BHK - BHK: Declining Assets And Market Seems Overly Optimistic

2023-07-03 08:42:04 ET

Summary

- Investors are in desperate need of income to maintain their standard of living in the current environment.

- BHK invests in a portfolio of reasonably safe bonds to provide a nice level of income for investors.

- The market appears to be betting on near-term rate cuts, which directly contradicts the Fed's statements.

- The fund's assets have declined for two years in a row and it will almost certainly need to cut its distribution.

- The fund is trading at a slight discount to the net asset value.

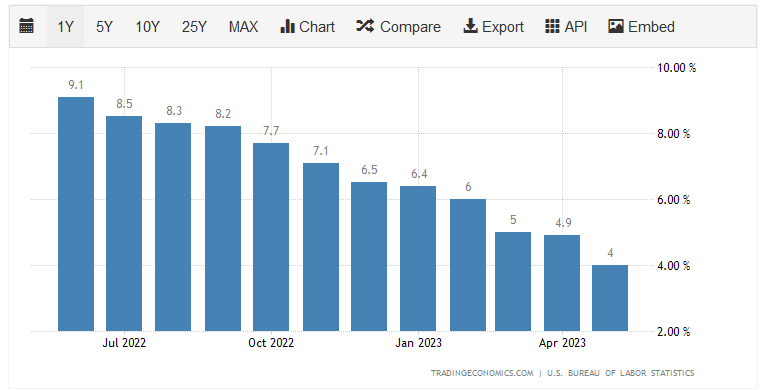

There can be little doubt that one of the biggest challenges facing the average American household today is the incredibly high inflation rate that dominates the economy. This rapidly rising cost of living is illustrated in the consumer price index, which claims to measure the cost of a basket of goods that is regularly purchased by an average household. As we can see here, the inflation rate has exceeded the 2% year-over-year growth rate that is considered healthy during each of the past twelve months:

{kind=link}

As I pointed out in various previous articles though, such as this one , the improvements that we see here recently are somewhat misleading because they are entirely caused by crude oil prices being lower in 2023 than they were in the corresponding month of 2022. The core consumer price index, which excludes volatile food and energy prices, shows much higher year-over-year growth and has barely dropped at all despite the Federal Reserve actively trying to combat inflation. The reasons for this are that interest rates are still far too low (the Taylor rule says that the federal funds rate needs to be set at 7.75% and kept there to get inflation down) and the government's rising spending. Regardless, the point here is that real wage growth has been negative for 26 straight months, which clearly indicates that people need to obtain additional sources of income just to maintain their lifestyles.

As investors, we are certainly not immune to this. After all, we have bills to pay and desire a certain amount of luxury and enjoyment in our lives. Fortunately, we have some options as to how we obtain the extra money that we need to sustain our desired lifestyles in an environment of rapidly rising prices. One of the best ways to accomplish this is to put our money to work for us and purchase shares of a closed-end fund that specializes in the generation of income. These funds are unfortunately not very well followed by the financial media and most financial advisors are not familiar with them. This is a shame because these funds have a few advantages over open-ended and exchange-traded funds. In particular, they are able to employ certain strategies that have the effect of boosting their yields well beyond anything else in the market and even beyond that of the underlying assets.

In this article, we will discuss the BlackRock Core Bond Trust ( BHK ) that currently yields an impressive 8.41% at today's price. That is certainly a high enough yield to turn the attention of anyone that is seeking to earn a high level of income from their portfolio assets. I have discussed this fund before, but that was a few months ago so a few things have changed. In particular, the Federal Reserve has apparently slowed up a bit on its monetary tightening regime, which should reduce some of the problems that bond funds have faced over most of the past year. This article will focus on this and other updates to our overall thesis but the biggest concern here is that the fund has failed to cover its distribution for two years.

About The Fund

According to the fund's webpage , the BlackRock Core Bond Trust has the stated objective of providing its investors with a high level of current income and capital appreciation. This is a rather unsurprising objective, particularly the current income component. This is because, as the name implies, this is a bond fund that has all of its assets invested in bonds with only a very small allocation to preferred stock:

CEF Connect

Bonds provide their investment return primarily in the form of direct payments to the investors. In fact, this is going to be the only return delivered over the life of the bond. This comes from the fact that an investor purchases a bond for its face value at issuance, receives regular payments from its issuer over the life of the bond, and then receives the face value back when the bond matures. A bond has no inherent link to the growth and prosperity of the issuing entity, so there is no in-built capital gains potential.

