FSD - BGX: Very Solid Income CEF Unless Interest Rates Rapidly Decline

2023-12-01 17:25:11 ET

Summary

- Blackstone Long-Short Credit Income offers an attractive 11.83% yield, in line with other alternative debt closed-end funds.

- The BGX closed-end fund aims to be interest-rate neutral, reducing negative impacts from interest rate increases.

- The fund has performed well over the past three years, outperforming the Bloomberg U.S. Aggregate Bond Index.

- The fund is mostly invested in floating-rate bonds so it is well-positioned for higher rates than the market expects. It does not have as much downside exposure as peers, though.

- The fund is paying its distribution fully out of net investment income and it trades at a reasonable valuation.

Blackstone Long-Short Credit Income ( BGX ) is a closed-end fund aka CEF that specializes in the generation of income for its shareholders. The fund’s very attractive 11.83% yield stands as a testament to its ability to provide a very reasonable source of income for its investors. In fact, this yield is in line with other closed-end funds currently being offered by alternative asset managers. We can see that here:

| Fund |

| Current Yield |

| Blackstone Long-Short Credit Income Fund |

| 11.83% |

| First Trust High Income Long/Short Fund ( FSD ) |

| 11.08% |

| Apollo Tactical Income Fund ( AIF ) |

| 11.69% |

| Ares Dynamic Credit Allocation Fund ( ARDC ) |

| 10.96% |

| Carlyle Credit Income Fund ( CCIF ) |

| 15.45% |

Admittedly, some of these funds use a very different strategy than the Blackstone Long-Short Credit Income Fund. However, they are by and large designed to be somewhat interest-rate neutral. As everyone reading this is certainly well aware, one of the biggest problems with most bond funds is that they are negatively impacted by interest rate increases. This is one of the reasons why so many of these funds have been crushed in the market over the past two years. The funds in the table above are designed to reduce that problem and deliver positive returns regardless of changes to the general interest rate environment.

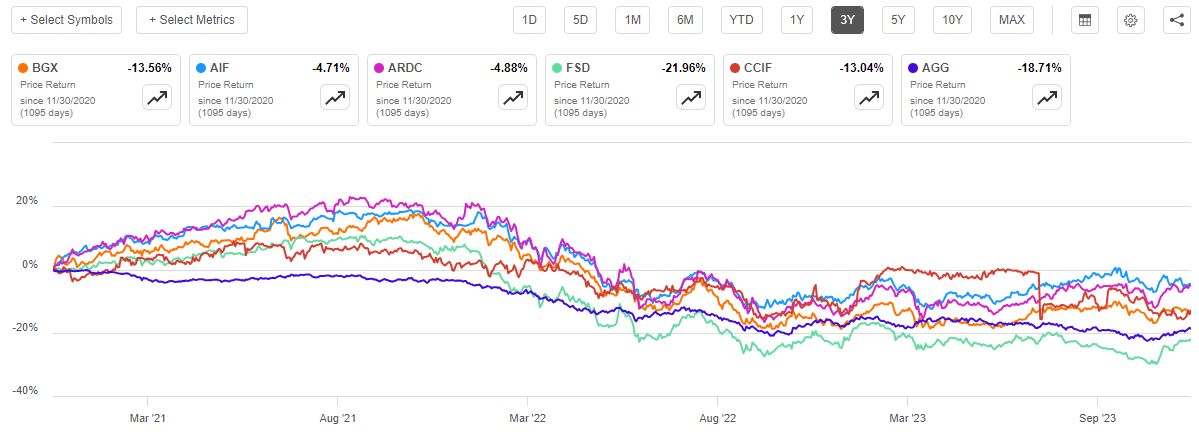

This certainly does not mean that these funds always succeed at delivering a positive return regardless of interest rate environments. For instance, the Blackstone Long-Short Credit Income Fund has seen its price decline by 13.56% over the past three years. That is better than the Bloomberg U.S. Aggregate Bond Index ( AGG ) over the same period, but it is not as good as the Apollo and Ares funds shown in the table above:

{kind=link}

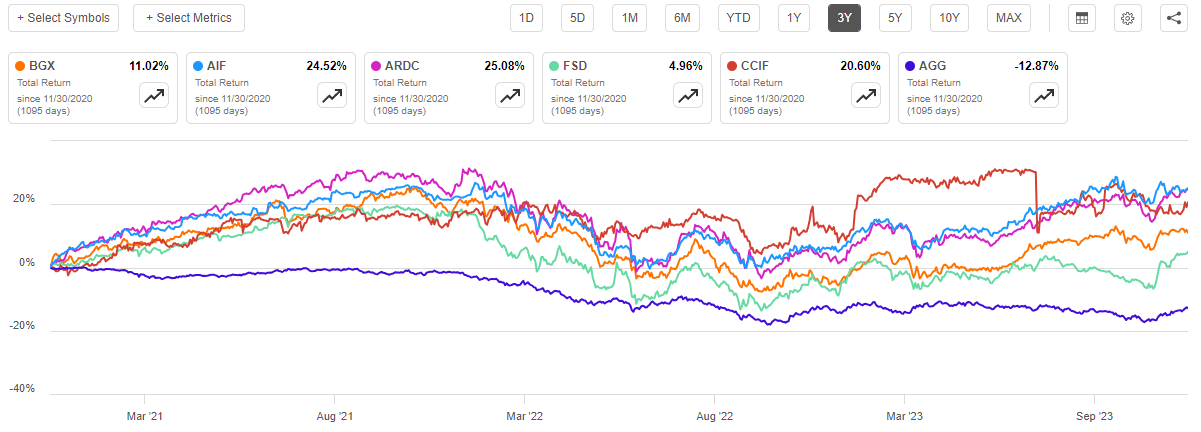

However, as I have pointed out before, we can sometimes get a misleading impression of a fund’s performance if we simply look at the market price. This is because closed-end funds tend to deliver the majority of their total returns to the shareholders via direct payments. After all, these companies usually pay out all of their investment returns in distributions and simply attempt to maintain a flat net asset value. As such, we need to take the distributions that the fund paid out over a given period in order to determine how well its shareholders actually did. When we do that, we see that the Blackstone fund managed to perform quite well over the trailing three-year period, although once again it was not as good as the Apollo or the Ares funds:

{kind=link}

As we can see, investors in the Blackstone Long-Short Credit Income Fund have received a total return of 11.02% over the past three years. That is much better than the 12.87% loss of the Bloomberg U.S. Aggregate Bond Index ETF. As there was a huge shift in the overall interest rate environment over the three-year period, this shows us that the Blackstone Long-Short Credit Income Fund’s attempt to be somewhat interest rate neutral has paid off to a certain extent. That is something that could certainly prove attractive to any investor today, since there is still some uncertainty as to the direction of interest rates, despite some market commentators suggesting the opposite recently.

Let us investigate further and see if this fund could be a reasonable addition to an income-focused portfolio today.

About The Fund

According to the fund’s website , the Blackstone Long-Short Credit Income Fund has the primary objective of providing its investors with a high level of current income. This is not particularly surprising considering that the name of this fund suggests that it intends to achieve its goal by investing in a portfolio that primarily consists of debt securities. As I have pointed out numerous times in the past, debt securities by their very nature have no net capital gains over their lifetimes. These securities are both issued and redeemed at face value, with the only investment gains over their lifetimes being the regular payments that they make to their investors. These regular payments serve as income, so it makes sense that a fund like this would have current income as its primary objective as opposed to something else.

