BGSF - BGSF's Excessive Expenses Are Trumped By Growth And Durable Competitive Advantages

2023-05-09 08:30:00 ET

Summary

- BGSF’s Real Estate segment secures strong franchise status.

- BGSF Professional segment continues to encroach on the lucrative consulting industry.

- Bloated operating expenses must be rationalized by BGSF management—once they are, sustained macroeconomic tailwinds for these businesses will deliver great profits.

BGSF (BGSF), a microcap staffing company found in the business services sector of our economy, is made up of two very different segments: Real Estate and Professional. Real Estate caters to apartment managers while Professional mainly provides IT consulting and contingent staff to entities broadly throughout the U.S.

In BGSF’s 2017 10-K , the company reported revenues of $273M and pre-tax earnings of $15M.

In BGSF’s 2022 10-K , the company reported revenues of $298M and non-divestiture, pre-tax earnings of $15M.

Within those five years, BGSF’s management acquired “higher margin” businesses and implemented the IT Roadmap—a company-wide technology update intended to improve efficiency.

Why, then, is the company less profitable and inefficient? During that time Mr. Market has pummeled BGSF’s share price (from over $22 in May of ’18 to less than $10 in May of ’23).

Also during that window of time, I released three articles and a blog post pumping up this company, exactly when profitability waned.

How on earth, then, do I now increase my previous intrinsic valuation ( offered here in 2020 ) of the company? In a nutshell, because:

- Real Estate segment has achieved strong franchise status;

- An upstart group of consultants within Professional is now equipped to consistently take market share from more bulky, traditional consulting firms;

- Operating expenses company-wide will be rationalized soon enough; and

- Both of the company’s businesses have substantial tailwinds at their back.

In this article, we will explore these simple explanations and conclude with how I value these two segments. A key part of my valuation is the mysterious Buffett metric of return on unleveraged net tangible assets (ROUNTA). I provide a deep dive of how I apply this metric to BGSF in the appendix.

In order to move quickly, I’m leaning herein on my previous articles and numerous links to Buffett’s own commentary on related items (e.g., durable competitive advantages) in case the reader requires additional context.

To be clear, I’m not making any recommendations in this article, even though I’m more bullish now about BGSF’s long-term future than ever before.

Impressive Top-line Growth, Overwhelmed by Expenses

A key reason for my bullishness is BGSF’s revenue growth. Five years ago, BGSF had three segments: Real Estate, Professional and Light Industrial, the latter of which provided staffing for logistics and warehousing. In early 2022, BGSF sold Light Industrial to jobandtalent , a Spanish digital temporary staffing agency . So, if we take pandemics and divestitures into consideration, top-line growth has been great.

See Figure 1 for yearly changes in revenue since 2017 for Real Estate, the growth and profit star of the show for BGSF. The big swing down in 2020 and subsequent recovery was caused by eviction moratoriums ((EMS)) brought on by the pandemic, discussed below (for greater context on EMs see my blog post here ). Including that most difficult of times, Real Estate’s five-year compound annual growth rate ((CAGR)) is 9.5%—which is 100% organic.

Figure 1

Author

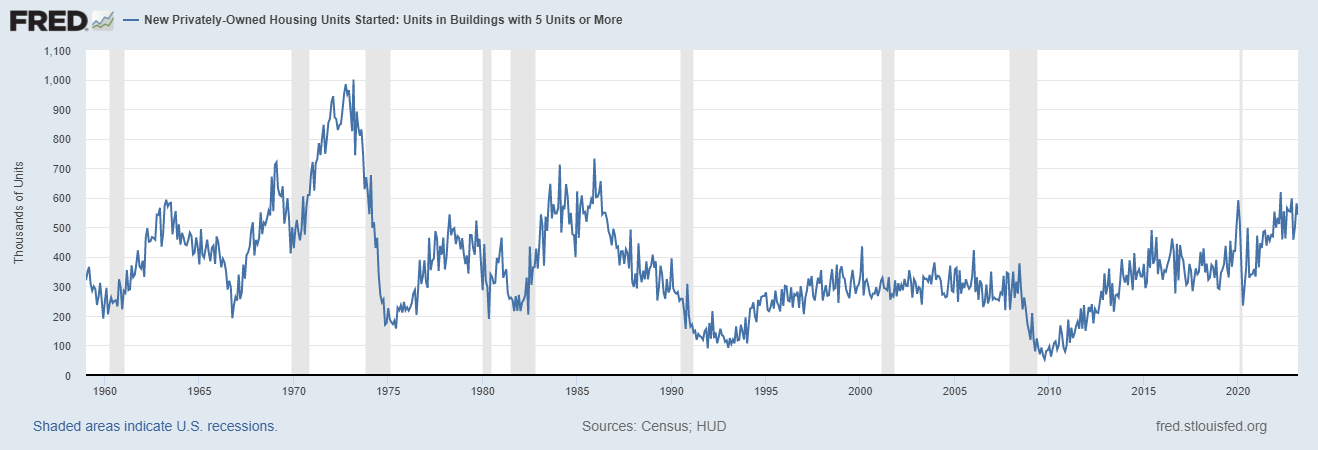

Well over 90% of Real Estate’s revenues come from placing maintenance and leasing professionals for multifamily properties. New apartments present limited opportunities to Real Estate. What we really need are older units that require maintenance and updates. Figure 2 shows apartment starts going back to 1959.

Figure 2

{kind=link}

There are plenty of old apartments out there. And the uptrend in new units started after the Financial Crisis of ’08-’09 bodes well for coming decades.

When you read media reports on how bleak the housing market is due to people not being able to find or afford single-family homes to purchase, just invert that message: apartments are doing great. We can expect very impressive growth from Real Estate for the foreseeable future.

Demographics and housing dynamics have compelled many investors into the apartment space. Of course, putting money into Real Estate is an indirect method of investing in apartments. Many investors—especially private equity—have gone straight to source . Let’s contrast owning all or a portion of a 300-unit property compared to an equal size investment in BGSF Real Estate. [1] Let’s say the apartment property is worth $20M, which means annual depreciation will be well over $500,000. Using depreciation as a proxy for capital expenditures, this is a lot of annual spend. The mortgage on this property would likely be north of $14M with monthly payments around $100K. Because of the cheap debt employed, the returns on this investment would have been very impressive pre-pandemic. However, during the worst 12-months of eviction moratoriums ((EMS)) revenues plummeted, costs remained about the same and losses would have been much higher than $250K for this hypothetical property. The federal government set aside billions in rent relief , but due to red tape and less-than-helpful tenants , much of that relief never made it back to landlords to make up for the losses. And what was recovered required yeomen’s work.

