TFC - Beware Big Tech And Buy These 7% Yielding Blue-Chip Bargains

2023-10-18 07:05:00 ET

Summary

- Big tech has driven the Nasdaq up 40% and S&P 20% this year. Big tech is now 30% of the market.

- The Nasdaq is pricing in 20% earnings growth this year and 63% EPS growth through 2025, ignoring a recession that the bond market says is a 96% probability.

- Historically, big tech's earnings fall about 20% during recessions, meaning there is a 40% difference between what is likely and what the market expects to happen.

- Big tech could be as much as 45% overvalued, adjusting for the likely recession in 2024. In a stagflation recession soaring rates could send the Nasdaq down 30% to 50%.

- Financials are the opposite of big tech. They are priced for recession already and trading at a bargain valuation of less than 12X earnings. And these two blue-chip bargains offer a safe 7% yield and coiled spring opportunities to lock in incredible Buffett-like return potential from blue-chip bargains hiding in plain sight.

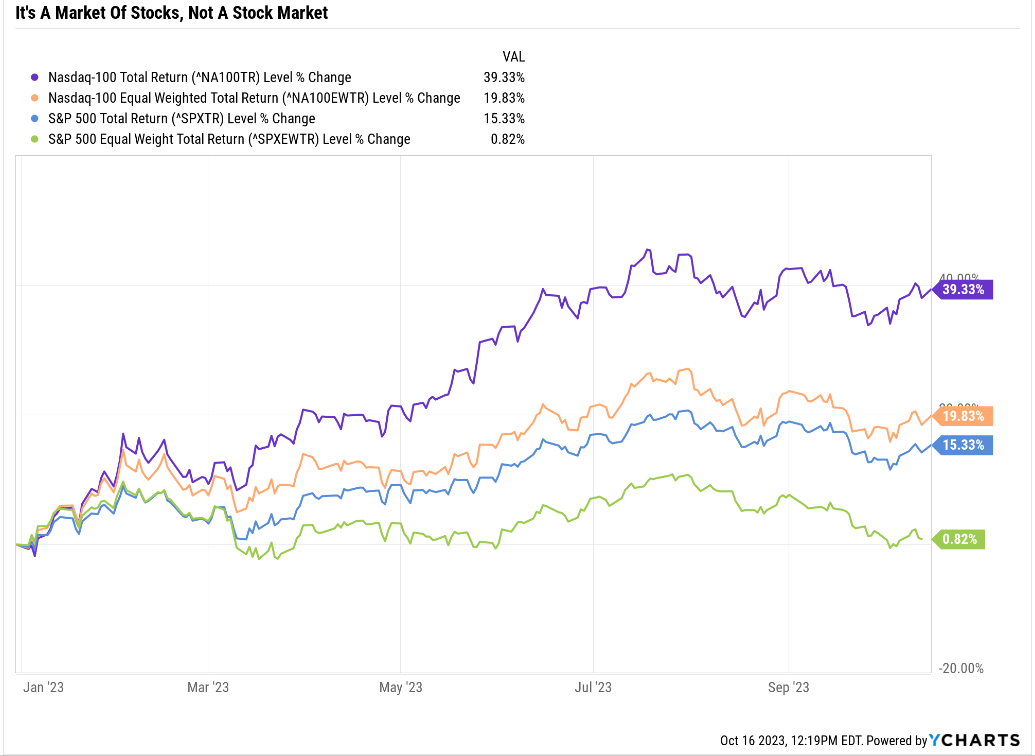

It's been a great year for investors, right? Actually, no it's been a great year for the magnificent 7 big tech names, and for the rest of the S&P 493, it's been a flat year.

{kind=link}

Now a lot of investors might be looking at that chart and thinking, "Looks like the Nasdaq ( QQQ )( QQQM ) is in consolidation and we could be set to soar again".

But I have one important warning.

"Be Greedy When Others Are Fearful And Fearful When Others Are Greedy" - Warren Buffett

There is no denying the magnificent 7 are some amazing world-beaters.

{kind=link}

Apple (AAPL), Microsoft (MSFT), Alphabet (GOOG)(GOOGL), Amazon (AMZN), NVIDIA (NVDA), Meta (META), and Tesla (TSLA) dominate our lives and our wallets.

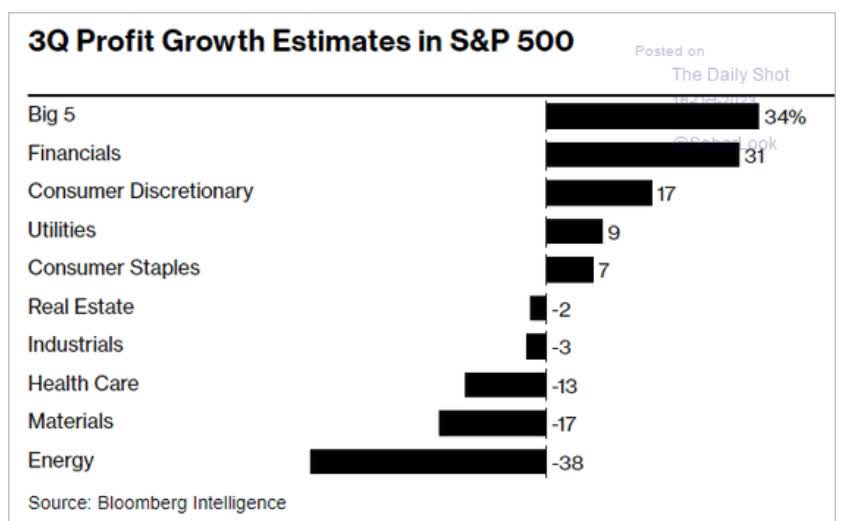

Today they make up 30% of the S&P 500 and are expected to be driving most of the earnings growth in Q3.

{kind=link}

The big five tech giants are expected to deliver 34% earnings of the profit growth for the S&P this quarter. That's amazing, right? 30% of the market cap and 34% of the growth! That's justified, the fundamentals make sense! Everyone into the big tech pool!

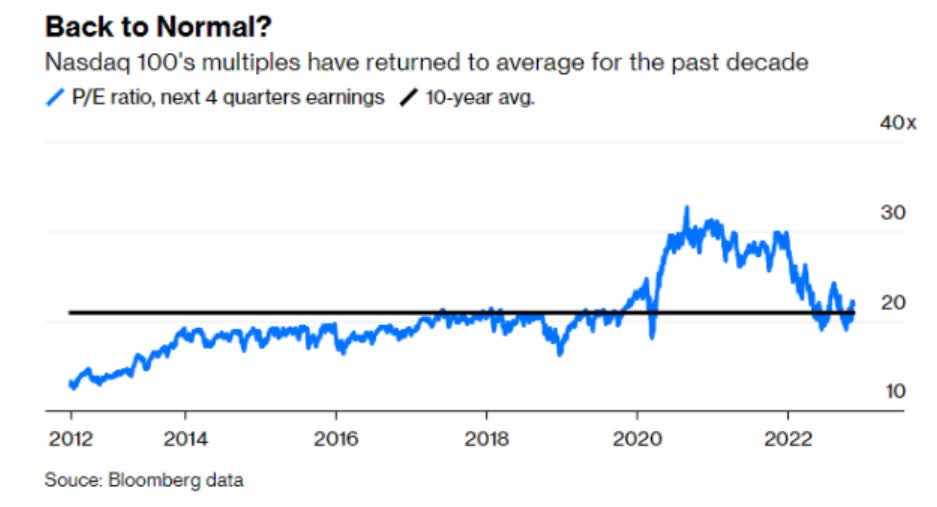

For 20 years the Nasdaq's historical market-determined fair value was 20.

{kind=link}

During the zero rates world? Still 20.

{kind=link}

So what this tells us is that with 91% statistical certainty we can estimate that 20X forward earnings is an objective market-determined fair value for the Nasdaq.

- its 25X for big tech itself

As Ben Graham explained, long term everything good, bad, and ugly about any company is baked into the price, as the market correctly "weighs the substance of a company".