The use of the terminology “Long-Short” in the fund’s name suggests that this is not a typical closed-end fund that simply purchases bonds or other debt securities and holds them. Rather, the terminology suggests that this fund will be engaging in short sales to allow it to profit from a security declining in price. The website explains this in more detail:

Blackstone Long Short Credit Income Fund is a closed-end fund that trades on the New York Stock Exchange under the symbol “BGX.” BGX’s primary investment objective is to provide current income, with a secondary objective of capital appreciation. BGX will take long positions in investments which we believe offer the potential for attractive returns under various economic and interest rate environments. BGX may also take short positions in investments which we believe will underperform due to a greater sensitivity to earnings growth of the issuer, default risk or the general level and direction of interest rates. BGX must hold no less than 70% of its Managed Assets in first- and second-lien floating rate loans (“Secured Loans”), but may also invest in unsecured loans and high yield bonds.

We can very quickly see how this strategy provides this fund with a somewhat interest rate-neutral return profile. As I pointed out in a few recent articles, such as this one , secured loans are typically floating-rate debt securities. A floating-rate debt security tends to have a very stable price regardless of interest rates. We can see this very quickly by looking at the iShares Floating Rate Bond ETF ( FLOT ), which tracks the BBG US Floating Rate Notes 5 Yrs and Less Index. As we can see here, this fund’s share price has been almost perfectly flat over the past three years:

{kind=link}

This is despite the fact that interest rates changed significantly over that period. The reason for this is simply that floating-rate securities always provide their investors with a yield that is competitive with newly issued similar securities in the market. As such, their price does not need to change in order for the yield to be competitive with new-issue securities. That is perhaps the biggest difference between these securities and traditional bonds.

As the fund’s description states, the BlackRock Long-Short Credit Income Fund will always have at least 70% of its securities invested in these floating-rate securities. At the moment, it actually has well above this level, which the fact sheet reveals:

Blackstone - Fund Fact Sheet

As we can see, 83.7% of the fund’s assets are currently invested in secured loans. In addition, the fund also has 2.3% of its assets invested in collateralized loan obligations, which also are typically floating-rate securities. Thus, the fund has fully 85% of its assets invested in things that should remain relatively stable regardless of the direction of interest rates.

The problem with floating-rate securities comes with the fact that they suffer when interest rates decline. This is because the price still remains stable, but the amount of income that they provide to their investors goes down. This is something that could weigh on this fund going forward depending on the direction of interest rates. As of right now, the market is pricing in 125 basis points of cuts to the federal funds rate next year. That is, to put it mildly, unlikely to happen barring a severe recession. According to the CNBC article that was just linked:

Interest rate cuts don’t happen during good times, something important for markets to remember amid hotly anticipated easing next year from the Federal Reserve.

If the Fed meets market expectations and starts cutting aggressively in 2024, it likely will be against a backdrop of a sharply slowing economy and rising unemployment, which in turn would bring lower inflation.

