NRGX - BGR And PEO: Big Oil Investments At Large Discounts

Summary

- PEO and BGR are the second and third-best performing funds on a total NAV return basis through the end of November.

- On a total share price return basis through the end of November, they've still done well, as the third and fourth best performing, respectively.

- Both of these, perhaps unsurprisingly, are funds heavily invested in energy.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on December 10th, 2022.

We are coming closer to the end of the year, and a trend that began last year has carried on through 2022. That was the energy sector being the strongest performing. This was after it was the worst performing in five of the seven years between 2014 and 2020. In 2021 it came back with a vengeance, and this year it is one of the only sectors that has stayed positive. At the time of writing, it looks like consumer staples have slipped back into negative territory slightly for the year. Utilities are also only slightly negative on a YTD basis.

{kind=link}

Although the energy sector had gone through its own bear market earlier in 2022, it was hard to notice as it had stayed positive the whole time through. More recently, things have been trending down again as the outlook for 2023 continues to remain uncertain. The only certainty we seem to be getting is that there is going to be a recession; the depth and duration are unknown.

YCharts

That being said, I believe there are a few things that can help benefit the sector in the short term. I've outlined them previously and will reiterate them once again here.

While I would be hesitant to invest in more energy too aggressively, considering the expectations for a recession next year, I believe the sector has a couple of things going for it. First, China shouldn't stay in lockdowns from COVID forever. If and when they open, demand for oil/natural gas and whatever other fossil fuels are used for energy could increase.

Secondly, OPEC seems more committed to helping support the current price after announcing production cuts several months ago. This was because they anticipated weak demand coming from weaker economies after central banks began raising interest rates aggressively. I believe this was a change in stance from back in 2015 when OPEC was more than content to keep pumping to drive out U.S. producers.

Thirdly, oil companies in the U.S. don't seem interested in investing heavily in bringing up production. Instead, they are providing more returns to shareholders and staying highly profitable. Rig counts have been growing but at a relatively slower pace.

YCharts

I'm not sure I blame them either since regulations , and the message out of the White House from the current administration has been quite negative on the fossil fuel industry. Why would they invest significant capital into an area of the market that is being ostracized?

I'm all for renewables, but I know this will be a transition of decades (centuries, maybe) and not years. There will also presumably always be a need for fossil fuels in some capacity, too. So the brown industry will never truly go away. One of the main reasons is that making equipment for renewable energy, such as wind and solar, requires oil .

That's what I shared at the end of November when looking at PIMCO Energy & Tactical Credit Opportunities ( NRGX ). Just in that short bit of time, we already know that China has loosened some of its lockdown policies . We also have OPEC confirming they are keeping production unchanged.

Exxon Mobil ( XOM ) has also announced that for the next five years, they are planning to keep CAPEX between $20 to $25 billion. However, they will be focusing on "a sizeable increase in investments aimed at emission reductions and accretive lower-emission initiatives, including its Low Carbon Solutions business."

That brings me to two funds I wanted to take a look at this year that have been performing exceptionally well. Of course, the overall sector of energy performing well is playing a key role in propelling energy-focused closed-end funds. Data below collected from CEFConnect showing returns through the end of November 2022