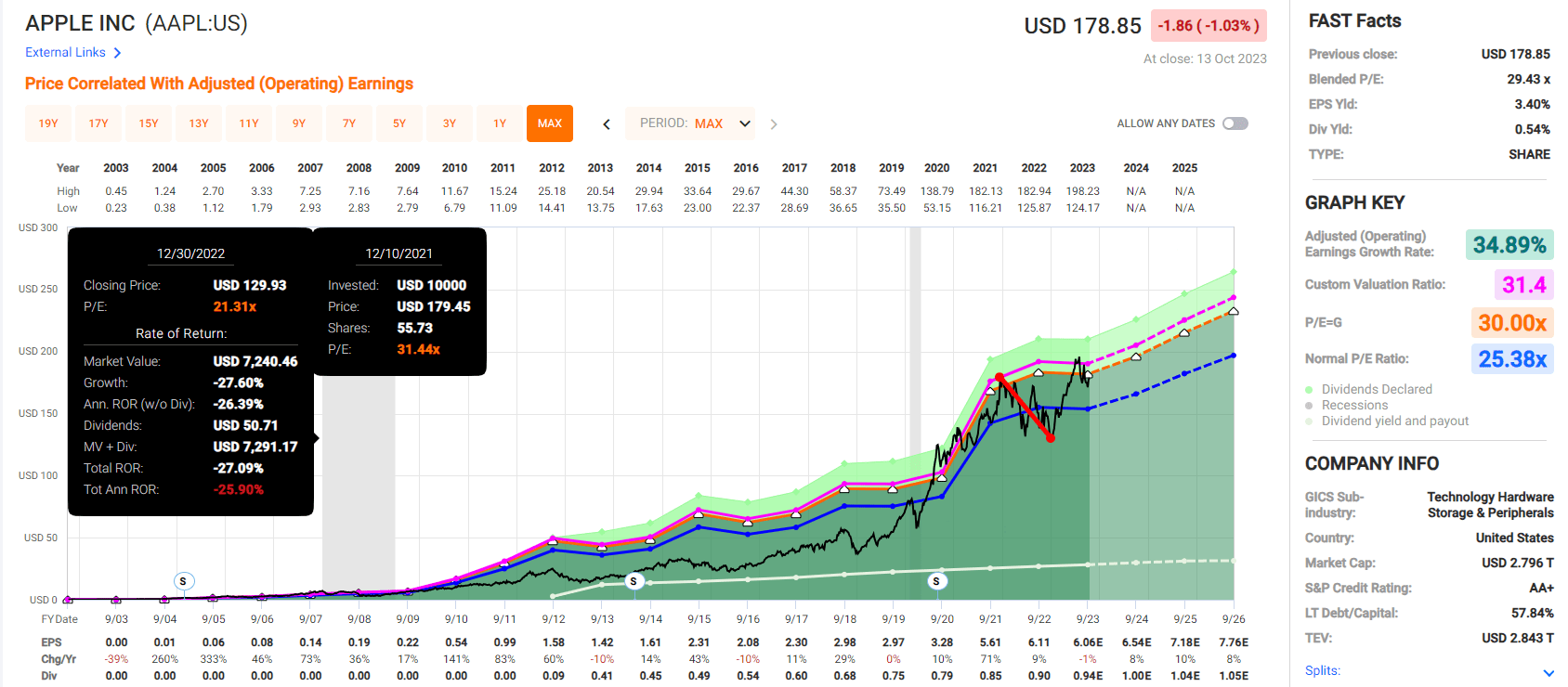

In the short term, prices can become unglued from fundamentals. That's how bubbles can form, with big tech darlings like Apple hitting a PE of almost 40 before the 2022 bear market.

Apple Was Obviously In A Bubble At 31X Earnings...But 32X In July? This Time Is Different!;)

{kind=link}

Anyone claiming Apple is a fair value or even a buyback in July was high on hopium.

- the victory of hope over experience

That includes Wedbush's Danny Ives, Wall Street's official Apple permabull.

- $240 12-month price target (educated wild guess) = 36X forward earnings = 44% historical premium

Such bulls always have a plausible-sounding story for why Apple is suddenly going to grade at 32, 34, or 36X earnings despite the fact that it's now a 9% growing company.

- growth consensus range for Apple is 3% to 15%

- median consensus 8.7%

Apple has become a luxury tech utility but I would call it the height of speculation to claim that a company that was fairly valued at 25X earnings growing at 35% is now suddenly worth 36X earnings growing at 9%.

- no matter how stable its cash flows might be

- and we don't actually know if Apple's sales will hold up in a regular recession yet

Don't get me wrong, I love Apple, but I'm telling you that anyone telling you Apple was a screaming buy at 32X earnings in July was a fool, a liar, or trying to sell you something, (possibly all 3).

As a business, Apple is my favorite company, but be realistic about what it can do in the future.

And the same is true of the magnificent 7 in general.

And this is where valuation becomes important.

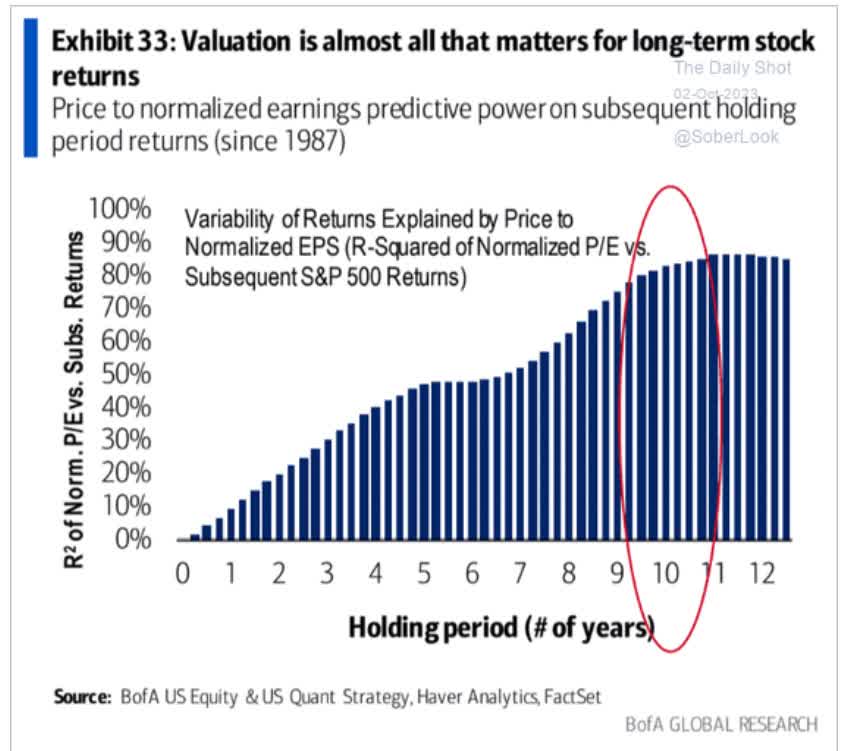

Valuation Never Matters In The short term But Always Matters In the long term

{kind=link}

Over 1 year? Valuation means very little to stock returns. Over 6 months or less? It means almost nothing.

Over 10 years? 80% of returns, and over 30 years? 97%.

In the short-term luck is 20X as powerful as fundamentals and valuation.

- why 12-month price targets are "educated wild guesses" by analysts,

- ignore these

In the long term, fundamentals and valuation are 33% as powerful as luck.

- Buffett, Graham, Dodd, Templeton, Lynch, Greenblatt, Marks, never tried to time the market

- pure fundamental value investors

We've just seen how over the last 10 years and 20 years, as long as QQQ has existed, the market's objective historical fair value, determined by billions of cumulative investors, was 20X earnings.

What about today? 23X, which is a 15% historical premium.

- S&P is a 5% historical premium

- Nasdaq was 30% overvalued back in July before the sell-off

Okay, so that means it's not really that bad to buy the Nasdaq, right? I mean, at worst, it trades flat for a year, right? No giant 2000-style 82% tech crash that leaves investors waiting 17 years to break even, right?

Nasdaq Fundamentals

FactSet Research Terminal

The consensus is for 19% EPS growth in the Nasdaq in 2023, another 18% in 2024, and then almost 17% in 2025.

That's 63% EPS growth in 3 years or 18% annually.

