AZNCF - BGY: Going Global For Discounts

2023-11-08 17:56:47 ET

Summary

- BlackRock Enhanced International Dividend Trust provides exposure to international equities, with a focus on dividend-paying companies.

- BGY offers a discounted share price and is invested in discounted international markets, making it an appealing option for global diversification.

- The fund employs a covered call strategy to generate additional distribution coverage and has a distribution yield of around 8%.

Written by Nick Ackerman, co-produced by Stanford Chemist.

BlackRock Enhanced International Dividend Trust ( BGY ) provides investors with exposure to a meaningful amount of equities outside of the U.S. market. Most closed-end funds that are "global" often still carry 50%+ to the U.S. and, therefore, are primarily invested in the U.S. BGY is different as the U.S. isn't even the largest exposure of the fund.

The fund's discount on top of global equities being relatively cheaper than their U.S. peers provides an appealing time to consider bringing more global diversification into one's portfolio. Investing in global securities via BGY provides for a basket of securities that are actively managed by a team familiar with international companies.

Since our last update , the fund's discount has widened a touch. That put additional pressure on the shares during this time, right about when equities more broadly started to slide lower.

BGY Performance Since Prior Update (BlackRock)

The Basics

- 1-Year Z-score: -2.16.

- Discount: -14.80%.

- Distribution Yield: 8.19%.

- Expense Ratio: 1.08%.

- Leverage: N/A.

- Managed Assets: $583.4 million.

- Structure: Perpetual.

BGY's investment objective is "to provide current income and current gains, with a secondary objective of long-term capital appreciation." In an attempt to achieve the objective, "under normal circumstances, the Fund invests at least 80% of its net assets in dividend-paying equity securities issued by non-U.S. companies."

In addition to focusing on dividend-paying stocks, they also squeeze out a bit more 'income' through writing covered calls. The fund's latest overwritten percentage comes to 41.52%. That can take in more option premiums along with the dividends that they collect to pass on to investors.

The covered call strategy can work best in a flat or slightly down market as it can still provide some capital gains to fund the fund's distribution. The trade-off to this is that in a raging bull market, it can also limit the upside as it runs up against the strike prices selected. In those cases, they either have the shares called away for less than the current market price, or they can choose to close the trade for a loss. Additionally, the managers could roll the trade, which can result in either a gain or a loss.

They don't employ leverage in the form of borrowings, which I believe is positive during this higher-rate environment.

Discounts On Discounts

The first discount worth highlighting is the fund-level discount. That is, where BGY's share price is trading relative to its net asset value per share. Not only does BGY sport a deep discount, but the discount is large, even on a relative basis. The relative basis is perhaps more important, too, as it indicates whether a CEF is truly a good value or not.

YCharts

Across the board, CEF discounts have widened substantially. According to RiverNorth's data , CEFs have only traded at wider discounts 6% of the time since 1996. This is whether they are leveraged or not. That is the case for BGY; even with no borrowings, the fund is being punished just the same in this higher-rate environment.

Additionally, BGY's focus on international investments puts it in a position where it is investing in discounted international investments. At least, relatively speaking, international markets are displaying much better relative valuations than their U.S. peers.

China, Europe, and Japan are all trading at not only relatively cheaper earnings multiples but below their 25-year averages and nearer to the low end of their 25-year average range. On the flip side, U.S. equities have come down in valuation from where they were near the higher end of the 25-year average range but are still trading above the average.

Global Valuations (JPMorgan)

This data is provided by the 4Q 2023 JPMorgan "Guide to the Markets" with data as of October 30, 2023.

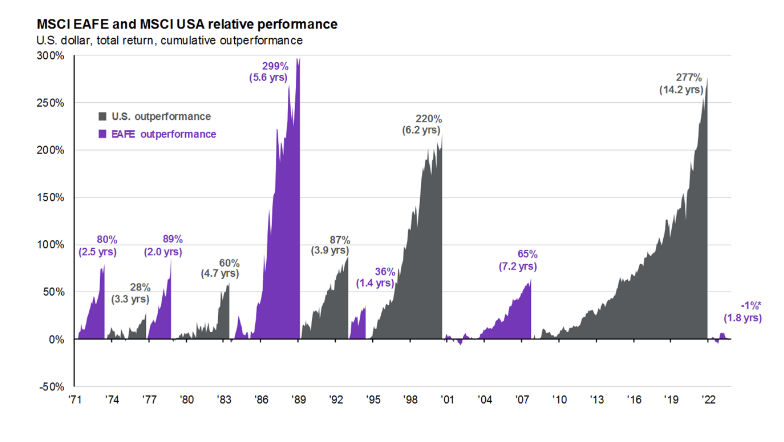

For most investors, in particular, those who may have started investing during or around the Global Financial Crisis, it could be easy to say that the discount is appropriate. The argument would be that the U.S. market 'always' outperforms. And for most of those investors' lives, that would be true. However, international investments and U.S. investments have historically taken turns in terms of outperforming each other.

{kind=link}

That doesn't mean that the U.S. won't keep outperforming, but if valuations start to matter, that could be the catalyst to see international take the lead. That could come as the result of the U.S. market staying flat and international equities catching up in terms of earnings multiples.

