BGH - BGH: Double-Digit ~10% Yield With A Double-Digit Discount

2023-11-14 21:08:32 ET

Summary

- Barings Global Short Duration High Yield Fund offers a fully covered double-digit distribution yield and trades at a double-digit discount.

- The fund's focus on shorter durations has helped its performance compared to other fixed-income investments during the current rate environment.

- BGH's portfolio has a higher allocation to lower credit quality issuers, but its diversified exposure and discounted portfolio reflect some of the heightened credit risk.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Barings Global Short Duration High Yield Fund ( BGH ) has been having to deal with higher rates just like any other fixed-income fund. However, the allocation to high-yield exposure and a particular focus on shorter durations has helped the fund, relatively speaking. Today, the fund offers a fully covered double-digit distribution yield that seems quite safe, given that the fund has seen an increase in net investment income in its last report.

At the same time, the fund trades at a double-digit discount, which also makes it a tempting offering at this time. It's been quite some time since we've covered this fund, having to go back to early 2021 . Given these favorable characteristics currently, this fund is worth a revisit for yield-hungry investors. In particular, yield-hungry investors want a rate that's well above the current risk-free rate to compensate investors willing to take the added risk.

The Basics

- 1-Year Z-score: -0.93

- Discount: -12.18%

- Distribution Yield:10.04%

- Expense Ratio: 3.51% (total expense ratio including leverage expenses)

- Leverage: 25.03%

- Managed Assets: $409 million

- Structure: Perpetual

BGH's investment objective is "to generate as high a level of current income as we determine is consistent with capital preservation, and seeks capital appreciation as a secondary objective."

In an attempt to achieve this objective, the fund will "invest at least 80 percent of its managed assets in corporate bonds, loans and other income-producing instruments that are rated below investment grade." They additionally note that the fund may "invest up to 50 percent of its managed assets in bonds and loans issued by foreign companies."

On the front of its "short duration" focus, the fund will "seek to maintain a weighted average portfolio duration of three years or less." The last available data shows that their duration came in at 2.48 years, a bit below their target but not a bad idea during this current rate environment.

The fund also employs leverage, but they aren't necessarily the most aggressively leveraged compared to other fixed-income peers. Still, that has pushed their latest total expense ratio up to 3.51% from last year's 2.60% total expense ratio. The fund pays at a rate of SOFR plus 0.76% on their borrowings.

Performance - Tempting Discount

Since our last coverage of the fund, it would appear that the fund has done poorly - at least if we are trying to compare it to the S&P 500 Index that's been flat during this time. Flat is better than a total return that's declined by -5.5%.

BGH Performance Since Prior Update (Seeking Alpha)

That said, if we compare the fund to more appropriate measurements, such as other fixed-income investments, then we'll see a different picture.

During this time, BGH, on a total NAV return basis, has been essentially flat. That's compared to the iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ), down around 6% at this time, and the ugly performance of iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ). LQD shows the real horrors that higher rates have had on the fixed-income market.

YCharts

This would be where BGH's focus on shorter duration has helped keep the fund's performance relatively better than these passively managed ETF peers. This is even considering that BGH utilizes a bit of leverage, which would have had an amplified negative effect on the fund during this down period.

Even the fund's total share price returns beat out its peers due to this better underlying portfolio performance. At the same time, since it was lower during this time, we know that the fund's discount has expanded. Today, the fund's deep discount represents a tempting valuation. Closed-end funds across the board have experienced significant discount widening.

We aren't at Covid sheer panic levels of discounts, but we are near lows of the last decade on 'normal' discount widening periods. That's what makes BGH particularly attractive at this time to consider, as this could add some additional upside potential.

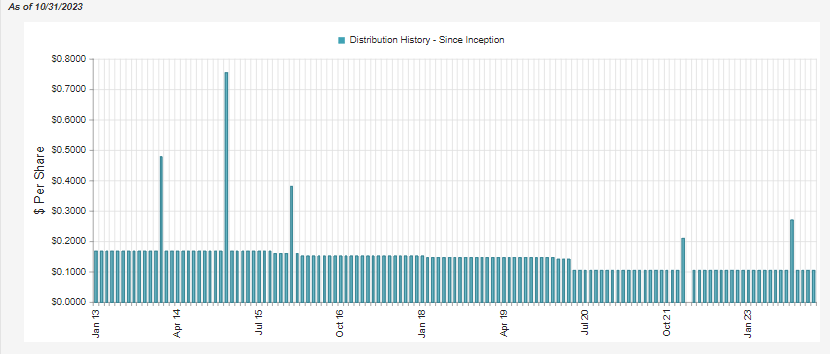

Distribution - Tempting Double-Digit Fully Covered Payout

For me, the fund's valuation is a higher driver of making a fund more tempting, as well as what the fund is holding. However, the fund's distribution here is certainly something that should make some income-oriented investors excited.

