ARLUF - Bet On NeoGames A Potential iGaming Winner

Summary

- NeoGames has recently acquired Aspire Global, making it a one-stop shop for iGaming software.

- The company is expected to grow very fast in the coming years.

- Debt levels have risen as a result of the acquisition, but aren't problematic.

- I estimate the company to be undervalued by approximately 25%.

Approximately a year ago I wrote an article about the iGaming industry . Since then we have seen a lot of consolidation in the market . One of the companies that was acquired was Aspire Global, a Swedish small-cap in which I had a small position. The company was acquired by NeoGames ( NGMS ), a company incorporated in Luxembourg, that mainly focused on iLottery games. With the acquisition of Aspire Global, NeoGames became a one-stop-shop in the iGaming market. In this article, I will explain why I think NeoGames could be a good investment.

The company

NeoGames is a B2B iGaming platform provider that is active in the entire world, and incorporated in Luxembourg. It was founded in 2005 and focused on the online lottery industry, partnering with governments and commercial companies to provide them with the resources needed to run an online lottery. In 2021 it made a bid to acquire Aspire Global, a Swedish B2B company that provides its customers with everything that they need to run an online casino, including casino games and sports betting. With the acquisition, the company is now almost a complete one-stop-shop (it doesn't currently offer live casino games). The company has done this quite successfully and is expected to more than double its EPS compared to last year.

NeoGames EPS (Seeking Alpha)

Besides the aforementioned acquisition, this is driven by the overall market growth. Over the past few years, many countries/states have legalized gambling. In the US this was driven by declaring the professional and amateur sports protection act, and prohibited sports betting (PASPA) unconstitutional in 2018. This opened the doors for online gambling and effectively also meant that the unlawful internet gambling enforcement act (UIGEA), which states that it is not allowed to knowingly accept payments in connection with the participation of another person in a bet or wager that is made through the internet and that is unlawful under state or federal law, is no longer valid. In Europe, we see a similar story as both the Netherlands and Germany have recently legalized online betting.

From a fundamental perspective, the company looks poised to do well and the Seeking Alpha quant rating currently gives it a B+ for growth compared to the consumer discretionary sector. Analysts expect the company to outperform in revenue growth, EBITDA growth, and free cash flow per share growth (they all have a rating of A- or higher). Thus if analysts are right you will buy a company that will grow very fast.

Neogames quant rating (Seeking Alpha)

From a financial leverage perspective, the company is also doing well even though it recently acquired Aspire Global. To acquire Aspire the company used a combination of cash and new shares. At the end of the quarter, the company's net debt to EBITDA (calculated by extrapolating the combined H1 EBITDA of Aspire and NeoGames) was approximately 3, which was up from approximately negative 1 (calculated based on the annual report). I don't think that this is a problem, as long as the company doesn't add much more. Also, note that the majority of the debt outstanding are lease liabilities. The debt to equity of the company was at 0.6 during the last quarter, which also doesn't worry me. I prefer to own companies that have a debt to equity below 1. This gives them room to borrow more if interest rates are low and protects them from having to pay a lot of interest when interest rates go up.

Valuation

To value NeoGames, I will use two discounted cash flow calculations, one based on a growth rate in perpetuity and the other based on EV/EBITDA exit multiple. Furthermore, I will also use a comparable company analysis to assign a value to the company.

Discounted cash flows

Whenever I use a DCF model I like to make use of scenarios; these scenarios represent a bear case, a base case, and a bull case. I use scenarios because you have to make a lot of assumptions when using a DCF, and by using scenarios you can see how this would affect the share price. I use revenue growth as estimated by analysts and COGS based on the COGS over the past three years, slightly adjusted based on my expectations. For NeoGames this leads to the following assumptions:

{kind=link}

To discount future cash flows, I have calculated the weighted average cost of capital ((WACC)). The WACC is based on the company's beta, my minimum required rate of return, the treasury rate, the company's cost of equity (based on the CAPM), and cost of debt (based on interest payments and value of debt). This leads to the following WACC estimation:

{kind=link}

For the perpetuity growth method, I use a perpetuity growth of 3%. Even though the iGaming market is expected to grow a lot faster a company cannot grow more than GDP in the long run. The average GDP growth rate over the past decade has been approximately 3%. Thus, the perpetuity growth rate is set to 3%. This leads to an average price of $14.87, which is below the current price of $17.29.

