QQQA - Better Than The SEC's NMS Plan

Summary

- The SEC has proposed amendments to RegNMS.

- There is a better alternative.

- The key to a more efficient market structure is to put the entire system into the hands of retail investors.

Introduction

The SEC made two primary proposals in recent amendments to Regulation NMS (National Market System). The article examines three alternative proposals -- the current system, the SEC's changes, and a third alternative. The SEC’s objectives are improved competition and greater fairness for retail investors. A better plan includes a simple transparent market structure that assures retail investors control revenues resulting from their transactions.

The suggested new plan incorporates aspects of the futures market structure to assure that the resulting system is simple, transparent, and inexpensive. The plan includes a new kind of exchange to improve upon futures and stock trading by trading spot and futures markets in tandem. An exchange that is mutually owned by retail investor-users.

The SEC plan

The amendments to RegNMS recently floated by the SEC boil down to these important proposals:

- An auction system designed to increase wholesaler competition for orders flowing from retail brokers.

- A requirement that retail brokers provide retail investors with a detailed description of the way these brokers fill orders.

A better plan

- An execution system that reduces the cost of transactions and improves the quality of prices.

This is an improvement over the micromanaging SEC’s specific way of changing PFOF. The SEC does not require that their change improves the lot of retail investors. It should.

- A report that provides retail investors with an accounting for revenues and costs associated with each customer investment.

Retail investors don’t care about the way brokers fill their orders. The SEC assumes this information is important to investors. The SEC might want to know what the brokers are doing. Investors do not. They want instead to be able to compare investment results achieved by each broker they use. How much of the value created by the transaction goes to the investor? How much goes to Wall Street?

The SEC’s proposals are meant to spread oil on the waters of controversy surrounding the meme fiasco of January 2021. Like most regulation changes, these proposals are reactive, not proactive. The problem with any regulatory rule change is that it limits the options of existing market participants instead of expanding investor opportunities.

- A single exchange with added capabilities owned by its customers as is Vanguard.

A better objective than the SEC’s goal of fairness to retail investors is to give them control of market execution.

SEC objectives

According to chair Gary Gensler, the SEC’s objectives are to “strengthen competition and ensure individual investors are fairly treated.”

- Competition. Competition is a factor

- in determining a retail investor’s choice of broker.

- in the retail broker’s choice of execution service (wholesaler or exchange).

- and in the wholesaler's choice of counterparties in laying off the risk resulting from filling retail orders.

A new, far simpler, system that would ensure competition in each of these markets would look only at each retail investor’s final investment results. This system would make it easy to compare one broker to another.

- Fair treatment. Fair treatment is a dubious proposition. Nothing in the movement of Adam Smith’s invisible hand has anything to do with fair treatment.

Smith puts it thus , “It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own interest. We address ourselves, not to their humanity but to their self-love, and never talk to them of our necessities but of their advantages.”

A less value-laden approach that would be more on point would be to require retail brokers to provide retail investors with full information – all the costs and revenues associated with each investment. This enables investors to foster competition at all three of the levels above with a single decision – the choice of broker.

Why regulation is a poor source of innovation in financial market structure

The SEC’s proposed auction mechanism is a good example of the shortcomings of any regulatory rule change. An auction market for wholesaler services is a complication to the already-too-complex stock market structure. Our market structure is already burdened with too many exchanges and other execution platforms. It is the essence of regulation to add requirements to the existing system, inevitably increasing cost and complexity.

There must be cheaper, faster, ways for retail investors to capture revenues paid to retail brokers by wholesalers.

There must be a way to replace the current maze of retail orders with a simpler, cheaper, more transparent, path to the ultimate seller. What are the desirable properties of this new path?

How to better meet retail investors’ investment objectives

In the hope of identifying specific innovations, this article considers the market’s needs as defined by the SEC and others who seek solutions. Any execution system ought to be judged based on three criteria.

- Transparency.

- Simplicity.

- Retail investor control of the financial market structure.