- 2009 to 2022 EPS growth of 14% annually

- 37-year EPS growth: 12.9%

- Morningstar analyst consensus: 12.1%

Do you know the Nasdaq is suddenly going to accelerate its growth rate by 50% and hold that for 3 years? Or maybe analysts are a tad too optimistic?

So what if the Nasdaq's earnings only grow 12% annually through 2025? Then the forward PE is now almost 25.

And what if we get a recession?

{kind=link}

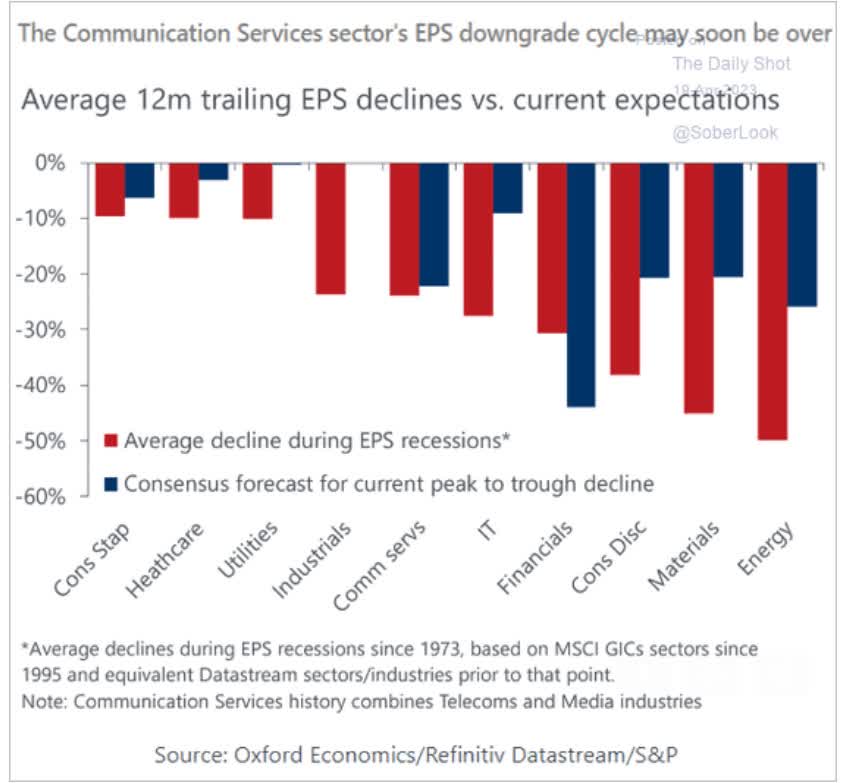

Since 1973 tech earnings averaged a nearly 30% decline during recessions.

Communications? Like GOOG and META? 20% decline.

Consumer Discretionary like AMZN and TSLA? 40% decline.

What does the bond market say is the odds of a recession next year? 96%.

The most liquid market in the world, the "smart money" on Wall Street, thinks there is a 96% chance that big tech earnings are historically going to fall off a cliff next year.

Meanwhile, the consensus is that earnings will soar almost 20%.

Do you see a potential problem here?

- a 40% disconnect between what historically happens and what the market is pricing in right now

So if there is a recession in 2024, which the data says is most likely, then the Nasdaq might not be trading at 23X but at 29X.

- A 45% historical premium

I don't care if you're looking at God's own company, a 45% historical premium is just asking for trouble.

Don't Forget About The Fed's War On Inflation

{kind=link}

In the short term stocks can trade like bonds and if interest rates spike and earnings disappoint (in a recession they will miss by a mile) then big tech can go off a cliff like in 2022.

Why might interest rates stay high or even go higher?

{kind=link}

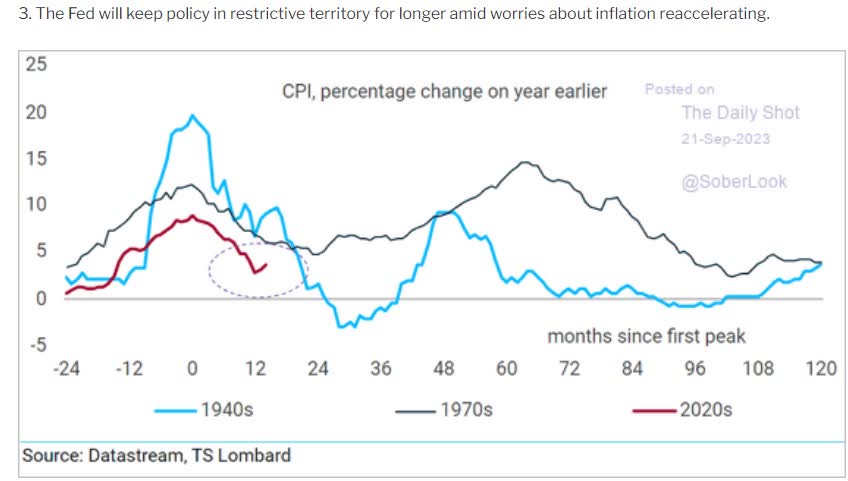

Because every other time we had mega-spikes in inflation it wasn't just one spike it was 3.

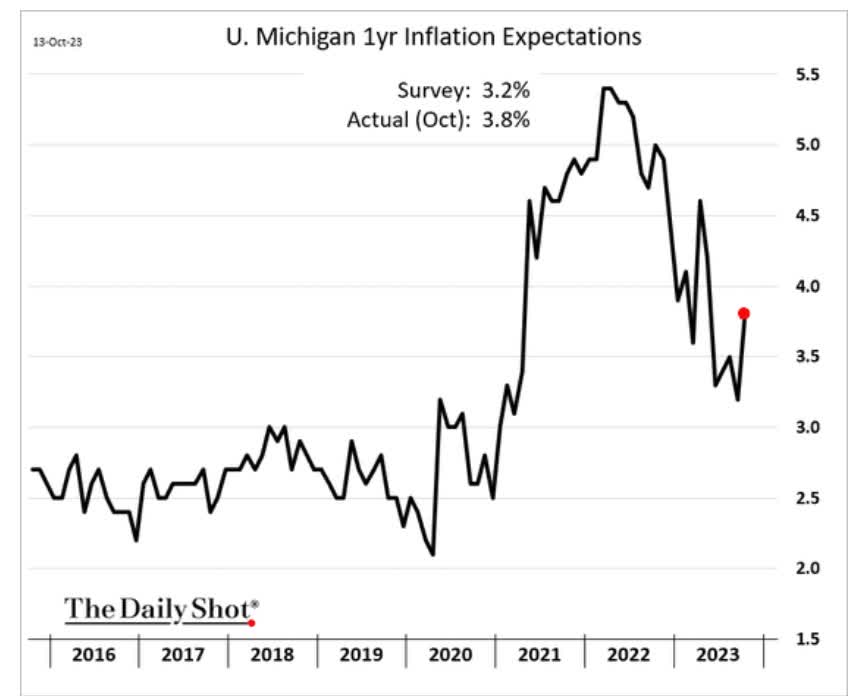

Assuming we're not set up for another 1970s wage-price spiral we could expect inflation to rise back to around 5% or so by January according to Goldman.

