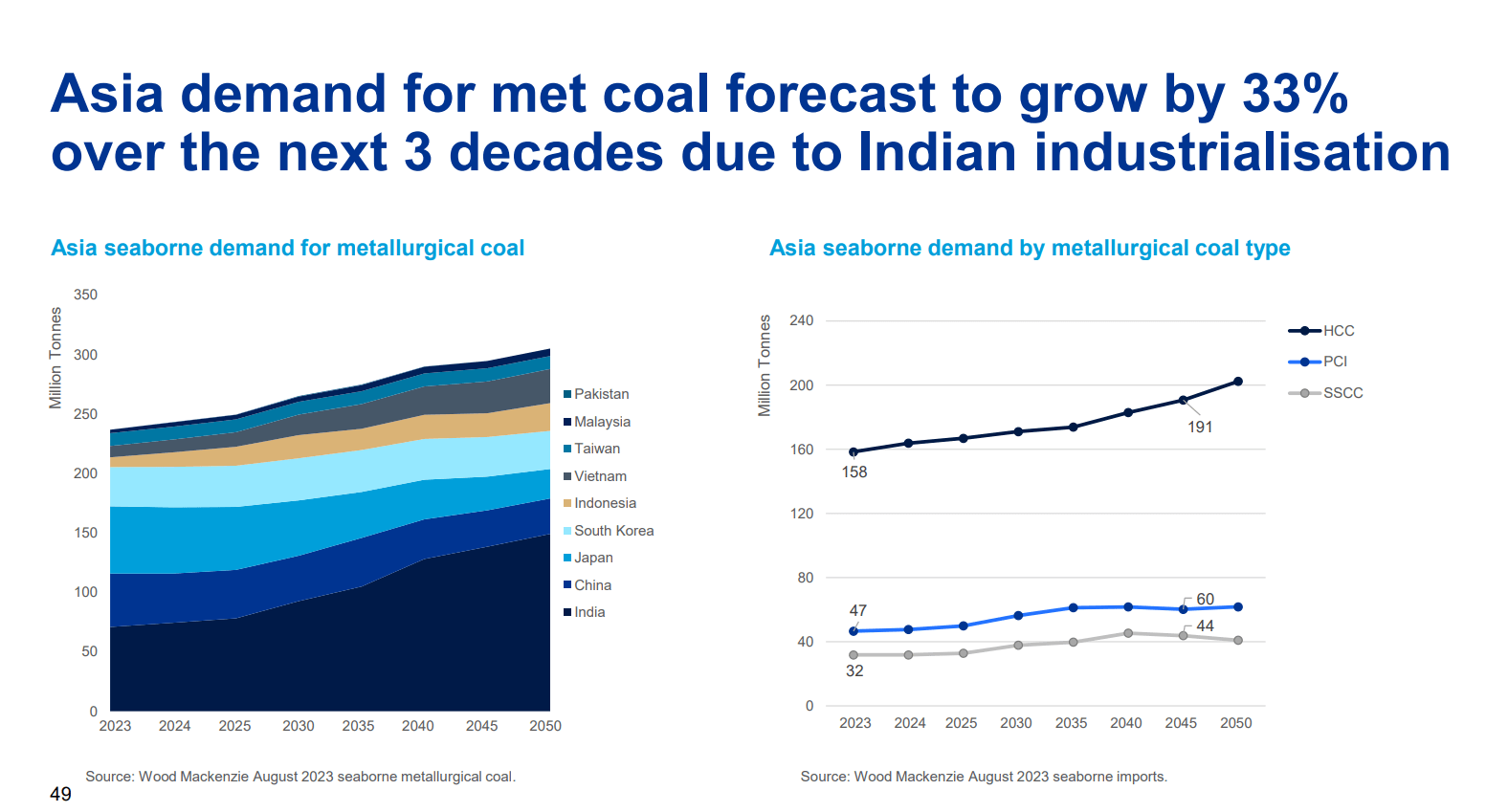

In the long term, coal demand in Asia is expected to grow significantly despite the revival of nuclear energy. The chart below shows the growth of the market by country.

{kind=link}

The primary driver is India. As a significant buyer of Whitehaven`s coal, Japan, South Korea, and Taiwan will reduce coal consumption at the end of the next decade. A notable observation is the expected growth of HCC (high cocking or metallurgical) coal used in steel production to fuel the blast furnaces. PCI or pulverized coal could be used for metallurgical purposes such as thermal coal in power generation.

In the long term, steel production will grow globally. The primary fuel will remain metallurgical coal till it is not discovered and implemented successfully inefficient and cheap enough blast furnaces running on renewables.

Acquisition of Daunia and Blackwater mines

On 18 October, Whitehaven announced its plans to acquire Daunia and Blackwater metallurgical mines from BMA. The latter is a joint venture between Mitsubishi and BHP. Both mines will expand the company`s reserve base and push its assets LOM further, as seen in the chart below.

