BDJ - BGY: Diversified Global Exposure At A Discount

2023-07-31 23:03:48 ET

Summary

- BlackRock Enhanced International Dividend Trust offers global exposure and an options writing strategy, making it a potential diversifier relative to other funds.

- BGY's investment policy provides that they will overweight international investments and dividend-paying companies, which naturally lean towards larger market cap companies.

- The fund's current distribution works out to 7.41%, and thanks to the large discount on the fund, the NAV rate is materially lower.

Written by Nick Ackerman, co-produced by Stanford Chemist.

BlackRock Enhanced International Dividend Trust ( BGY ) carries some of the lowest U.S. exposure to diversified global funds that I've covered. Even with a closed-end fund that has a "global" focus, they can often carry 50% or more in U.S. exposure. That could set up BGY to be a bit more of a true diversifier in global positioning. The fund also has an options writing strategy without leverage, which is the case with most of BlackRock's equity CEFs. While the fund is trading at a deep discount, it could be worth considering.

The Basics

- 1-Year Z-score: -1.05

- Discount: -12.90%

- Distribution Yield: 7.41%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Assets: $636.5 million

- Structure: Perpetual

BGY's investment objective is "to provide current income and current gains, with a secondary objective of long-term capital appreciation." In an attempt to achieve the objective, "under normal circumstances, the Fund invests at least 80% of its net assets in dividend-paying equity securities issued by non-U.S. companies." They also have no reservations about what market cap they'll invest in but will tend to stick to larger cap companies. Naturally, these are going to be the companies paying dividends anyway.

The fund will then write call options on individual positions in the fund to both try to dampen volatility and generate gains for the fund's distribution. They target an overwrite of 30 to 40%, and their last fact sheet put the overwrite just over this upper range at 41.19%. Even more recently, at the end of May 31st, 2023, they listed that they were overwritten by 42.93%.

BGY Portfolio Overwritten (BlackRock (highlight from author))

{kind=link}

By being overwritten to a greater degree, it could indicate the management team is leaning more bearish. This would be because covered calls can cap upside potential and would indicate they don't anticipate strong upside potential from here on most of their portfolio.

As is usually the case for BlackRock CEFs, the fund's expense ratio is quite reasonable. With no leverage, we don't have to worry about any added costs with higher interest rates from the Fed.

Performance - Deep Discount

BGY has some similar sister funds, but there are also some differences to consider. They take a similar approach to investing, but instead, they have varying degrees of U.S. relative to global exposure. For example, BlackRock Enhanced Equity Dividend Trust ( BDJ ) is the mostly U.S. pure-play fund. Then, they also have the BlackRock Enhanced Global Dividend Trust ( BOE ). BOE is the most similar to BGY, but with more of a 50/50 split between U.S. and global positions.

In looking at the last decade's performance between these three funds, it's quite clear who the winner was. It was BDJ due to massive outperformance in U.S. equities during most of this period.

