XLE - BGR: Volatile Energy Equities Does Not Translate Well To Call-Write Strategies

2023-08-10 00:58:29 ET

Summary

- The BlackRock Energy and Resources Trust is a closed-end fund that focuses on investing in energy and natural resource companies.

- The fund aims to provide total returns through current income and capital gains. It employs a call-writing strategy to generate premium income to enhance its distribution.

- The boom/bust nature of energy equities does not translate well to call-writing strategies, leading to long-term underperformance.

Normally, we see call-write strategies applied to broad market indices like the S&P 500 Index or the Nasdaq 100 Index. However, the BlackRock Energy and Resources Trust applies a call-writing overlay to a portfolio of energy equities to generate high current income.

Overall, I am not a fan of applying call-writing overlays to sector funds like the BGR. The boom/bust nature of energy equities means that monthly returns often exhibit large tails. Furthermore, during a long rally, like we have experienced since the COVID lows, a call-write strategy may give a false impression of being able to sustain high distribution yields. However, once we analyze the strategy through a cycle, we realize giving up positive tails during bull markets translate into disappointing long-term total returns.

For those currently invested in the BGR fund, I would be mindful of the dynamic described above and not hold it forever.

Fund Overview

The BlackRock Energy and Resources Trust ( BGR ) is a closed-end fund ("CEF") that aims to provide total returns through current income and capital gains by investing in stocks of energy and natural resource companies. The BGR fund also uses a call-writing overlay to generate premium income to enhance distributions to unitholders.

The BGR fund has $396 million in net assets and charge a 1.26% gross expense ratio.