{kind=link}

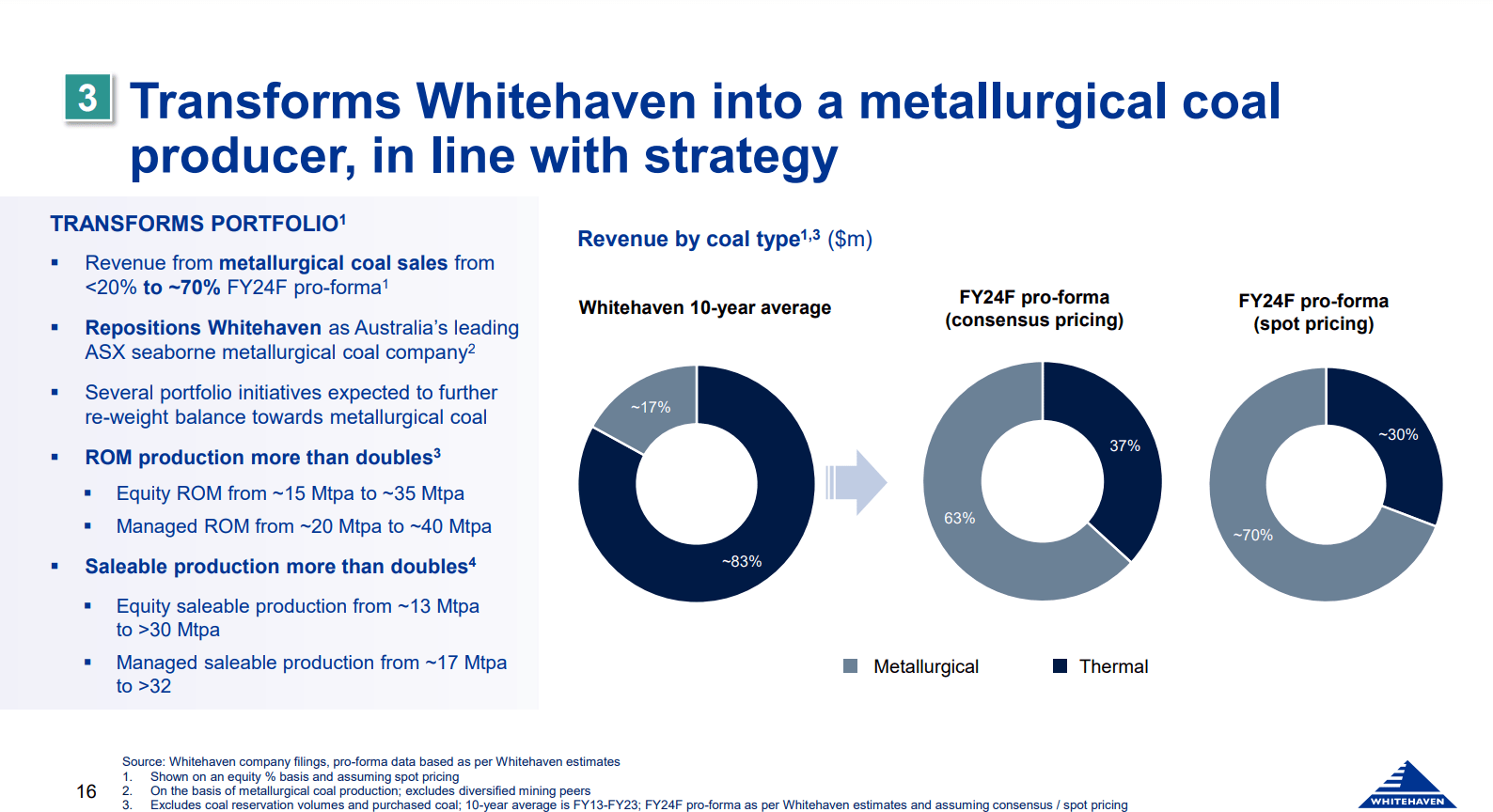

New mines are in Queensland, Bowen Basin. Their resources will increase the company's resource base by 75%. The recoverable reserves will grow by 29%. The acquisition will change the company's revenue structure. Thermal coal represents 83% of average ten-year sales. After the acquisition, metallurgical coal sales will dominate with 63%, as shown in the graph below.

{kind=link}

I think the shift from thermal to metallurgical coal is positive in the long run. Renewable energy sources will not replace coal in the foreseeable future. However, in the next 15 years, nuclear power plants will gradually substitute coal plants. I expect the demand for thermal coal to peak at the end of the decade due to the transition to nuclear energy in China and India. Nevertheless, this is not the end of coal.

Coal is not required only for power generation. It is an integral part of steel manufacturing. Regardless of our energy sources, the world needs an astounding amount of steel yearly. Iron and metallurgical coals are the two primary inputs in the steel factory. In conclusion, Whitehaven has locked its position as the primary metallurgical coal player in the Far East for the coming decades.