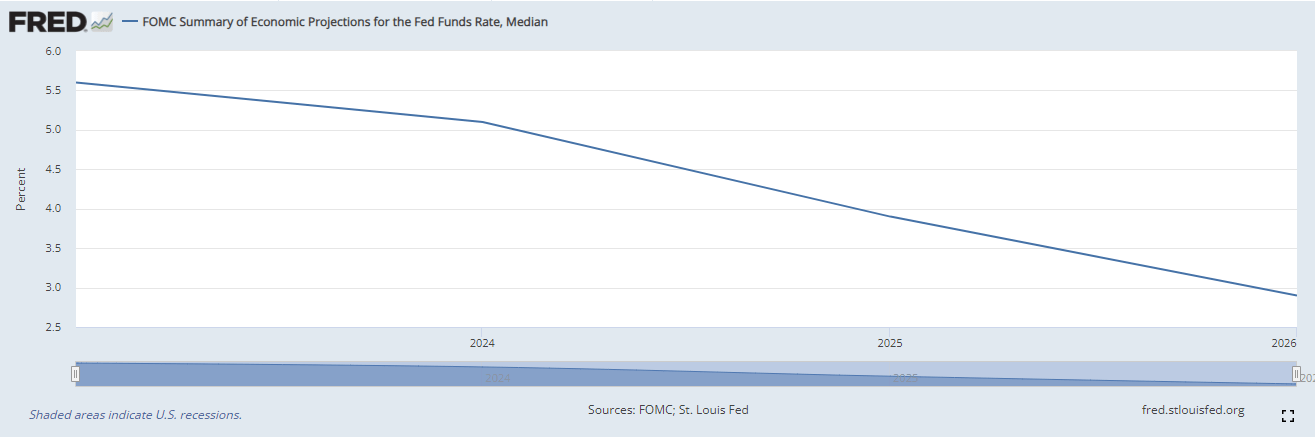

There are certainly some signs that the economy will enter into a recession in the near future if it is not already in one. That could be sufficient to prompt the Federal Reserve to cut interest rates, which appears to be what the market currently expects. However, the members of the Federal Open Market Committee do not currently expect anything close to 125-basis-points of cuts. The median projection right now is a single 25-basis point cut in 2024:

{kind=link}

If indeed the projections by the Federal Open Market Committee prove to be more accurate than the market, then it seems almost certain that floating-rate securities will outperform traditional bonds. After all, these securities should maintain a stable price in that scenario but bonds most certainly will not as it means that rates will be higher than are currently priced in. The Blackstone Long-Short Credit Income Fund’s current positioning should work out pretty well here. However, if rates are cut at all, the fund’s current 85% allocation to floating-rate credit will cause its investment income to decline.

However, it is possible that a severe enough recession will occur that causes the Federal Reserve to cut rates by much more than the 25-basis points that its members are currently projecting. In that case, we want to have exposure to traditional bonds, as traditional bonds should rise in price and their coupon payments do not decline. The fund does have this exposure, as 15.5% of its assets are invested in junk bonds, but this is not enough to cause this one to outperform a traditional junk bond fund. As such, investors who are concerned about falling interest rates may want to consider a fund like the Ares Dynamic Credit Allocation Fund, which has a more balanced portfolio between the two types of debt security. With that said though, the Blackstone Long-Short Credit Income Fund will still derive some benefit from falling interest rates due to the appreciation of those junk bonds, it is just not as much as it would otherwise be.

The fact that the Blackstone Long-Short Credit Income Fund can short-sell bonds gives it a bit of an advantage in rising interest rate environments as well. After all, traditional bonds fall when interest rates rise so shorting can provide the fund with the ability to take advantage of that. However, the fund currently has no short positions, which may be a good idea considering the uncertain direction of interest rates right now. The fact that it can do this could help it to boost its performance in a rising rate environment, however. That is something that could be attractive to long-term investors, as we have no real way of knowing what the future holds. The fact that the fund can short bonds could also provide it with the ability to take advantage of a rapidly rising increase in junk bond default rates . After all, shorting a junk bond which then goes into default is a pretty good way to make money.

In short, it appears that this fund is well-positioned for rising interest rates. The floating-rate securities should outperform traditional junk bonds in such an environment and the fact that it can short-sell securities adds to its ability to take advantage of any event that causes the price of all bonds or only specific bonds to decline. Unfortunately, the fund does not have as much exposure to traditional fixed-income bonds as some of its peers, so the Blackstone Long-Short Credit Income Fund could very easily underperform other funds during a period of falling interest rates.

Leverage

As is the case with most closed-end funds, the Blackstone Long-Short Credit Income Fund employs leverage as a method of boosting the effective yield of the assets that it receives from the investments in its portfolio. I explained how this works in a number of various articles. To paraphrase myself:

In short, the fund borrows money and then uses that borrowed money to purchase senior secured loans and junk bonds. As long as the yield that the fund receives from the purchased securities is higher than the interest rate that has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

It is important to note that the use of leverage to boost effective yields is not as effective today with rates at 6% as it was a few years ago when interest rates were effectively zero. This is because the difference between the rate at which the fund can borrow money and the yield that it receives from the purchased assets is much narrower than it once was.

