CLDT - Beware Of The Risks Of Chatham Lodging Trust

2023-06-29 12:42:25 ET

Summary

- Chatham Lodging Trust has underperformed the Real Estate Select Sector SPDR Fund ETF this year, declining by 22%.

- Despite showing signs of recovery from the pandemic, the REIT's high debt load and low dividend yield make it unattractive to investors.

- The company's net interest expense has increased due to high interest rates, consuming 67% of its operating income.

- Although it's trading at a low forward price-to-FFO ratio, the likelihood of continued underperformance due to either a recession or persistently high inflation and interest rates makes it a risky investment.

Chatham Lodging Trust ( CLDT ) has dramatically underperformed the Real Estate Select Sector SPDR Fund ETF ( XLRE ) this year, as it has declined 22% whereas the ETF has remained essentially flat. Due to its underperformance, the REIT has become remarkably cheap, as it is trading at a forward price-to-FFO ratio of only 7.5 . However, Chatham Lodging Trust has a material debt load, with its interest expense consuming most of its operating income. Given also the volatile performance record of the REIT and its low dividend yield (3.2%), the stock does not appear attractive, even after its decline this year.

Business overview

Chatham Lodging Trust is a self-advised REIT that engages in investing in upscale, extended-stay hotels and premium, select-service hotels. The trust owns 39 hotels, which have a total of nearly 6,000 rooms in 16 states.

Chatham Lodging Trust was severely hurt by the coronavirus crisis, which caused a collapse in global air traffic. The impact of the pandemic was especially pronounced on business travel, which may not return to pre-pandemic levels anytime soon due to a persistent trend for remote business meetings.

On the bright side, the pandemic has subsided, and hence global travel is in recovery mode.

{kind=link}

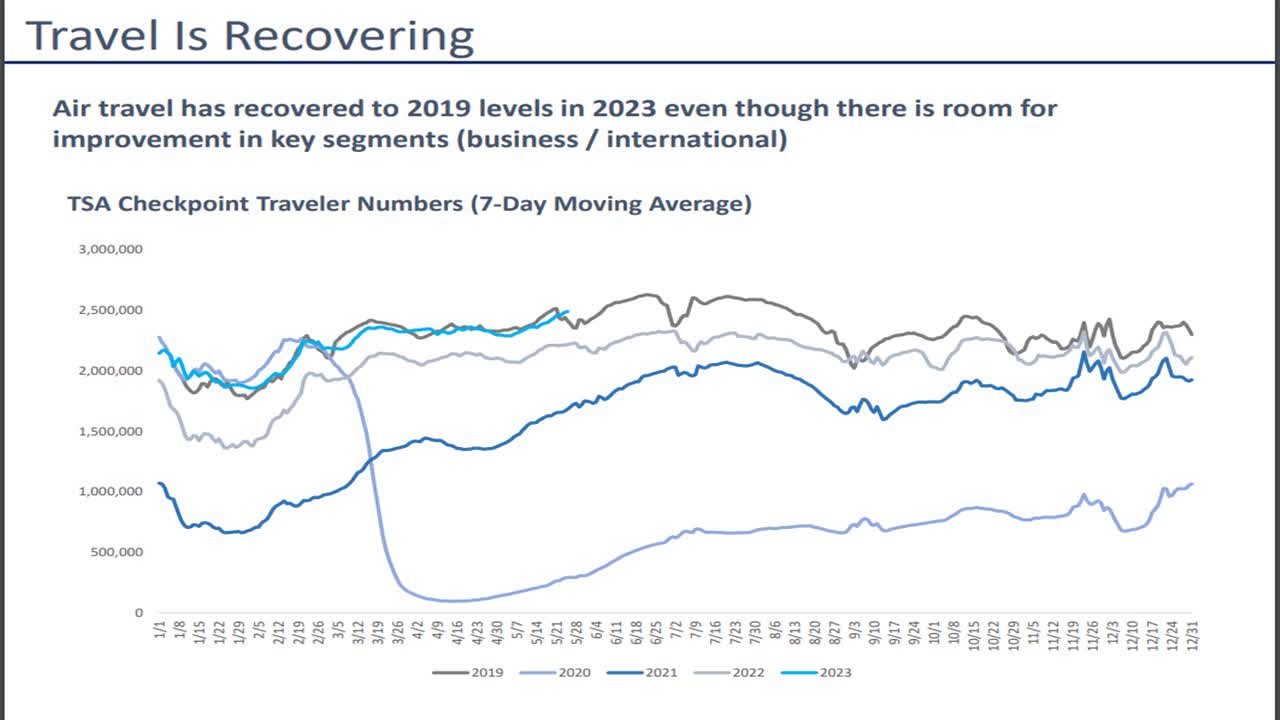

Source: Investor Presentation

As shown in the above chart, global air traffic has recovered to pre-pandemic levels this year. The premium hotels of Chatham Lodging Trust are likely to greatly benefit from the ongoing recovery of global travel.

Indeed, early signs of a recovery were evident in the first quarter. Chatham Lodging Trust grew its EBITDA 34% and more than doubled its FFO per share over the prior year's quarter, from $0.07 to $0.16, surpassing the analysts' consensus by $0.03. The 25% growth of revenue per available room (RevPAR) in the quarter was the fourth best among all lodging companies.

