BGSF - BGSF Inc.: A Tale Of 2 Scenarios

2023-03-14 18:33:56 ET

Summary

- The company has some potential in rewarding shareholders in the future if efficiency measures are achieved.

- Zero cash position and high levels of debt are a little worrisome in my opinion, but other than that, the books look quite good.

- Two models, one with static margins shows the company is overpriced and one with better margins shows the company has potential.

Investment Thesis

BGSF, Inc. ( BGSF ) just reported its FY2022 results with quite good increases y-o-y. In this article, I will present two different valuations, both will consider a decrease in revenues due to a potential recessionary period and bounce back, however, the main difference between the models will be the management's ability to expand profit margins. In one model, the margins will stay relatively static, in the other, the margins will see a similar improvement that it has obtained in the past but on a more conservative side.

Under the static margins model, the company is overpriced, with no good cashflow generation in sight, lots of debt, and zero cash. On the model with improvements in margins, the company still has a lot of room to grow in the future, if it can achieve better efficiency long-term through improvements in IT and focusing on trimming non-revenue generating segments. At this point, it is quite difficult to tell if the management will improve its balance sheet going forward and if the upcoming recession is going to affect its operations in a meaningful way. Right now, I would suggest patience until there are more answers to the unknowns.

The Company and FY2022 Results

BGSF Inc. is a nationwide leader in strategic workforce solutions, with over 30,000 people placed and 9,000 clients served across the US annually. The company provides temporary staffing services for various industries, such as information technology, professional services, and real estate.

The main points to look at from FY2022 are the increases in revenue y-o-y of almost 25%. Gross profit of 28% of which 26.9% was organic growth, gross profit margins saw an increase of 80bps to 34.7%.

Overall these results are great, and the company is quite small so it is not unexpected that it would grow in double digits for a while. The important thing to ask is if they can sustain this and keep improving their profit margins further as they have done in the past, considering that there might be a recession coming in the next 12-24 months.

The Future Potential and Headwinds

The management is focusing on the implementation of IT systems that would improve the efficiency of the company, which would translate into margin expansions. The company's IT solutions have been scaled up for a company that generates $1B in revenue. They are about a third of the way there so far, with the most recent acquisition of Horn Solutions, which in 2022 was a $30m revenue company, which is around 10% of total revenues that BGSF achieved in FY2022. The management did not give any guidance on how long it would take them to achieve $1B in revenue as that would be quite a speculation, but keeping everything as it is growing right now, the company would need to achieve around 13% average growth per year for the next decade and that is with improving profit margins. That is a bit far-fetched, in my opinion.

The firm is set on improving margins in the future, this will help the bull-case scenario. That way it will be able to generate more FCF which will be beneficial to the shareholders in the long run and should see an increase in their share price.

Quite impressive organic growth seen at the company suggests that acquisitions hardly play a major role in growing revenues, however, that is not to say that M&As hurt the company, I'm just not sure if it is worth it that much to acquire, as opposed to focusing on your existing operations to drive revenue growth. I'd like to see some more numbers in the later quarters to have a better view of these acquisitions synergizing well, which may account for greater revenue growth in the long run.

In terms of headwinds, there is so much uncertainty in the global markets that could affect the company's short-term outlook. The increases in interest rates and what the fed is hoping for - an increase in the unemployment rate - in the future could dampen the demand for its services. The CEO does not see the macroeconomic environment affecting the growth of the company, by saying in the earnings transcript that they are poised for another strong year, citing exactly the strong employment numbers and not addressing the potential downturn in the economy in the upcoming 12-24 months.

I'm not sure I could be very optimistic the same way as she is. In 2019, and 2020, the company experienced -23% and -6% respectively in revenue declines. Now I don't think we would see such numbers again in the next upcoming recession; however, I do believe we will see some declines as demand subsides.

What is promising for the company in the future is the potential of becoming more streamlined and efficient. The company has been improving its margins in the last 5 years with gross margins seeing an 8% increase, while EBIT margins have somewhat declined. If the company can achieve higher margins in the future, the company can become much more desirable to an investor.