The systems compared

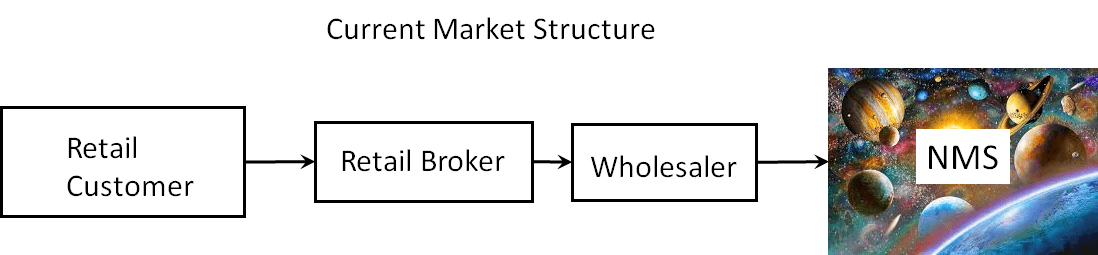

The current system. The graphic below describes a retail investor’s order flow for the current market structure. In the current structure, a customer chooses a retail broker which has an agreement to pass customer orders to a wholesaler who executes the order and then lays off the risk at a profit by filling the same order in the National Market System ((NMS)).

{kind=link}

Existing Market Structure (Author)

The table below indicates payments and receipts in the current system. In the graphic below, green boxes represent receipts, and red boxes, payments.

- The broker collects interest and dividend payments from the issuer of the security and passes them to the customer’s account.

- While the purchased security is in the customer’s account, it may be lent to other NMS participants who pay fees and interest to the broker while the security is in the broker’s customer account and to the broker’s wholesaler while the security is in the retail broker’s account with the wholesaler.

- The broker’s chosen wholesaler pays the broker for the right to place the order at a price below the best price in the market, PFOF.

- The customer pays fees to the broker, including clearing fees and exchange fees.

Current Market Payments (Author)

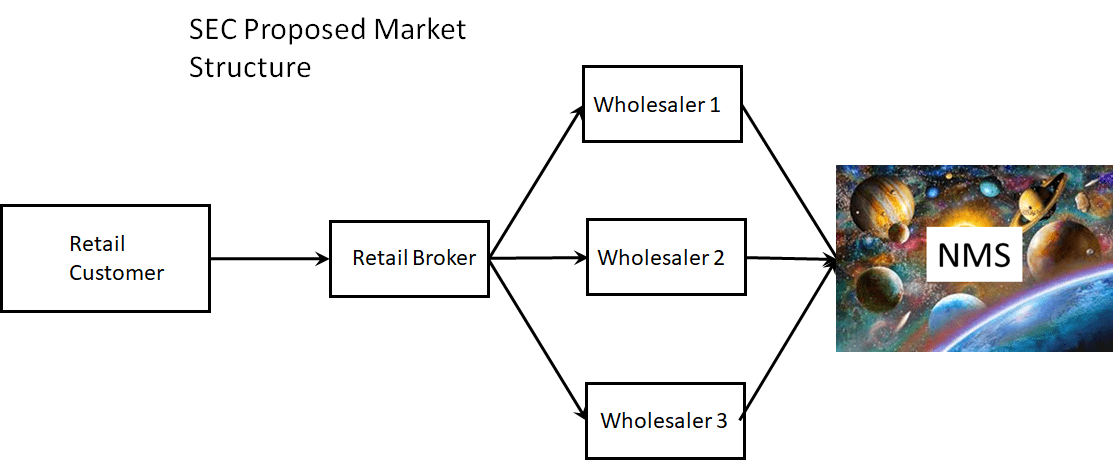

The SEC proposal. The graphic below describes a version of the SEC’s proposed market system, where the SEC’s proposed auction involves three brokers. The auction adds complexity to the current market system, even though each wholesaler lays off the retail transaction in the same NMS.

{kind=link}

SEC Proposed Structure (Author)