Portfolio Holdings

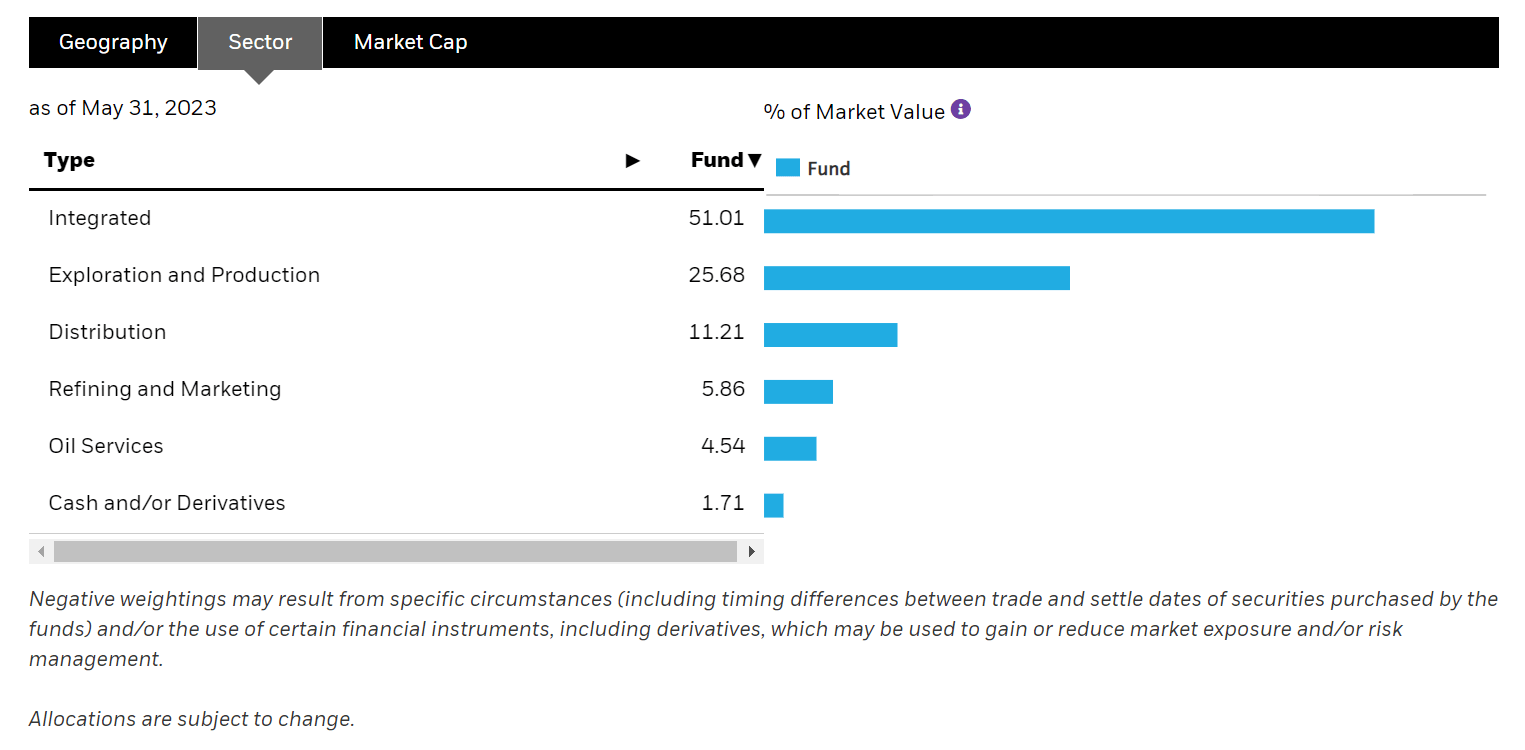

Figure 1 shows the sector allocation of the BGR fund as of May 31, 2023. The fund is primarily invested in energy equities, with 51.0% of the portfolio invested in integrated oil & gas companies, 25.7% invested in exploration & production companies ("E&Ps"), 11.2% invested in distribution companies, and 5.9% invested in refining and marketing.

{kind=link}

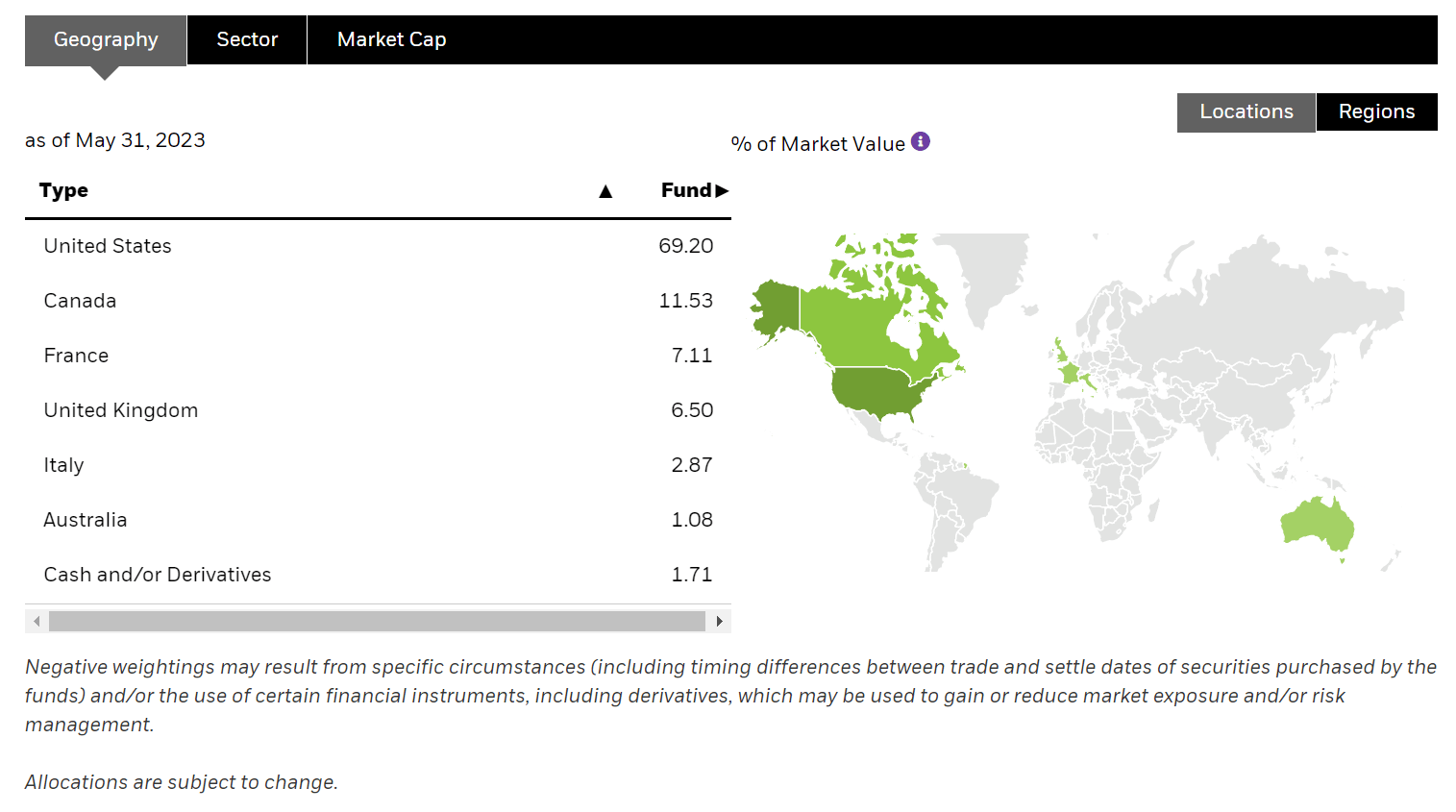

The BGR fund is North America focused with U.S.-domiciled companies accounting for 69.2% of the portfolio and Canada accounting for 11.5% (Figure 2). The fund also owns a handful of securities in Europe and Australia.