Briefly on Financials

I am not a big fan of a company that has no cash on hand. It makes the company less flexible and less secure to keep paying the dividend. Paying dividends by taking on extra debt without any cash to pay back that debt does not sit well with me. They will need to comply with debt covenants and if they are not able to cover interest payments and debt repayments at the same time, the dividend is not very safe in my opinion. The management does not seem to think that's a relevant factor and seems to believe that their debt level is reasonable and will continue to utilize it for future working capital requirements and business acquisitions. To be fair, it has not been a problem in the past as they haven't had any cash on their books for a while now and seem to be doing fine, but that could change if something unexpected happens. I would feel safer if the company had some sort of cushion.

Looking further into the debt, the interest coverage ratio is around 12x, which indicates that the company has sufficient earnings and will not default anytime soon, coupled with a .4 debt-to-equity ratio, the company seems to manage the debt efficiently for now and may see operations continue as usual, without slashing it dividend or completely getting rid of it.

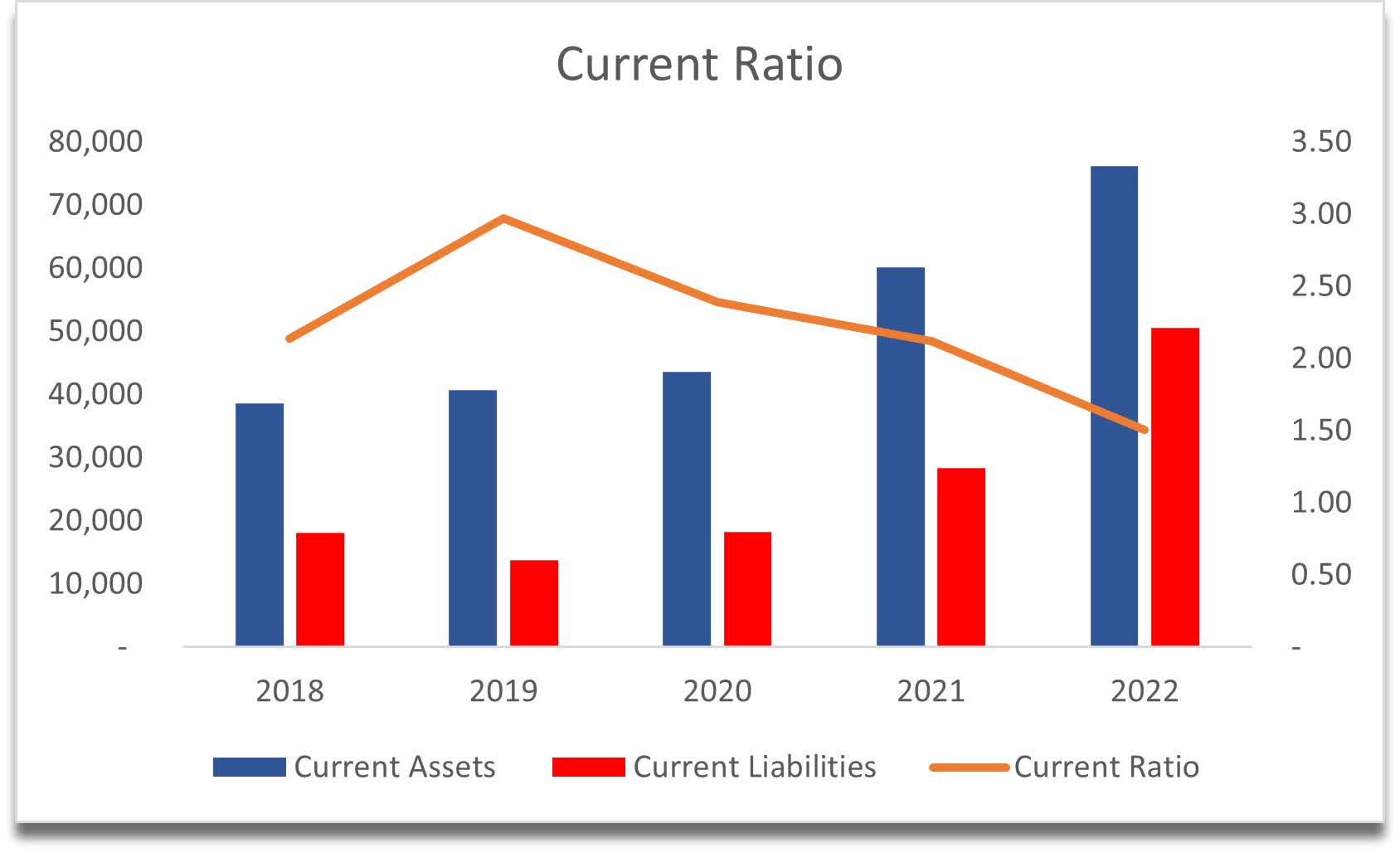

I am also not a fan of a dip in the current ratio in FY2022, which is below 2.0 now. The company has become less efficient in paying off its short-term obligations and if this continues, it could experience some liquidity problems, but if the company manages to chug along as they have in the past and get back over that 2.0 ratio, it will be once again in a healthy position.