Landlords have rebounded forcefully of late, just in time to see huge percentage increases in mortgage rates, severely crimping returns.

Real Estate, on the other hand, doesn’t require anything more than modest debt so increasing interest rates are of no concern. Before the pandemic, the Real Estate segment's business was arguably more economically attractive than your typical apartment property. During the worst 12 months of EMs, if we split BGSF’s home office expenses and depreciation between Real Estate and Professional (see pp 71 and 72 of 2021 10-K ), I estimate Real Estate turned an operating profit of $5M with only $260K in depreciation! It’s hard to imagine a worse time for apartments; BGSF simply downsized and salvaged a profit. And see Figure 1 for how impressive Real Estate was able to snap back revenues, picking up right where it left off pre-pandemic. Unlike the debt-laden, bulky 300-unit property—which can’t grow or shrink in size—Real Estate is fleet of foot, national in scope and pays for its own fast growth.

Before moving on to the revenues of Professional, we should note that Real Estate has a non-residential group which focuses on providing staff to commercial properties (office buildings, strip centers, indoor/outdoor malls, etc). This small group (I estimate revenues around 5% of Real Estate’s total $121M ’22 revenue) had just gotten off the ground pre-pandemic. After fighting through an impossible ’20 and ’21, this commercial group is attacking a Real Estate space that is still in flux but shows promise.

In 2017, Professional’s top line was $127M compared to 2022’s $173M—which translates to a CAGR of about 5.5%.

Under pandemic conditions, that is nice, but keep in mind management’s commitment to growing this business via primarily acquisitions. Very recent acquisitions add about $40M of revenue to 2023’s top line, so I estimate the 6-year CAGR will approach 7% by the end of fiscal 2023. Gross profits have improved along the way. Unfortunately, shareholders won’t see any of that profit if the expenses required to run that business remain high. This begs the question: When management sought out these higher margin businesses, just which line item of margin was the focus?

The Professional segment’s future is also bright from a growth perspective as it focuses on IT consulting. I estimate that the current market for IT consulting is approaching half a trillion dollars. And that only grows as more businesses, schools, governments, NGOs, etc. shift from yesteryear’s systems to the software/cloud services available today.

SG&A Is The Problem

In 2017, BGSF’s Selling, General and Administrative (SG&A) line item on the income statement was 16% of revenues.

In 2022, BGSF’s SG&A was 28% of revenues.

The difference in that singular line item is the difference between an impressive financial year and a disappointing one (and SG&A has been out of line for a few years now). Keep in mind that the vaunted and well publicized IT Roadmap (see p. 8, BGSF 2019 10-K )—implemented between 2019 and 2022—was supposed to improve efficiencies. This one-time $12M-ish expense spread out over 3 years (some capital expenditure and some operating expense) now looks small as SG&A is running about $30M (!) more annually than it was in 2017. And this from a company whose IT consulting group sells itself on smooth implementation of technology updates.

There is plenty of good news on this SG&A front. First, to repeat, the top line has grown impressively. Revenue growth can quickly heal self-inflicted SG&A wounds.

Second, BGSF management knows this controllable line item must be rationalized.

And third, to secure the Real Estate franchise, it is better to over-protect the castle than under-protect.

But what is a reasonable SG&A for the BGSF of 2023?

To help answer that critical question, let’s take a quick look at some peer companies’ SG&A for 2022 as a percentage of revenues: Kelly 19% , TrueBlue 22% , Manpower 15% , Kforce 22% , ASGN 20% and Robert Half 29% .

Viewing BGSF’s segments as two very different businesses, I suggest Real Estate’s SG&A should be lower than all the above peers except Manpower. The Professional segment requires more spending. On average, I estimate an acceptable outcome for BGSF is 23%-or-less companywide. If it had been 23% in 2022 (all else the same), we would have seen BGSF’s pre-tax earnings from continuing operations at $29M—doubling actual results.

So why has BGSF’s SG&A gotten out of control? Management has been quiet on this subject (see second half of their 2022 Q4 earnings call from March 9, 2023).

An antagonist of management might argue it is because technology upgrades have been poorly implemented—embarrassing for a company marketing its prowess at helping other entities through such change management. The much-heralded IT Road Map was only close to budget as long as you don’t count all the bodies thrown at undone work due to still-endemic inefficiencies.

A more charitable argument is that in 2017, under previous management, the company was using tin cans and copper wires to communicate. In reality, back then, salespeople and back-office workers were relying on spreadsheets and stamped time sheets. As such, the 16% of revenues SG&A occupied was deceptive. A more reasonable approach to viewing trends in the company would be to start with a normalized SG&A in 2017 that approximated 18% of revenues. In doing so, we imagine technology solutions that resembled those from circa 2010 for BGSF, costing about $6M annually more than reported.

To remain a viable, compliant company, major technological investments were required for communication, processes, continuity and reporting. As discussed in more detail in the next section, there is tremendous good that comes from all that investment over the past four years. Still, SG&A has been out of bounds in recent years.

What Wins Out? Enduring Competitive Advantages

On the surface, it appears BGSF has more than adequate growth and excessive expenses. Let’s dig deeper to better understand how this might play out.

I can’t speak to the short term, but long term BGSF’s enduring competitive advantages will win out over spending. Of course, as Buffett explains, enduring competitive advantages—or moats —can be found in the form of either franchises or low-cost providers. I’ve identified three moats for Real Estate and one for Professional. Of those four, two of them are of the low-cost provider variety, one fear based and one a strong franchise. A franchise allows superior pricing— Buffett’s most important factor when evaluating a company.

The Real Estate segment has such a franchise. Let’s perform a thought experiment comparing Real Estate and Business K, whose hypothetical staffing operations are standardized and commoditized—meaning it has branch offices spread throughout the U.S. and places a range of talent (e.g., workers for warehouses, stadiums, restaurants, etc.).

