BYND - Beyond Meat's Future Is More Uncertain Than Ever

2023-11-10 10:57:23 ET

Summary

- Beyond Meat's Q3 results were weaker than expected, with declining revenues and negative gross profits.

- While the stock bounced on the news, Beyond Meat's share price is likely to resume its longer-term downward trend.

- Beyond Meat could be an attractive short at this point, but this is a crowded trade.

- Pairing a short position in Beyond Meat with a long position in Oatly, a similar company with better fundamentals, could reduce risk somewhat.

Beyond Meat ( BYND ) just preannounced third quarter results, which were significantly weaker than expectations. Revenues continue to slide and gross profit was negative again. While free cash flow was positive, this was only achieved through working capital management. It is becoming increasingly difficult to see how Beyond Meat remains a viable company at this point. The bounce in Beyond Meat’s share price was completely unjustified, providing a short opportunity.

While Beyond Meat’s share price is highly likely to trend downward over time, the Beyond Meat short is a crowded trade. The company’s stock also has a history of dramatic moves which are not justified by the company’s fundamentals. Some of this risk could be reduced by entering a pair trade with Oatly ( OTLY ), which is in a similar position but has far better fundamentals and a significantly lower valuation. Investors would still need to be prepared for highly adverse share price movements in the near term though as sentiment fluctuates and shorts potentially exit their positions.

Bull Case Failure

I had at one point suggested that Beyond Meat could be an attractive, albeit highly speculative, long opportunity. This was really dependent on the company’s ability to maintain strong branding, drive widespread adoption of its products and reduce the cost of its products below real meat.

Beyond Meat appears to have failed on all of these fronts. The plant-based meat market is now relatively fragmented and Beyond Meat is facing pricing pressure. Plant-based meat also remains a niche product with costs generally well above real meat.

While I managed to make money on an investment in Beyond Meat, I haven't really considered the company a viable long since early 2021. Despite this, until now I still felt the company could turn itself around if it could reach price parity with meat. With the latest results and Beyond Meat's forward plan, I don't really see how the company can resolve its issues.