What Do You Think 5% CPI Would Do To Inflation Expectations

{kind=link}

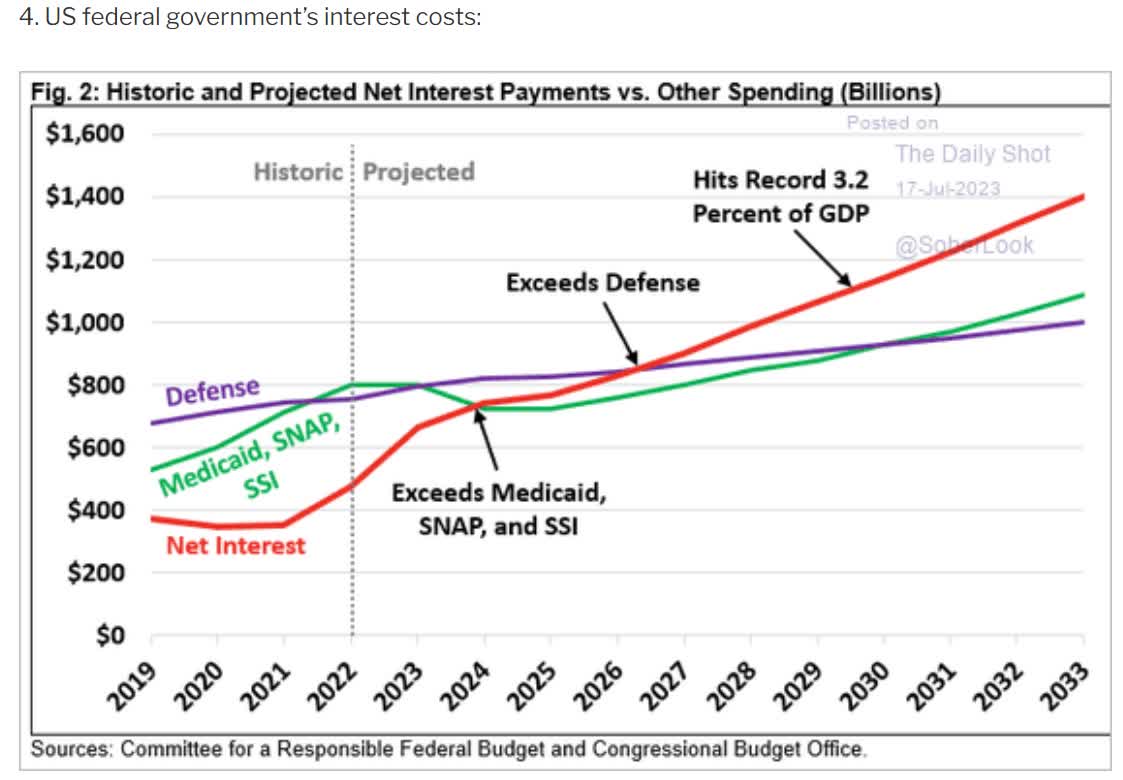

And let's not forget the real reason the Fed has to beat inflation. The national debt.

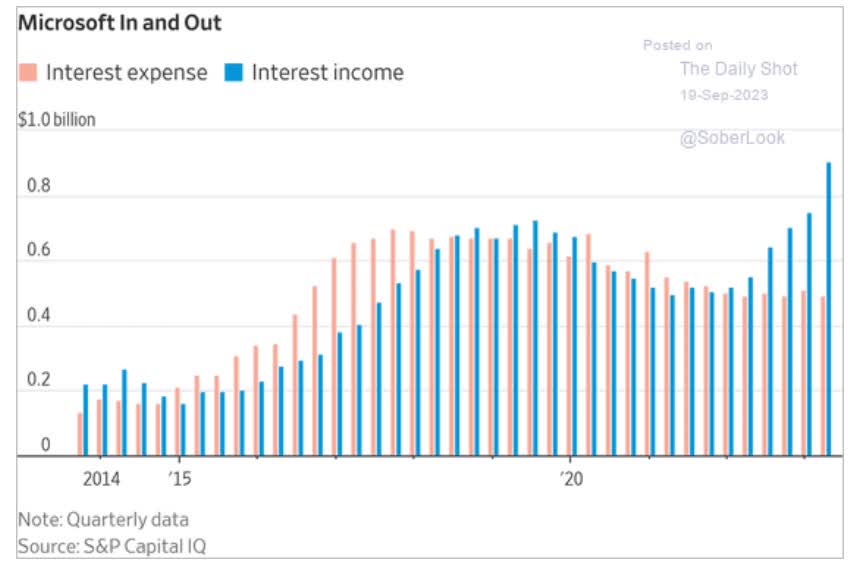

But didn't the government extend its bond profile like corporations did? For example, Microsoft gorged on 30-year bonds at record-low rates of 1%.

Now MSFT is sitting pretty and earning hundreds of millions in annual in extra free interest.

{kind=link}

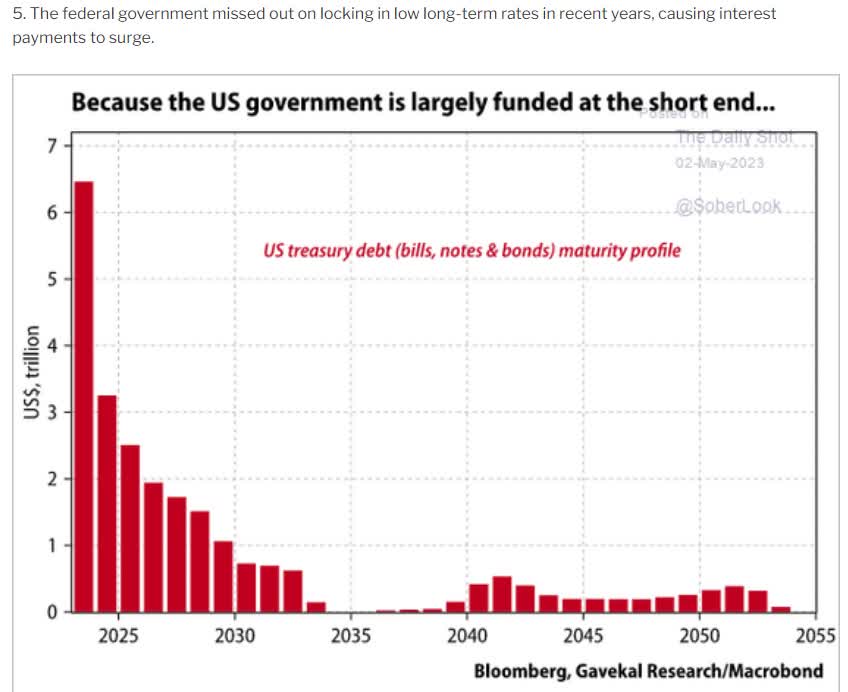

Nope, the US government didn't do that. Why? Who knows.

{kind=link}

The US Treasury has to refinance most of its debt in 2023 and 2024 and the Fed has no plans to cut short-term rates until November of 2024.

- Bloomberg thinks they might hold rates at 5.25% through 2026

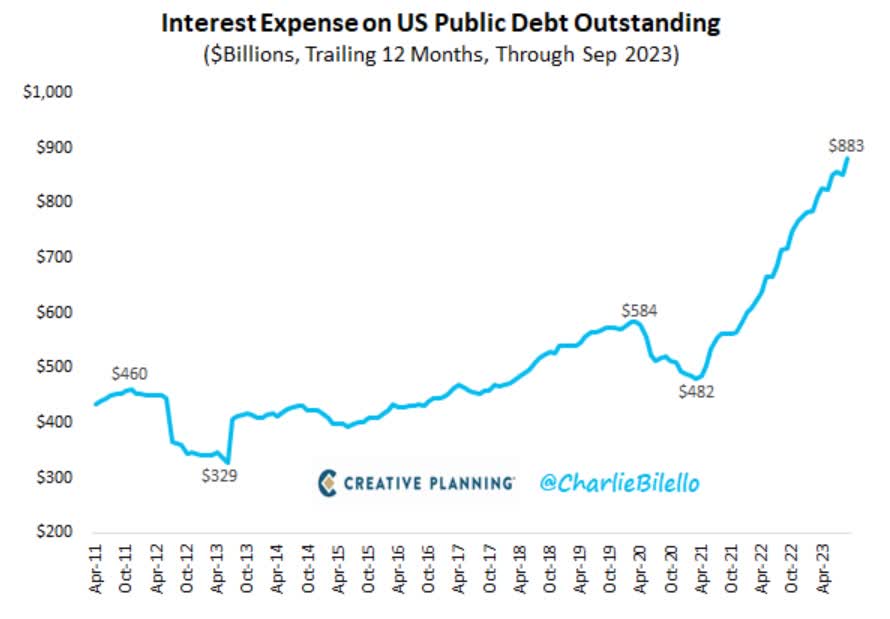

Higher for longer means interest costs are soaring.

{kind=link}

And guess what happens in the future?

{kind=link}

And that's assuming a 10-year yield of 3%!

By 2053 the national debt interest would be about 12% of GDP according to the Congressional Budget Office...assuming 10-year yields of 3%.

Can you see a problem here? The government can't afford inflation to stay high.