Compare two similar sales representatives, one from each business. K’s representative marks up his placements an average of 25% (e.g., a painter who receives $10/hour costs the paying employer $12.50/hour). To keep numbers simple, let’s assume this salesperson has a huge book of business, and places enough workers to generate $3.75M in K’s top-line revenue. The aforementioned 25% mark-up translates to gross margins for K of 20% ($750K of the $3.75M).

The salesperson for Real Estate marks up her placements an average of 50% (e.g., a painter who receives $10/hour costs the paying employer $15/hour). For the same number of placements as K’s representative, Real Estate’s generates over $4.6M in top-line revenues with gross margins of about 35% ($1.6M of the $4.6M). RE’s salesperson receives modestly higher compensation than K’s.

That pricing difference is incredible, but five years ago I didn’t know if it was durable so I categorized it as a weak franchise while holding out hope it would graduate.

Graduate it did.

I now deem Real Estate a strong franchise. It is the only staffing firm with a national footprint (now international) that caters exclusively to apartments, which is why it can mark up prices so high. No other sizable firm competes in this space exclusively. When apartment managers call Real Estate, they know what they are looking for and will get. The value that apartment managers place on Real Estate continues to grow.

Being first to market offers benefits if a business can build a moat—in this case, if it can create scale and invest in technology—which is exactly what Real Estate has been doing. Our first moat, then, is a very impressive franchise model that is durable.

Real Estate’s second moat is expense based. Returning to our two sales representatives, let’s now consider the money that is needed to support operations. In K’s case, there are the full-bore expenses of a branch office (lease, insurance, utilities, technology, etc.), as well as the constant support from home office (a multiple of the previous parenthetical). I estimate K’s pre-tax income from that hypothetical representative approximates 5% of revenues. Unimpressive.

For Real Estate, there are rarely branch-office expenses. When it opens a new territory, it hires a remote sales representative—an obvious way to cut costs substantially.

I estimate Real Estate’s pre-tax income from that hypothetical representative approximates 20% of revenues. Most of that impressive outcome is thanks to franchise pricing, but a good chunk of it comes from reduced overhead. That’s a business you want to own for a long time.

Real Estate’s third moat is fear based and unlike the first two moats that were built by hand, this one was triggered by a natural disaster: Covid-19.

The eviction moratoriums (EMs) that came with the Covid-19 pandemic proved brutal for apartment owners and service providers like Real Estate. I’m not arguing herein that EMs were good; they were very, very bad for Real Estate. But some good has come from them. Any staffing company that previously had considered entering the apartment space has been scared straight (irrationally).

The best news here is that EMs have been extraordinarily rare in this country . Prior to 2020, we’ve had a couple of regional EMs of short duration after hurricanes. During the Great Depression, various EMs were implemented in spots around the country. That’s it. Extremely rare. All regional. All short term. My opinion is formed from my research: Those outside the apartment industry will carry a misplaced recency bias against investing in them for some time, even though the Supreme Court’s ruling in Alabama Association of Realtors v. Department of Health and Human Services substantially narrows which federal entities can invoke such short-term measures in the future (emphasis on short-term ). Stated differently, recent EMs have no historical precedence and cannot be executed as easily going forward.

To summarize Real Estate’s durable competitive advantages, it has achieved a strong franchise (its first and most durable moat) in singularly cornering staffing for the apartment industry; its lowest-cost-provider (second) moat has been eroded by out-of-bounds spending that should be corrected shortly; and the irrational fear EMs have struck in other staffing companies regarding apartments created a bonus (third) moat that should have staying power into the next decade. The fourth and final moat I have identified is found in the Professional segment. Compared to five years ago, this segment has effectively left finance and accounting staffing and is now in the IT consulting space, competing with traditional consultant companies like Accenture, PwC and Deloitte as well as traditional staffing firms that have waded into the consulting waters like Robert Half and ASGN. I offer a more thorough description of this changing and growing industry in my blog post of 11/1/21, Recounting My Errors and Correctness On BGSF 27 Months Later: Bolshevism and Sentiment .

In addition to leaning on that blog post, I now invoke my Seeking Alpha seven-part series on the Home Healthcare ((HHC)) industry from 2009 ( final article linked here ) as the similarities have merit. 14 years ago, I released that series with a focus on four public companies that I felt were destined to do well in the healthcare sector for a variety of reasons, rock-bottom pricing among the most important. Essentially, I argued then that HHC players would strip away market share from expensive skilled nursing and ambulatory care facilities while at the same time benefit from a quickly growing population of 70+ year olds.

In today’s consulting space, we can view the Accentures of the world as bulky facilities (their partners are drastically overpaid and their expense reports expensive) while, in many cases, outfits like BGSF Professional and Kforce can provide the same services and contingent staff for less money. And similar to our growing elderly population demanding healthcare solutions, more and more organizations are demanding IT consulting. I’m not arguing here that I’ve identified any durable competitive advantages for Professional, rather, staffing companies that are competing with traditional consulting companies have stiff tailwinds for the foreseeable future. The “industry moat,” if you will, exists for all the lower-cost players (staffing-cum-consulting companies) in this growing space.

Noteworthy for BGSF’s IT consulting group: recent acquisitions have strategically enabled end-to-end and global consulting abilities.

How to Value BGSF

BGSF’s management team is led by three people—CEO and Chairperson Beth Garvey, retiring CFO Dan Hollenbach and incoming CFO John Barnett—all of whom I’ve gotten to know over the past five years. In my estimation, each of these managers has integrity, energy and intelligence.

The board of directors and management must realize that SG&A is unacceptable and quickly act to correct it. It is the board’s job to ensure management performs. It is the shareholders’ collective job to ensure the board performs.

The good news here is that the other shareholders I know mirror my faith in current management.

Industry Forces

The staffing industry is, for the most part, cyclical. [2] In my experience, over the long term, cyclical stocks outperform defensive stocks. The reason, I suspect, is that cyclicals are more frequently undervalued because most investors shun them due to their inherent volatility. Starting from a lower price (valuation), it is easier for these stocks to outperform the more dearly priced defensives.

And within the cyclical space, staffing companies are superior investments because of two macroeconomic tendencies: 1) the outsourcing of non-core functions by businesses and other entities; and 2) more gig work (as explained in more detail in previous articles ). Further, staffing is a very low-capital business: there aren’t a lot of depleting assets to replace. That’s a double-edged sword as barriers to entry are low—which is why overspending on protecting our castle is a forgivable sin.

