BHK - BHK: 2 Years Of Declining NAV Spells Trouble For The Distribution

2023-03-17 15:51:57 ET

Summary

- Investors are in desperate need of additional income to maintain their standard of living in today's environment of high inflation.

- BlackRock Core Bond Trust invests in a bond portfolio and applies leverage to boost the overall yield of the portfolio.

- The bond market is likely to be under pressure for a while, so this closed-end fund may continue to have trouble providing capital gains.

- The fund's assets have been declining for two years, which presents very serious concerns about its ability to sustain the distribution.

- The fund is trading at a discount, but it is not large enough to compensate for the risks to the distribution.

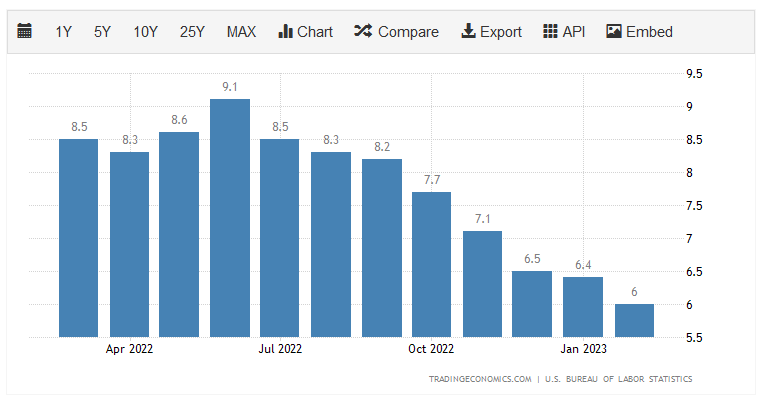

It is without a doubt that one of the biggest challenges facing the average American recently has been the incredibly high inflation that has dominated the economy for the past eighteen months. Unfortunately, this inflation does not appear to be going away anytime soon, as the latest CPI report from the Bureau of Labor Statistics showed that inflation increased by 0.4% month-over-month and 6% year-over-year in February. There has now not been a single month over the past year in which the annual inflation rate came in under 6%:

{kind=link}

Two of the areas that have seen the greatest increase in prices have been food and energy, which are both necessities. As this has been going on for quite a while now, the budgets of many people are getting strained, and they are taking on second jobs or entering the gig economy in order to get the extra money that they need just to keep their bills paid or their bellies full. The fact that so many people are taking on additional work is probably one reason why the jobs market remains so strong, despite the massive layoffs that have been seen throughout the economy. I discussed this in two recent blog posts (see here and here ). The point of all this is that Americans are desperate for income just to tread water in today's economy.

As the areas that have been seeing rapidly rising prices are necessities, it is likely that many of you reading this are also feeling a bit more financially stretched than you were a few years ago. The fact that the market has dropped has only exacerbated this problem. Fortunately, as investors, we can put our money to work for us in order to generate additional income. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are not really well-followed by the investment media or indeed by most investors, which is a shame because they provide an easy way to obtain a diversified portfolio of assets that can usually deliver a higher yield than pretty much anything else in the market.

In this article, we will discuss the BlackRock Core Bond Trust ( BHK ), which is one fund that investors can use to generate a high level of income. This is evident in the fact that the fund yields 8.52% as of the time of writing, which is certainly enough to satisfy most people that are searching for income today. I have discussed this fund before, but a few months have passed since then, so naturally, some things have changed. In particular, the fund released its 2022 annual report so we will be sure to take a look at that in this article.

About The Fund

According to the fund's webpage , the BlackRock Core Bond Trust has the stated objective of providing its investors with a high level of current income and capital appreciation. The focus on current income is not at all surprising, considering that the name of the fund implies that it is a bond fund. A look at the portfolio confirms it, as the fund is almost entirely invested in bonds with a very small preferred stock allocation:

CEF Connect

The fact that the fund focuses on current income should not be surprising in this light because bonds deliver the overwhelming majority of their return in the form of direct payments to investors. Their potential for capital gains is quite limited, which is why this fund stating that capital appreciation is one of its goals is quite confusing. The reason why bonds do not have much potential for capital gains is that they have no inherent link with the growth and prosperity of the issuing company. After all, a company does not increase the amount that it pays its creditors just because its income increased in a given period of time. In addition to this, bonds always pay their face value at maturity, so over the long term they cannot inherently deliver capital gains.