| Name |

| Ticker |

| Manager |

| Total NAV Return |

| Total Share Price Return |

| Tortoise Energy Independence Fund |

| [[NDP]] |

| Tortoise Capital Advisors, LLC |

| 57.90% |

| 56.66% |

| Adams Natural Resources Fund |

| [[PEO]] |

| Adams Natural Resources Fund Inc |

| 48.29% |

| 47.53% |

| BlackRock Energy and Resources Trust |

| [[BGR]] |

| BlackRock |

| 41.81% |

| 45.09% |

| ClearBridge MLP and Midstream Fund |

| [[CEM]] |

| ClearBridge |

| 39.62% |

| 42.37% |

| NB MLP Income Fund Inc. |

| [[NML]] |

| Neuberger Berman |

| 38.16% |

| 42.53% |

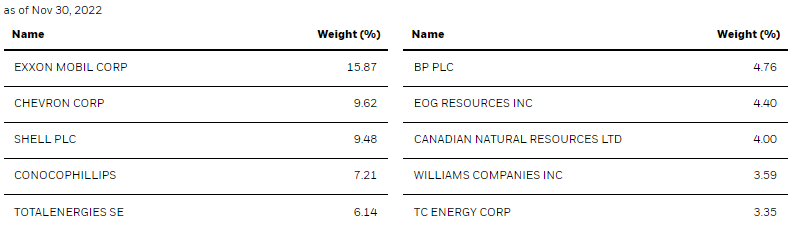

All five of these funds could benefit going forward from what I outlined above. However, I wanted to take a particular look at PEO and BGR. I believe these are interesting funds because they are tilted heavier toward the major oil players. With Exxon Mobil, Chevron ( CVX ) and ConocoPhillips ( COP ) are major weightings in each of these funds.

I think sticking towards the higher-end quality and more financially stable companies in the energy space could be a safer bet. They should be able to withstand a recession better, just as they've proven historically. PEO and BGR, while they have similarities in their holdings, have slightly different strategies that they execute, which can make them complement each other. That's why an investor could consider both.

Adams Natural Resources Fund

- 1-Year Z-score: -1.75

- Discount: -15.84%

- Distribution Yield: 1.83% (regular distribution only)

- Expense Ratio: 0.58%

- Leverage: N/A

- Managed Assets: $552.7 million

- Structure: Perpetual

PEO " seeks to deliver superior returns over time by capitalizing on the long-term demand for energy and materials. The Fund invests in energy and natural resources stocks and seeks to generate returns that exceed its benchmark as well as consistently distribute dividend income and capital gains to shareholders."

Similar to the other Adams fund, Adams Diversified Equity Fund ( ADX ), PEO has an incredibly long history. The inception date goes back to 1929. PEO also went through a name change when ADX had. Formerly, the fund was known as the Petroleum & Resources Corporation.

Another similarity with ADX is that the fund doesn't utilize any leverage. That can be a positive, especially when your underlying investments are volatile enough.

The fund's expense ratio is incredibly low for the closed-end fund space - another characteristic that is present in ADX. However, it's still on the higher end if it was competing against an ETF. In 2021, the average expense ratio for an ETF was 0.49%.

The fund's discount has widened out more recently despite the strong performance the fund has provided this year. However, it has consistently traded at a deep discount.

YCharts

I believe that now investors have collected the big year-end special, they've sold the fund off. The fund pays a minimum distribution of 6% annually. In strong years such as 2022, it can be significantly larger. Combining with the regular, they paid out an 8.1% distribution yield through 2021. Going back to the long history of this fund, that made for the 71st consecutive year-end capital gains distribution and 88 consecutive years of paying out distribution to investors.

The ex-dividend date for the fund was November 18th. Since then, the discount has widened once again. Most investors don't find this type of distribution policy too attractive. I believe that's why the large discount might be present in PEO.

{kind=link}

Then again, the entire closed-end fund energy sector continues to remain at some significant discounts. Investors being bitten by leverage and significant losses in 2020 are likely drivers of this. For PEO, they aren't leveraged. This was to their benefit as both the price and NAV have eclipsed pre-COVID levels.

YCharts

As mentioned above, PEO is an interesting energy play for investors wanting more exposure to this sector due to their financially stable positions. These are the oil majors that have basically handled anything thrown at them for decades. They will continue to be companies that are required for decades to come. I believe that makes it essentially a set-and-forget type of holding, if you want it to be.

On the downside, it could be easy just to consider investing in the oil majors on one's own rather than buying a fund that's pretty heavily weighted towards the top holdings. That's likely another reason why a large discount exists in this fund.

PEO Top Ten (Adams Funds)

That's where BGR might come in handy for some investors, as they also implement an option writing strategy in the mix. That's an area where not all investors are comfortable doing themselves.