Any staffing company is subject to the industries it serves. In the case of BGSF, the Real Estate segment is hyper focused on apartments. Apartments are subject to economic cycles. [3] The Professional segment provides IT consulting and contingent staff to any entity anywhere in the economy and is, therefore, also subject to economic cycles.

The Professional segment’s future is also bright from a growth perspective as it focuses on IT consulting. Even if the IT consulting space was stagnant, Professional, like other staffing-cum-consulting companies, would steal market share from traditional outfits. In such a non-industry-growth setting, I imagine Professional’s top-line growing 2%-4% organically.

But this industry is fast growing. I estimate that the current market for IT consulting is approaching half a trillion dollars as more businesses, schools, governments, NGOs, etc. shift from yesteryear’s systems to the software/cloud services available today.

Tailwinds for Real Estate’s and Professional’s respective top lines are stiff for years to come due in large part to industry dynamics.

Financials

The numbers are clear to me: If I could afford it, I would purchase BGSF today in its entirety, justifying this bold move using strictly Real Estate’s financials. Stated differently, I would pay $100M for only the Real Estate portion of BGSF today if I could afford it.

I am not making any recommendations in this article. I am merely giving my opinion on how I value this company.

If I owned 100% of BGSF Real Estate, I would get SG&A as a percentage of revenue down in the upper-teens as quickly as possible. It might take me a few years to get there. And because I don’t want to estimate revenues that far out, let’s use my estimate of this year’s sales while using X-ray vision to look through the current fat on the SG&A line item to see a slimmed down version of what I opine it should be (18% of revenues).

Hypothetical 2023 -- Peering Through Real Estate’s Bloated SG&A

Revenue $132M

Gross Profit $47.5M

SG&A $23.8M (hypothetical, slimmed down 18% of revenue)

Software Amortization $1M

Depreciation $400K

Operating Income $22.3M

Interest Negligible

25% Total Taxes $5.6M

Net Income $16.7M

Net Tangible Assets $13M – as explained in Appendix

Pre-tax RONTA 100%-150% (!) – as explained in Appendix

For a growth company like that—by itself, without Professional—Mr. Market could easily fix a market cap of $250M (or about $24/share).

But we are using X-ray vision for that view. Reverting to “as reported,” company-wide SG&A accounts for 28% of revenues. I remind the reader that it was merely five years ago when the three BGSF’s segments (Real Estate, Professional and Light Industrial) aggregated 16% SG&A.

The Professional segment requires a higher SG&A than RE, I admit. But if we simply right the RE ship, the current very low price for all of BGSF from Mr. Market would turn upward quickly.

Of course, in reality, when buying bits and pieces of BGSF from Mr. Market today, we get the benefit of having the growing Professional segment thrown into the bargain.

Let’s say the highly prized consultants in the Professional segment can justify SG&A expenses as a percentage of revenue at 30%.

Less Hypothetical 2023 -- Leaving Professional’s SG&A Too High

Revenues $230M

Gross Profit $78.5M

SG&A $69M (leaving it around 2022 levels)

Software Amortization $1.5M

Depreciation $750K

Operating Income $7.25M

Interest Expense $1M (just for the “it” not the “theys” as explained in Appendix)

25% Total Taxes $2M [4]

Net Income $4.7M

Unleveraged Net Tangible Assets $25M – as explained in appendix

Pre-tax ROUNTA Less than 20% —as explained in appendix

That is not a business worth buying by itself. But if Mr. Market is offering it along with Real Estate at no extra charge, I’ll take it and immediately work to cut the fat out of SG&A. A more efficient Professional segment could, by itself, catch a price from Mr. Market of $15/share. A very efficient operation could fetch $30/share.

In buying BGSF from Mr. Market today, we also take on a pro-rata portion of about $80M in debt. Once SG&A is brought back in line, that is really a non-issue. An efficient BGSF could easily lower that to $40M within the next five years. And for that efficient and growing company five years from now, $40M of debt would be less than modest.

Draw your own conclusions about BGSF’s short-term future and stock price. The top lines for both businesses are promising—right now, all eyes are on SG&A.

Recall GEICO had a great stumble 50 years ago and almost went bankrupt before management showed its intrinsic value by leaning hard into its enduring competitive advantage (lowest-cost provider due to lack of field agents). It is my opinion that BGSF has multiple enduring competitive advantages. It is only a matter of time before all of them are repaired and/or strengthened. The financial windfalls can last for decades.

APPENDIX – A Deep ROUNTA Dive

In Why Buffett Prefers ROUNTA To RONTA , I offer substantial context for the mystical Buffett metric of return on unleveraged net tangible assets (ROUNTA). That article is summarized below.

- In the 1970s, Buffett shifted away from the cigar butt approach to investing (buying a company well below its net tangible assets);

- By the 1980s, Buffett’s partner, Charlie Munger, had convinced him that to scale investment operations, they would need to adhere to a nuanced version of valuing companies based on their respective returns on net tangible assets (RONTA);

- This transition is well-documented, but poorly understood;

- To help identify and gauge a business’ economic goodwill (as distinguished from its accounting goodwill), Buffett and Munger make unorthodox adjustments to textbook RONTA in:

- The treatment of intangible assets;

- Earnings based on intelligent amortization; and

- Liabilities based on leverage.

In this appendix, we will review two step-by-step ROUNTA calculations to help readers grasp how to apply Buffett and Munger’s unorthodox mental adjustments to textbook RONTA. I’ve read and listened to Buffett thoroughly, but he doesn’t give specifics in this adjustment process. With substantial diligence, I’ve attempted to broadly quantify his vague words into helpful execution.

A simple mental trick can be quite useful when approaching ROUNTA: use the pronoun “it” when referring to a business; do not get a visual of something that is made up of the corporate leaders (executives or board members). The business is made of employees, customers, vendors, culture, products and services, and it resists being likened to other entities via metaphor or analogy. A business is its own thing, and it is where you measure ROUNTA.

Once a business—“it”—is profitable, others will try to get their stake which is where the “theys” step in: executives, tax authorities, regulators, owners, lenders and lawyers will eventually surround and infiltrate the business. Executives, directors, owners and lenders augment the business and should be associated with the corporate entity , so visualizing such people (some of the “theys”) when contemplating the company is perfectly acceptable. Their involvement (and, as investors, we are one of the “theys”) will complicate calculating finances and returns of the business. We can’t ignore the “theys.” But we can bypass them with our initial ROUNTA analysis.