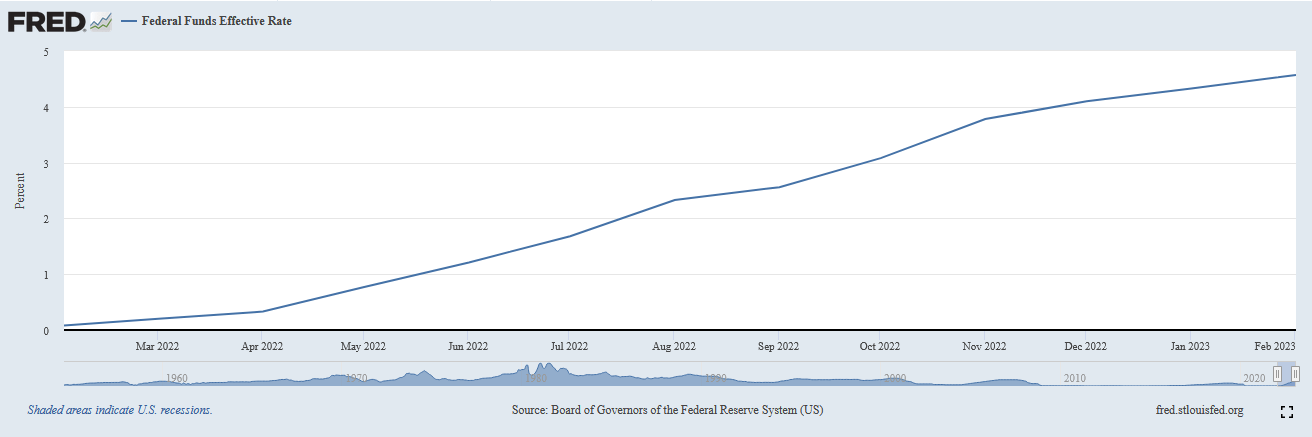

With that said, bond prices do fluctuate with interest rates. It is an inverse relationship, so in most cases, rising interest rates cause bond prices to decline and vice versa. The reason for this is that newly-issued bonds will have a yield that correlates to the current interest rate in the market. In a rising rate environment, this will cause brand-new bonds to have a higher yield than already existing and outstanding bonds. Nobody will purchase an existing bond with a lower yield than an otherwise identical brand-new bond so the price of the existing bond must decline so that it delivers the same yield-to-maturity as an identical newly-issued bond. This is very important today because, as everyone reading this is no doubt aware, the Federal Reserve has been raising its benchmark federal funds rate in order to combat the high inflation in the economy. These rate hikes have been quite aggressive over the past year, as the federal funds rate was 0.08% in February 2022 but stands at 4.57% today:

{kind=link}

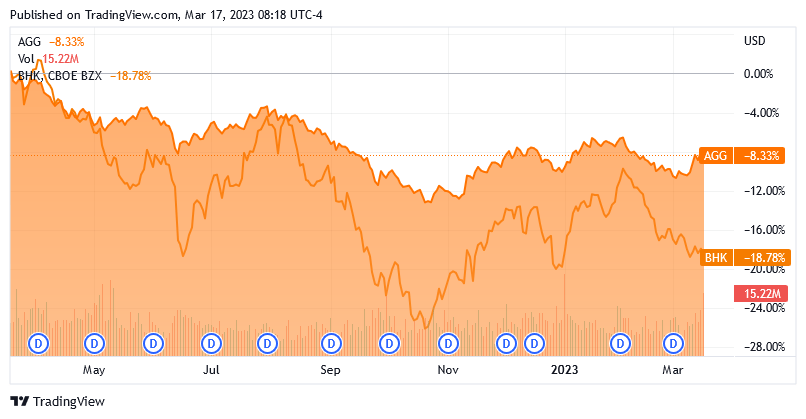

This is the biggest reason why bond prices have declined over the past year. Indeed, the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 8.33% over the trailing twelve-month period as of the time of writing. The BlackRock Core Bond Trust has certainly not been spared from this carnage, as it is down 16.78% over the same period:

{kind=link}

Although the BlackRock Core Bond Trust closed-end fund does have a much higher yield than the index, it was not enough to close the gap between the two funds. Overall, the index fund delivered a higher total return over the period, but both funds handed their investors losses. While the recent trouble in the banking sector could mean that we are close to the peak of the rate hiking cycle and that the worst is likely to be behind us, the Federal Reserve is currently expected to keep raising rates until at least the middle of the year because inflation has yet to cool down to an acceptable level. Anyone purchasing a bond fund, including the BlackRock Core Bond Trust, will likely see the value of their investment decline for at least the next few months.