Ycharts

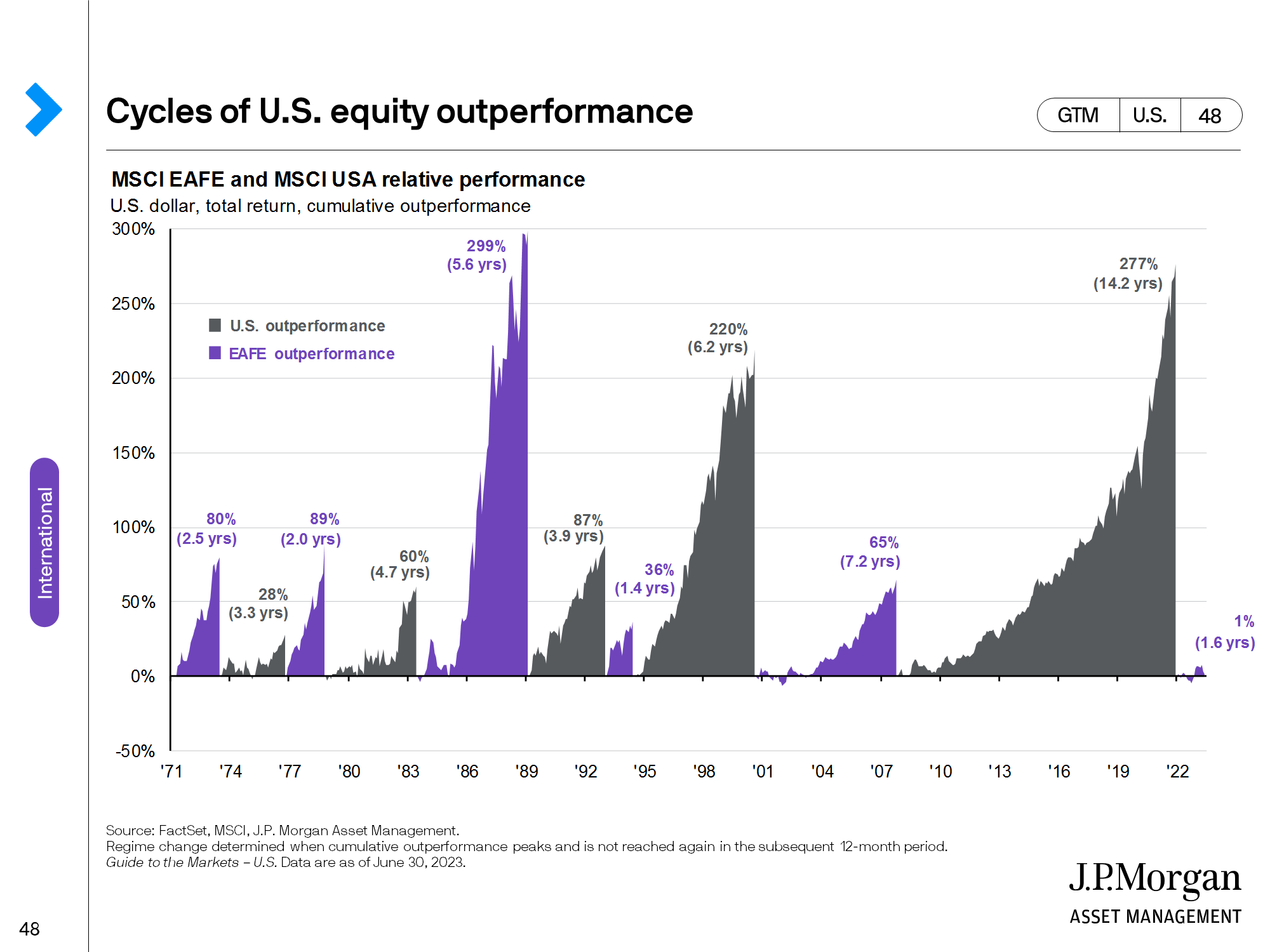

However, international markets aren't always the lagging area to invest. Historically, there have been periods when global investments would have paid off. In fact, more recently, global investments have been showing a glimmer of hope through some outperformance.

{kind=link}

Whether this continues or not is really anyone's guess. Relative valuations support the idea that international could continue to outperform, though, with global investments representing better valuations relative to the U.S. equity market.

It's also important to note that all three of these funds also emphasize positions in more value-oriented sectors rather than growth. That would have also limited their historical results relative to something like the S&P 500 Index. The S&P 500 Index has carried more growth-oriented tech exposure, and that weighting seems only to become more and more concentrated as the years go by.

I would also point out specifically for BGY that it launched in mid-2007. With hindsight, this fund was set up right in time to take the biggest plunge in most of our lifetimes. So the fact that the fund lost massive amounts right away isn't too surprising.

Looking at the NAV only shows us the destruction that happened during that time. We can see a better representation of the fund's performance on a total NAV return basis, which would include the distributions along the way. While they delivered meager results during this period, the distributions would have offset the losses for an individual if they invested right at inception and held the fund the entire time.

Ycharts

Making BOE more attractive at this time is the fund's deeper-than-usual discount. We've noted discounts have been widening for CEFs across the board, and BGY is another example of this happening.