{kind=link}

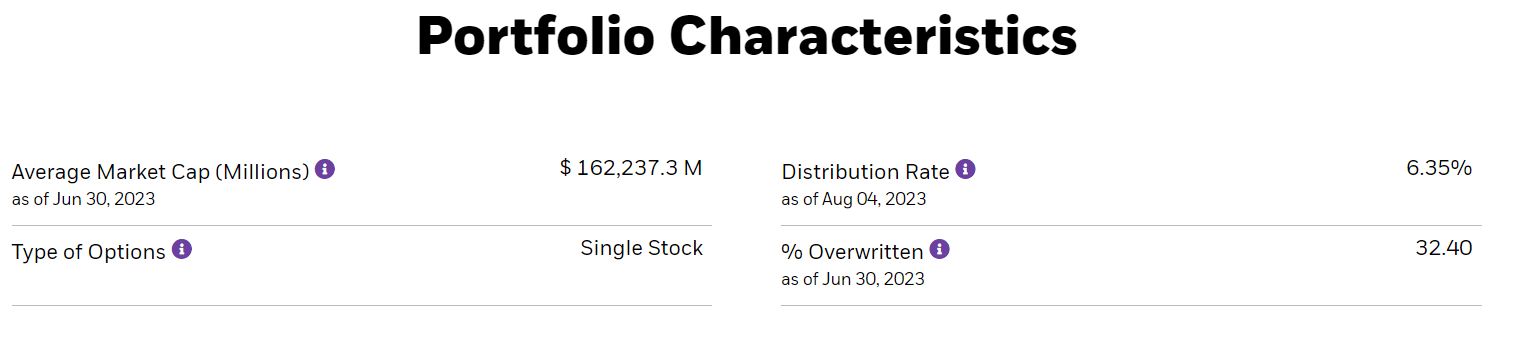

The BGR fund has written single stock call options on approximately 1/3 of the portfolio (Figure 3).