For the second method, I use the average EV/EBITDA of the company, but adjust it downwards given the current environment with higher interest rates (the company hasn't been public for that long). The average EV/EBITDA of the company over the past year has been approximately 37.8. In my opinion, this is way too high, especially given the current environment with rising interest rates. I, therefore, assume an EV/EBITDA multiple of 20. This leads to a price target of $31.28.

Comparable company analysis

For the comparable company analysis, we use peer firms in the same industry. As the company is a software provider in the iGaming industry we will use companies that also focus on this. Unfortunately, it is quite hard to find companies that are 100% comparable as they either have a legacy business, only offer a limited amount of services or also focus on gambling itself. Therefore it might be that some companies aren't perfectly comparable but it should give a good indication. For this comparison, we will use the following companies: Light & Wonder ( LNW ), Aristocrat Leisure ( ARLUF ), Kambi Group ( KAMBI ) and Bragg Gaming ( BRAG ).

| Company |

| Forward revenue growth |

| EBITDA Margin |

| Net debt/EBITDA |

| NTM P/S Ratio |

| NTM EV/Revenue |

| NGMS |

| 86.45% |

| 19.11% |

| 3 |

| 2.2 |

| 2.6 |

| LNW |

| -1.21% |

| 27.28% |

| 3.8 |

| 2.1 |

| 3.4 |

| ARLUF |

| 8.04% |

| 30.11% |

| -0.1 |

| 4.4 |

| 4.3 |

| KAMBI |

| 9.18% |

| 18.17% |

| -1.18 |

| 2.7 |

| 2.6 |

| BRAG |

| 39.01% |

| -0.08% |

| -1.57 |

| 1 |

| 0.9 |

| Average |

| 28.29% |

| 18.92% |

| 0.79 |

| 2.5 |

| 2.8 |

All data has been taken from the company's Seeking Alpha pages, with the exception of the net debt to EBITDA which was taken from Tikr.com.

What we can see from the graph above, is that NeoGames has the highest revenue growth, is middle of the road in margin, and has one of the worst debt-to-EBITDA ratios. I would argue that based on the numbers presented the company should at least trade for the average of these companies. Based on the NTM Revenue that would imply a share price of $18.96 based on the P/S ratio and a price of $22.12 based on the EV/Revenue.

If we combine both price targets from the DCF and both price targets from the comparable company analysis we would get a total share price of $21.81, which is approximately 25% higher than the price at the moment of writing.

Catalysts

Even though a company could be severely undervalued, it could take months/years before it approaches fair value. Thus, it is useful to look for potential catalysts, which could push the stock price towards your estimated fair value. I currently see two catalysts for NeoGames. The first one is the overall market growth and the second one is further consolidation of the iGaming market.

Market Growth

There are multiple sector reports on the iGaming market and all of them are forecasting double-digit growth. The first reason that is given are partnerships between betting companies and big associations like the FIFA (soccer), NFL and NHL, as well as with major clubs. This will make more and more people aware of betting companies and also stimulates going to their website. As avid sports followers might have noticed, we have already seen an increase in sponsorships in sports with the NFL sponsored by FanDuel (DUEL), DraftKings (DKNG), and Caesars (CZR) and almost half of the UK's soccer clubs sponsored by a betting company.

Caesar's washington capital sponsorship (Caesar's Investor relations)