Financial Results

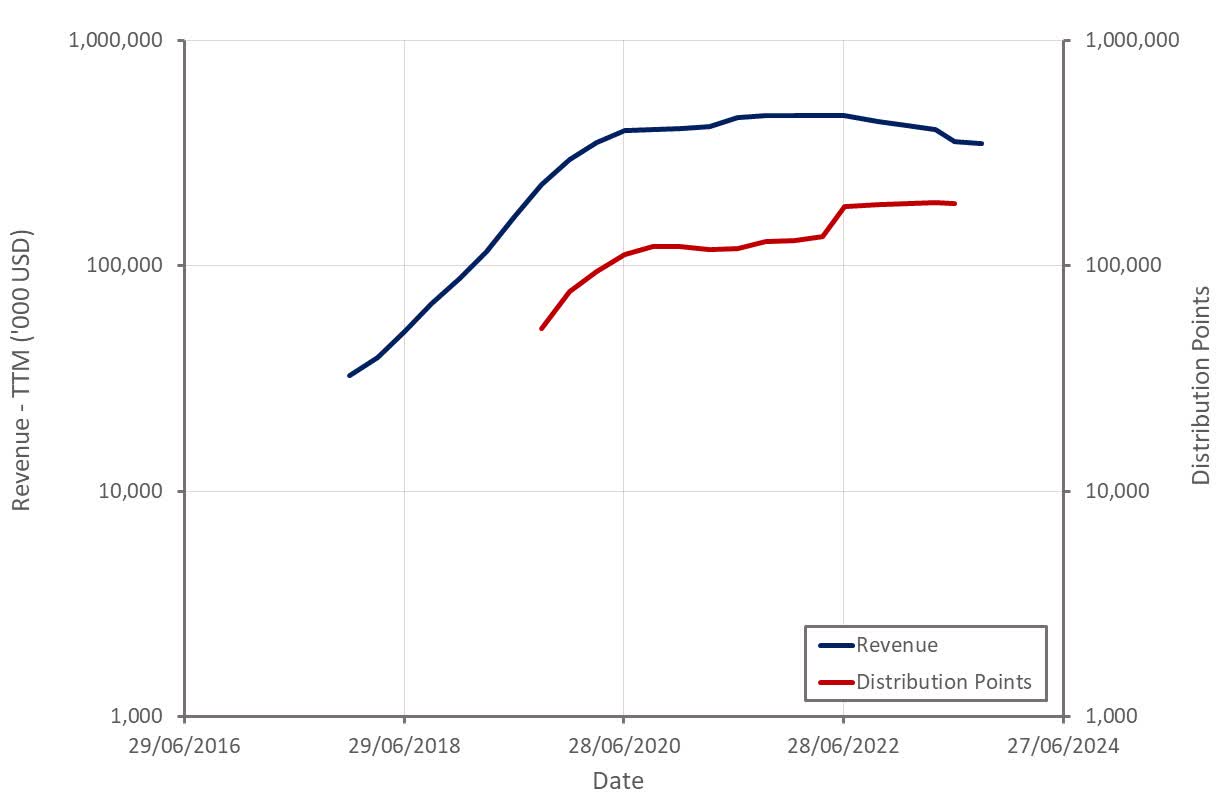

Beyond Meat was anticipating a return to growth in the third quarter of 2023, but instead saw a 9% YoY decline in revenue. International growth was strong , but this was more than offset by weak sales in the US. The company also lowered full year guidance, which now implies roughly an 18% YoY revenue decline in the fourth quarter. Net revenues are expected to be in the range of 330-340 million USD , representing a 19-21% decline compared to 2022.

Figure 1: Beyond Meat Revenue (source: Created by author using data from Beyond Meat)

{kind=link}

Third quarter weakness was attributed to sector-specific and consumer headwinds , including soft demand in the plant-based meat category in the US. Given that Beyond Meat generally offers premium priced products, inflationary pressures on consumer budgets could be an issue.

Burger King recently stated that it has no plans to expand its plant-based offerings in the US. Plant-based options are more popular internationally, particularly in Western Europe, than they are in the US. While demand trends are reportedly stable, the lack of expansion plans suggests that demand isn't particularly strong.

Archer-Daniels-Midland has also seen lower demand for plant-based proteins. This was attributed to destocking and weak end market demand, which is expected to continue into 2024.

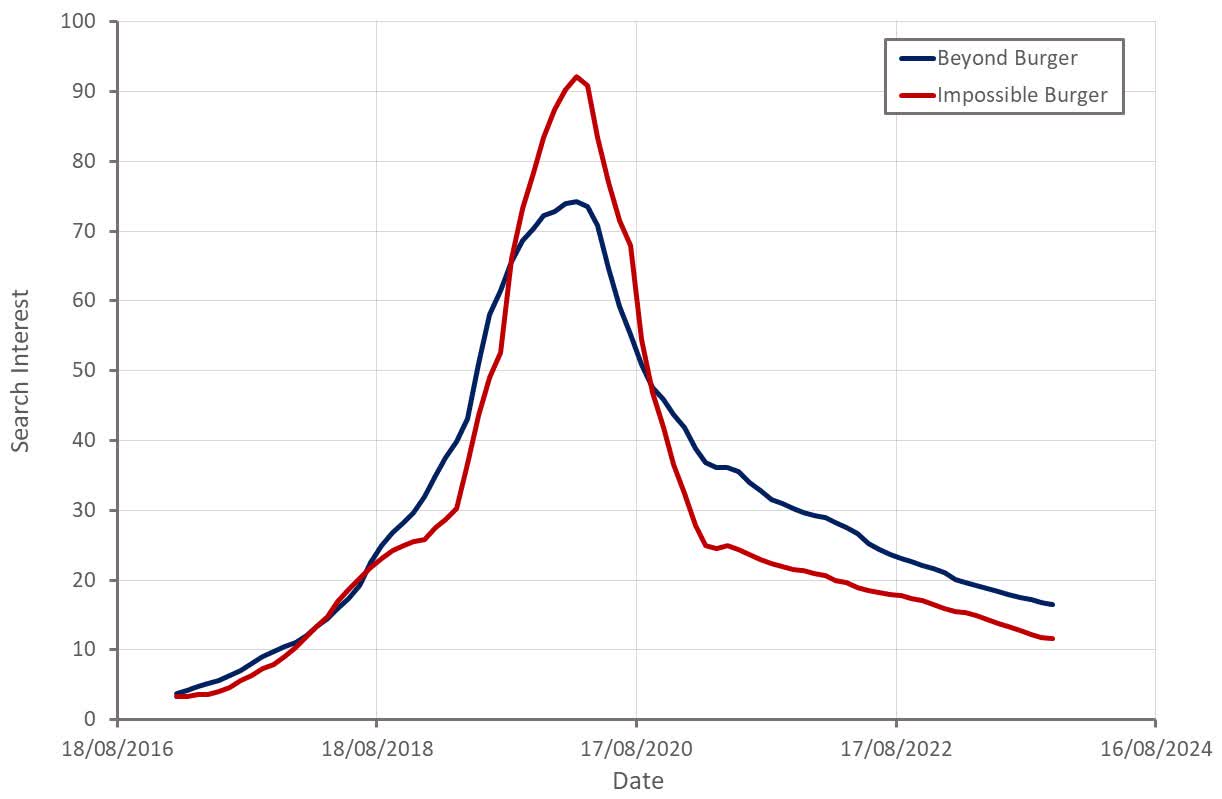

Health concerns also appear to be an ongoing issue. Beyond Meat has spent considerable time on recent earnings calls discussing misinformation regarding its products and has suggested countering misinformation is an important part of its strategy going forward. Health concerns could also be a growing issue for Oatly .