- 3% inflation = 5% 10-year yields long-term (historical norm)

- 4% inflation (3.7% today) = 6% 10-year yields long-term

- 5% inflation = 7% 10-year yields long-term

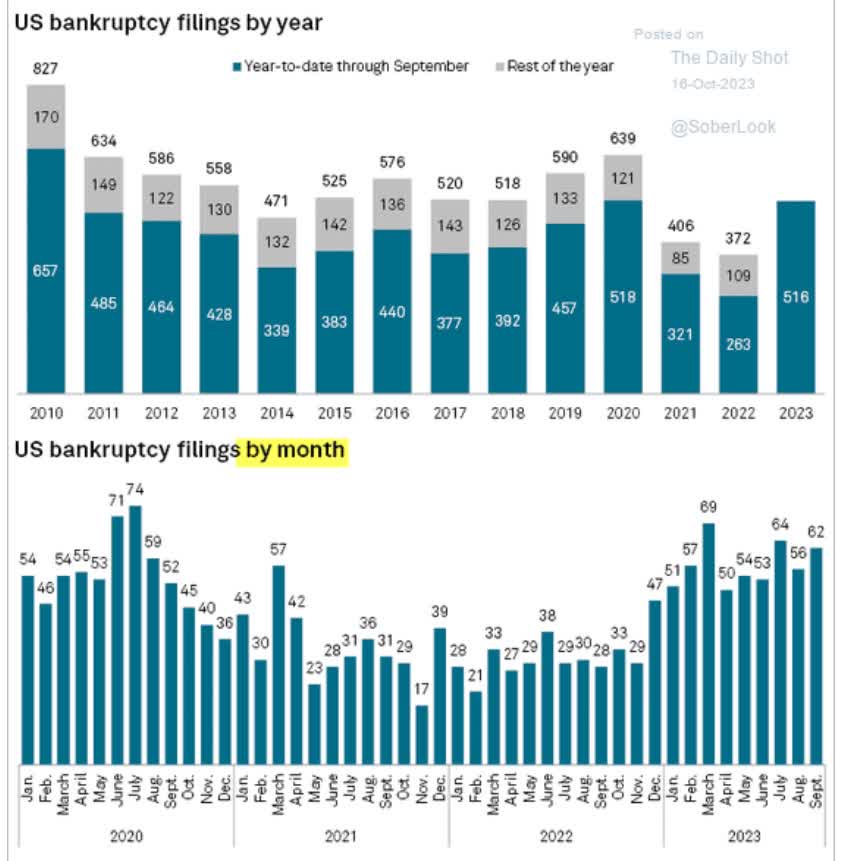

US corporations are already feeling the pinch from higher rates.

{kind=link}

Already bankruptcies in 2023 are double what they were at this time last year.

And they are on track to hit the highest level in 13 years.

Seeking Alpha

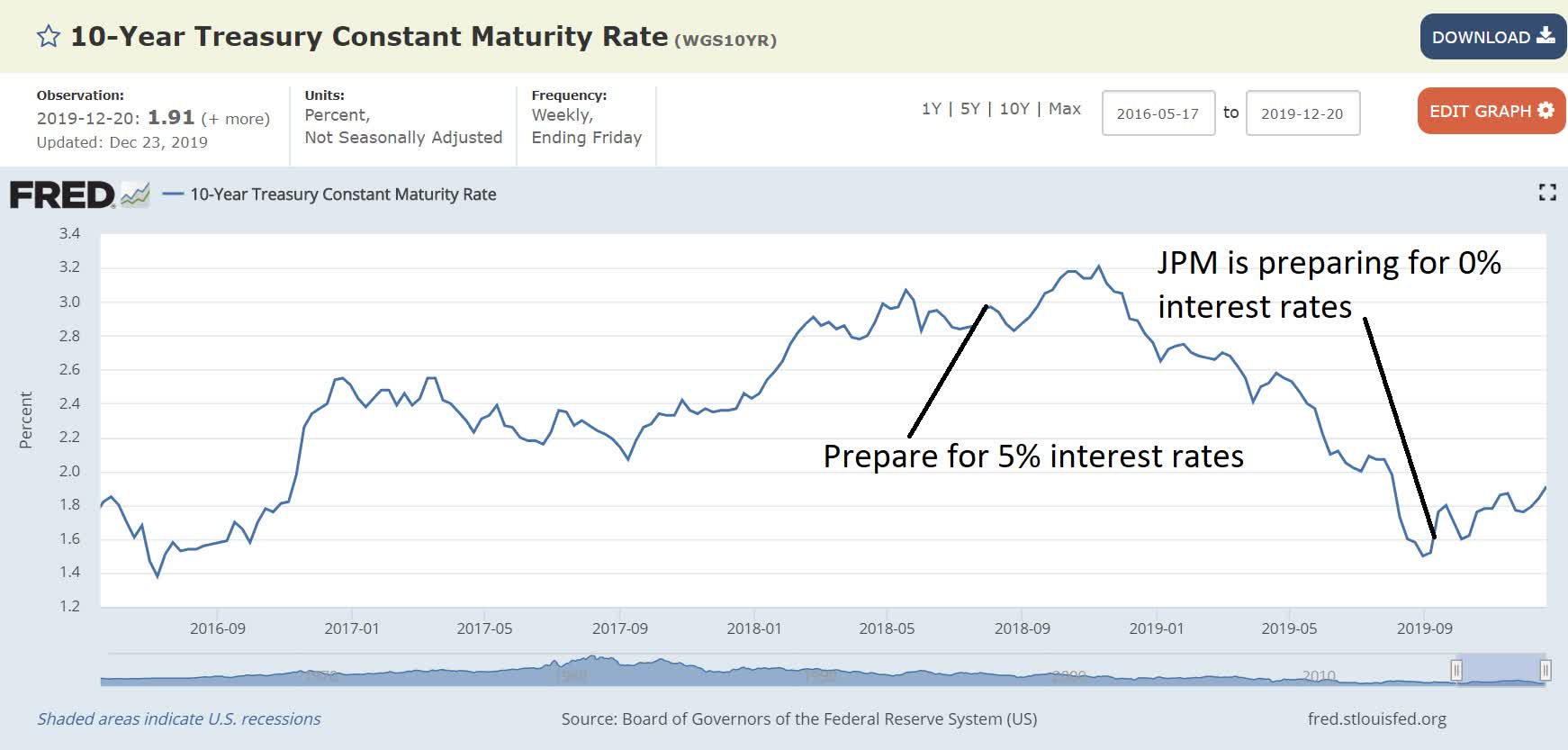

Jamie Dimon warns that the Fed might have to go a lot higher than the market currently expects. In fact, his worst-case scenario is the Fed going to 7%. Isn't Jamie Dimon famous for his hilariously wrong interest rate calls? Yup.