Ycharts

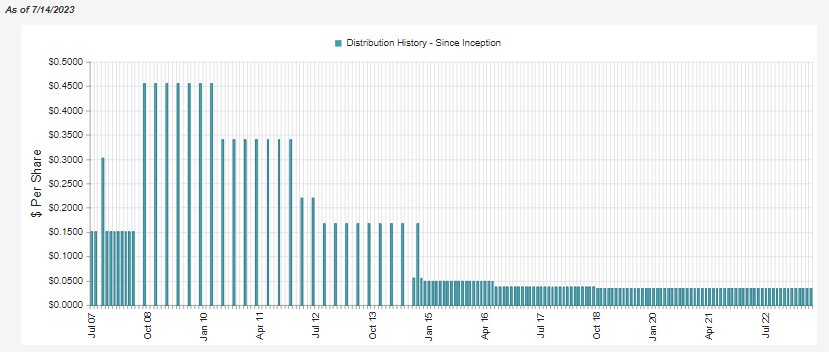

Distribution - Attractive Monthly Pay

The fund's current distribution works out to 7.41%. However, thanks to the large discount, the distribution rate on the NAV comes to a more modest 6.46%. For a period of time, around the GFC, they switched to a quarterly pay but are now back to paying monthly and have been doing so for a considerable period of their life.

Naturally, given the GFC and underperforming global exposure of the fund, they've had several cuts in their history. Though they've been able to maintain the current rate for a fairly lengthy period of time now. Given the reasonable NAV rate, I don't foresee this being cut, at least with what is known at this time.

{kind=link}

For BGY, the fund's net investment income coverage comes to around 25%. That isn't unusual for equity funds, as they will frequently rely on significant capital gains to fund their distributions. We can also see that they've been repurchasing shares in an effort to reduce the fund's discount.

{kind=link}

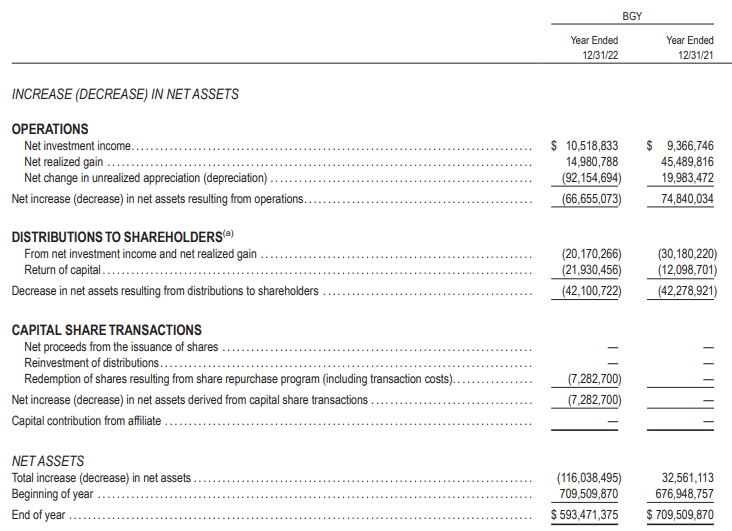

To generate capital gains, the fund doesn't only rely on appreciation from the underlying portfolio. This is where options writing can also help support the payout in the last fiscal year, which contributed to nearly $12 million in realized gains for the fund. Perhaps a small consolation given the substantial unrealized losses in the investments of the portfolio, but any positive contribution helps mitigate the damage.

BGY Realized/Unrealized Gains/Losses (BlackRock (highlight from author))

For tax purposes, the fund has classified the payout from various sources. The return of capital that we saw in 2022 would have been destructive ROC. However, for 2021, the fund's NAV had risen, which would suggest it was covered. We can even see in the above NII and realized gains were more than enough to cover the payout.

{kind=link}

This would appear to be the result of having capital loss carryforwards from 2020 that they could use to offset the realized gains. At the end of the last fiscal year, they didn't list any more carryforward losses, so ROC could be limited going forward depending on what they do in terms of portfolio moves through 2023. They could choose to sell their losers and keep their winners, which would result in generating more losses for this year that could potentially offset more gains.

Overall, a lack of consistency in the fund's distribution tax classifications can make it much more difficult for investors to choose a taxable or tax-sheltered account. An argument for both could be made as there can be significant ordinary income distributions, as was the case for 2021. Then 2022 would show that long-term capital gains and ROC benefits would be missed out on in a tax-sheltered account, as those two classifications dominated the breakdown.