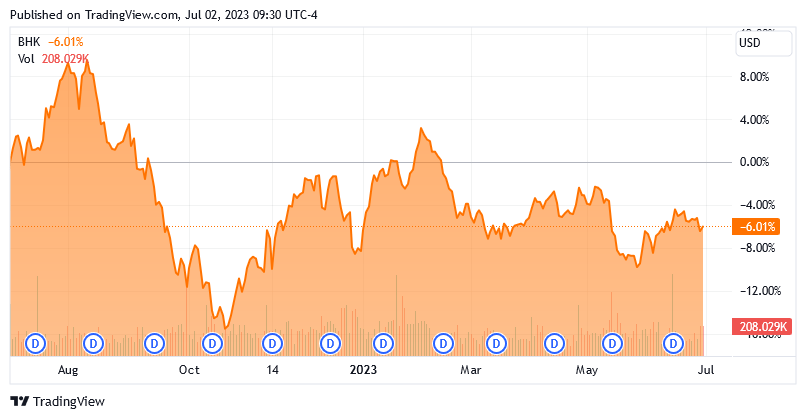

With that said, the market price of bonds does vary over their lifetimes based on interest rates and a few other factors. This makes it possible to achieve capital gains by buying and selling bonds prior to their maturity date. Indeed, this was one of the only ways to make money off bonds over the past decade due to the incredibly low-interest rate environment in pretty much all developed nations. The relationship between bond prices and interest rates is inverse, so when interest rates go up, bond prices go down. This has been the case for most of the past year as the Federal Reserve has hiked the federal funds rate from 0% in February 2022 to 5.00% today. This has had a devastating effect on bond funds like the BlackRock Core Bond Trust. As we can see here, over the past year the fund is down 6.01%:

{kind=link}

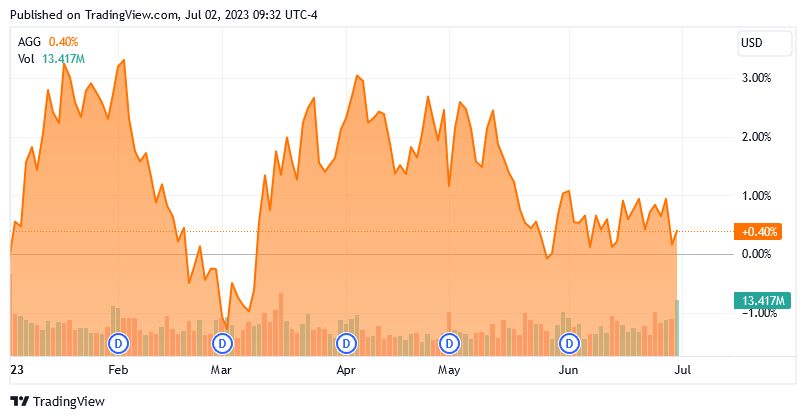

This negative trend is unlikely to reverse in the near term. Although the Federal Reserve did not raise the benchmark federal funds rate in June, it did strongly imply that there would likely be two more rate hikes later this year. However, the market seems to be pricing in a rate cut. The Bloomberg U.S. Aggregate Bond Index ( AGG ) is actually up 0.40% year-to-date:

{kind=link}

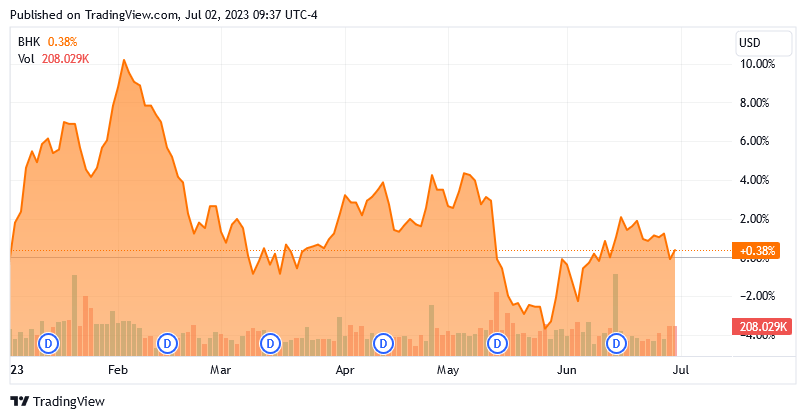

This makes absolutely no sense unless the market is expecting a rally in bonds, which should only happen if the Federal Reserve cuts rates. Thus, it appears that the market is overly optimistic based on the comments from the Federal Reserve officials. This optimism has actually spilled over into this fund too, as the BlackRock Core Bond Trust is up 0.38% year-to-date:

{kind=link}

Thus, if the Federal Reserve does indeed show some backbone and holds to its own statements, we could see a reversal in the fund's share price during the second half of the year.