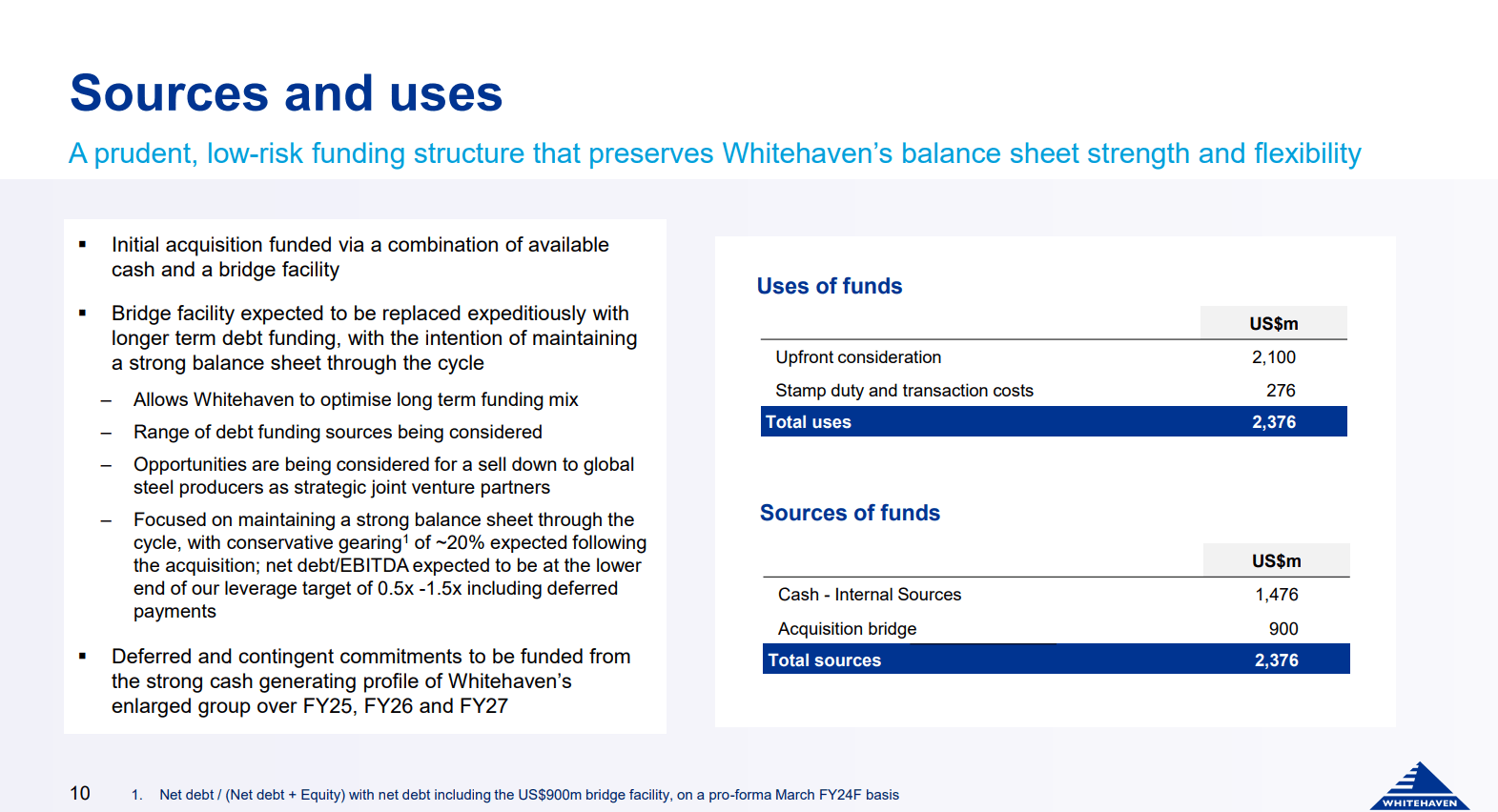

The company will use its funds and acquisition bridge to fund the acquisition. The chart below gives some details on that.

{kind=link}

The total cost of the deal is $3.2 billion. The company has $1.85 billion in cash reserves and a total debt of $125 million. The plan is to use $1.476 of own funds and borrow the rest. The transaction is expected to be completed in June 2024.

Fundamental Analysis

Coal companies are a hidden gem. They offer robust balance sheets with formidable efficiency. They have excellent liquidity and solvency and, at the same time, realize double-digit ROI and ROE.

Balance sheet

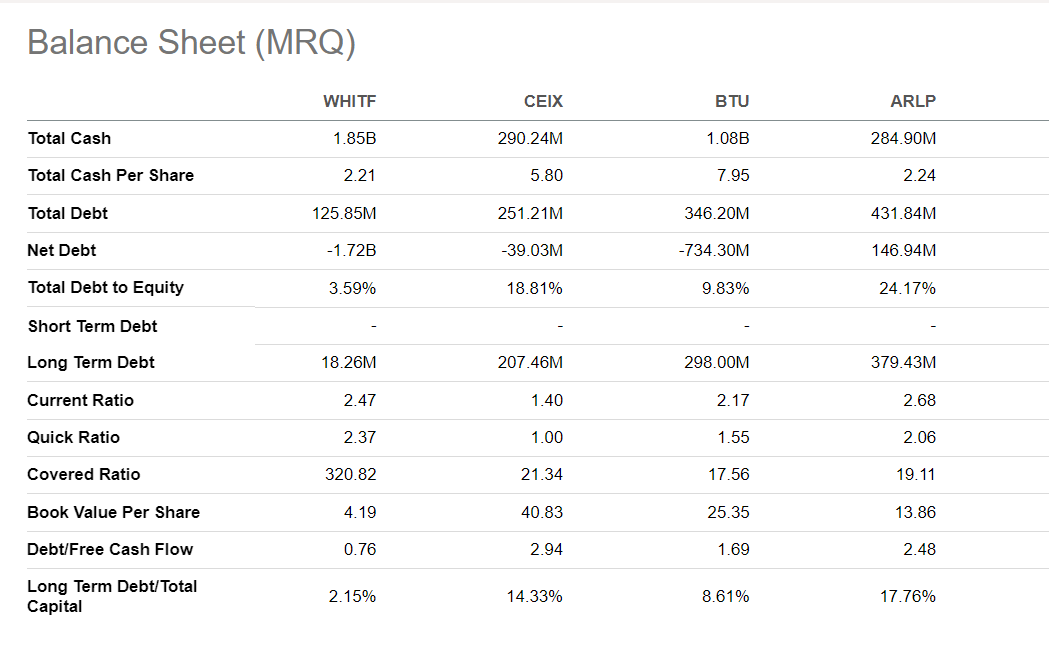

The table compares Whitehaven with its major competitors.

