BGX - BGX: Long/Short Loan Fund That Is Actually Just Long

Summary

- Blackstone Long-Short Credit Income Fund is a fixed income closed end fund.

- The vehicle is overweight floating rate loans, and has a high leverage ratio of 40%.

- The CEF is supposed to have a long/short portfolio, but currently there are no short positions.

- The CEF is at the bottom of the cohort from a performance standpoint when compared to other leveraged loan CEFs.

- A recessionary environment is one where long/short vehicles are supposed to shine; BGX does the opposite.

Thesis

Blackstone Long-Short Credit Income Fund ( BGX ) is a fixed income closed end fund. As per its literature:

The Fund's primary investment objective is to provide current income, with a secondary objective to seek capital appreciation. Under normal market conditions, the Fund will invest at least 70% of its Managed Assets in secured loans and at least 80% of its Managed Assets in credit investments. The Fund is a diversified, closed-end management investment company and may employ a long-short strategy. The Fund's short positions may total up to 30% of net assets

The fund ultimately invests mainly in floating rate loans, with a very high leverage level of 40%. What is interesting about this fund is its long/short mandate. In a recessionary environment like today, this type of fund is supposed to thrive via its ability to generate income via strong credits (long only positions), and also be able to take advantage of the weakness in some names shorting them. That is the beauty of a long/short strategy - in the normal course of business a manger can identify which credits are weak, and this mandate allows a manager to profit from that view.

Well BGX hasn't. In effect, BGX is only long as of the latest fact-sheet and furthermore, its 1-year performance is at the bottom of the cohort when compared to other floating rate loan funds. Disappointment here is an understatement. The very thing that should differentiate BGX (i.e. the ability to short credits) is not there, and the fund's performance is lacking.

BGX is currently a long-only fund, having no short positions:

Long/Short Positions (Fund Fact Sheet)

Today's recessionary environment should be one where funds like BGX could thrive by making money both on the long side via strong credits and the short side via dislocations for companies with free cash flow issues.

Analytics

- AUM: $0.14 billion.

- Sharpe Ratio: 0.09 (3Y).

- Std. Deviation: 18 (3Y).

- Yield: 10%

- Premium/Discount to NAV: -13%

- Z-Stat: -1

- Leverage Ratio: 40%

Holdings

The fund holds a portfolio mostly composed of floating rate loans:

Asset Allocation (Fund Fact Sheet)

We can see the CEF following the classic secured loan / high yield bond composition, with just a sliver of other asset classes layered in.

The fund does not take excessive risk via its CCC bucket:

Ratings (Fund Fact Sheet)

We can see the vehicle is overweight 'B' names, and has a rough 10% allocation to CCC credits.

Performance

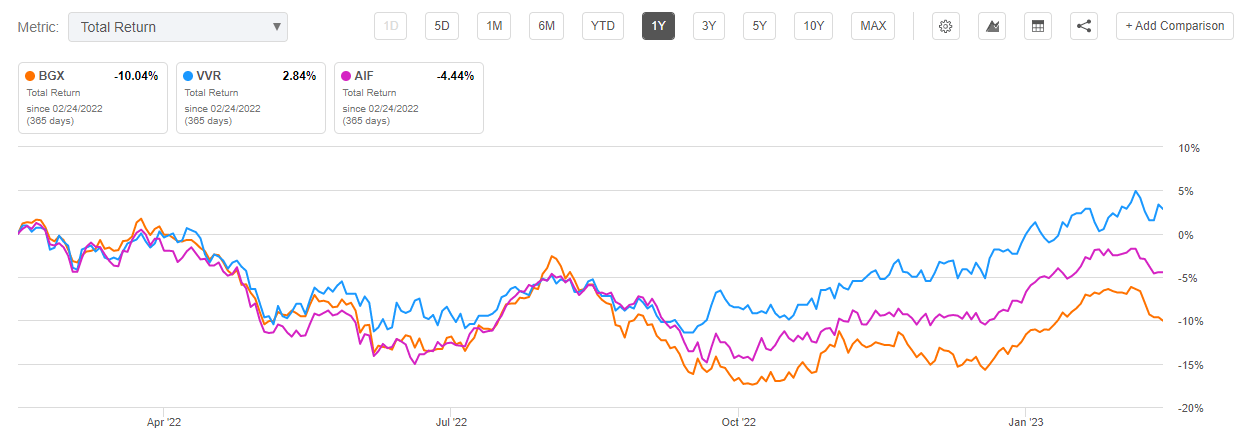

The fund has been trailing its peers in the floating rate loan space in the past year:

{kind=link}

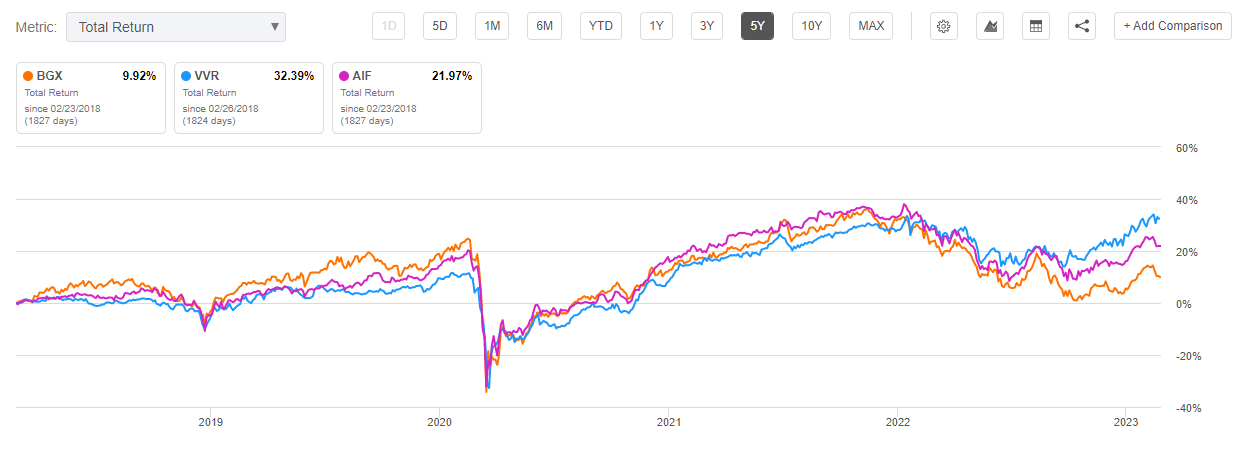

The same is applicable on a 5-year lookback period:

{kind=link}

We would have expected much more here. When you have a CEF that has a mandate to short credits, and you are entering a recessionary environment, that mandate should be your winning card. As a fund, you are able to take advantage of credits which will weaken given the macro situation, while at the same time generate income/carry via stronger names which would be long only holdings. One could say today's environment can be perceived as an ideal one - money can be made easily both on the long and short side. BGX has failed to take advantage of that.

Premium/Discount to NAV

The fund has been trading in a fairly narrow discount range in the past year:

We can see the fluctuations in the discount to NAV are in a very tight range of -15% to -11% here. The fund does not have a high beta to market risk-on / risk-off moves due to its poor performance. The market participants are telling us that the fund will ultimately underperform, irrespective of risk-on/risk-off conditions. This is not a vehicle that can be picked up at a large discount to NAV and traded for a substantial tightening.

Conclusion

BGX is a fixed income CEF. The fund is overweight floating rate loans, which compose over 70% of the portfolio. The fund has a classic build, with the rest of the exposure mainly falling in the high yield bond bucket. The CEF however runs a high leverage ratio of 40%. What is supposed to differentiate BGX is its long/short mandate, the fund being able to short weak credits. Surprisingly, BGX has no short positions as of the last fact sheet. A recessionary environment like today's, should be an ideal time for funds like BGX to generate outsized results. BGX hasn't. In fact, when compared to other floating rate loan funds, BGX is at the bottom of the cohort from a performance standpoint. We do not see any appeal in BGX here - it does not take advantage of its short mandate, nor is it able to generate a robust performance from its long positions. Retail investors are much better set-up to invest capital in this asset class via vehicles such as [[VVR]], [[AIF]] or [[EAD]].

For further details see:

BGX: Long/Short Loan Fund That Is Actually Just Long