{kind=link}

{kind=link}

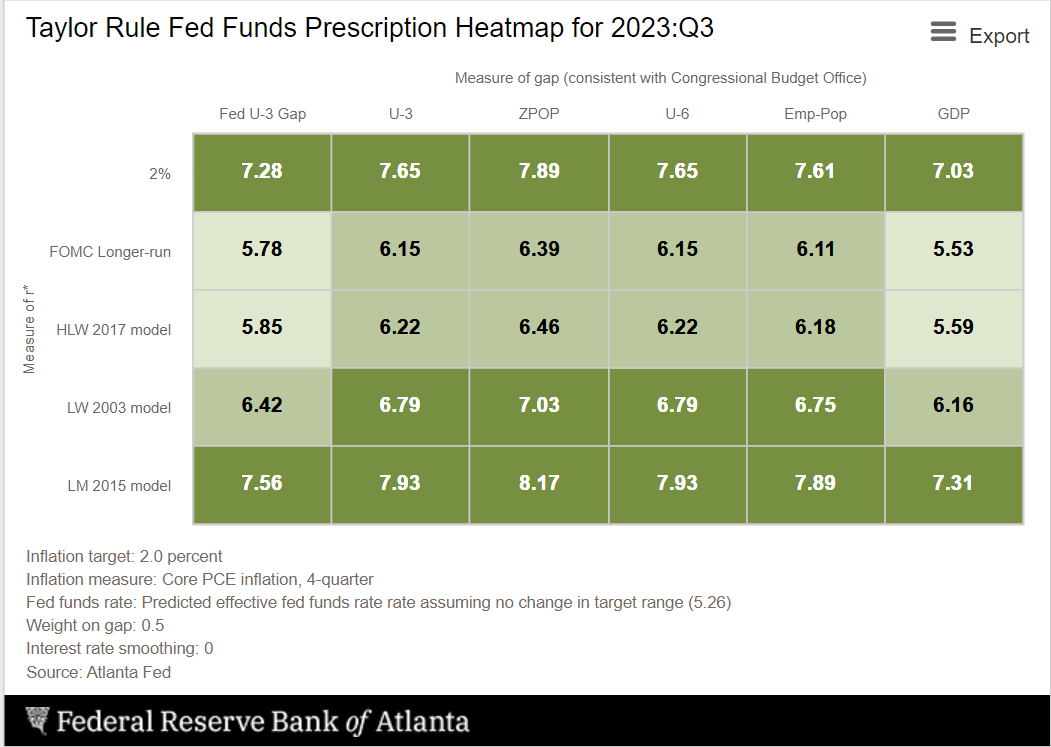

But if inflation doesn't come down (and it's been rising for 3 straight months now) the Fed's own models say it has to go a lot higher.

How high?

{kind=link}

If the Fed is serious about 2% inflation (and they keep saying they are) then the Fed's own models say 7% to 8% Fed funds rate RIGHT NOW is where they should be at.

So Jamie Dimon's 7% worst-case isn't even the Fed's worst-case, which is potentially over 8%.

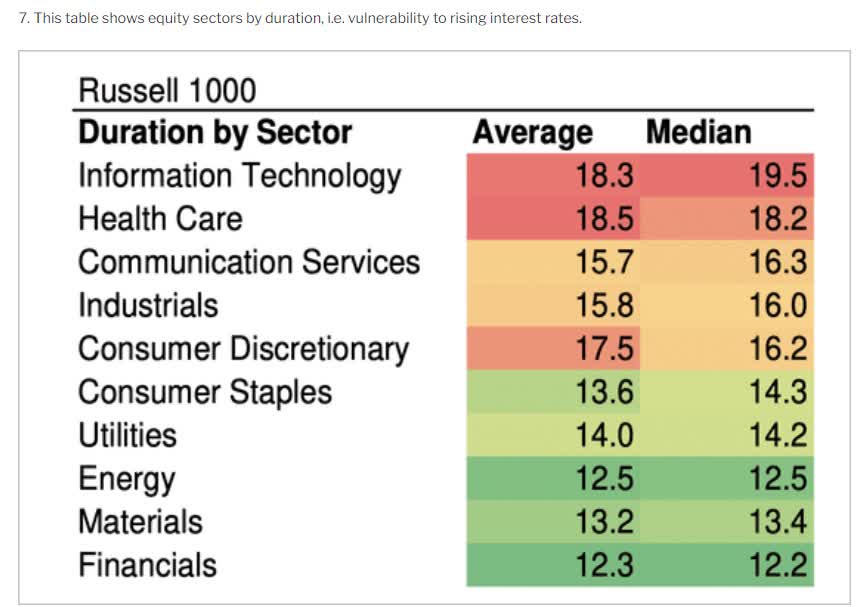

Can you imagine what the most rate-sensitive sector would do in a stagflation recession where earnings fall 20%, and then rates soar?

My oh my, that would be a really unpleasant year, to say the least.

Financials...The Perfect High-Yield Hedge Against The Stagflation Scenario

Remember what sector was the least rate-sensitive?

And do you remember which sector was right there with big tech in terms of driving mega earnings growth in Q3?

And do you know what sector is also flat this year? Financials.

{kind=link}

Financials historically trade at 13.5X earnings and are trading at 11.7X today, a 14% historical discount.

- mirror image of the Nasdaq's premium

So what are financials pricing in?

XLF Fundamentals

FactSet Research Terminal

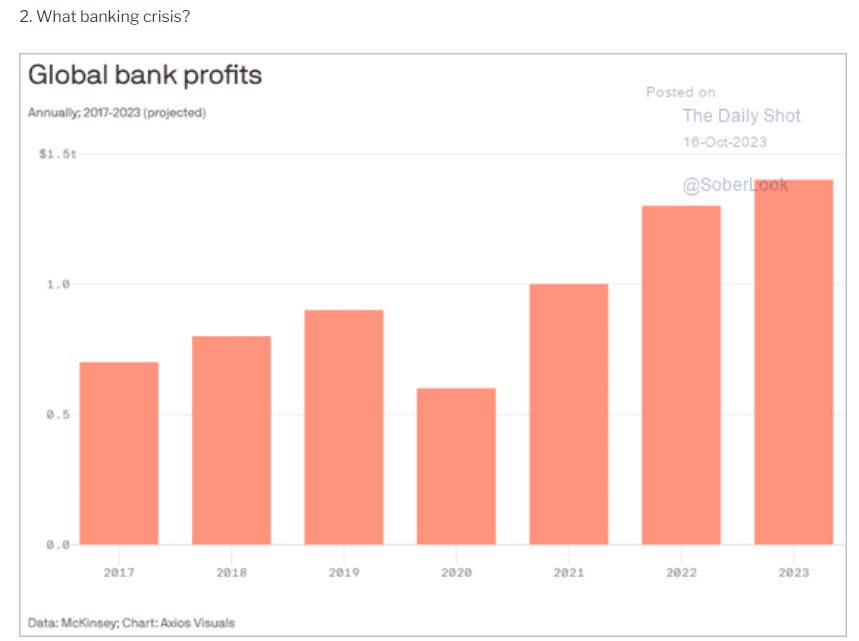

Financials are pricing in a mild recession this year and so far big financials like JPMorgan, Citigroup, and Wells Fargo are beating expectations.

{kind=link}

Do you see a disconnect here? Big tech is the most rate-sensitive yet big finance is actually benefiting from rising rates.

Yet big tech's earnings are expected to soar 20% this year while big financials are expected to shrink.

And in a higher for the longer world, which for now the data says is our reality, financials are likely to thrive and Big tech's high valuations could lead to years of stagnant returns or possibly a 30% to 50% bear market crash.

Could you buy XLF or VFH (Vanguard's financial ETF)? Sure, that would work.

- VFH is a better ETF and yields 2.5%

But I'm a stock picker, so here are two of my favorite 7% yielding US financial blue-chips that are coiled springs ready to soar, and potentially too cheap to ignore.