ROUNTA is sublime because it helps us simplify an otherwise complex outcome: how much money the business—“it”—requires in day-to-day operations vs. how much it kicks out to the “theys.” The mathematical outcome of ROUNTA is the same math that every CEO in the world tries to predict when determining capital allocation. [5]

If we invest in businesses that turn huge ROUNTAs, the profits will make their way to shareholders through all the other “theys” soon enough. [6]

ROUNTA is Buffett’s effort to get the clearest picture as to what it costs a business (UNTA) to get a profit (RO). EBITDA turns a blatant blind eye to costs/expenses. Depreciation is a real expense— and the worst kind .

To make all of this clearer, let’s use a real-world example and estimate ROUNTAs for BGSF’s fiscal years 2017 and 2022. Be warned, there are dangers in performing such specific calculations. The real point is to get an approximation of both the denominator and numerator of this ratio, not focus on exacting math. The remainder of this appendix is not meant for all readers—there is some unorthodox and heavy accounting lifting here and the reader is expected to have multiple SEC filings open to understand the adjustments being made.

Two ROUNTA Calculations—Wisdom Spun Too Finely

Basic finance courses teach that NTA is the product of total assets minus goodwill/intangibles minus total liabilities. As demonstrated in this section, using net tangible assets as a proxy for how much it costs to maintain the business is a splendid way to approach investing. But NTA’s accounting in the corporate structure too often fails to depict reality.

To calculate a business’ NTA and UNTA we need “its” balance sheet—which is an imperfect picture painted by management of the economic reality of the business’ assets and liabilities. A good management team will do its best job in presenting this picture, but never with perfect knowledge. An automobile may carry a book value of $10,000 with a remaining (finite) life of five years. That’s good to know when contemplating future expenses, even if the automobile ultimately gets replaced earlier or later than five years. Estimates are required in business.

Less intuitive than tangible assets are intangibles, which is where we make our first adjustment to textbook NTA.

If you look at p. 13 of Buffett’s 2013 LTS you will see the section titled Manufacturing, Service and Retailing Operations , in which he starts with non-GAAP presentations of a balance sheet and earnings statement. He then explains:

Our income and expense data conforming to [GAAP] is on page 29. In contrast, the operating expense figures above are non-GAAP and exclude some purchase-accounting items (primarily the amortization of certain intangible assets). We present the data in this manner because Charlie and I believe the adjusted numbers more accurately reflect the true economic expenses and profits of the businesses aggregated in the table than do GAAP figures.

I won’t explain all of the adjustments – some are tiny and arcane – but serious investors should understand the disparate nature of intangible assets: Some truly deplete over time while others in no way lose value. With software, for example, amortization charges are very real expenses. Charges against other intangibles such as the amortization of customer relationships, however, arise through purchase-accounting rules and are clearly not real costs. GAAP accounting draws no distinction between the two types of charges. Both, that is, are recorded as expenses when earnings are calculated – even though from an investor’s viewpoint they could not be more different.

In the GAAP-compliant figures we show on page 29, amortization charges of $648 million for the companies included in this section are deducted as expenses. We would call about 20% of these “real,” the rest not. This difference has become significant because of the many acquisitions we have made. It will almost certainly rise further as we acquire more companies.

Eventually, of course, the non-real charges disappear when the assets to which they’re related become fully amortized. But this usually takes 15 years and – alas – it will be my successor whose reported earnings get the benefit of their expiration.

Every dime of depreciation expense we report, however, is a real cost. And that’s true at almost all other companies as well. When Wall Streeters tout EBITDA as a valuation guide, button your wallet.

Our public reports of earnings will, of course, continue to conform to GAAP. To embrace reality, however, remember to add back most of the amortization charges we report.