{kind=link}

Whitehaven excels on all metrics I consider. The company is flushed with cash ($1.85 billion) and has a mere $125 million debt. The company also has the lowest long-term debt vs free cash flow.

Whitehaven has successfully reduced its debt levels for the last three years, as shown in the table below.

{kind=link}

It is worth mentioning even in 2019, the company's leverage was at 11.5%, measured by the Total Debt/Equity (TD/E) ratio. In 2020, the pandemic has shaken the global economy, and Whitehaven has increased its debt levels to 36.7% TD/E to finance the company`s operations. Since 2022, the company has repaid a significant portion of its debts.

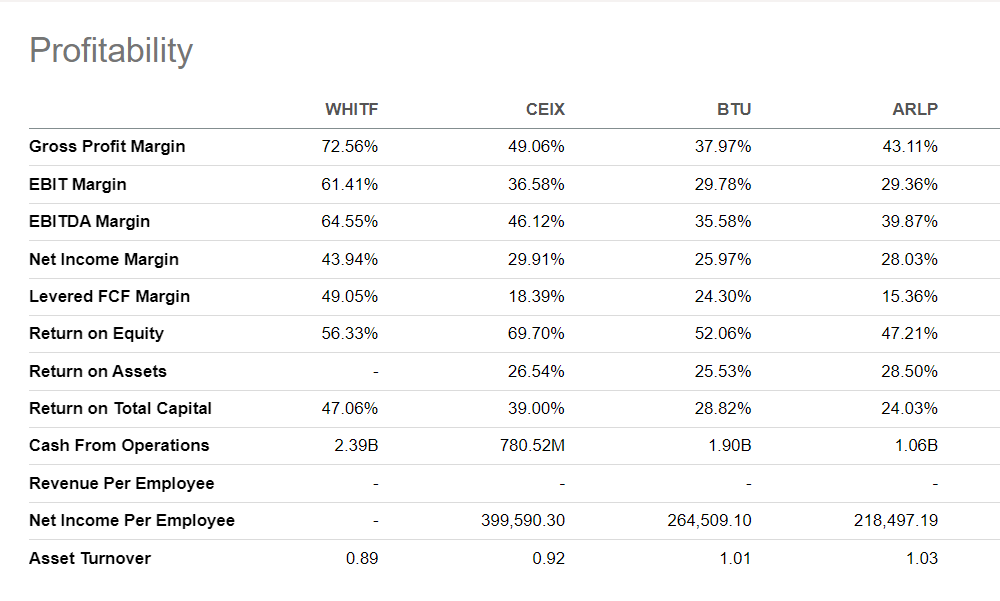

Profitability and efficiency

Coal prices are well below their last peak, yet Whitehaven is impressively profitable. Even if the coal price remains steady at its levels, the company's margins are high enough to sustain these results. The chart below compares the same enterprises based on their profitability figures.

{kind=link}

ROI, EBITDA margin, and FCF margin exceed the rest of the group with significant margins.

Even at depressed coal prices, Whitehaven is minting money at a formidable rate. In the next few years, I expect the coal prices to increase due to the reasons affecting all extractive businesses: lack of investments, shortage of engineers, and legal constraints. No commodity is excused from the adverse impact of that triad.

The most crucial profitability metric is the free cash flow generated by the enterprise. For capital-intense businesses in the long term, FCF is a function of the company`s CAPEX. FCF yield and CAPEX as % of revenue are shown on the chart below:

{kind=link}

Whitehaven is an undisputable leader in its peer group. It achieved 82% free cash flow yields at 4.2% CAPEX/Revenue. These numbers mean the company has abundant firepower to expand its operations, pay dividends/buyback shares, and acquire other companies. Proof of that statement is the announced acquisition of Blackwater and Daunia coal mines from BMA.