{kind=link}

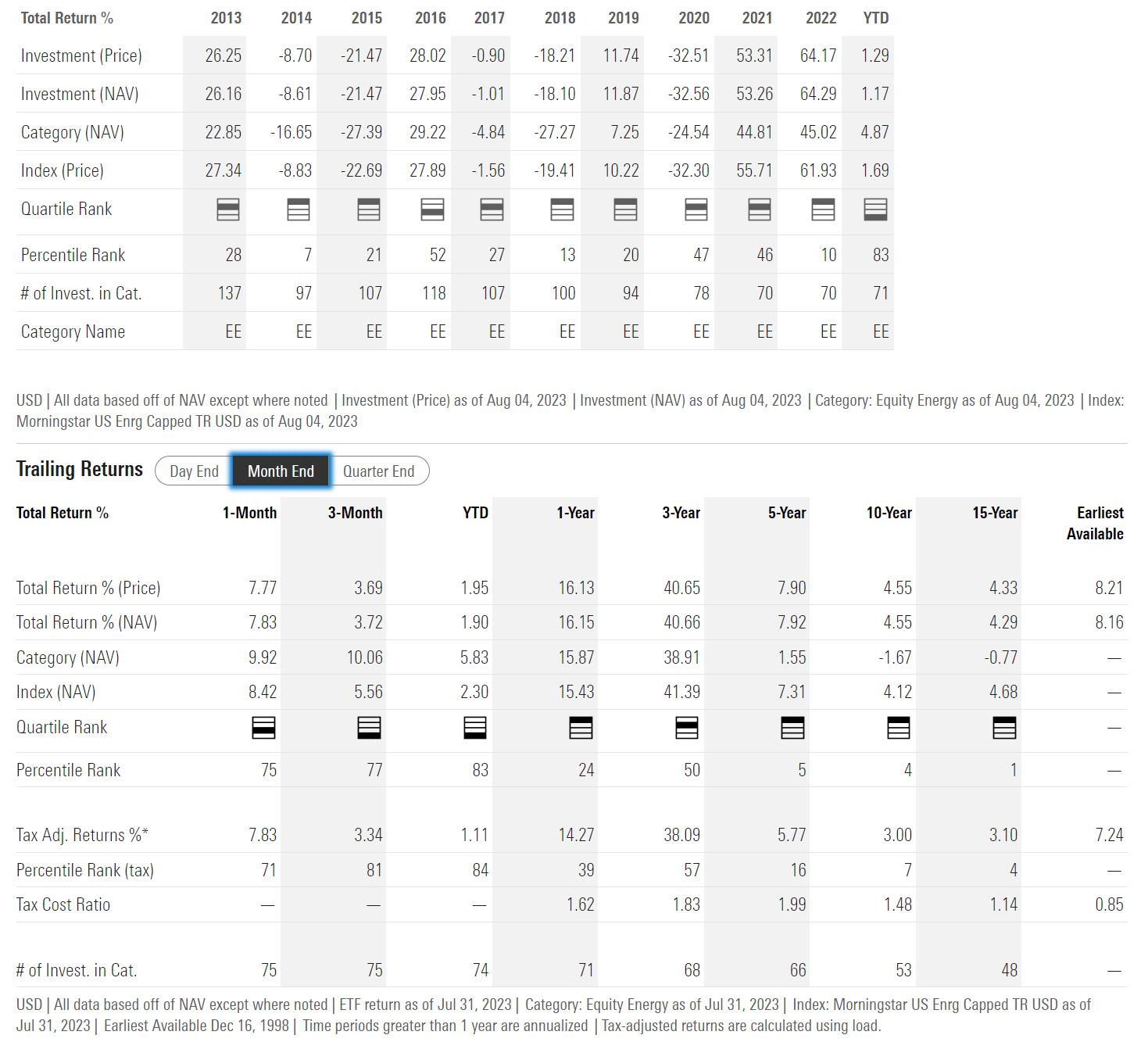

Returns

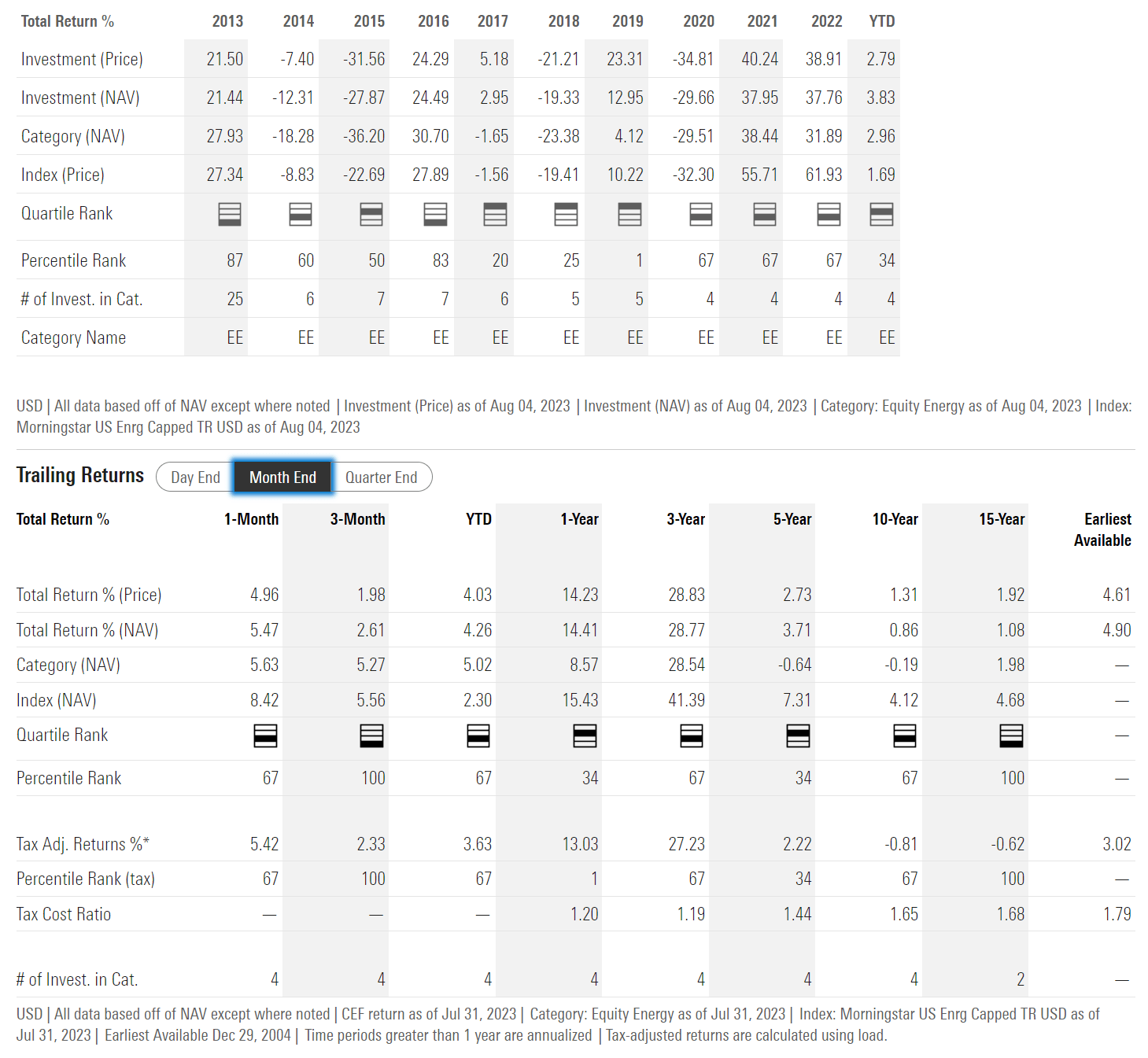

Figure 4 shows the historical returns of the BGR fund. The BGR fund has had very strong returns in 2021 and 2022, returning 38.0% and 37.8% respectively on NAV. However, the fund's long-term track record is much more modest, with 5/10/15Yr average annual returns of 3.7%/0.9%/1.1% respectively to July 31, 2023.