The growth in RevPAR resulted from similar growth in both occupancy and average daily rate, with both increasing by approximately 14%. Compared to 2019, RevPAR fell 6%, primarily due to the performance of the four Silicon Valley hotels, which negatively affected results by 700 basis points. However, excluding those hotels, RevPAR edged up almost 1% compared to 2019.

More importantly, in the first four months of 2023, compared to 2019, RevPAR improved every month, with decreases of 12%, 5%, 4%, and less than 2%, indicating a positive trend and a sign that business travel is continuing to recover across the country, even in Silicon Valley. Leisure travel also remained strong, with strong growth in all leisure markets. It is also remarkable that Chatham Lodging Trust has exceeded the analysts' FFO-per-share estimates for 8 consecutive quarters. This is a testament to a sustained recovery of the business from the pandemic.

Moreover, Chatham Lodging Trust has begun to observe a recovery of the demand from countries like Korea, Japan, Taiwan, and China in its Silicon Valley hotels and Bellevue, Washington Hotel. However, the decline in intern programs this year due to reduced programs by large tech companies will probably result in a decline in intern revenue of 80%-90% across the four hotels in Silicon Valley and Bellevue, Washington. Nevertheless, the strong recovery of the other hotels is likely to offset this headwind. Indeed, analysts expect Chatham Lodging Trust to grow its FFO per share 3% this year, from $1.19 to $1.23.

Debt

Just like many other REITs, Chatham Lodging Trust has been significantly affected by the adverse environment of multi-year high interest rates. Due to the unprecedented pace of interest rate hikes executed by the Fed, the net interest expense of the REIT has increased 10% , from $24.2 million in 2021 to $26.5 million in the last 12 months. This increase is much smaller than the increase experienced by other REITs, but it is material. Indeed, net interest expense is currently consuming 67% of the operating income of Chatham Lodging Trust.

Even worse, the Fed recently indicated that it could implement a few more rate hikes in order to restore inflation to its target range of 2.0%-2.5%. The additional rate hikes are likely to increase the interest expense of the REIT even more, as the REIT will have to refinance a portion of its debt in the upcoming years. The company has a debt maturity of $301 million next year and about $350 million in 2027. Given the current market capitalization of $464 million of the stock, the debt maturity next year is undoubtedly significant.

The net debt (as per Buffett's calculation, net debt = total liabilities - cash - receivables) of Chatham Lodging Trust is currently standing at roughly $496 million . As this amount exceeds the market capitalization of the stock, it is certainly burdensome, particularly given the high interest expense of the REIT. To cut a long story short, Chatham Lodging Trust is adversely affected by multi-year high interest rates due to its debt load. In fact, its debt is the primary reason behind the poor performance of the stock this year in my view.

Dividend

Due to the impact of the pandemic on its business, Chatham Lodging Trust suspended its dividend for nearly three years, from the beginning of 2020 to the end of 2022. Even worse, the REIT is currently offering an annualized dividend of $0.28 , which is 79% lower than the annualized dividend of $1.32 offered in 2019. As a result, the stock is now offering a dividend yield of 3.2%, which is much lower than the median dividend yield of the REIT sector ( 5.0% ).

On the one hand, the REIT has a forward FFO payout ratio of only 23% and hence it seems to have ample room to raise its dividend. On the other hand, due to its high debt load, the trust may not raise its dividend meaningfully for the foreseeable future. In addition, the suspension of the dividend for nearly three years proves that the REIT is highly vulnerable to economic downturns. This is an important risk factor to consider, as the Fed is doing its best to cool the economy and may cause a recession at some point in the near future.

Valuation

Chatham Lodging Trust is currently trading at a forward price-to-FFO ratio of 7.5. As the REIT is expected by analysts to remain in recovery mode next year and grow its FFO per share 11% in 2024, the stock is trading at only 6.7 times its expected FFO in 2024. These FFO multiples are markedly low.

If a recession does not show up and interest rates begin to moderate next year, Chatham Lodging Trust may have significant upside potential. If the REIT reverts to a price-to-FFO ratio of 10.0 next year, it will have approximate upside potential of 50% (=10/6.7 - 1). This is not an extreme scenario, as it will simply mean that the stock will revert to the level it was at just five months ago.

On the other hand, if a recession does not show up, the economy is likely to remain somewhat heated and hence the Fed may keep interest rates at multi-year highs for a prolonged period. In such a case, high interest rates are likely to increase the interest expense of the REIT even further. Overall, Chatham Lodging Trust has significant upside potential in the positive scenario (essentially a perfect landing executed by the Fed, i.e., restoration of inflation without a recession), but it is likely to continue to underperform in the most likely scenarios, which include either a recession or persistently high inflation and interest rates.

Final thoughts

Due to its vast underperformance this year, Chatham Lodging Trust has become exceptionally cheaply valued. As a result, it may highly reward investors in the positive scenario of a soft landing of the economy. However, I always recommend avoiding companies with a high debt load, as these stocks are risky and tend to underperform the broad market over the long run. The dramatic underperformance of Chatham Lodging Trust over the last decade (-47% vs. +165% of the S&P 500) is a testament to the risk of the REIT in my view.

For further details see:

Beware Of The Risks Of Chatham Lodging Trust