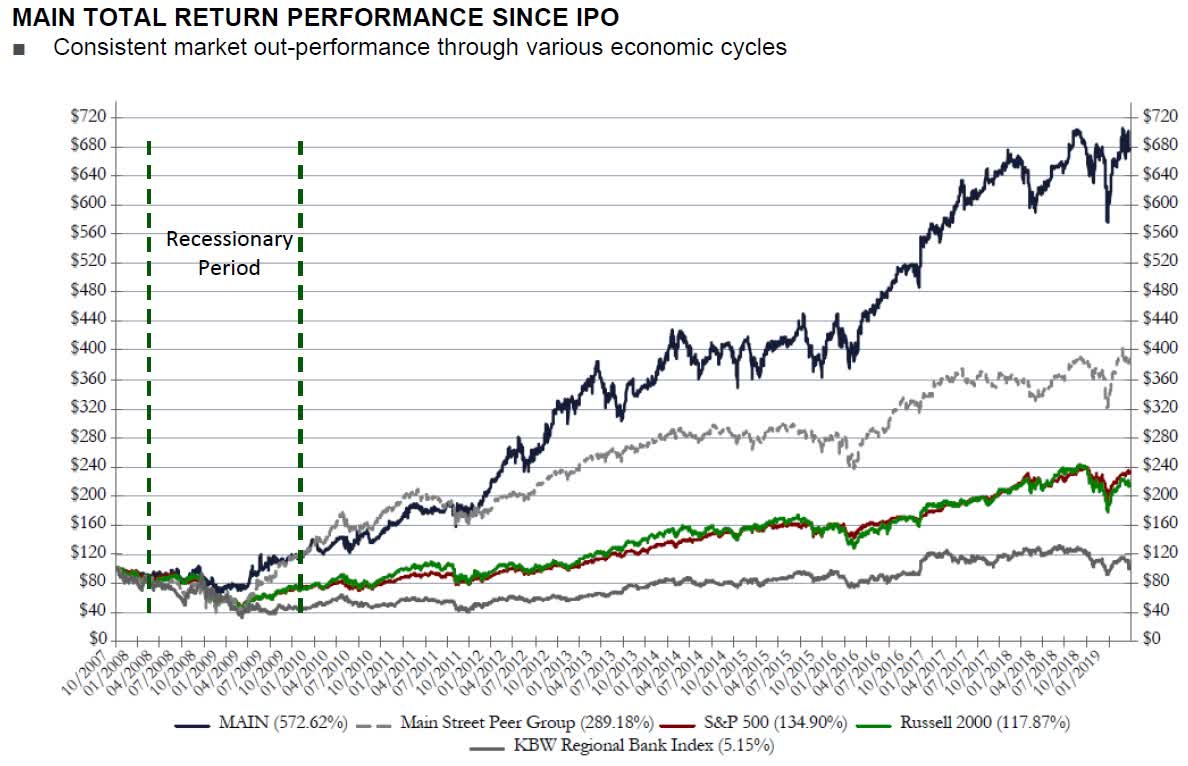

Main Street Capital ( MAIN )

Further Reading

Main Street is famous for 2 main things. First, it's one of the few internally managed Business Development Companies (BDCs).

It's founder-led, with CEO Dwayne Hyzak owning $336 million shares of this company.

- about 10% of the company

Hyzak started at MAIN in 2007 when it IPOd and started his career as a forensic accountant specializing in telling whether a company has a strong balance sheet or is cooking its books.

He led MAIN through the financial crisis as the only BDC to not cut its dividend.

Then it kept growing its dividend during the Pandemic.

12 consecutive years of dividend growth and 15 years without a cut (the only BDC to not cut across multiple recessions).

Why is MAIN so safe? Because its CEO is a master of risk management, AND while he gets paid $7 million per year (half in stock), his dividends from that $336 million position are paying him $23.5 million in dividends.

- $2 million per month

Do you think that the external management of a BDC really cares about dividend safety? How about the founder of the company who owns 10% of shares and is getting paid 3X his total compensation in dividends?

Yup, Hyzak is eating his own cooking and the Warren Buffett of his industry.

{kind=link}

I'm not kidding about Hyzak being the Buffett of BDCs. MAIN has doubled the historical returns of its peer group, just like Buffett has doubled the annual returns of the S&P for decades.

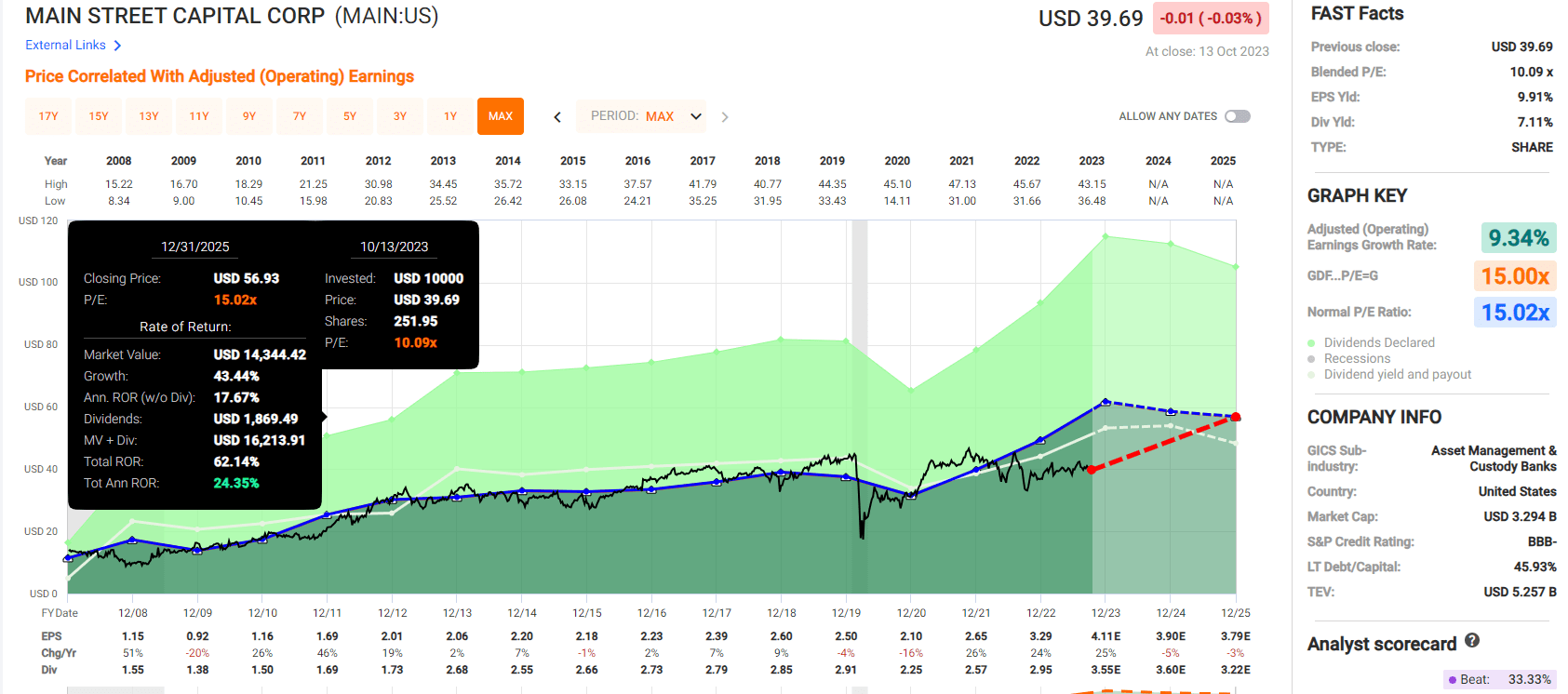

Fundamental Summary

- yield: 7.0% (5X S&P 500)

- dividend safety: 80% very safe (2.1% dividend cut risk)

- overall quality: 70% medium-risk blue-chip

- credit rating: BBB- stable (11% 30-year bankruptcy risk) - highest in the industry

- long-term growth consensus: 8.0%

- long-term total return potential: 15% vs 10.2% S&P 500

- current price: $40.24

- historical fair value: $57.23

- discount to fair value: 30% discount (strong buy) vs 5% overvaluation on S&P

- 10-year valuation boost: 3.6% annually

- 10-year consensus total return potential: 7.0% yield + 8.0% growth + 3.7% valuation boost = 18.7 % vs 10.1% S&P

- 10-year consensus total return potential: = 455 % vs 160% S&P 500.

You don't have to wait 10 years to earn Buffett-like returns from this blue-chip bargain hiding in plain sight.

{kind=link}

How would you like to triple the market's returns total returns both over the next few years and the next decade?

How about a 7% safe yield paid monthly? Well, that's what MAIN offers today. Better than the Nasdaq? I think so.