The fact that BlackRock Core Bond Trust is up almost as much as the index has been a boon to investors in the fund. As this fund has a much higher yield than the index, it has given a much higher total return than the index over the same period. This is particularly so if one was reinvesting the dividends due to the effects of compounding. This could also offset some of the potential risks here should the bond market's optimism over the direction of interest rates prove to be wrong.

One of the advantages that the closed-end fund has over the bond index is that it is actively managed. As such, the fund's managers are able to sell overpriced bonds and use the proceeds to buy bonds issued by companies in out-of-favor sectors. This could reduce the risk of losses in the event of a bond market correction. Unfortunately, it also results in higher expenses. After all, it costs money to trade bonds or other assets, and these expenses are billed directly to the fund's shareholders. This creates a drag on the fund's performance and makes management's job more difficult. After all, the fund's managers need to earn a sufficiently high return to cover the added expenses and still have enough money left over to provide the shareholders with an acceptable rate of return. This fund's 104% annual turnover is incredibly high for a fixed-income fund, which indicates that it is almost certainly incurring heavy costs due to its trading activity. However, it has outperformed the index year-to-date so we can excuse this.

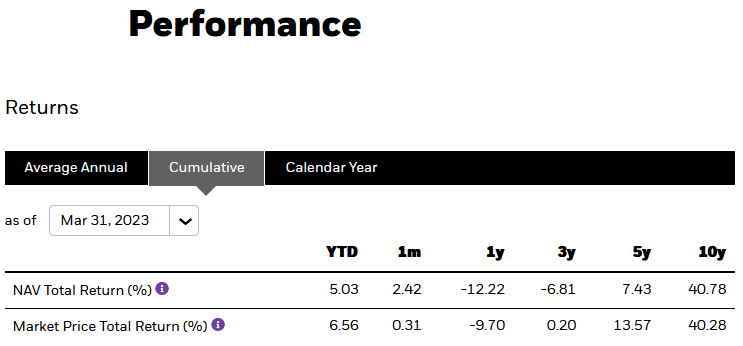

As I have noted in past articles on closed-end funds though, it is not uncommon for the market price performance of these funds to differ from the performance of the actual portfolio. While this can frequently provide opportunities for investors to acquire shares for less than they are actually worth, it is also problematic when we want to determine the performance of the fund's actual portfolio. As of the time of writing, the fund has only provided year-to-date information about its portfolio's performance through March:

{kind=link}

As we can see, the fund's portfolio delivered a 5.03% total return in the first three months of the year. That was a lot better than the 2.96% total return delivered by the bond index over the same period, which speaks well for this fund. However, we do not have any more recent data than this regarding the fund's performance based on net asset value and this information is a few months old at this point.

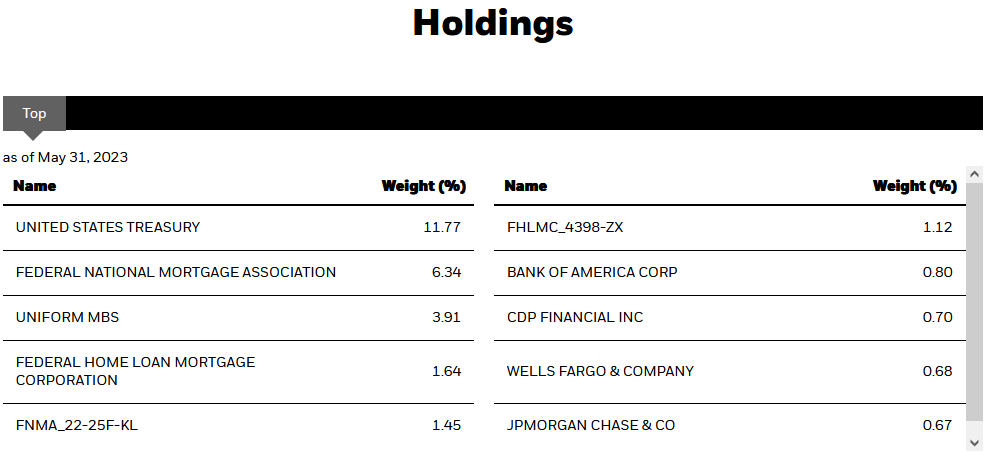

Unlike many other bond closed-end funds such as the BlackRock Corporate High Yield Fund ( HYT ), the BlackRock Core Bond Trust invests in investment-grade securities. In fact, its largest holdings are U.S. Treasuries and mortgage-backed securities issued by Fannie Mae and Freddie Mac:

{kind=link}

This should be somewhat comforting for those investors that are worried about default risk. The United States government cannot default in a nominal sense, despite some of the claims that emerged in the debt ceiling fight. While it can default through inflation and repaying the Treasury securities with weaker dollars, that is not normally considered a default. The Congressional Budget Office estimates that the United States Treasury will pay $640 billion in interest on the national debt during the 2023 fiscal year. It projects that total income tax collection will be $2.523 trillion over the period. Clearly, there is no risk of a nominal default on publicly-held Treasury securities. Thus, the default risk is essentially zero on a sizable portion of the fund's holdings.

The same is probably true of the Fannie Mae and Freddie Mac securities in the portfolio. While these are not explicitly guaranteed by the United States Federal Government, we saw during the subprime mortgage crisis back in 2008 that the government will step in and guarantee these securities in a worst-case scenario. Thus, these can probably be considered risk-free as well. These securities combined with the U.S. Treasuries account for 30.14% of the fund's portfolio:

{kind=link}

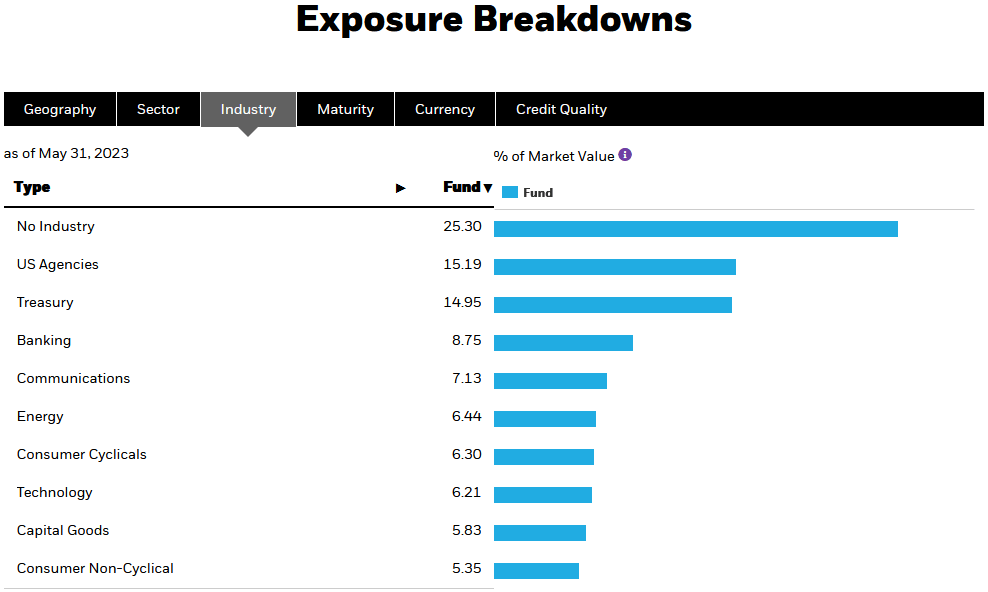

Thus, we only have 69.86% of the portfolio that carries some form of default risk. Fortunately, we see that even the non-U.S. government debt held by the fund tends to be rated fairly highly:

{kind=link}

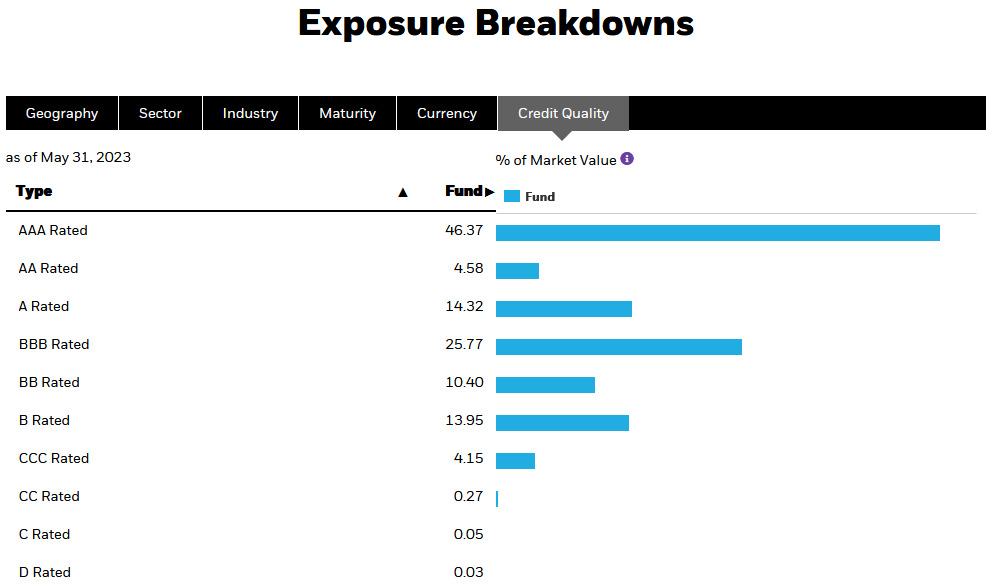

An investment-grade security is anything rated BBB or above. As we can clearly see, that is 91.04% of the portfolio (the reason that the above chart shows more than 100% weighting to all bonds in total is because of leverage). As investment-grade securities are highly unlikely to default and the fund has 1,711 holdings as of the time of writing, we can clearly see that we probably do not have to worry about much besides interest-rate risk here. This was discussed earlier in this article.

Leverage

Earlier in this article, I stated that closed-end funds such as the BlackRock Core Bond Trust have the ability to employ certain strategies that boost their yields beyond that of the underlying assets. One of these strategies is the use of leverage. In short, the fund is borrowing money and using that borrowed money to purchase bonds and similar assets. As long as the interest rate that the fund pays on the borrowed money is less than the yield of the purchased securities, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will normally be the case. With that said, the fund is not going to benefit as much from this strategy today as it did a year ago when interest rates were effectively zero.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since this would expose us to an excessive level of risk. I do not normally like to see a fund's leverage exceed a third as a percentage of its assets for this reason. Unfortunately, this fund's levered assets currently comprise 39.61% of its portfolio so it exceeds that level. This could be a risky situation for risk-averse investors as it will cause the fund to decline much more than the index during a market correction. The fact that the fund's assets are relatively safe securities helps a bit, but the securities that blew up Silicon Valley Bank were U.S. Treasuries, so not even those are safe from interest-rate risk. Overall, I would prefer to see this fund have lesser leverage and lower risk, especially since this fund seems to be an investment-grade bond fund.