BlackRock Energy and Resources Fund

- 1-Year Z-score: -2.18

- Discount: -14.35%

- Distribution Yield: 5.94%

- Expense Ratio: 1.33%

- Leverage: N/A

- Managed Assets: $382 million

- Structure: Perpetual

BGR's investment objective is "to provide total return through a combination of current income, current gains and long-term capital appreciation." To achieve this, they will "under normal market conditions, invest at least 80% of its total assets in equity securities of energy and natural resources companies and equity derivatives with exposure to the energy and natural resources industry. The Trust may invest directly in such securities or synthetically through the use of derivatives. The Trust utilizes an option writing (selling) strategy to enhance dividend yield."

The fund's expense ratio is significantly higher than PEO's, but it is more in line with other CEFs. Similar to PEO, the fund also doesn't employ any leverage. However, BGR takes its strategy a step further and writes covered calls on the underlying positions in its portfolio. The overwritten portion was last at 37.74%.

This can be beneficial and a hindrance. Despite the significant overlap in the portfolios between the funds, we see that PEO has won out in terms of total NAV return performance. One of the reasons for this is that when prices are rapidly rising, the upside can be capped with covered call funds if the position is called away. They can close or roll the option out if they don't want the position to be called away. Closing would likely result in a loss for the fund. That's exactly what we've seen as well. They realized nearly $23 million in losses from the options they wrote in the first half of 2022.

{kind=link}

In looking at some of the other BlackRock peers, we can see that those funds had benefited from the options written in the portfolio. This was because, with general equities falling, they didn't have to close their positions. They simply collected the premium, and the options expired worthless.

At the same time, the appreciation in BGR's portfolio, both realized and unrealized, was way more than sufficient to offset these losses generated. BGR still put up quite respectable results, and if energy were ever to move flattish, BGR could be the bigger beneficiary. However, flat and energy markets don't seem to ever come up in the same sentence.

This characteristic of the fund is likely at least one reason why BGR isn't making new five-year highs in price and NAV like PEO is. While they are close to or above COVID levels that were touched at the beginning of 2020, the current price and NAV were still higher back in 2018.

YCharts

That could make BGR the more conservative play with its slightly defensive options strategy. I would also note that it still outperforms other CEFs that are focused on the energy space and are leveraged. These leveraged funds should be killing it if all else were equal. But of course, we know that isn't true. It isn't equal.

BGR has chosen to focus primarily on the energy majors. They've also put a fair weighting on the exploration and production industry or E&P. E&P will naturally correlate with the overall energy prices because they can directly benefit from higher prices. The downside is that they can also be more volatile as they feel the downside.

{kind=link}

Why this benefits BGR as being a relatively better performer this year is because other energy-related CEFs tend to invest in midstreams or MLPs. These often tend to be more stable regarding cash flows since significant portions of these operations are tied to fixed-fee contracts. That means they don't benefit the same way when times are good. In theory, they shouldn't feel it when times are bad, either. In practice, though, we often see them fall in sympathy anyway.

Here's a look at the Energy Select Sector SPDR ( XLE ) compared to the ALPS Alerian MLP ETF ( AMLP ). This is a look at the last ten years. I've included both price and total return metrics because a significant portion of MLP returns is via distributions. As we can see, XLE, which represents the larger energy players and several E&P positions, has easily topped the results of AMLP.

YCharts

Of course, both of these categories can play to different types of investors. Someone in larger energy companies is probably looking for total returns. Those looking for income will gravitate towards midstreams and MLPs every time.

At this time, BGR is also showing a wider-than-usual discount. Despite the strong performance of this sector in the last two years, it would seem that they are the first to start selling off with the potential headwinds next year. For BGR, we are looking at discount that's near the widest in the last decade. Only during COVID did the discount widen out even further.

YCharts

Conclusion

BGR and PEO are two closed-end funds offering a similar focus of investing heavily in the oil majors. At the same time, BGR having an options strategy tilt makes the end result a bit different. Of course, positioning and a higher expense ratio are also likely to play a role.

Both of these funds are offering some attractive discounts at this time too. The main reason it seems like discounts could be widening is due to the potential headwinds of 2023. It seems almost certain that we will see a recession, but the question is how deep and how long. Sticking with the larger, more financially stable companies in the energy space appears to be a fairly reasonable strategy with that outlook. That is if you want to stay invested in the energy space overall.

For further details see:

BGR And PEO: Big Oil Investments At Large Discounts