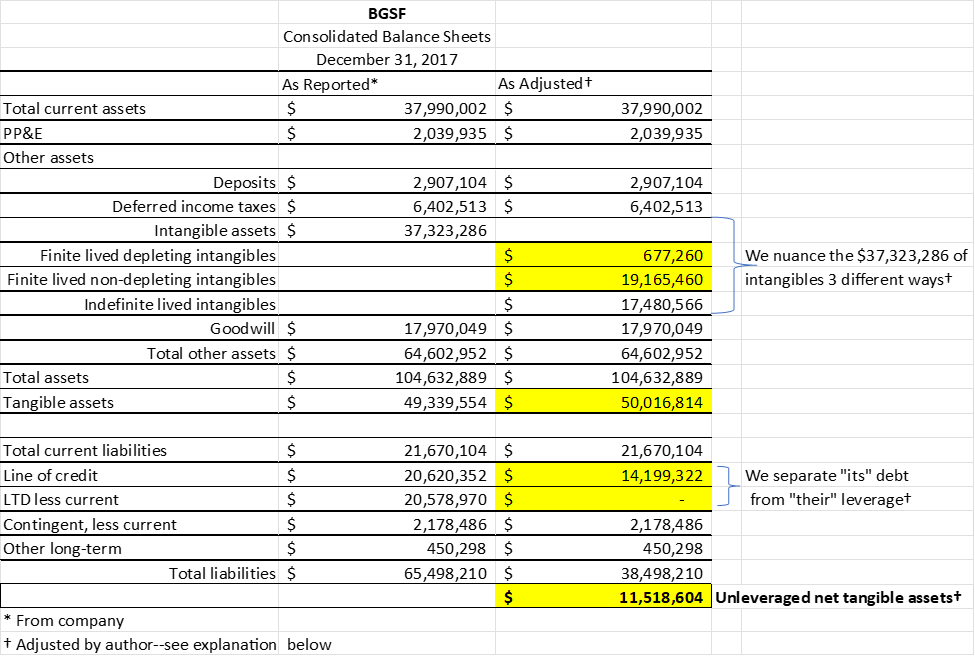

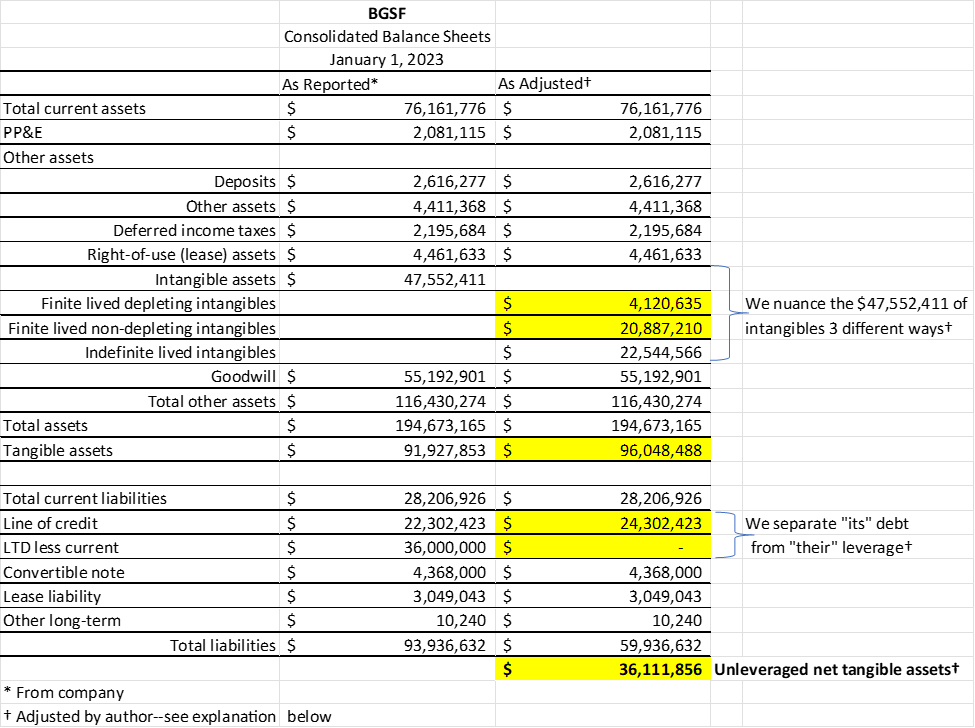

With that guidance, let’s review BGSF’s balance sheets—with my conjoined UNTA adjustments—from 2017 and 2022 (see Figures 1 and 2).

Figure 1

{kind=link}

Figure 2

{kind=link}

Of the nuances in calculating UNTA, analyzing/adjusting intangibles is straightforward and objective. In Figure 1, the first yellow cells highlight these. On the 2017 10-K balance sheet, BGSF reports $37,323,286 in intangible assets, and then, on page 50 , breaks that figure into two buckets: “finite lived” (amortized) and “indefinite lived” (unamortized). The indefinite lived assets (net carrying value at that point was $17,480,566) should be subtracted from tangible assets in both textbook NTA and nuanced UNTA calculations. But the finite lived assets must be broken down into two sub-categories, what I refer to above as finite lived depleting intangibles and finite lived non-depleting intangibles. [7] In the first yellow cell of Figure 1, the $677,260 of finite lived depleting intangibles is made up of the then-carrying value of BGSF’s computer software (yikes, that’s tiny!). That these are amortized makes perfect sense: like automobiles, software must be updated and eventually replaced. It walks and talks like tangible assets. It really shouldn’t be considered anything like the other intangibles.

In the second yellow cell of Figure 1, I show $19,165,460 of finite lived non-depleting intangibles—$18M of the then-net carrying value of customer lists and almost $1M of covenants not to compete (p. 50). This is exactly what Buffett harps on above: “Charges against other intangibles such as the amortization of customer relationships, however, arise through purchase-accounting rules and are clearly not real costs.” If we are trying to get a clear view of the company’s costs/expenses, amortizing these intangibles doesn’t help; rather it nonsensically strips away at our pre-tax income figure. We are going to adjust that charge out of our RO math below. We are also going to subtract this figure from assets to figure tangible assets—just like textbook NTA math.

Let’s review the same lines in Figure 2 (2022) before moving on to leverage.

The finite lived depleting intangibles grew quickly due to BGSF’s IT Roadmap, and in 2022 was $4,120,635 (p. 57, 2022 10-K ). This line item is still comprised only of computer software— which walks and talks like tangible assets and is how I will categorize it in our UNTA math. The finite lived non-depleting intangibles line item of $20,887,210 is once again made up of predominantly the then-net carrying value of customer lists and a small amount of non-compete covenants (p. 57).

We thus conclude our adjustments to assets with a pair of noteworthy changes in each year: tangible assets are increased due to the finite lived depleting intangibles line item (computer software), and while we follow textbook NTA rules in handling finite lived non-depleting intangibles, we must put a pin on its amortization, to which we will return when we adjust pre-tax income.

Less-Straightforward and Less-Objective Liabilities Adjustments

Buffett rarely uses decimals. His use of estimates with numbers is very intentional. The words he offers are similar: ambiguity is a big player.

Offering step-by-step ROUNTA calculations for BGSF includes precision and, therefore, is in many ways a fool’s errand. My assigning which leverage to count and which to not (see below) is precise for 2022, but less precise in 2017. When dealing with anything more than modest debt, adjustments get subjective. I repeat here that Real Estate’s business model is so good that it can pay for its own growth while spitting out gobs of capital for allocation elsewhere. Real Estate doesn’t need more than modest debt.

The Professional segment is different. This doesn’t necessarily make it bad; rather it requires more diligence and vigilance when analyzing debt. It also requires using estimates. And the more you study businesses the easier estimates get.

Great businesses don’t require anything more than modest debt, mostly used for day-to-day operational needs with the occasional increase during financial hardships or growth that will be paid back quickly. BGSF management has aggressively grown the Professional segment via mostly acquisitions with some organic expansion. Using leverage for this is fine, as long as superior returns on capital are garnered and used to pay off the debt. [8]

Let’s look at BGSF’s debt situation before and after its acquisition of Horn Solutions in December 2022 as an example of how I work leverage adjustments into UNTA. As I described in the longer ROUNTA post, once a business is saddled with more than modest debt, using both an NTA lens and an UNTA lens may be helpful (as more debt is added, NTA becomes less useful). Once debt gets to leveraged status— admittedly , a frustratingly vague term —only UNTA should be used (NTA, in this case, is worse than useless, it is deceptive).