The use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that a fund is not employing too much leverage because that would expose us to an excessive level of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Blackstone Long-Short Credit Income Fund has leveraged assets comprising 37.68% of its portfolio. This is certainly above the one-third level that we really want to see in order to ensure a reasonable balance between the risk and the reward. However, in this case, it is probably not a big problem. As we have already seen, the overwhelming majority of the assets in the fund’s portfolio are floating-rate securities that should have reasonably stable prices regardless of interest rates or just about anything else in the economy. As such, the volatility here is very low, which reduces the probability that this fund will encounter any real problems with its debt. Overall, we probably do not need to worry too much about the fund’s leverage at the current level, but we probably do not want it to get much higher.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Blackstone Long-Short Credit Income Fund is to provide its investors with a very high level of current income. In pursuance of this objective, the fund purchases a variety of floating-rate debt securities, which usually have a fairly large spread over the market interest rate due to the fact that these securities are typically backed by companies with below-investment-grade credit ratings. The fund collects the interest payments that it receives from these securities into a pool of money, and it then borrows money to purchase even more securities, using part of the money that it receives to cover the interest payments on the borrowed funds. That boosts its yield further. Finally, the fund pays out all of the money that it receives to its shareholders, net of its own expenses. We can expect that this would give the fund’s shares a very high yield.

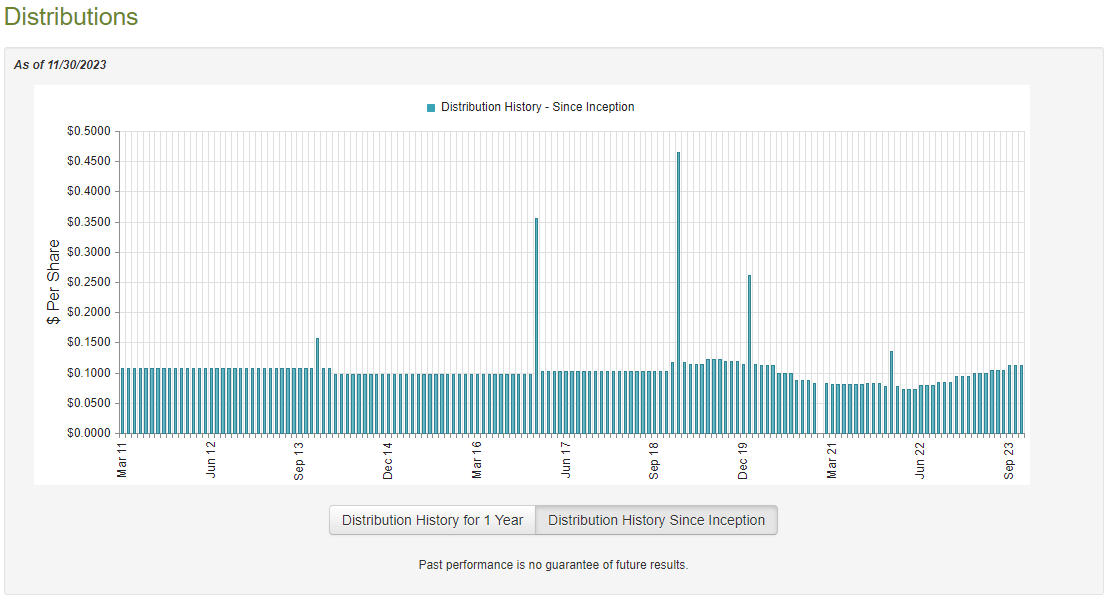

That is certainly the case, as the Blackstone Long-Short Credit Income Fund pays a monthly distribution of $0.1120 per share ($1.344 per share annually), which gives it an 11.83% yield at the current price. The fund’s long-term distribution history unfortunately leaves something to be desired though, as the fund has changed its payout quite often over its lifetime:

{kind=link}

As we can see, the fund’s distribution has been variable over most of the past five years, although prior to that it was reasonably stable. This is something that may prove to be a bit of a turn-off for those investors who are looking for a safe and secure source of income to use to pay their bills or finance their lifestyles. However, the fact that this fund has increased its distribution three times in the past twelve months helps to increase the appeal of its proposition. The fact that this fund has been increasing its distribution lately is certainly not surprising though, as most closed-end funds that have substantial exposure to floating-rate debt securities have been doing the exact same thing. This recent distribution growth helps in the face of inflation, which is a problem that we have all been suffering from recently.

As is always the case though, the fund’s history is not exactly the most important thing for new investors. After all, anyone purchasing the fund today will receive the current distribution at the current yield and will not be negatively impacted by the actions that the fund has had to take in the past. The most important thing right now is how well the fund can sustain its current distribution. Let us investigate this.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a relatively recent report that covers a very interesting period of time. As everyone reading this is certainly well aware, the first half of 2023 was characterized by a very euphoric market that widely expected interest rates to start coming down in the second half of 2023. While that has since been proven to be incorrect, there was still some potential to earn money by selling appreciated assets into a euphoric stock and bond market. This report should give us a good idea of how well the fund was able to take advantage of that situation, although I will admit that I am not especially optimistic about its capital gains prospects considering that this fund is mostly invested in floating-rate securities.

During the six-month period, the Blackstone Long-Short Credit Income Fund received $12,460,646 in interest from the assets in its portfolio. This fund does not receive income from any other source, so that figure represents the entirety of its investment income. It paid its expenses out of this amount, which left it with $8,032,147 available for shareholders. That was, fortunately, sufficient to pay the $7,510,590 that that fund paid out in total distributions. Thus, it appears that this fund is easily covering its distributions out of net investment income, which is exactly what we want to see from a fund like this.

The fund was also able to benefit from capital gains during the period, although not to the degree that we might really like to see. During the six-month period, the fund reported net realized losses of $6,111,164 but this was more than offset by $10,087,644 net unrealized gains. Overall, the fund’s net assets increased by $4,498,037 after accounting for all inflows and outflows.

This fund appears to simply be paying out its net investment income to the shareholders. That is a good sign, and it suggests that the fund should be able to sustain its current distributions as long as its net investment income remains around the current level. As long as short-term interest rates are at their current level, we should not have to worry about a distribution cut.

Valuation

As of November 30, 2023 (the most recent date for which data is currently available), the Blackstone Long-Short Credit Income Fund has a net asset value of $12.99 per share. The shares, however, only trade for $11.44 each. This gives the fund’s shares an 11.93% yield at the current market price. That is not as attractive as the 12.99% discount that the shares have had on average over the past month, so it is certainly possible that a better price could be obtained simply by waiting for a bit. However, a double-digit discount is generally representative of a reasonable entry price for any fund so there is probably no real reason to delay buying in if you wish to add this fund to your portfolio.

Conclusion

In conclusion, the Blackstone Long-Short Credit Income Fund is an interesting closed-end fund that is well positioned to take advantage of high rates going forward. The fund also has some positive exposure to declining interest rates, but it is admittedly not as good in that respect as some of its peers. The fund’s floating-rate exposure could cause its net investment income to decline rapidly next year if the Federal Reserve cuts interest rates as rapidly as the market expects, but at the moment that does not seem likely unless there is a severe recession in the near future. The fact that this fund can short-sell securities could give it some interesting potential for profits, but it is not currently exploiting that opportunity. Overall, the fund looks reasonably solid unless interest rates really do decline very rapidly next year.

For further details see:

BGX: Very Solid Income CEF Unless Interest Rates Rapidly Decline