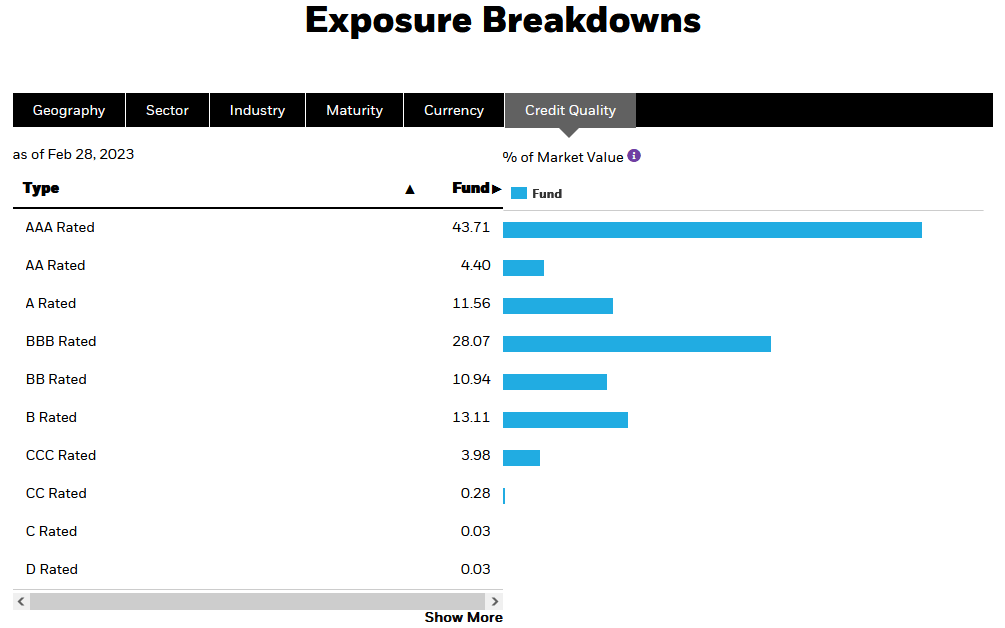

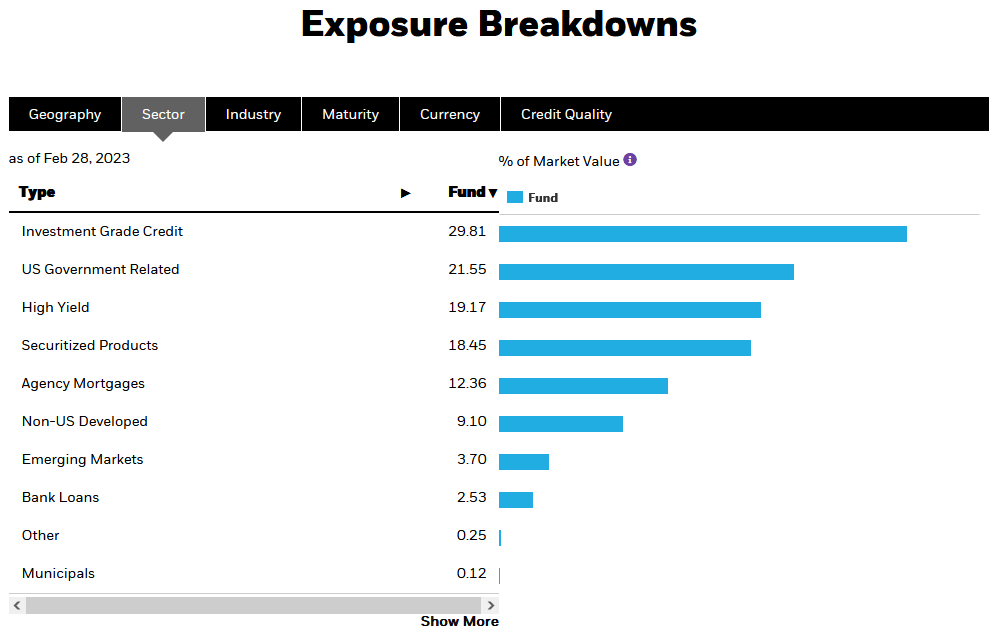

One of the things that we frequently see with closed-end bond funds is substantial exposure to speculative-grade bonds. This is because junk bonds tend to offer higher yields than investment-grade securities. However, that may also be concerning to risk-averse investors because of the higher default risk. The BlackRock Core Bond Trust could be a comforting pick for those concerned about this since its portfolio consists mostly of investment-grade bonds:

{kind=link}

An investment-grade bond is anything rated BBB or above by the major credit rating agencies. As we can clearly see, that is 87.74% of the bonds in the portfolio. The remainder of the portfolio consists of junk bonds, but the allocation to these is small enough that we can almost ignore it. There are very few AAA-rated entities in the market apart from certain sovereign governments, so as might be expected, a substantial proportion of the fund's holdings are U.S. government bonds:

{kind=link}

This will undoubtedly add to the fund's appeal among those investors that are concerned about the loss of principal to defaults. After all, the United States government is widely perceived as being completely free of default risk. There is even an argument that can be made that the government cannot default due to a clause in the Fourteenth Amendment of the U.S. Constitution. This risk-free situation only applies if the fund chooses to hold the bonds to maturity, though. After all, the "toxic assets" that caused the losses that ultimately resulted in a run against Silicon Valley Bank were U.S. Treasury securities.

BlackRock Core Bond Trust appears to rarely hold securities to maturity, however. The fund had an annual turnover of 104.00% in 2022, which implies that it did a great deal of trading. In fact, that is one of the highest turnovers that I have ever seen for a fixed-income fund. The reason that this is important is that it costs money to trade bonds or other assets, and these costs are billed to the fund's shareholders. That creates a drag on the portfolio's performance. After all, the fund's management has to generate sufficiently high returns to overcome these expenses as well as produce a return that satisfies the investors. This is a very difficult task to achieve, and few management teams accomplish it consistently. That is one reason why actively-managed funds tend to underperform their benchmark indices. As we have already seen, this one did underperform the U.S. bond index over the past twelve months, so it is not an exception to this rule.

Leverage

In the introduction, I noted that closed-end funds like the BlackRock Core Bond Trust have the ability to earn a higher yield than any of the underlying assets actually possess. One strategy through which this is accomplished is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase bonds. As long as the purchased assets have a higher yield than the interest rate that must be paid on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. This could therefore be one reason why the fund has underperformed its index over the past year. As such, we need to ensure that the fund is not using too much leverage since that would expose us to too much risk. As a general rule, I do not like to see a fund's leverage above a third as a percentage of its assets for this reason. Unfortunately, the BlackRock Core Bond Trust is not currently fulfilling this requirement. As of the time of writing, the fund's levered assets comprise 39.44% of the portfolio, so it is using more leverage than we really like to see and could therefore be exposing us to an excessive amount of risk. However, the fund is mostly invested in reasonably safe securities so this is not as big of a concern as it would be if it were using its borrowed monies to purchase shares of start-up companies with no revenue. Still, I wish this fund were somewhat less levered given the fact that it was U.S. Treasury bonds declining in value that caused havoc in the banking system over the past week.