{kind=link}

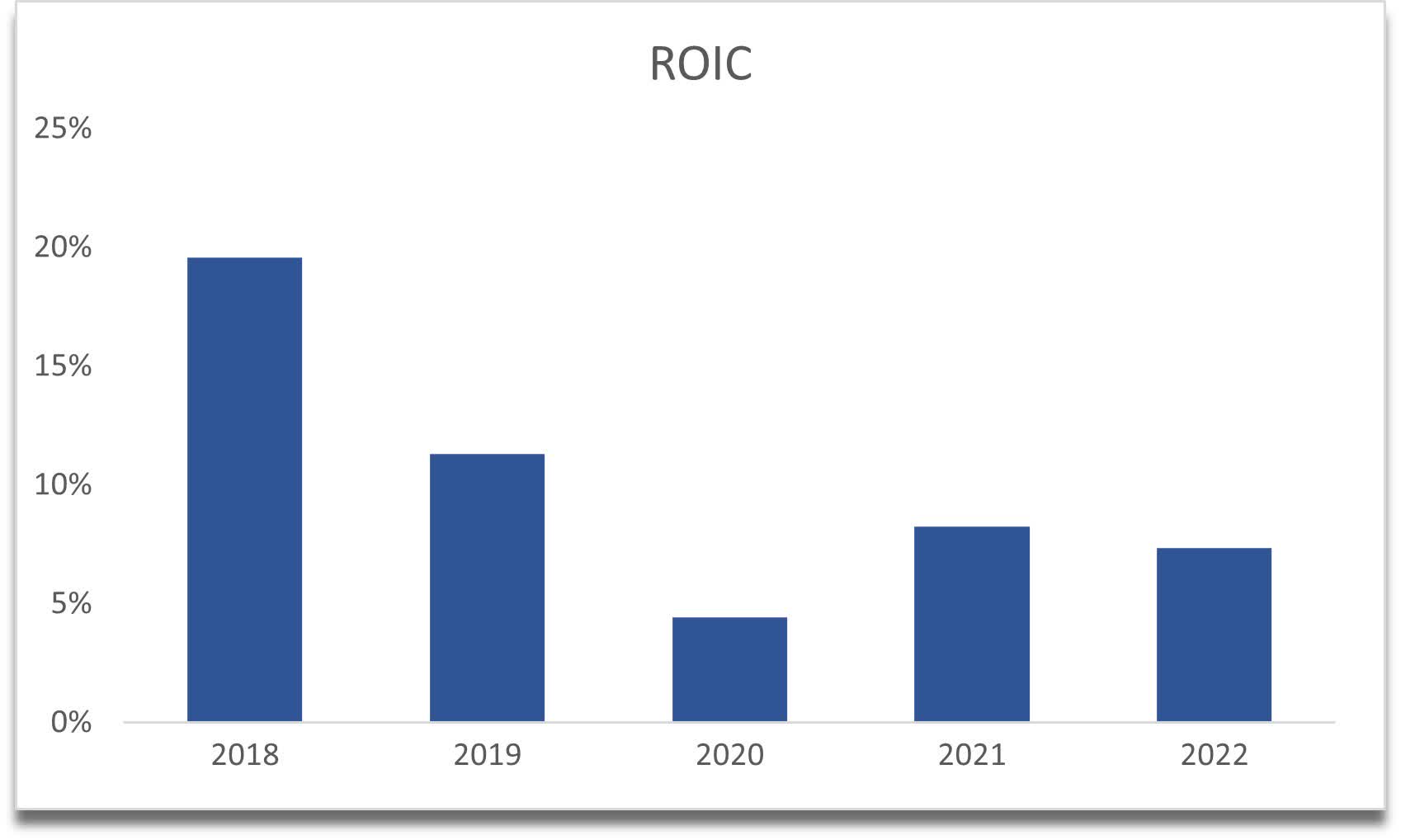

Return on invested capital is acceptable, however, it has seen a slight decline too which may continue in the future if we see a deterioration in the economy, but we won't know until we see more numbers in the upcoming quarters.

{kind=link}