They currently pay a 10.04% distribution rate on a share price basis. This rate is juiced thanks to the fund's meaningful discount. On the NAV rate, the fund has to earn closer to 8.8% to continue the current payout (spoiler alert: they are earning it.)

{kind=link}

The fund's payout has been fairly consistent with the environment it was working in - and that was lower yields over time as we were in a zero-rate environment that caused several cuts in their distribution.

Today, the fund's distribution seems pretty solid where it is now, and that is thanks to once again its short-duration focus. With exposure to floating rate securities and those with short maturities, they can participate in higher yields much quicker than something like investment-grade debt, which is exactly why we saw BGH blow LQD's performance away in the last couple of years.

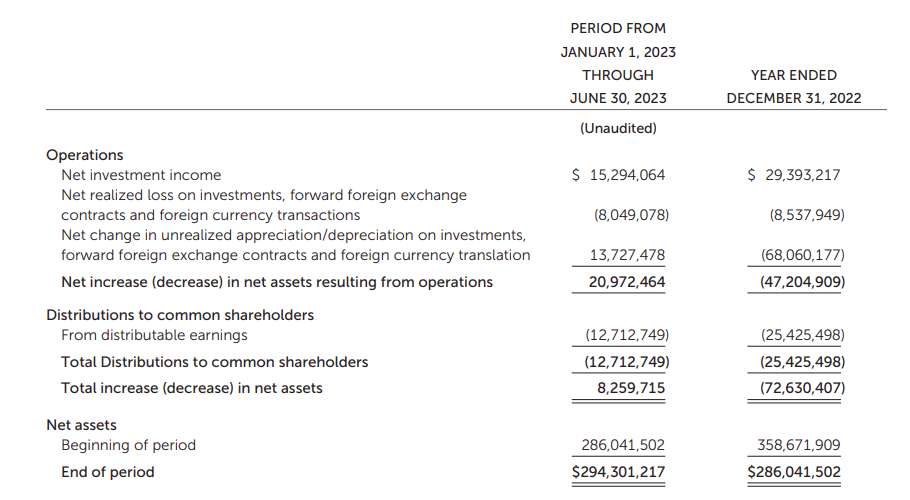

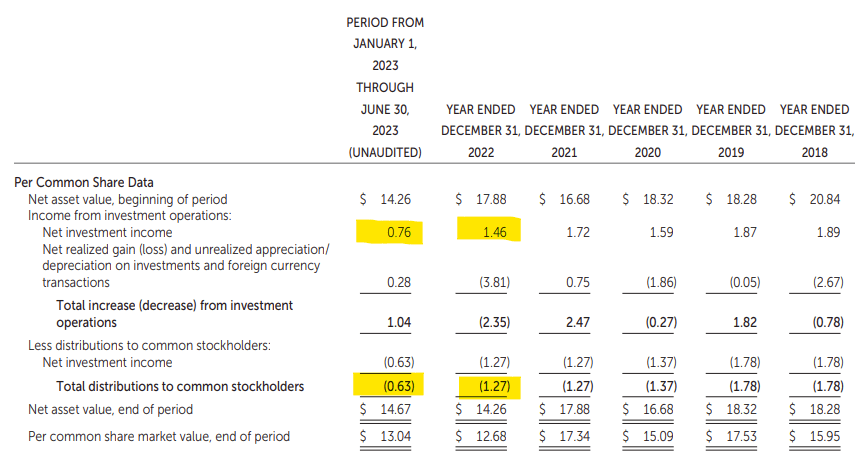

The distribution was last covered entirely through net investment income generated on the portfolio. The higher expense ratio has been offset by the fund's floating rate exposure in its portfolio and higher yields that have driven NII higher.

{kind=link}

NII on a per-share basis is on pace to run higher than last year. Last year, they earned $1.46 for NII. In the first half of this year, the fund earned $0.76, and that would put it on pace for a $1.52 NII per share. This helped drive why there was a special that it paid out earlier this year of $0.166. At the current pace,

{kind=link}

At the current rate, there could be further specials or an increase in the payout. Either or both of these actions wouldn't be too surprising as long as the bottom of the economy doesn't fall out.

For tax purposes, the prior two years saw the fund's entire distribution classified as ordinary income. This would be anticipated to be the case going forward as a fixed-income-focused fund that is covering its distribution through income. That would make the fund more appropriate for a tax-sheltered account.