Distribution Analysis

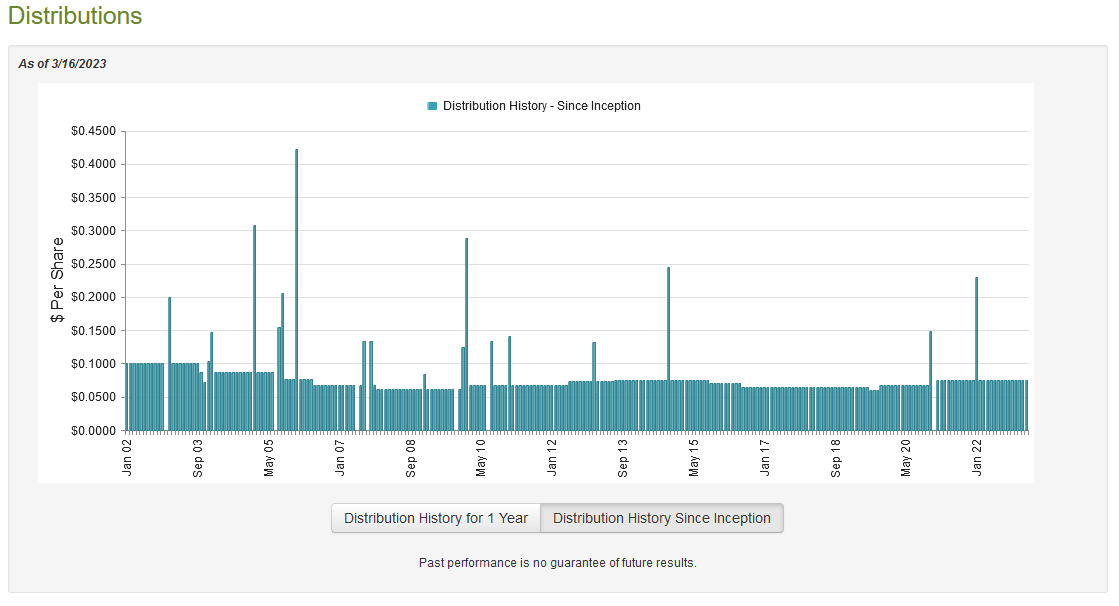

As stated earlier in this article, the primary objective of the BlackRock Core Bond Trust is to provide its investors with a high level of current income. In order to accomplish that goal, the fund invests in a portfolio of bonds and then applies a layer of leverage to boost the effective yield of the portfolio. As bonds are currently paying higher yields than they have in a decade, we can assume that this strategy would probably allow the fund to have a reasonably high current yield. That is certainly the case as the BlackRock Core Bond Trust currently pays a monthly distribution of $0.0746 per share ($0.8952 per share annually), which gives it an 8.52% yield at the current stock price. The fund has, unfortunately, not been particularly consistent about this distribution over the years and it has varied quite a bit over time:

{kind=link}

This variation in the fund's distribution is likely to reduce its appeal somewhat in the minds of those investors that are seeking a stable and consistent source of income to use their bills or finance their lifestyles. However, it is not out of the ordinary for bond funds to vary their yields over time as fluctuations in interest rates can have a significant impact on the fund's ability to generate income and it is not sustainable for a fund to pay out more money than it can earn. The fund has been very consistent about its distribution since December 2020 though, despite the fact that interest rates have increased a lot since then. That may be somewhat comforting for investors. It is also important to remember that anyone purchasing the fund today will receive the current distribution at the current yield, so the fund's past performance is not nearly as important as its future performance for anyone purchasing the shares now. As such, let us have a look at the fund's finances and attempt to determine how sustainable its distribution is likely to be.

Fortunately, we have a very recent document that we can consult for that purpose. The fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. This is a much more recent report than we had available the last time that we discussed this fund, and it should give us a better idea of how well the fund performed during the second half of 2022. This is quite nice since 2022 was a very turbulent year for the bond market in general, as we already discussed. During the full-year period, the BlackRock Core Bond Trust received a total of $416,151 in dividends and $47,338,779 in interest from the assets in its portfolio. This gives the fund a total investment income of $47,754,930 over the period. It paid its expenses out of this amount, leaving it with $34,621,610 available for shareholders. That was, unfortunately, not nearly enough to cover the $44,321,199 that the fund actually paid out in distributions over the year. This is likely to be somewhat concerning as the fund's net investment income was insufficient to cover the distribution.

With that said, the fund does have other methods through which it can obtain the money that it needs to compensate the shareholders. For example, it might have been able to earn capital gains that can be paid out. As might be expected considering the turbulence in the market though, the fund generally failed at this task over the year. It reported net realized losses of $58,306,032 and posted net unrealized losses of $179,504,308 during the period. Overall, the fund's assets declined by $247,242,455 after accounting for all inflows and outflows. That is certainly concerning as the fund clearly failed to cover its distribution. This is not an isolated incident either as the fund's assets also declined by $51,656,041 during the full-year 2021 period. This is not sustainable, and the fund is clearly distributing more money than it can afford. It would not be at all surprising if the fund cuts its distribution in the near future.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Core Bond Trust, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. That is, fortunately, the case with this fund today. As of March 16, 2023 (the most recent date for which data is available as of the time of writing), the BlackRock Core Bond Trust had a net asset value of $11.01 per share but the shares currently trade for $10.62 each. That gives the fund a 3.54% discount to net asset value at the current price. While that is better than the 1.27% discount that the shares have had on average over the past month, it still seems a bit too expensive considering that the fund will probably have to cut the distribution and take a hit to its market price in the near future. Unless the fund can be acquired at a much larger discount, it is probably best to stay on the sidelines.

Conclusion

In conclusion, the past year has not been particularly good for bond funds, and it probably will not improve in the near term despite the recent problems in the banking sector. This is a disappointment because investors need income today and bond funds are one of the easiest ways to get that income. The BlackRock Core Bond Trust appears to have a reasonable portfolio and it is one of the few closed-end funds that invest mostly in investment-grade debt, but the fund appears to be over-distributing and may be forced to cut the payout in the near future. For that reason, the current discount is not large enough to justify purchasing BlackRock Core Bond Trust today.

For further details see:

BHK: 2 Years Of Declining NAV Spells Trouble For The Distribution