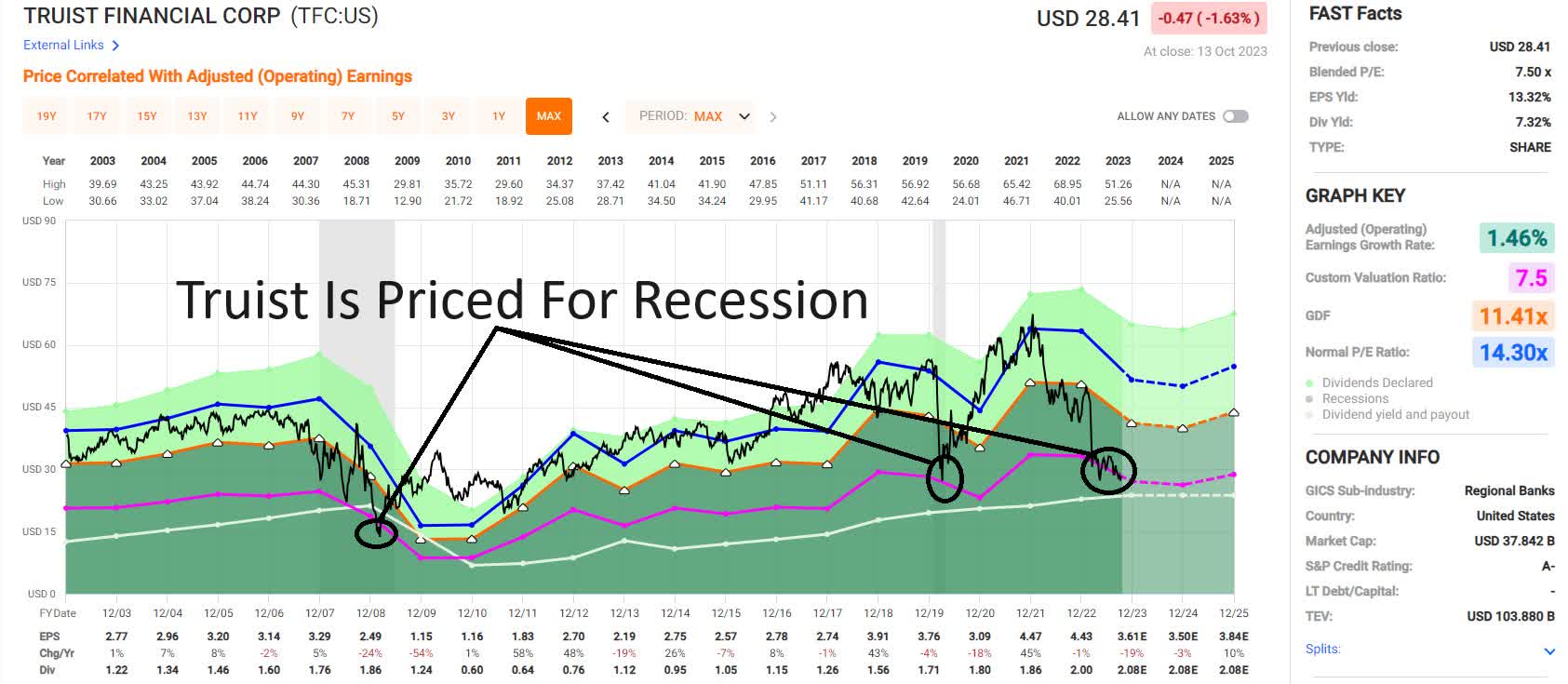

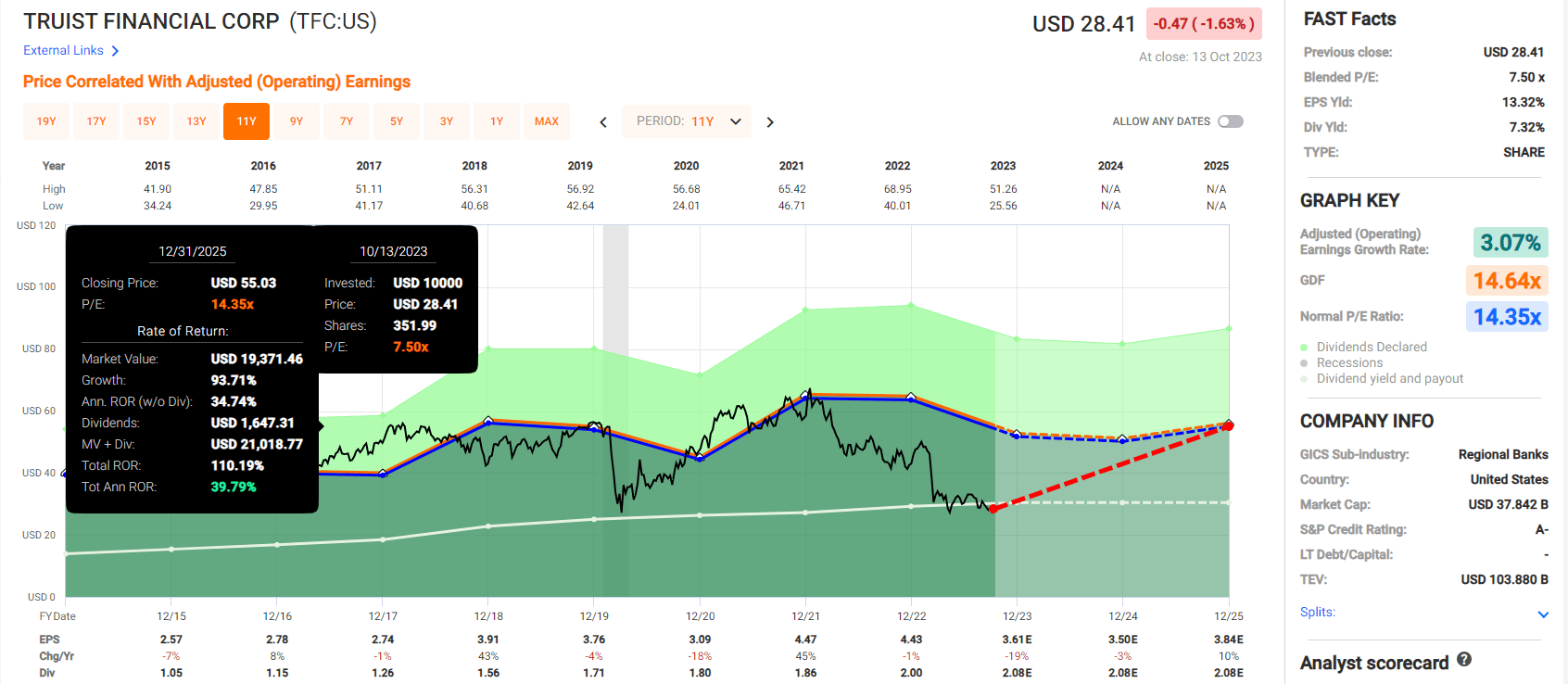

Truist Financial ( TFC )

Further Reading

{kind=link}

I'll make it very simple. Truist is priced as if we were in recession already. Not just a recession but a Pandemic/GFC-style economic catastrophe.

Is a recession likely in 2024 or 2025? Yes, 96% probability, according to the bond market.

Is it going to be a catastrophic meltdown? Almost certainly not.

So that makes Truist a 7% yielding coiled spring A-rated blue-chip.

- A- stable credit rating = 2.5% 30-year bankruptcy risk

Fundamental Summary

- yield: 7.2% (5X S&P 500)

- dividend safety: 70% very safe (3.0% dividend cut risk)

- overall quality: 64% medium-risk blue-chip

- credit rating: A- stable (2.5% 30-year bankruptcy risk)

- long-term growth consensus: 8.7%

- long-term total return potential: 15.7% vs 10.2% S&P 500

- current price: $28.99

- historical fair value: $60.28

- discount to fair value: 51% discount (Buffett-style "fat pitch" ultra value) vs 5% overvaluation on S&P

- 10-year valuation boost: 4.7% annually

- 10-year consensus total return potential: 7.2% yield + 8.7% growth + 7.4% valuation boost = 23.1% vs 10.1% S&P

- 10-year consensus total return potential: = 699 % vs 160% S&P 500.

{kind=link}

Bottom Line: Big Tech Is Priced For Perfection, And These 7% Yielding Blue-Chips Are Priced For Catastrophe

I'm not saying the magnificent 7 aren't world-beaters.

I'm saying that the idea that the Nasdaq is going to report 60% earnings growth in the coming 3 years is AI-driven hype and hopium.

Are interest rates going to soar? Probably not.

Might they keep rising? Yes, there is a very plausible way that could happen.

Right now, financials are the anti-tech.

Earnings are crushing expectations (very low bar to clear).

Valuations are dirt cheap, especially for MAIN and TFC.

These are high-quality, safe 7% ultra-yield blue-chip bargains priced for an economic collapse for which there is no evidence.

If you're looking to earn close to 100% potential returns within 2 to 3 years, while locking in a mouthwatering 7% yield and likely beating the Nasdaq in the coming years, TFC and MAIN are two amazing opportunities today.

For further details see:

Beware Big Tech And Buy These 7% Yielding Blue-Chip Bargains