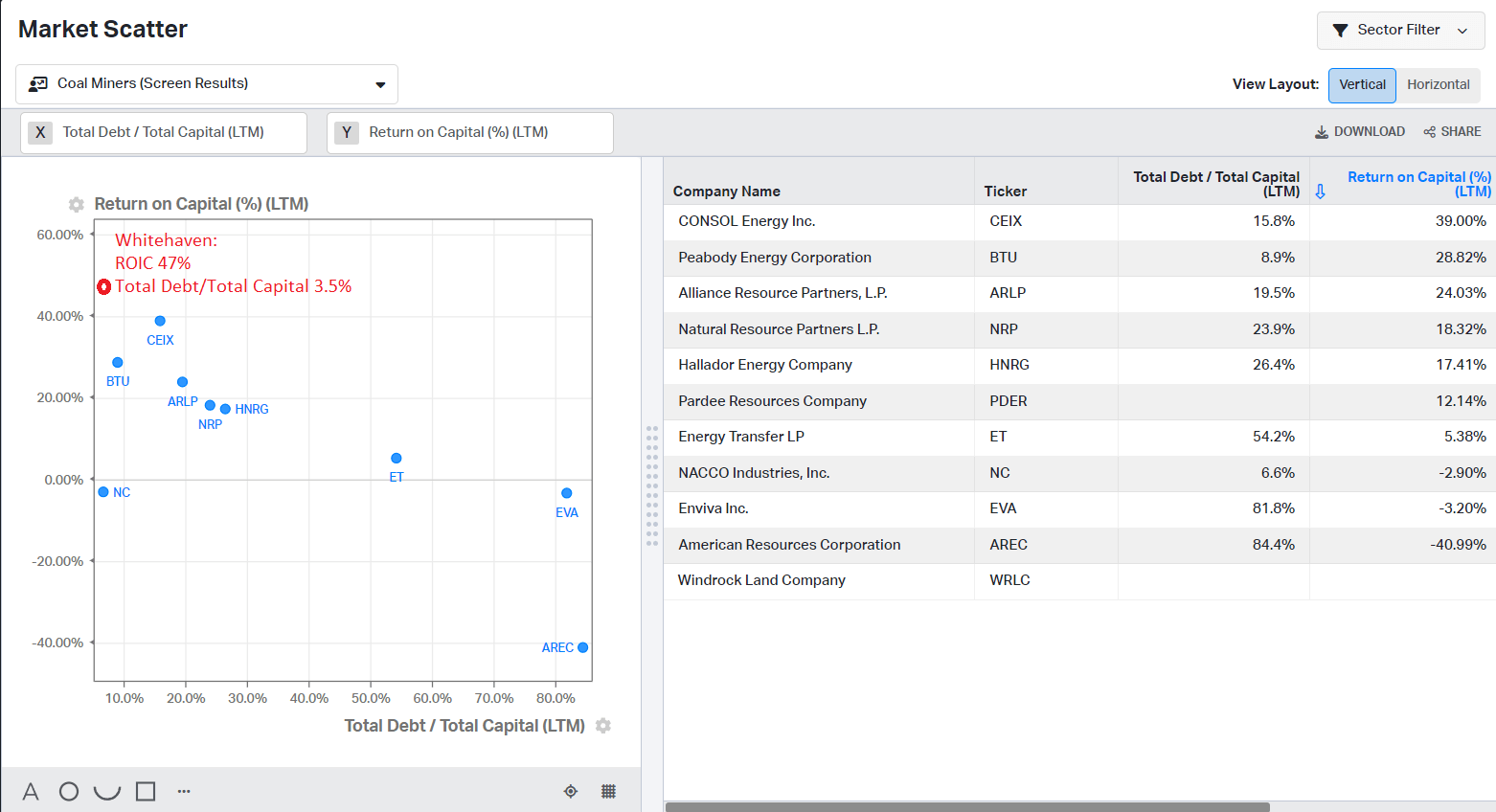

Let's see how the coal miners utilize their capital. The table below uses two metrics to assess a company's capital allocation efficiency: Return on Capital versus Total Debt/Total Capital.

{kind=link}

Whitehaven holds the pole position in the group with 47% ROIC and 3.5% Total Debt/Total Capital ratio. The second most profitable company, CONSOL, achieved a 39% Return on Capital at Total Debt/Total Capital at 15.8%.

Dividends

Ten-year bond yields briefly touched the 5% level, squeezing the equity risk premium more. Buying a bond, we have guaranteed principal and cash flows. This could not be said for equity investments. When buying stocks, we need compensation for the excess risk we take. Dividends with yields higher than bond yields solve that issue. Coal miners distribute dividends with respectable yields.