Figure 2: Beyond Burger Search Interest (source: Created by author using data from Google Trends)

{kind=link}

While much of this may be due to the macro environment, it is hard to believe that there are not also some Beyond Meat specific issues. Search data seems to indicate that Beyond Meat and Impossible Foods have been subject to roughly the same trends. This broadly echoes previous commentary from Beyond Meat regarding market share. On the negative side, Beyond Meat planned to drive sales through promotions in the third quarter but this proved to be ineffective . If promotional activity is not impacting sales, it would suggest that pricing is only one of Beyond Meat's problems.

Beyond Meat's gross profit margin in the third quarter was around -9%. This was the result of both declining prices and rising cost per pound. Gross profit for the full year is now expected to be approximately breakeven, which implies gross profit margins of around -2% in the fourth quarter.

Full year operating expenses are now expected to be 245 million USD or less, before one-time separation costs and non-cash savings related to previously granted, unvested stock-based compensation associated with the company’s reduction in force. This suggests that operating profit margins will continue to fall in the fourth quarter.

Figure 3: Beyond Meat Profit Margins (source: Created by author using data from Beyond Meat)

{kind=link}

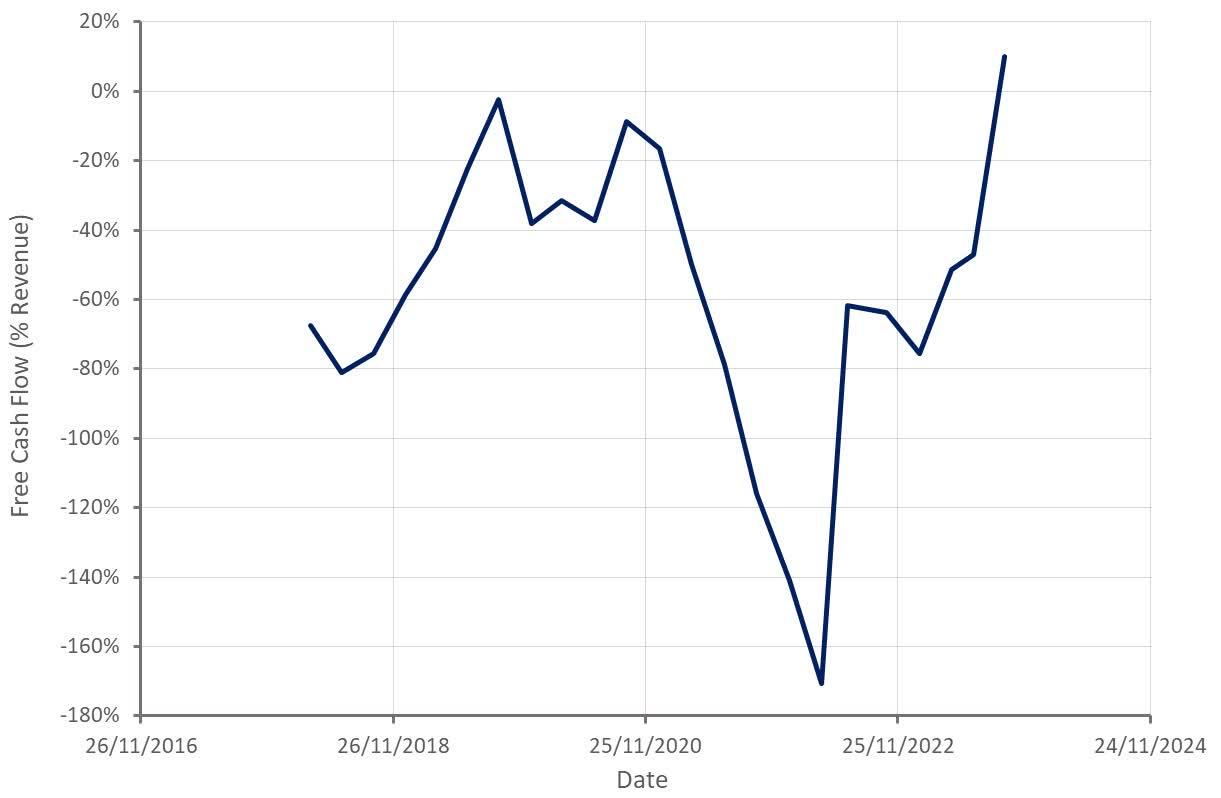

Beyond Meat's free cash flow is generally less than its operating profits as the company has to invest in growth (working capital and PP&E). With the business shrinking, working capital can become a source of cash though. Beyond Meat is now taking this to the extreme to reduce cash burn. Investors should not mistake this for a reduction in losses though. Using working capital as a source of cash is not sustainable. Management has stated that positive cash flows from the third quarter will not be sustained going forward. At some point in the near future Beyond Meat will no longer be able to reduce working capital, and at this point cash outflows will blow out again.

Figure 4: Beyond Meat Free Cash Flow Margin (source: Created by author using data from Beyond Meat)

{kind=link}