BGH's Portfolio

BGH takes a diversified approach to building a high-yield income portfolio. They invest through both loans and bonds, as well as investing in collateralized loan obligations. The loans and CLO exposure are where the fund gets its floating rate exposure, and that helps keep the fund's duration lower. The "other" is primarily the CLO exposure.

BGH Portfolio Composition ( Barings )

Given this exposure, the fund's credit quality in its portfolio is on the lower end. This is where the higher the risk to offer, the higher yield comes in. Baa is investment grade, and below that is all speculative grade or "junk."

BGH Portfolio Credit Quality (Barings)

The Caa and below is a fairly shockingly high allocation in this fund that does make it junkier compared to peers. This is the area where companies are at the most risk for defaults and bankruptcy.

The first fund that comes to mind that is invested as junky as this portfolio would be KKR Income Opportunities Fund ( KIO ). They are also invested quite similarly in terms of their asset allocation, so it makes them a pretty solid peer. That said, KIO is even junkier , with nearly 35% of their portfolio being invested in the equivalent of Caa or lower. The "not rated" portion for KIO is also high at 14%.

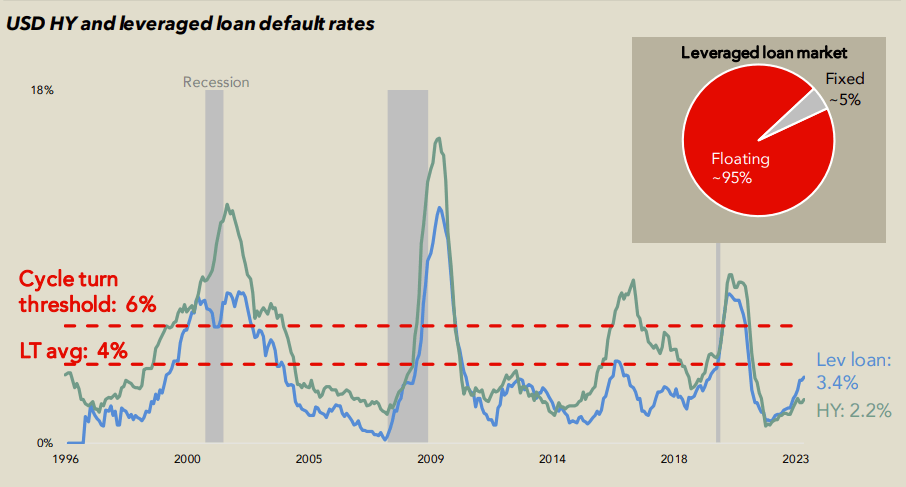

With the expectation for the economy to cool going forward, watching default rates is going to be a key focus. This is especially true when we get into these sorts of funds that invest not only in non-investment-grade bonds but some of the lowest rungs of the non-investment-grade pool.

Defaults were relatively low for the last couple of years, but that has been trending higher . This is precisely what the Fed wants to see because that means the economy will slow down, and the hope is that it will also bring down inflation. For leveraged loans, the default rates have outpaced bonds now as yields on these instruments start to get stretched higher. That's the ugly side of the floating rate exposure.

{kind=link}

On the other hand, being higher in the capital stack has historically meant a higher recovery rate for loans relative to high-yield bonds. The recovery for loans is at about 60%, while high-yield bonds state that the recovery has been around 40%.

So, by investing in BGH and other high-yield-focused funds, we are taking a bet on the manager to be able to navigate through this period successfully and limit losses. It isn't that they'll avoid all defaults, but if they can have more winners than losers. Spreading their portfolio across hundreds of positions is generally what a high-yield fund will do.

However, BGH takes a fairly narrow focus with 181 issuers. With CLO exposure, these are pooled investments that can have their own hundreds or thousands of packaged loans within them. That can help offset further risks, but it is a relatively smaller sleeve of their portfolio.

Additionally, some of the credit risk is already priced in with not only BGH's discount, but the weighted average market price of BGH's holdings is also discounted at $83.87.

Conclusion

BGH is sporting a deep discount with an attractive double-digit yield that's being fully covered. It was being covered enough that the fund paid a special earlier in the year, and we could see more or a higher regular distribution in the future. That is with the assumption that the economy doesn't slump too hard heading into next year. If that happens, then just maintaining the distribution rate at the current level would be ideal.

The portfolio runs on the junkier side with a higher allocation to the most speculative rungs of the credit quality scale, which makes them more economically sensitive. This is somewhat offset by the fund's diversified exposure and with its underlying portfolio already being discounted to reflect the heightened credit risk. Though the fund's utilization of leverage will amplify any downside moves (as well as upside moves.)

For further details see:

BGH: Double-Digit ~10% Yield With A Double-Digit Discount