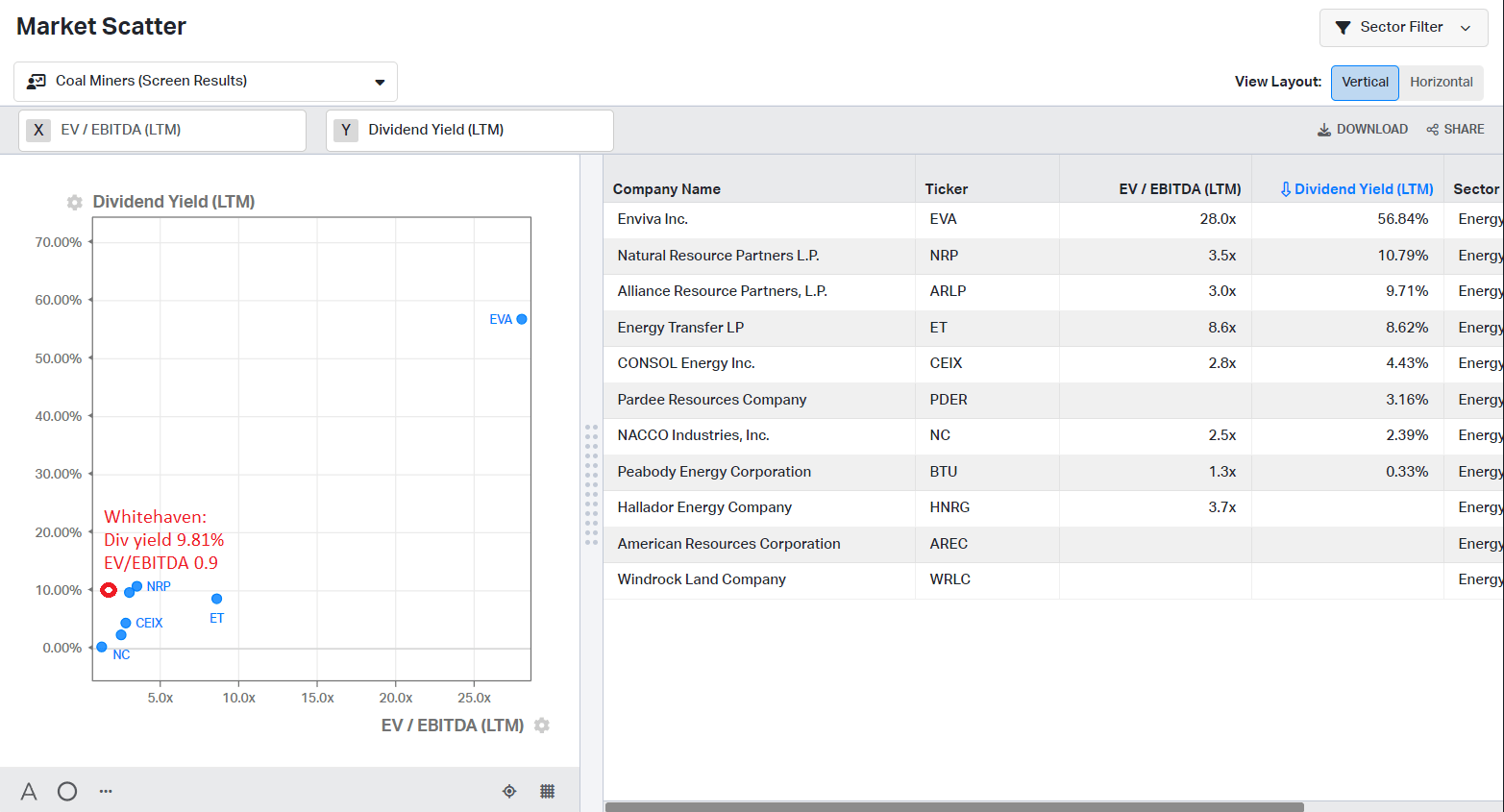

The following chart compares Whitehaven's dividends against EV/EBITDA with several other coal mining companies.

{kind=link}

Whitehaven and Alliance maintain dividends with impressive yields. The former distributes dividends twice yearly, with yields expected to be 10-12.5%. However, Alliance has a 3.0 EV/EBITDA multiple, while Whitehaven is 0.9. We pay less for similar dividend yields by buying a Whitehaven share.

Price vs. value

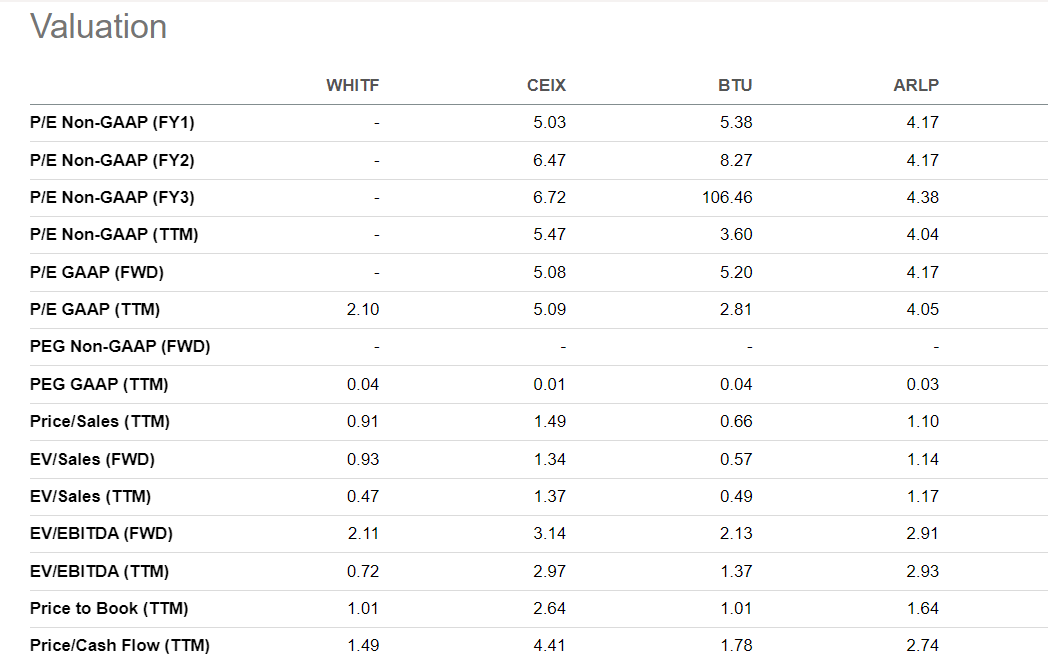

Using every metric, the coal mining industry offers excellent value at the current market prices. The chart below compares Whitehaven and a few other coal companies' multiples.

{kind=link}

Peabody has the lowest EV/Sales ratio; Whitehaven comes second with 0.97. Looking at the EV/EBITDA, Whitehaven is the leader, with the lowest value at 2.11. The situation with the P/E TTM is similar. Being aware of the imperfect EBITDA is a valuable indicator of a company's long-term performance.