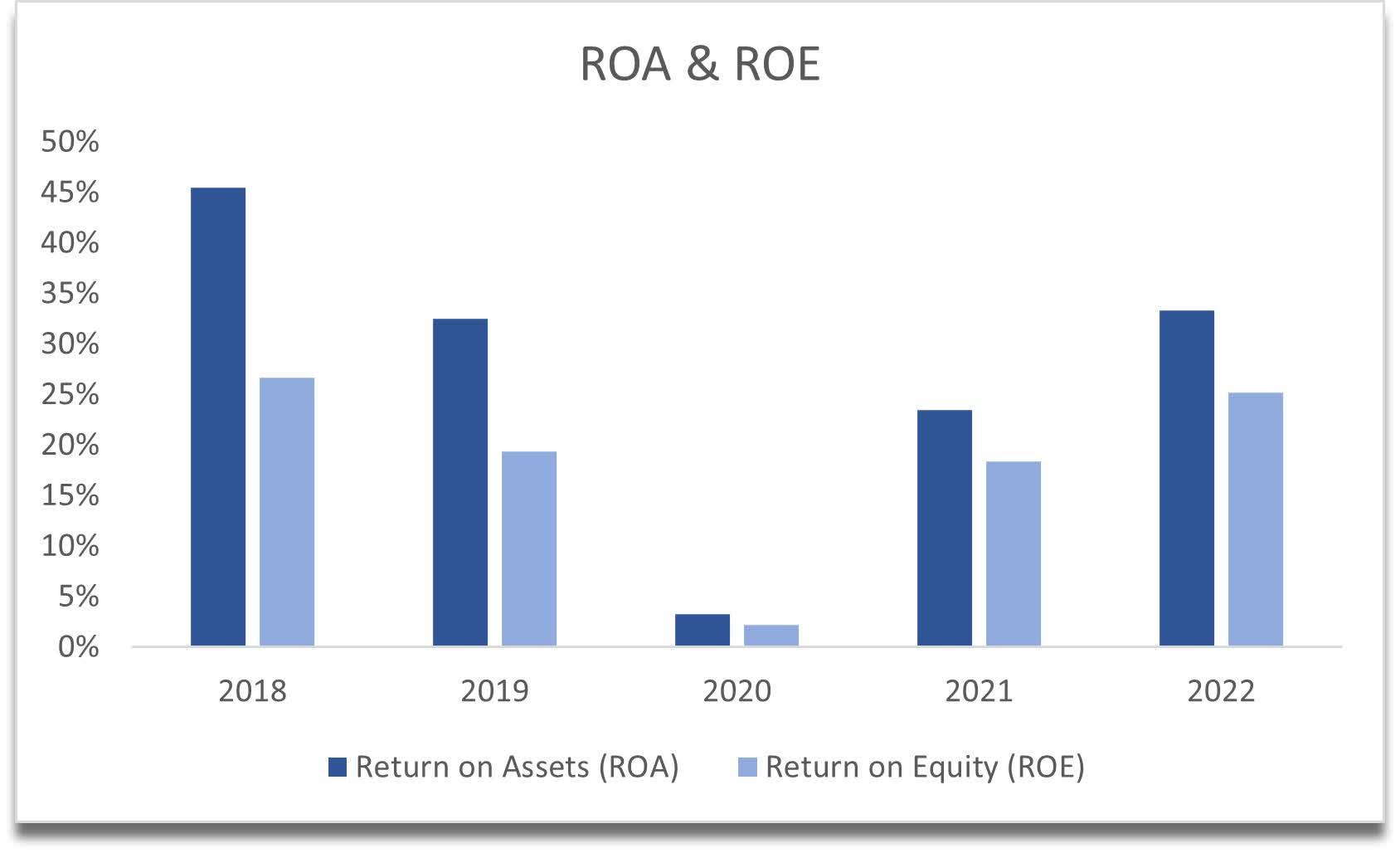

Return on assets and equity are very good here, which tells me that the management is very capable of producing profits and is very efficient. This further tells me that the debt levels may be sustainable if they keep achieving great returns in the future.