{kind=link}

As with all call-writing strategies, over the long run, the BGR fund has underperformed versus peers that do not write call options. This is because systematically writing call options will trade away upside for premium income, skewing the average monthly returns lower.

For example, Figure 5 shows the historical returns of the Energy Select Sector SPDR ETF ( XLE ) for comparison. The XLE ETF had even stronger 2021 and 2022 returns of 53.3% and 64.3% respectively and it has delivered 5/10/15Yr average annual returns of 7.8%/4.6%/4.3% respectively to July 31, 2023.

{kind=link}

Distribution & Yield

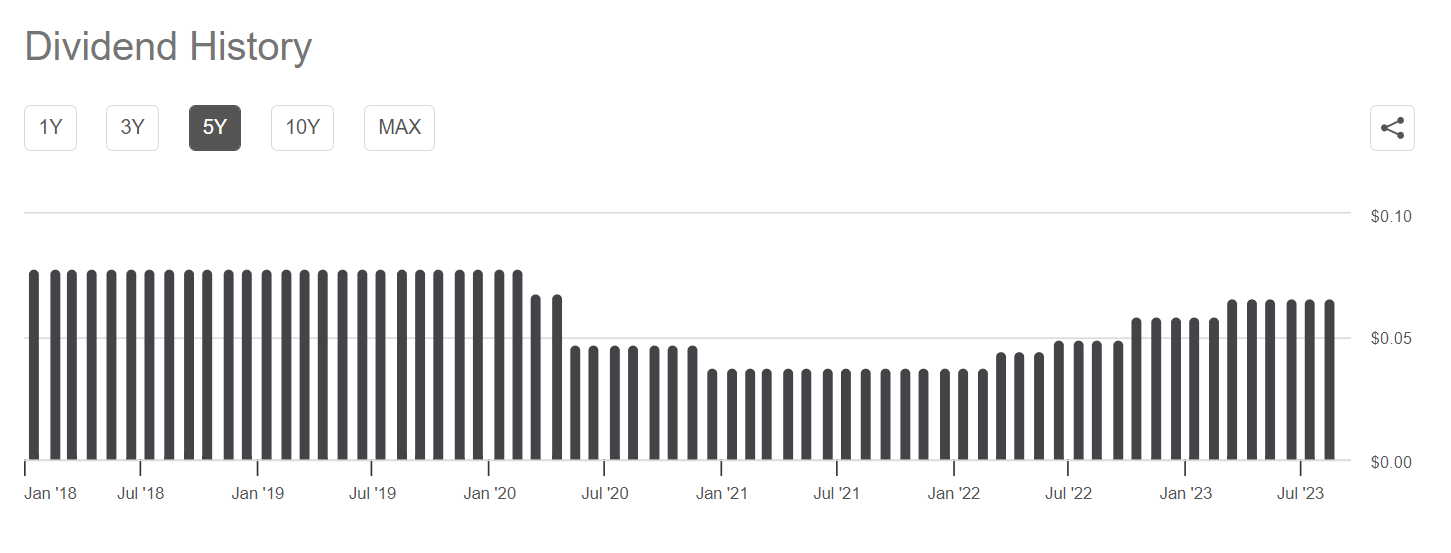

In terms of distribution, the BGR fund is currently paying a $0.0657 / share monthly distribution, which translates into a forward yield of 6.3%. On NAV, the BGR fund is yielding 5.5%.

BGR's monthly distribution has been raised several times in the past few years, from post-COVID lows of $0.0375 / month to $0.044, $0.049, and $0.0585 in 2022, and recently to $0.0657 / month (Figure 6).