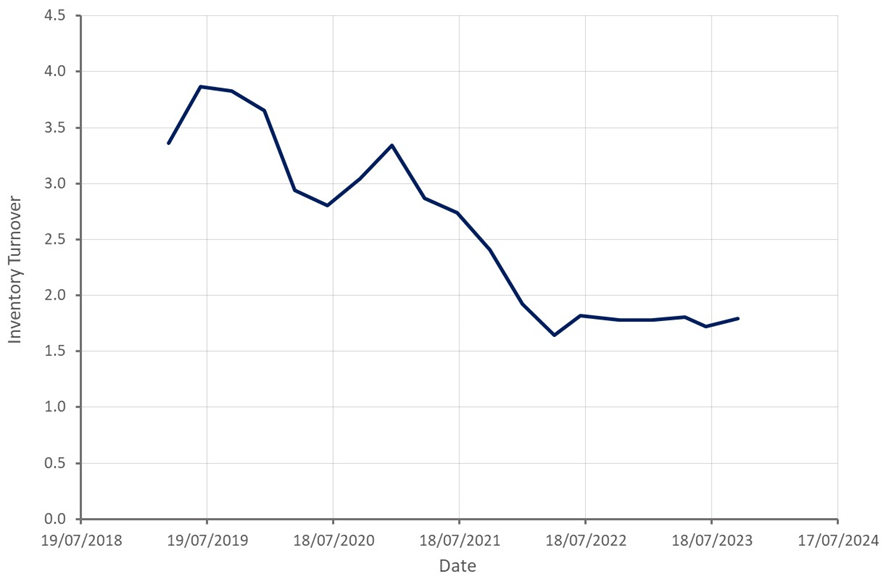

Beyond Meat has reduced inventory levels in each of the past 6 quarters, but this can only be taken so far before low inventory levels begin to cause operational issues.

Figure 5: Beyond Meat Inventory Turnover (source: Created by author using data from Beyond Meat)

{kind=link}

Liquidity and Solvency Risk

Beyond Meat has a shrinking runway in which to reach breakeven, and its third quarter results have substantially increased uncertainty regarding the company's viability. Beyond Meat can cut operating expenses but falling revenue is making this process difficult. In addition, high fixed costs associated with production are undermining gross profit margins, which may be a more difficult issue to resolve. This is exacerbated by the fact that Beyond Meat's product range has expanded while revenues have declined, undermining economies of scale at the product level significantly.

Beyond Meat is pursuing a number of initiatives to reduce its losses:

- A 19% reduction in its global non-production workforce (65 employees)

- Higher prices to support gross margin expansion

- Inventory management to reduce cash burn

- Focus on channels and geographies that are growing

- Counter misinformation

These initiatives do not inspire confidence for a number of reasons. Price increases risk exacerbating the decline in sales, which may make the company’s current problems worse. Inventory management is a one-time lever that does not improve profitability. Countering misinformation through marketing will add to expenses, and if this is ineffective it will increase losses rather than reduce them.

Beyond Meat's numbers suggest around 810 total employees, with roughly 470 in production roles and 340 in non-production roles. While cutting overheads is necessary, Beyond Meat must also drive greater productivity from its manufacturing operations.

The reduction in force, and a reduction in hiring, is expected to lower cash operating expenses by 9.5-10.5 million USD in 2024, along with 1-2 million USD of non-cash savings. Beyond Meat expects to incur around 2-2.5 million USD of cash expenses in the fourth quarter related to the reduction in force. Given the size of Beyond Meat's losses, these numbers aren't really material.