Collecting An ~8% Distribution Yield

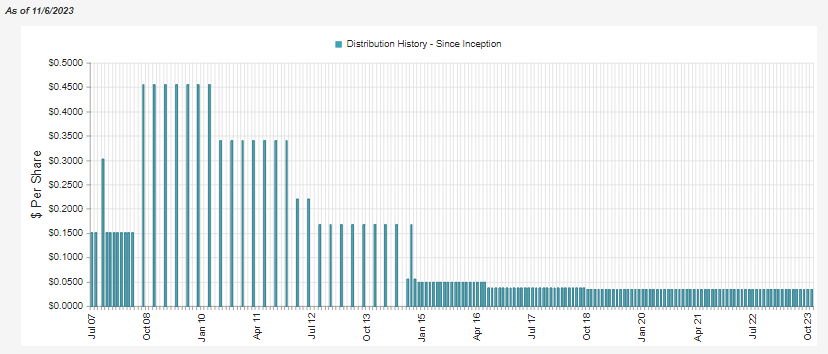

BGY has several distribution cuts in its history, and that isn't too surprising as this is a pretty familiar pattern from international CEF peers. It goes back to once again the fact that U.S. equities had dominated their global counterparts for well over the last decade.

{kind=link}

At the same time, the international-focused funds paid the same distribution rate as their U.S. counterparts. As equities in the U.S. have become weaker over the last two years - outside of the mega-cap tech names that have driven much of 2023's results - we are starting to see cuts from equity funds. This is a move to right-size their payouts as capital gains started to dry up.

BGY is no different from any other equity fund, and that means they require capital gains to fund their distribution. Thanks to a large discount, investors are receiving an 8%+ distribution rate from a portfolio that has to earn 6.98% to achieve it.

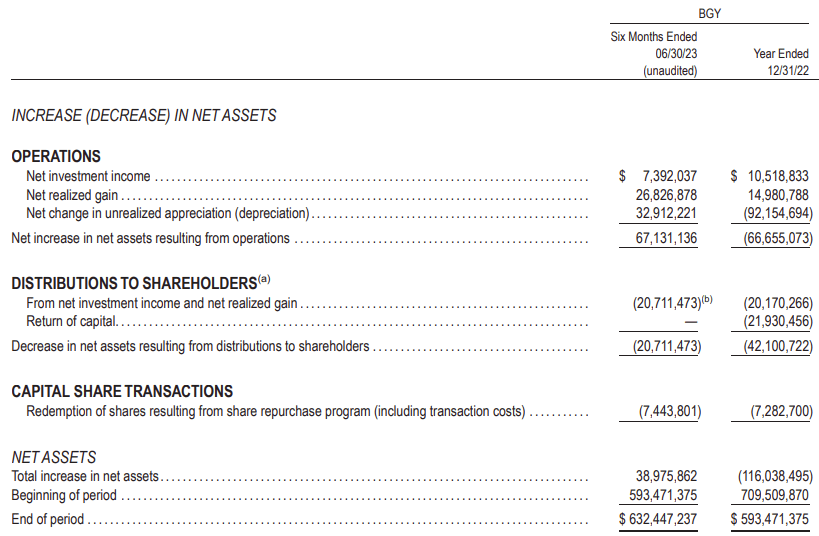

Since BGY focuses on dividend payers, that has helped the fund's net investment income coverage a bit, NII coverage came in at 35.7% in the first six months of the year. That is up quite a bit from last year, which is another encouraging trend if that can continue. The fund also realized a significant amount of capital gains that put it well over covering the distribution for the first half of the year.

{kind=link}

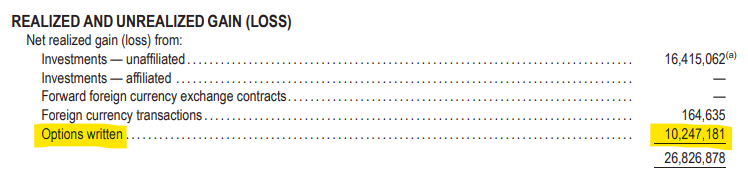

A meaningful portion of those realized gains actually came in the form of option premiums as well, which can highlight the benefit of writing covered calls. Between the NII and option writing gains, the fund's distribution was just about covered, and those are two sources that can provide fairly regular cash flows.

{kind=link}

Since this report, the second half of the year has been more challenging. That had seen the unrealized losses side of the equation rise materially and drive down the total returns of the fund. Still, with a fairly reasonable distribution rate on the NAV currently, I wouldn't suspect they would cut at this time.

For tax purposes, we discussed that in our previous update. Here's a recap:

For tax purposes, the fund has classified the payout from various sources. The return of capital that we saw in 2022 would have been destructive ROC. However, for 2021, the fund's NAV had risen, which would suggest it was covered. We can even see in the above NII and realized gains were more than enough to cover the payout.