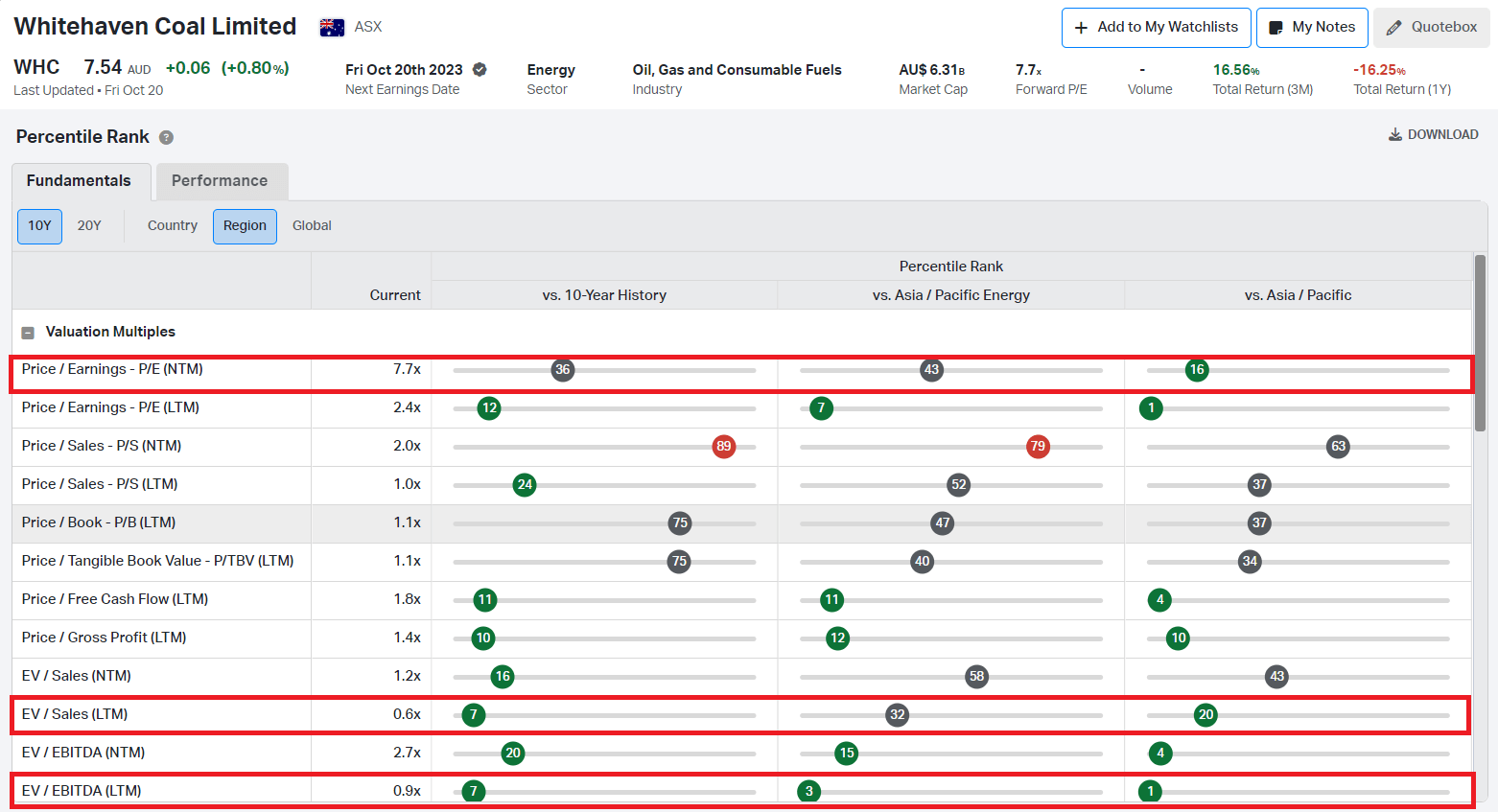

Now, let's look at the big picture. The chart below compares EV/Sales, EV/EBITDA, and P/E within three sets of data:

- Whitehaven ten years average

- Asia/Pacific Energy stocks

- Asia/Pacific broad market

{kind=link}

EV/EBITDA ratio in their data sets is in the bottom percentile, meaning the stock is extremely cheap. EV/Sales and Price/Earnings paint a similar picture.

Despite the company's qualities and generous dividends, Whitehaven has been trailing for twelve months. The company is deeply undervalued against its past metrics and regional peers.