Just after its divestiture of the Light Industrial segment last year , BGSF’s long-term debt was paid off and its line of credit showed about $14M drawn (p. 4, 2022 Q1 10-Q )—as low a figure as you will find in recent years. Of that $14M, was there any residual leverage from previous acquisitions of goodwill/intangibles that required adjustments? Over time, these debts should be paid off and that math for adjustments goes away. To simplify the matter, as of last April, we reset any leverage math for BGSF and view $14M as less-than-modest debt. [9] , [10]

The price for Horn was $42.7M, of which $14M was allocated for intangible assets and $26M for goodwill, paid predominantly with debt—let’s call it $38M debt and $5M other (p. 54, 2022 10-K ).

Separating the “its” from the “theys” is extremely helpful at this point in our math. As much as corporate officers and directors think about the company’s capital structure, a business itself is its own thing. Almost none of Horn’s intangibles and absolutely none of its goodwill purchased by BGSF in December 2022 are of concern to the “it” (in this case, BGSF’s Professional segment). Those newly acquired intangibles and goodwill don’t affect its operations. True, there is an impact to economic goodwill, but we are focused here on how to address the accounting goodwill and intangibles purchased with newly issued debt. In my mind, the debt that Real Estate and Professional (the “its”) were carrying for operations didn’t change upon the acquisition: the day before and the day after Horn was acquired, that debt load totaled approximately $24M (very similar to the $27M reported in the 2022 Q3 10-Q ).

Relying on textbook math for net tangible assets, after bringing Horn’s assets and liabilities onto BGSF’s consolidated balance sheet, we deduct the newly added goodwill/intangibles. That is exactly what we are doing with this UNTA math. The next step is quite different from the textbook: we ignore $38M of leverage when subtracting liabilities from tangible assets to settle on unleveraged net tangible assets.

To subtract that debt would be to double subtract the Horn goodwill and intangibles. Assume Professional’s NTA was $40M before the Horn acquisition. If we subtract the new debt, NTA would approach zero after adding Horn.

That doesn’t make any sense if we are trying to get a real picture of the depleting assets required to keep up the business. But if we focus on the “it,” a nuanced calculation of UNTA makes perfect sense. We nuance the intangibles and apply the U to avoid double subtraction.

That debt must be paid off, of course, but if the business can turn a great ROUNTA that won’t be a problem. Like tax authorities and shareholders, lenders are part of the “theys,” and they will take their share of profits. ROUNTA bypasses the “theys” so we can focus on the “it;” we can then tackle the “theys” one at a time. Of utmost importance, ROUNTA enables us to seek out superior businesses, without getting tripped up in the corporate structure.

With that Horn discussion as our focal point for the liabilities portion of 2022 adjustments completed, see my highlighted unleveraged net tangible assets figure at the bottom of Figure 2: $36.1M.

For 2017 leverage adjustments, we will use the same approach with an abbreviated explanation while transitioning to even more estimates (a far superior methodology than above). BGSF acquired two companies in 2017, Smart Resources for about $8M and Zycron for about $23M (pp. 47-49, 2017 10-K). About $27M of those $31M aggregate dollars were allocated to goodwill/intangibles. Hence, I am subtracting about $27M of the leverage (which was used primarily to fund the acquisitions) to reflect a closer-to-reality operating debt level of $14M (see “As Adjusted” column on Figure 1). This leads us to a 2017 UNTA of $11.5M.

You don’t have to be a math major to appreciate that the denominator for the ROUNTA equation in 2017 ($11.5M) is far more attractive than that of 2022 ($36.1M). BGSF spent money on many assets in those five years, which can be economically appropriate only if they keep returns high. So, let’s check out the income portion of this equation to see if 2022 profits vs. costs kept pace with 2017. Spoiler alert: they don’t.

Straightforward Pre-tax Adjustments

The majority of our discussion in figuring ROUNTA is on the cost/expense portion—ignored by EBITDA. UNTA imperfectly gives us an idea of what the business costs. There are options for the numerator, but for consistency’s sake I’ve settled on pre-tax earnings, which was “reported” by BGSF in 2017 as $14.5M and in 2022 as $14.9M.

The first adjustment to earnings is to add back in those phony amortization dollars. Recall that pin we dropped on the $19,165,460 of finite lived non-depleting intangibles from 2017. Total amortization expense for 2017 is $5.7M (p. 40, 2017 10-K ), the vast majority of which we will add back into pre-tax earnings. Let’s use $5.5M as our phony amortization charges.

The second adjustment is to separate interest paid for the “its” vs. the “theys.” In 2017, the two acquisitions were in the first half of the year. Using a quick estimate, let’s say there was an average of $12M of operational debt all year at 6% APR: $720K of interest paid for the “its.” That means we add the remaining interest paid ($2.5M—p. 38, 2017 10-K ) for the “they” back into pre-tax earnings. Our current running total is: reported $14.5M + $5.5M phony amortization + $2.5M interest paid on behalf of “they” = $22.5M.

We could stop there in good faith, but let’s go one step further and try to get a more realistic picture of earnings. The SG&A expense in 2017 was not sustainable. We are trying to value what this business is worth going forward, so let’s use the estimate I offered above: change the 16%-of-revenue SG&A line item to 18%, which adds about $6M of expenses, giving us our final adjusted 2017 pre-tax income of $16.5M.

So our return on ($16.5M) unleveraged net tangible assets ($11.5M) in 2017 equals 143%. A precise number that is just silly to state due to the estimates used above. I suggest Buffett’s description of all of this would be to call 2017 returns terrific and skip the previous five pages. Munger would likely make a derisive comment about the above specificity but agree that BGSF’s businesses in 2017 put together a great year measured in terms of ROUNTA.

From the 2022 10-K, BGSF’s pre-tax reported earnings are $14.9M. First, let’s add back in the phony amortization dollars, which I estimate to be $3M (p. 45, 2022 10-K ). Next, we have to think through the timing of that Horn acquisition. Even though it took place with only three weeks of the year remaining, I’ve got its balance sheet consolidated in my 2022 figures as if it were making up the UNTA denominator the entire year, [11] which is fine if we can use a good estimate of what Horn’s contribution to pre-tax income would have been for that same time period (the reported figures only show three weeks of income contributions). On p. 55 of the 10-K, management gives us Supplemental Unaudited Pro Forma Information on that acquisition (though it is mixed in with a smaller and older acquisition). With this we can add $2.5M to the pre-tax line. Finally, we separate interest paid for the “its” vs. “theys.” In this case, no math required as debt for “theys” was assumed with less than a month left in 2022. This gives a total adjusted pre-tax income of $20.4M.