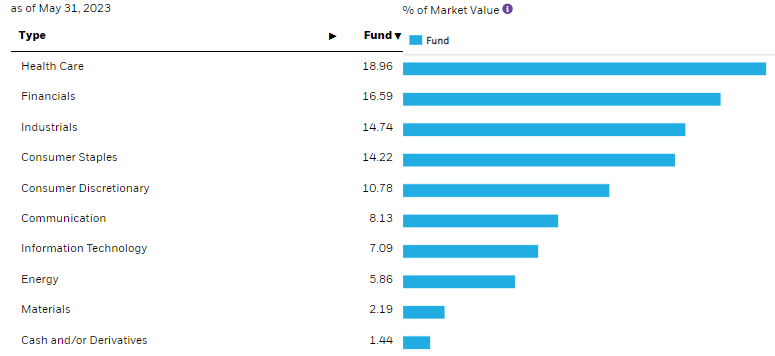

BGY's Portfolio

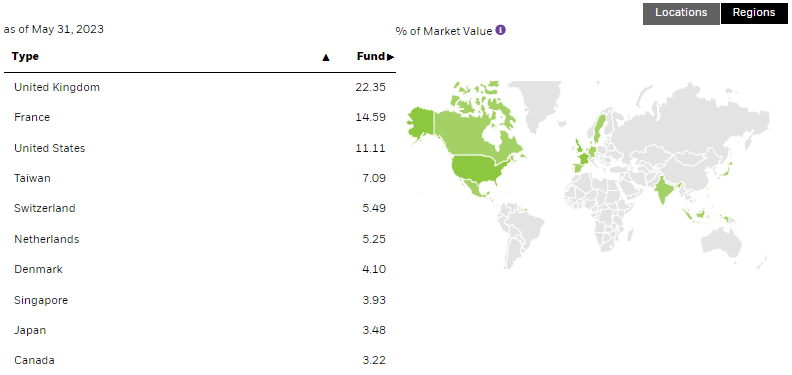

Despite having a target of at least 80% of investments outside the U.S., they do come up a bit short in this category. The last breakdown shows that they still have a weighting of 22.35% allocated to U.S. holdings. Still, as I mentioned at the open, this is quite a small amount relative to the other global diversified equity funds that I've covered.

{kind=link}

One of the reasons I own BDJ and BOE is that they don't carry overweight positions in tech. Instead, they have a value-oriented approach that favors healthcare and financials generally. For BGY, they've stuck with the same type of allocation. In fact, the fund underweights tech even more relative to its sister funds upon the last time I provided updates for both BDJ and BOE .

{kind=link}

With that being the case, it could help explain another reason for underperforming the other two on top of having a heavier weighting to companies outside the U.S. Being tilted towards the value-oriented sectors meant that the declines in 2022 were actually fairly muted relative to something like the S&P 500 Index. The options writing also would have helped dampen some of the losses too.

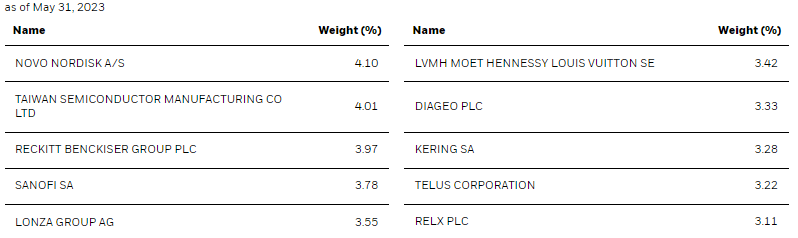

In the top ten, there are none of the mega-cap growth names that are frequent guests in other diversified CEFs. This is also consistent with being able to potentially be a better diversifier even if one already owns several diversified funds.

{kind=link}

The top ten represent nearly 36% of the portfolio. The fund overall carries 38 total positions. In that case, that takes away from some of the fund's diversification, at least relative to its sister funds.

BDJ carries 87 total positions, and BOE is at 53. The larger the global presence in the portfolio, the more limited the number of holdings seems to be the trend here. This isn't necessarily a negative, but it could indicate that the management team isn't that bullish on many companies outside the U.S. at the moment.

Conclusion

BGY delivers a more globally tilted portfolio than most diversified equity CEFs I'm familiar with. Investors could choose this fund to diversify their portfolios more while collecting a decent monthly distribution. The NAV rate of the payout seems to be reasonable, and I wouldn't believe that a cut for the foreseeable future would be required.

For further details see:

BGY: Diversified Global Exposure At A Discount