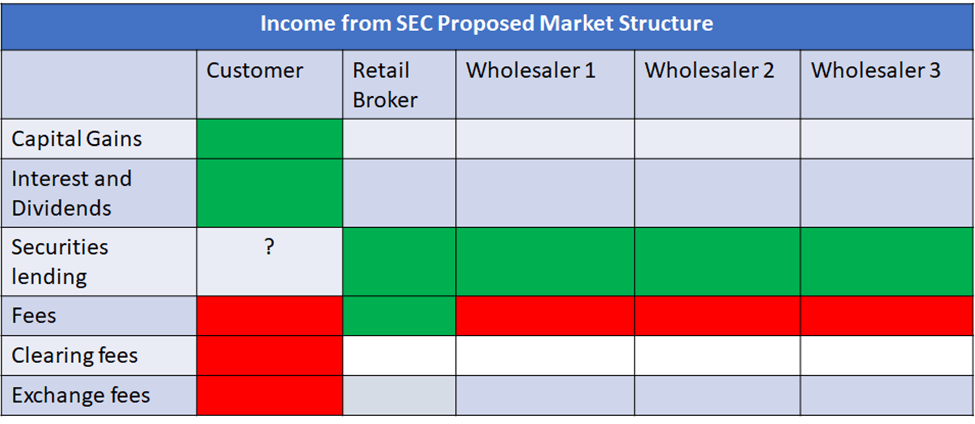

The table below shows the flow of income in the SEC’s proposal. The benefit of the proposal is that there is competition between wholesalers for retail orders. This competition comes at the cost of added complexity. While the SEC proposal may reduce wholesaler profits, as with any added layer of transactions, the auction adds to the total resource costs of the entire transaction. In other words, the proposal may reduce Wall Street profits, but resources devoted to execution will certainly increase. The payments table is the same as the current market structure except for the addition of retail-broker-chosen wholesalers.

{kind=link}

SEC Market Payments (Author)

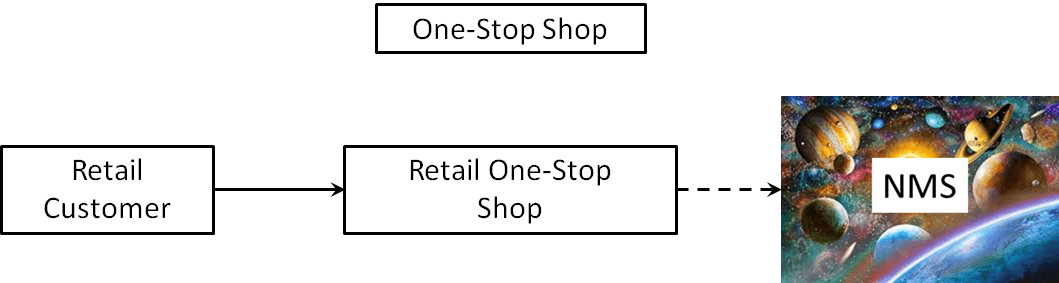

A better alternative: a One-Stop-Shop. The graphic below shows how the One-Stop Shop simplifies the NMS. Note the dotted line from the One-Stop Shop to the NMS. That order path is a second transaction entered by the One-Stop Shop to manage the risk associated with the customer fill. The customer order is always filled inside the One-Stop Shop. In other words, the entire process is a single transaction.

{kind=link}

One-Stop Shop Structure (Author)

Risks from the retail investor’s transaction are borne by the exchange. The dotted line indicates the exchange transaction that lays off the exchange exposure created by the execution of the retail investor’s order.

The table below shows the flow of income in the One-Stop Shop proposal.

One-Stop Shop Payments (Author)

The One-Stop Shop relies on competition from counterparties in the NMS to assure the quality of retail price. This competition drives complexity outside the One-Stop Shop and into the NMS. The One-Stop Shop creates a retail market structure far simpler than the alternatives.

The differences between a futures exchange like CME and the One-Stop Shop.

- The One-Stop Shop is mutually owned by its customers. Thus, income related to exchange operations is always returned to retail investors, either by direct payment on a per-transaction basis or by dividends. This would put an end to PFOF.

- The One-Stop Shop originates its version of each security. This practice creates the capability of trading both spot and futures versions of each listed security in tandem.

Similarities to futures

- The One-Stop Shop eliminates inter-exchange arbitrage since all orders must be processed by the exchange clearinghouse – the counterparty for every customer transaction.

- The payments table is the same as the structure of the futures except for the addition of interest, dividends, and securities lending fees.

- The One-Stop Shop will be a natural monopoly much like CME Group is today.

Conclusion

A government agency like the SEC cannot bring proactive change to the NMS. Regulators are designed to react to failures of the system, to limit existing system failures.

Yet the natural function of market structure is to merge orders, passing them all through a single node. The key change that defangs the monopolistic beast is the exchange government by investors. Investors are indifferent to the way they earn rewards from their investments – profit from exchange ownership or gains from their portfolios.

For further details see:

Better Than The SEC's NMS Plan