Divide that by the UNTA of $37.4M and we get a ROUNTA for 2022 of 55%, or stated better, in a range of 40%-60%. A dramatic turn for the worse over 5 years.

Stop the Madness

Every time I start talking about all this stuff, Charlie reminds me that I’ve never prepared a spreadsheet. But, in effect, in my mind I do. (Warren Buffett, Berkshire Hathaway Annual Meeting, May 2007 )

You’ve got a complex system and it spews out a lot of wonderful numbers that enable you to measure some factors. But there are other factors that are terribly important, [yet] there’s no precise numbering you can put to these factors. You know they’re important, but you don’t have the numbers. Well, practically (1) everybody overweighs the stuff that can be numbered, because it yields to the statistical techniques they’re taught in academia, and (2) doesn’t mix in the hard-to-measure stuff that may be more important. That is a mistake I’ve tried all my life to avoid, and I have no regrets for having done that. (Charlie Munger, Academic Economics: Strengths and Weaknesses, Considering Interdisciplinary Needs , October 2003)

For master investors, these step-by-step ROUNTA calculations are, I suspect, laughable. The specificity is counterproductive.

Investors should stop getting to the 10 th or 100 th decimal place. Numbers are useful, but we should spend more time contemplating what numbers miss. The idea that BGSF’s 2017 financial success could be quantified into the specific number of 143% ROUNTA is ridiculous.

Think of a master mechanic who can watch and listen to an engine to figure where problems lie. A diagnostic machine, to him, might seem a waste of time. Think of a master chef who doesn’t need to study an ingredient list or directions to create a wonderful meal. Buffett doesn’t think in specific ROUNTA terms like those laid out above . Rather, I lay out those terms and numbers to try and help non-masters get their brains wrapped around some distant relative of what we can strive for.

Take my 2022 BGSF UNTA figure ($36.1M) and imagine what we are to do in 2024 when debt obligations fall from the reported 1/1/23 $66M gross figure to, say, $50M (down $16M). The accounting goodwill figure for Horn will, presumably, still be the same, while the intangibles will not have been amortized by anything close to $16M. Further, let’s say the “it” stopped expanding organically to pay off its operational debt. How then do we split up the gross amount of debt between operational (to be counted) and leveraged (excluded from UNTA)? Separately, what if organic expansion is used aggressively? In that case, there is no goodwill but more than modest debt.

The answers to these questions are imprecise.

In his testimony to the Financial Crisis Inquiry Commission on June 2, 2010 ( see the 37.43 mark here ) Buffett admits: “It’s very hard to define leverage, because you can have some institutions that are 10 for 1 and their assets are all Treasury bills and it doesn’t make any difference, and you can have somebody that’s 3 for 1 and it can be all second mortgages and you got lots of trouble.” As I detail in my longer ROUNTA blog, when unsure whether to use either the UNTA lens or the NTA lens, use them both to help get an idea of the costs of a business. Less precision, more worldly wisdom .

[1] Multifamily property ownership using substantial debt has been a favorite of private equity managers for several years. Those PE funds with only fixed mortgage rates won’t feel the pinch of increased interest rates immediately but will struggle deploying dry powder in this space going forward. Those PE funds with floating rates on mortgages or other leverage are feeling substantial pain right now. More realistic interest rates on large debt loads are stripping multifamily property ownership of its economic attractiveness.

[2] AMN Healthcare and Cross Country Healthcare are good examples of defensive staffing firms because they cater exclusively to the healthcare sector.

[3] Originally in my 2019 article, I mistakenly thought of RE’s services being rendered for apartments fairly equally between maintenance for in-place residents and make-ready work for apartments being turned over (i.e., preparing or updating a unit between residents). In other words, whether times were hard (few unit turnovers and more in-place maintenance) or good (more turnover and less in-place maintenance), the need for help from RE would remain fairly constant. I was wrong. In reality, about 70% of the work performed by RE’s placements is for the turnover variety. As such, macroeconomic cycles play a role. There is always work to be done on B- and C-class apartments, but there is more work when residents are moving.

[4] Layering interest expense from “theys” (well over $3M) into this math complicates the matter unnecessarily as it would show tax expense decreasing substantially. If we just focus on the “it,” we can address the “theys” later.

[5] Admittedly, most have never heard of ROUNTA and errors in judgment are common. But the fiduciary responsibility of management is to allocate capital to garner the best returns.

[6] Any Finance 101 class will cover the magic of compound interest . In the ROUNTA blog post from ’20, we spent some time reviewing Kraft Heinz and its 86% ROUNTA. Buffett claims it is a great business because it “uses about $7B of tangible assets and earns $6B pre-tax on that.” As such, there is no compounding of interest. Stated differently, we keep $7B in the business annually and at the end of each year we pull out $6B. There are lenders and tax entities to pay before we get our portion of the after-tax profits, but it is still an impressive haul. Great ROUNTAs can compound if we can find other businesses in which to invest offering similar returns. Or, in some instances, like BGSF Real Estate where growth is ongoing, we can simply flip all that money right back into the business and it does compound until the business reaches market saturation.

[7] The latter’s name does smack of an oxymoron. Call it what you will. It is “finite lived” in that it will be amortized by accountants but “non-depleting” because it lacks comparison to depreciable assets.

[8] I don’t want to lose focus on the topic at hand, but it should be noted that issuing stock instead of debt is only intelligent when we give away nothing more than we get. This means if the stock price is deficient, it should not be used.

[9] Note that this debt payoff on behalf of the Professional business was had via a sale of a separate business by the corporate entity.

[10] Many investors are used to seeing some level of cash on the balance sheet. For companies of similar size to BGSF, the “Cash and cash equivalents” line item might show several million dollars. Since BGSF uses the line of credit as an alternate to cash, we should ignore the lack of cash and focus on other measures, like current ratio—even if it requires us to split the current and long-term sections of the balance sheet (i.e., imagine the line of credit is drawn down by $7M so that the company shows $7M cash on hand).

[11] We could have easily completed this same step for 2017 (p. 49, 2017 10-K), but why? That was a ROUNTA blow-out year! It was an EBITDA blow-out year. It was an everything blow-out year. Incredible returns. Point made. Going this extra step would further the notion that we need to get an average of multiple years.

For further details see:

BGSF's Excessive Expenses Are Trumped By Growth And Durable Competitive Advantages