Figure 6 - BGR distribution has been raised in the past few years (Seeking Alpha)

{kind=link}

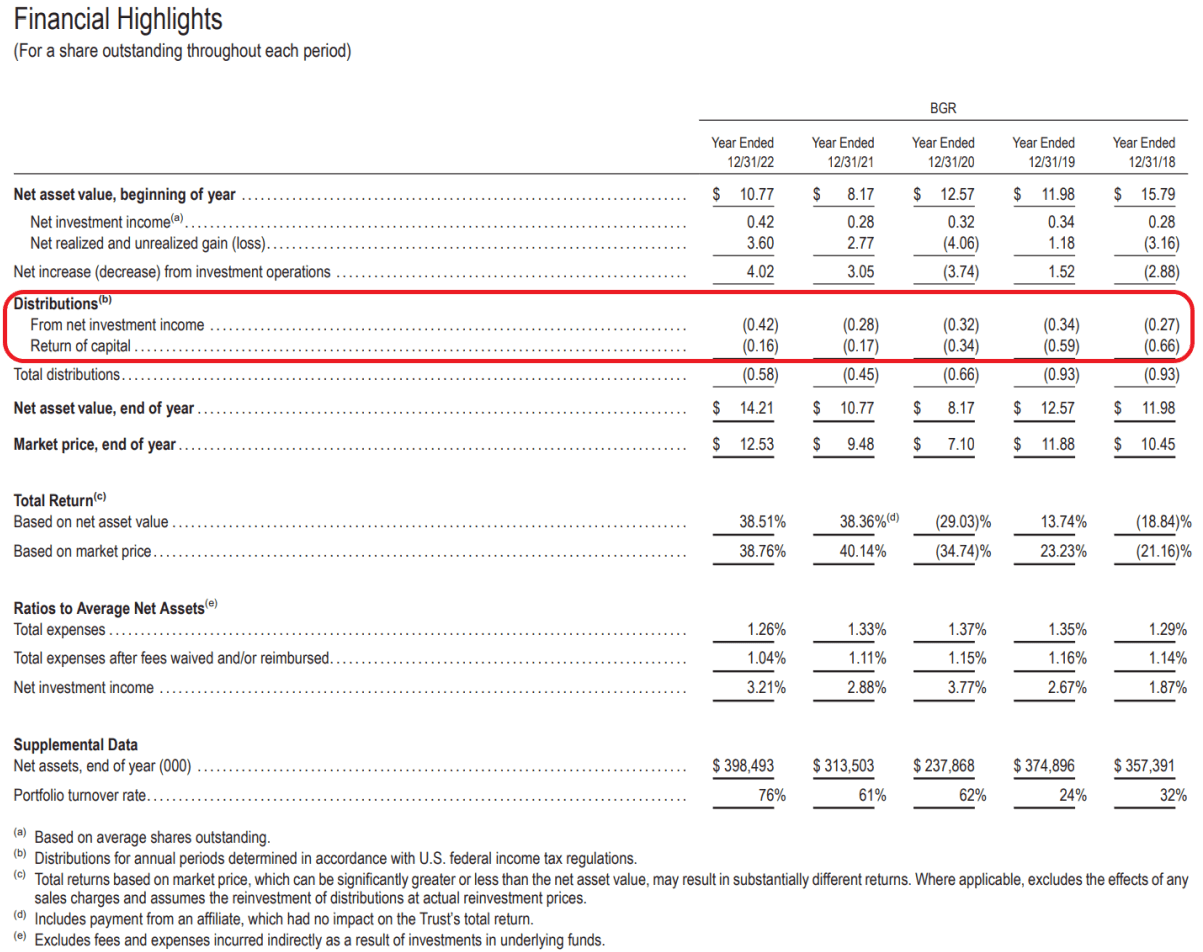

Historically, a portion of BGR's distribution is funded from return of capital ("ROC"), ranging from 71% in fiscal 2018 to 28% in fiscal 2022 (Figure 7).

Figure 7 - BGR has historically funded distribution partly from ROC (BGR annual report)

{kind=link}

Is BGR's Distribution Sustainable?

For me, it is hard to assess whether BGR's distribution is sustainable. On the one hand, in the past few years, the BGR fund has done exceptionally well, with 3 Yr average annual returns of 28.8% (from Figure 4 above), so technically, it is earned more than enough to fund its 5.5% of NAV yield.

However, if we look longer-term, the BGR fund has earned average annual returns of 3.7% over 5 years and ~1% over 10 and 15 years, so the distribution does would appear unsustainable in those time frames.