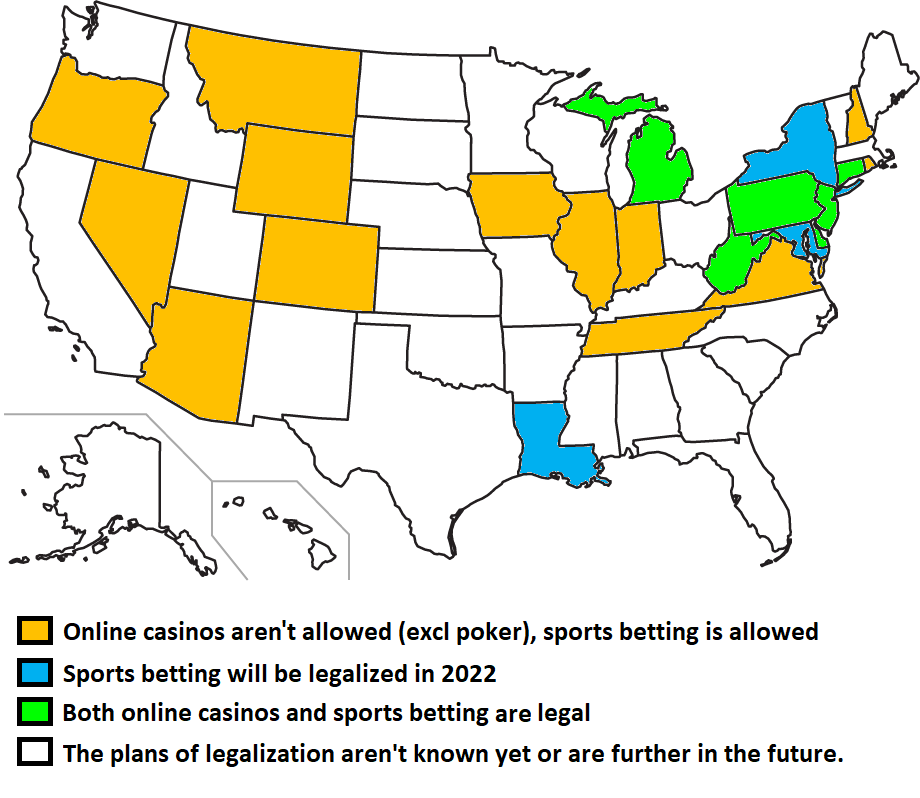

A second reason that was given is increased legalization. In the past few years we have seen multiple countries (for example the Netherlands and Germany), and, in the US, states legalize online gambling. At the moment approximately 50% of the states have legalized gambling so if the remaining states legalize online gambling this significantly increases the total addressable markets.

Overview of states that have legalized gambling (Author, data from playUSA (2021))

{kind=link}

The third and final reason that was given is the increased adoption rate of online payment gateways. The more these payment gateways are trusted and used the easier it is for customers to deposit money into their gambling accounts. Furthermore, there are a lot of countries where people don't have a bank account and if these people get access to a bank account it also makes it a lot easier to deposit money through payment gateways, further increasing iGaming TAM.

Further consolidation

The second reason that the stock might pop is that it will be acquired by another company or that one of its customers make a large acquisition (not being iGaming software). Many major players in the iGaming industry have developed their own software or acquired an iGaming software provider. A recent example includes the acquisition of SBTech by DraftKings, which gives them the opportunity to develop the company's sportsbook software to its own needs.

There are some customers of DraftKings that might want to do something similar such as MGM Resorts ( MGM ) or Caesars Entertainment, although the latter recently disposed of its stake in the company. The initial sale was initiated before the company expanded beyond the iLottery business, so it might have been a different story if the company still owned shares today. Additionally, the small market cap of the company and the fact that it offers everything from lottery games to sports betting makes it an interesting option for potential acquirers. I expect that this is quite likely down the road, although it could take a few years before it comes to fruition.

Risks

As with any investment there are some risks when it comes to NeoGames. The first and main risk is that countries could decide to make gambling illegal again. I currently do not expect this to happen but if gambling leads to mental problems, increased debt levels and/or other negative side effects, countries might take this step. This could have a significant impact on the company's operations depending on the country. The likelihood I would say is currently relatively low as more and more countries are doing the opposite and are legalizing online gambling.

The second risk that I see is that in the current environment people have a lower disposable income as costs begin to rise. This affects the company as it earns a percentage of net gaming revenue. The likelihood of this is very high as inflation keeps running riot. Nevertheless, a study conducted on gambling behaviour during the great financial crisis shows that people actually tend to spend more on luck-based gambling when unemployment rises. Therefore, I think that the impact of this would be relatively muted.

Conclusion

NeoGames is an interesting company that could have a bright future. The company recently acquired Aspire Global and now offers almost everything that you will need to run an online casino. The company's revenue growth rate looks outstanding, but the acquisition of Aspire came at a cost and net debt to EBITDA has risen significantly. I expect that the company will try to lower this in the near future, by either increasing EBITDA or lowering debt levels.

Based on a DCF and a comparable company analysis I estimate a fair value for NeoGames of $21.81, which gives an upside of approximately 25%. The company currently has two catalysts that could help it reach that price point, which are the rapid growth of the iGaming market or being acquired by an online casino owner. Nevertheless, an investment in the company is not risk free so it is important to keep an eye on the progress of legalization and delegalization of online gambling and the general economic environment.

For further details see:

Bet On NeoGames, A Potential iGaming Winner