This would appear to be the result of having capital loss carryforwards from 2020 that they could use to offset the realized gains. At the end of the last fiscal year, they didn't list any more carryforward losses, so ROC could be limited going forward depending on what they do in terms of portfolio moves through 2023. They could choose to sell their losers and keep their winners, which would result in generating more losses for this year that could potentially offset more gains.

{kind=link}

BGY's Portfolio

The portfolio has a fair bit of turnover, with the last six-month period showing a rate of 26%. That puts it on pace to have more buying and selling activity compared to last year's 41% but below the 71% turnover seen in 2021.

With that said, there can be a fair bit of changes in the portfolio between updates. In the geographic allocation, there have been some fairly meaningful shifts since our last update that showed the data as of May 31, 2023. The U.K. exposure remains the highest exposure of the fund, but that has come down from the 22.35% allocation previously.

BGY Geographic Exposure (BlackRock)

Additionally, France was the second largest weighting at 14.59%, and that has now sunk to below the U.S. exposure that was previously 11.11%. This means we saw a small bump in the U.S. exposure that BGY is carrying, but it still remains well below the level we see in other international funds.

We've also seen a material increase in exposure to Japan. On an absolute basis, it isn't the most noteworthy, but on a relative basis, the exposure climbed materially from the 3.48% allocation it was at previously.

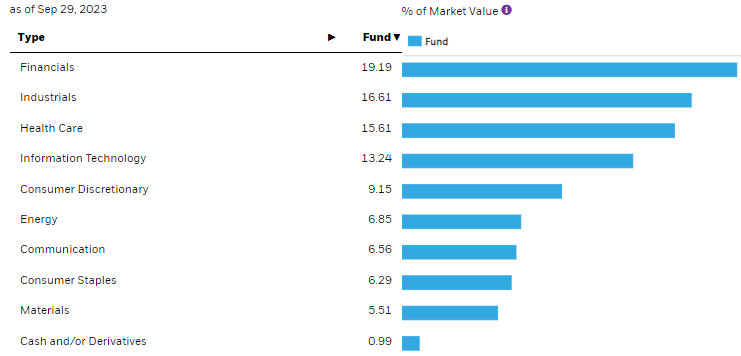

The fund has also shifted its sector exposure. They continue to focus on a more value-oriented portfolio but have pushed up financials to the largest weighting of the fund. It came from the combination of increasing financial exposure from 16.59% but also taking down healthcare exposure, where it previously stood at 18.96%.

{kind=link}

Industrial exposure also shifted higher from 14.74%, while consumer staples saw a drop from the 14.22% weighting it was previously to being one of the smaller allocations of the fund. That seemed to be driven, in part, by the tech allocation climbing from the 7.09% it was at previously.

So, the fund has seen its value-oriented tilt remain the largest allocation due to carrying financial, industrial, and healthcare exposure. However, they've been shuffled a bit, and tech saw a small bump. Perhaps no coincidence either, as the tech sector during the time of these updates had outperformed. It produced a negative return as a whole for the sector, but that was still better than consumer staples, which were hit particularly hard through this period.

YCharts

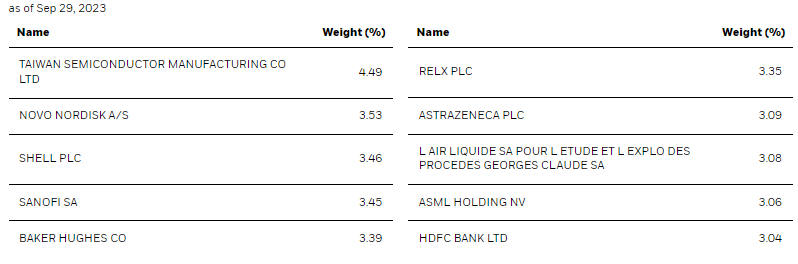

Turning to the fund's top ten holdings, here we see a few familiar names that we saw in the last update. Though there were quite a few new names making their way to the top ten holdings. That being said, with similar weightings amongst equities toward the top, it only takes some fairly small gyrations to see names come in and out of the top ten. BGY only carries around 40 positions, so overall, the fund is concentrated when compared to peers.

{kind=link}

Taiwan Semiconductor Manufacturing Company Limited ( TSM ) has seen its allocation climb a touch, and that was good enough to slide into the top spot. That overtook Novo Nordisk A/S ( NVO ). This is a reflection of at least some of the reasons why we would have seen tech exposure climb while healthcare exposure sink for the fund during this period.

Shell plc ( SHEL ), Baker Hughes Company ( BKR ), and AstraZeneca PLC ( AZN ) are just a few 'new' names to make it to the top ten. However, these were names already present in the fund earlier in the year , meaning they aren't exactly new names to the portfolio.

Conclusion

BGY can diversify one's portfolio to international investments. Global equities are cheaper right now than their U.S. counterparts, and history has shown that the U.S. doesn't always outperform, despite what it probably feels like for most investors. BGY provides exposure to these cheaper international markets as a 'truly' diversified global fund as it doesn't overweight U.S. exposure like most other global CEFs. Combining the discount at the fund level and the discount on international investments continues to make BGY an interesting bet at this time.

For further details see:

BGY: Going Global For Discounts