In my opinion Beyond Meat probably has something like an 18-36 month runway, dependent on to what extent losses can be reduced. While Beyond Meat has a lot of liabilities, there is nothing substantial coming due in the next few years. Long-term liabilities are a mix of financial leases, operating leases and convertible senior notes.

Table 1: Estimates of Beyond Meat's Cash, Inventory and Long-Term Liabilities (source: Created by author using data from Beyond Meat)

Based on its most recent results, I believe it is highly likely that Beyond Meat will need to raise capital again in the future, but this will likely be difficult. The company already has a large amount of debt, which has extremely attractive terms. Trying to issue debt at the moment would not be feasible as the terms would be prohibitive.

Beyond Meat’s market capitalization has held up reasonably well given the company’s poor performance over the past few years, making issuing equity a possibility. Cash requirements at the moment are probably something like 200 million USD per year (excluding liquidation of working capital). Beyond Meat can certainly issue more equity but this is just kicking the can down the road unless the company can dramatically reduce costs.

Beyond Meat's convertible notes are due in 2027, which is really the day of reckoning for the company. Beyond Meat needs to have a profitable and growing business by this time to have a chance of repaying this debt. Beyond Meat may be able to negotiate something with the debtholder, but the outcome is unlikely to be favorable for existing shareholders.

Short Opportunity

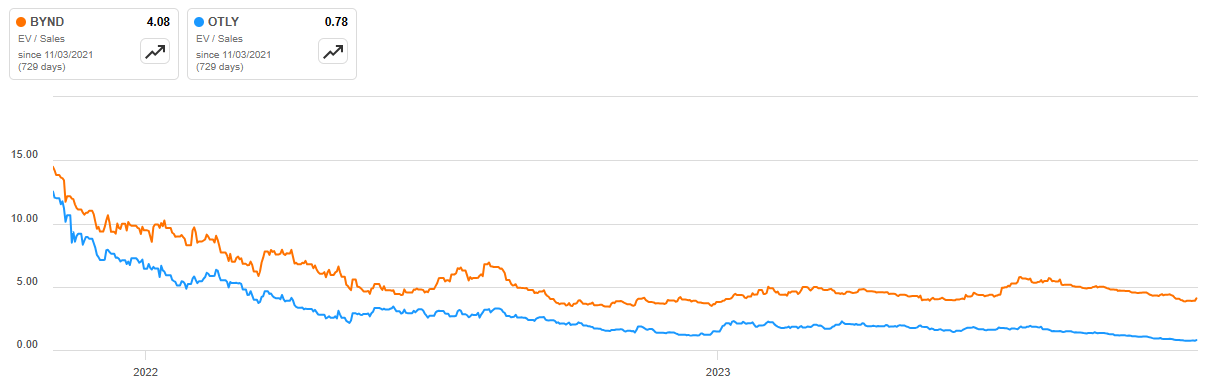

Taking a short position in Beyond Meat is risky given the stock’s volatility and the fact that short interest as a percentage of float is already nearly 50%. This risk could potentially be reduced slightly by taking an offsetting long position in Oatly, which is in a similar position to Beyond Meat but has far better fundamentals, and a much lower valuation:

- Oatly is still growing sales

- Oatly's gross profit margins are positive and have been improving

- Oatly's problems are concentrated in Asia

- Oatly's core European business is profitable and growing

- Similar to Beyond Meat, Oatly doesn’t have large lease or debt obligations due in the near-term.

- While Oatly has much less debt, it is incurring around a 50 million USD annual interest expense, while Beyond Meat has modest interest income.

- Oatly's low valuation makes issuing equity less feasible

Investors would need to keep in mind that fundamentals may not matter in the short-term though, and a highly adverse movement in this position could occur before it begins to pay off. At some point these factors will begin to matter, particularly as Oatly’s struggles in Asia provide it with a clear path to resolving a lot of its issues.

Figure 6: Beyond Meat and Oatly EV/S Multiple (source: Seeking Alpha)

{kind=link}

Risks

- The Beyond Meat short trade is crowded, meaning borrowing costs are high and there is an elevated risk of a short squeeze driving the stock price higher.

- Beyond Meat is a high beta stock that has exhibited significant momentum in the past. Regardless of company fundamentals, Beyond Meat's stock could move significantly higher if equities trend upward.

- Beyond Meat still has considerable time in which to resolve its issues before it may need access to more capital.

- Interest rates may have already peaked, and lower interest rates could make refinancing debt or raising capital more feasible.

For further details see:

Beyond Meat's Future Is More Uncertain Than Ever