Distribution Analysis

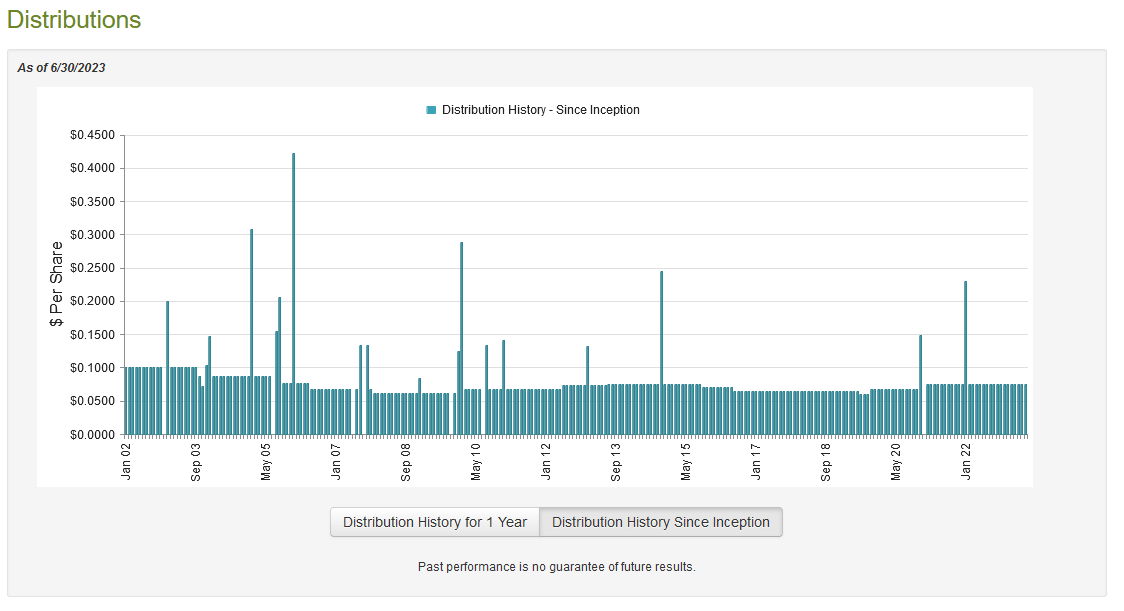

As mentioned earlier in this article, the primary objective of the BlackRock Core Bond Trust is to provide its investors with a high level of current income. This is accomplished by purchasing primarily investment-grade bonds, as well as trying to obtain gains by trading these bonds. Unfortunately, such gains are difficult to come by in a rising rate environment like the one that we have had over the past year. The fund also applies a layer of leverage to boost the effective yield of the assets in its portfolio. Thus, we can assume that this fund can probably provide a reasonably high yield to its shareholders. This is certainly the case as the BlackRock Core Bond Trust currently pays a monthly distribution of $0.0746 per share ($0.8952 per share annually), which gives it an 8.41% yield at the current price. Unlike many other fixed-income funds, this one has been very consistent with its distribution and has not cut it over the past two years. Its long-term history has been somewhat more variable, though:

{kind=link}

The fact that the fund has not cut in the wake of last year's challenging conditions for bonds may endear it to those investors that are seeking a safe and secure source of income to use to pay their bills or cover other expenses. However, the fund has varied its distribution historically so it is certainly not perfect in this regard. The fact that this fund has been able to maintain its distribution during a time when most of its peers have not is confusing and bears further investigation. In particular, we want to make sure that the fund can actually afford the distribution that it pays out since we do not want to be the victims of a distribution cut. After all, a distribution cut would reduce our incomes and might cause the fund's share price to decline.

Unfortunately, we do not have an especially recent document that we can discuss for the purposes of our analysis. The fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. As such, it will not include any information regarding the fund's performance over the past six months. This is unfortunate because the past six months have been much better for bonds than all of 2022. Despite the fact that the bond market seems to be overly optimistic right now, there could still be some profits to be made by trading bonds. The fund might have been able to exploit that, but we have no way of knowing for certain right now. During the full-year period, the fund received $416,151 in dividends along with $47,338,779 in interest from the assets in its portfolio. This gives the fund a total investment income of $47,754,930 over the period. It paid its expenses out of this amount, which left it with $34,621,610 available for the shareholders. This was, unfortunately, not enough to cover the $44,321,199 that the fund paid out in distributions during the period. This is somewhat concerning as we normally like a fixed-income fund to be able to pay its distributions out of net investment income. That is obviously not the case here.

However, the fund does have other methods through which it can obtain the money that it needs to cover its net investment income. For example, it might have capital gains that can be paid out. This was, unsurprisingly, not the case with this fund during the period. The BlackRock Core Bond Trust reported net realized losses of $58,306,032 and had another $179,504,308 net unrealized losses. Overall, the fund's assets went down by $247,242,455 after accounting for all inflows and outflows. This is concerning, to put it mildly. As I noted in my last article, this represents the second straight year of asset declines. During the full-year 2021 period, the fund had a net investment income of $38,808,459 and net realized gains of $18,970,678. That was barely enough to cover the $56,675,846 that it paid out in distributions, but there was not enough left over to carry through to 2022 and offset the overpayment. Thus, the fund failed to cover its distributions over the two-year period. At the start of 2021, the fund had total assets of $886,969,812 but this figure was down to $588,071,316 at the start of this year. It is hard to believe that it was able to completely offset this asset decline year-to-date, so it appears that this fund needs to cut its distribution. Investors should be prepared for such a possibility.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Core Bond Trust, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of June 29, 2023 (the most recent date for which data is available as of the time of writing), the BlackRock Core Bond Trust has a net asset value of $10.86 per share but the shares only trade for $10.64 each. This gives the fund's shares a 2.03% discount to net asset value at the current price. This is not quite as good as the 3.20% discount that the shares have had over the past month, so it might make sense to wait until the shares decline a bit in price before purchasing.

Conclusion

In conclusion, the BlackRock Core Bond Trust has certainly benefited from the optimism in the bond market with regard to interest rates. Unfortunately, this optimism may be unfounded, which could result in a market correction. The fund also has seen its assets decline substantially over the past two years and it is difficult to see how it can avoid a distribution cut at some point. The price is reasonable though, but I will admit that I would like to see a larger discount to account for the risks of a near-term market reversal.

For further details see:

BHK: Declining Assets And Market Seems Overly Optimistic