{kind=link}

Overall, it seems like the books are managed quite well. The lack of cash and high amounts of debt in my opinion are red flags, but if the company manages to operate even more efficiently in the future, it may not be a problem, but I would be slightly worried for now, because of that uncertainty in the economy.

Valuation

As I mentioned above I will take a look at the company from two different perspectives, both of which will have a recession implemented in the future, which will reduce revenues, but one will have stable margins throughout the model and one will have margin expansion due to the management's ability to make the company more efficient.

For the stable margins model, I have a slight decrease in revenues in '23 of 9%, I figured this would be sufficient as I do not see huge unemployment numbers in the future, especially like the ones we saw during COVID. In '24 the company's revenues are flat y-o-y, then 15% for '25 and '26, and then around 8% for the remainder of the model until 2032. This gives me an average yearly growth of 7%.

I also have a conservative case scenario, where average growth is 5% a year until 2032, and an optimistic scenario with an average growth of 9% per year.

For the improving margins model, I have modeled an improvement of 4% on gross profit margins, EBITDA margins improved by 4.8%, and EBIT margins by 4.4% by 2032. Gross margins might be a little conservative seeing that the company managed an 8% improvement in the last 5 years, EBITDA and EBIT might be a stretch since these two have gone down a little bit in the last 5 years, but the company may achieve these metrics if management's efficiency plans work well.

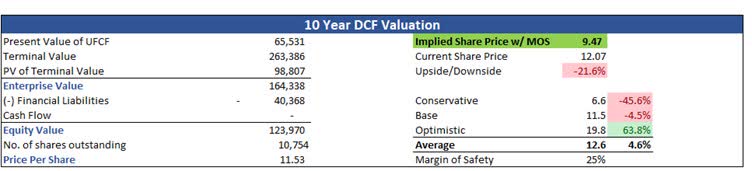

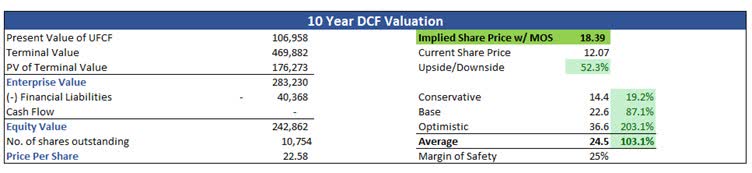

I also like to add a 25% discount to my final intrinsic valuation to have some margin of safety. If the company is not able to achieve further efficiency and just stays on the same margins as they already have, the company is quite overpriced at these levels, as its intrinsic valuation is $9.47 implying a 21.6% downside.

If the company can achieve better margins in the future, the company is a good contender for a long-term hold, as the intrinsic value is $18.39 which implies a 52% upside from the current share price.

{kind=link}

{kind=link}

Conclusion

I see two very different roads that the company may take in the future. It is hard to know which way it is going to take. It will depend on the situation of the economy, on how well the management is handling the balance sheet and the company's liquidity, which as I said I have my worries, but so far they seem to be doing quite well in how it is running. If the company does not manage to improve its margins the company is not worth an investment and would need to figure out how to become an attractive investment for future investors. If the company is able to achieve some sort of margin expansion, it could be a potential investment and if there is no recession or the recession won't negatively affect the company then I could see the share price go up quite a bit in the long run.

I would wait right now for a couple of months to see how well the management is going to perform in implementing the efficiency strategies and what the economy is going to look like in the next 6 months or so, as I am sure there will be more clarity regarding interest rates, inflation, and the unemployment rate.

For further details see:

BGSF, Inc.: A Tale Of 2 Scenarios