Volatile Energy Equities Does Not Work Well With Call-Write Strategies

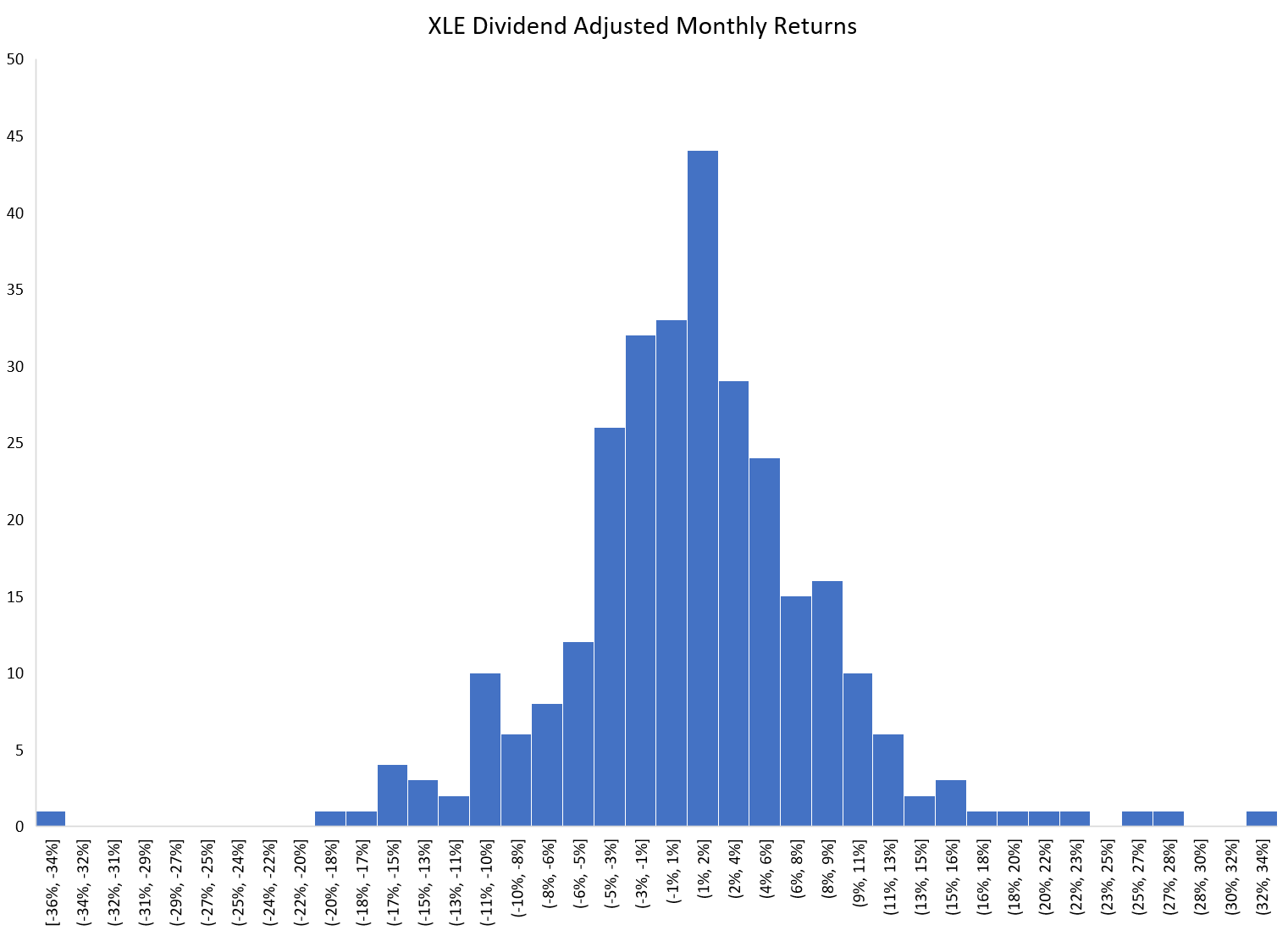

I believe the issue lies in the volatile asset class that is energy equities. The boom/bust nature of energy equities does not lend well to a call-writing strategy, as the monthly return distribution of energy equities, modeled as the dividend adjusted monthly returns of the XLE ETF, exhibit large tails (Figure 8).

Figure 8 - XLE dividend adjusted monthly returns histogram (Author created with data from Yahoo Finance)

{kind=link}

Furthermore, the monthly returns of the XLE ETF show high auto-correlation (95% correlation between monthly returns and 1-month lagged returns), which suggest energy equities tend to go on multi-month 'swings'.

So a systematic strategy of writing calls may appear to be sustainable when energy goes through large multi-year rallies like it has since 2020, but over the long-term through multiple cycles, the strategy underperforms because upside returns are capped during rallies while downside returns are uncapped (Figure 9).