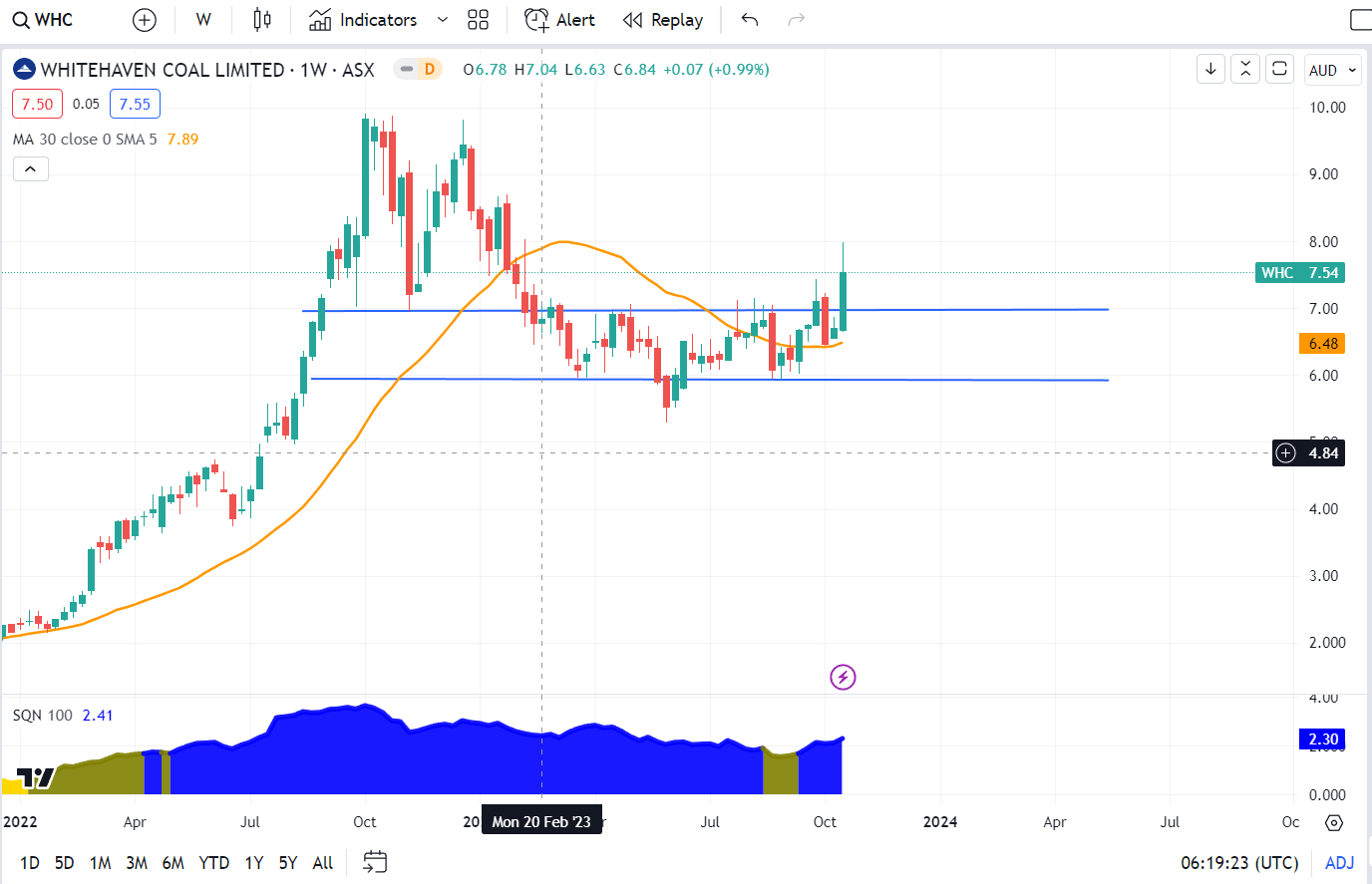

Price Action

The fundamental analysis tells why and at what price to buy. The price action tells us when the odds are in our favor. The chart below represents Whitehaven price action on a weekly base.

{kind=link}

I use the SQN indicator developed by Van Tharp. It indicates four market regimes: bull volatile (blue), bull quiet (green), neutral (yellow), bear quiet red), and bear volatile (dark red). Currently, the price is bull-volatile regime. Last week, the candle closed well above the resistance at $7.0. In my opinion, it is a confirmed breakout above the 30-week moving average. That setup is excellent for entry despite the market being in a bull-volatile regime.

Risks

Whitehaven is exposed mainly to economic and market risks. Financially, the company is stable, and I do not expect any difficulties in case of long-term declining copper prices.

The risk of another "green" driven political decision, a wave of measures against fossil fuels, will profoundly affect their prices. However, that will be a short-term issue. Politicians can stay detached from physical reality for a while; The longer they refuse to admit their mistakes, the higher the price we eventually pay. We have already observed these dynamics in nuclear energy.

The markets have been under significant pressure due to the steep bond bear market and glowing issues with the US regional banks.

The energy stocks hold their positions well. It's true for all consumable fuels. The uranium had a spectacular bull run last month, and oil and gas stocks are on the move, too. Coal stocks move sideways.

Investors Takeaway

Whitehaven is an excellent company positioned in one of the most overlooked niches of the energy sector. Acquiring BMA assets will transform Whitehaven into a metallurgical coal global leader along with Teck Resources. The company has ideal finances and maintains impressive profitability despite low coal prices. Its ROI and ROE are more suitable for biotech growth companies than not for a cost-intensive business such as coal mining. The company offers top value compared to its peers. Measured with EV/EBITDA, it is the cheapest among its peers. I expect at least 50% repricing in the short term. On top of that, we receive dividends with exceptional yields while waiting. The weekly chart shows a supportive price action with a confirmed breakout and candles above 30WMA. Whitehaven is an outstanding business in an overlooked niche sold for pennies. The company gets a strong buy rating given its strengths.

For further details see:

Bet On Dirty Energy: Whitehaven Coal