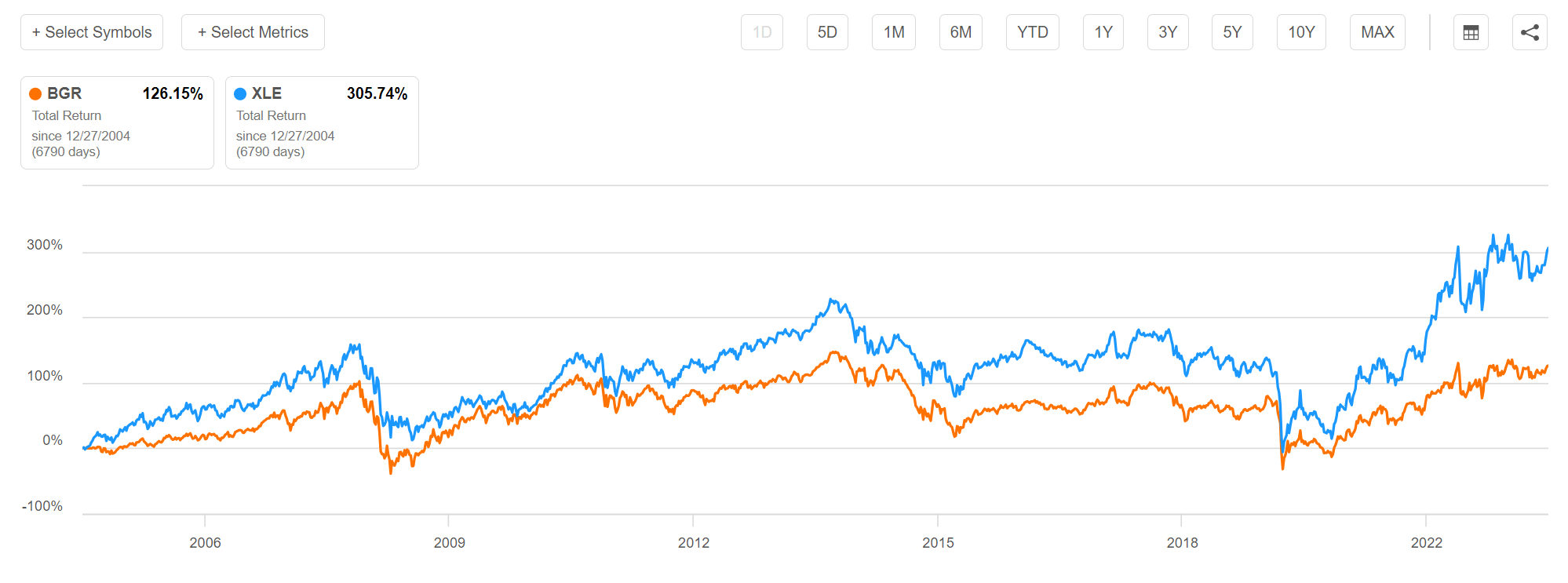

Figure 9 - BGR total return significantly underperforms over the long-term (Seeking Alpha)

{kind=link}

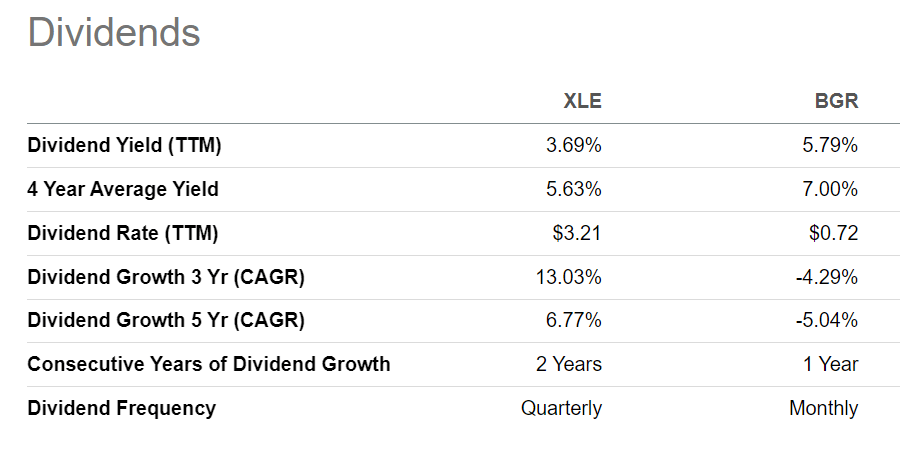

Finally, the BGR fund itself does not pay a substantially higher distribution to justify its long-term underperformance. The XLE ETF pays a trailing 12 month distribution of 3.7% compared to 5.8% for BGR (Figure 10).

{kind=link}

Conclusion

The BlackRock Energy and Resources Trust applies a call-writing overlay to energy equities to generate high current income. Overall, the boom/bust nature of energy equities does not translate well into a call-writing strategy, as upside returns are capped while downside capture is unlimited. What ends up happening is that during bull markets, like the one we are currently experiencing, the BGR fund appears to be a high performing fund that pays an attractive distribution. But through an energy cycle, total returns are actually very poor and the distribution is not 'earned'.

For energy exposure, I would stay away from call-writing strategies like the BGR since one needs to maximize upside in order to earn a decent total return through a cycle.

For further details see:

BGR: Volatile Energy Equities Does Not Translate Well To Call-Write Strategies