BHK - BHK: Risks May Be Higher Than The Market Believes

2023-11-22 07:04:39 ET

Summary

- The BlackRock Core Bond Trust offers a high yield of 8.82%, higher than U.S. Treasury securities and major bond indices.

- The fund's share price has declined 5.67% since July, worse than the Bloomberg U.S. Aggregate Bond Index.

- The fund primarily invests in investment-grade securities, distinguishing it from high-yielding funds that invest in riskier assets.

- The market may be pricing far greater rate cuts than will ultimately happen, causing the bonds held by this fund to be overpriced.

- The distribution may be secure, but the fund's current price does not appear to be considering the possible risks here.

The BlackRock Core Bond Trust ( BHK ) is a closed-end fund that investors can purchase in order to earn an income from the assets that they have managed to accumulate in their portfolios. The fund’s current 8.82% yield stands as a testament to the fund’s capacity to provide its investors with an income, as this yield is substantially higher than U.S. Treasury securities or any of the major bond indices right now. It is also higher than any of the major equity indices, but that goes without saying since most income-focused investors are buying bonds right now anyway. The fund’s yield is, however, lower than many other bond funds. After all, over the past few weeks, we have discussed a number of fixed-income closed-end funds that boast double-digit distribution yields at their current prices. However, most of these high-yielding funds invest in junk bonds or leveraged loans that are made to companies that may not be in the best position financially. The BlackRock Core Bond Trust is different, as its portfolio is primarily invested in investment-grade securities.

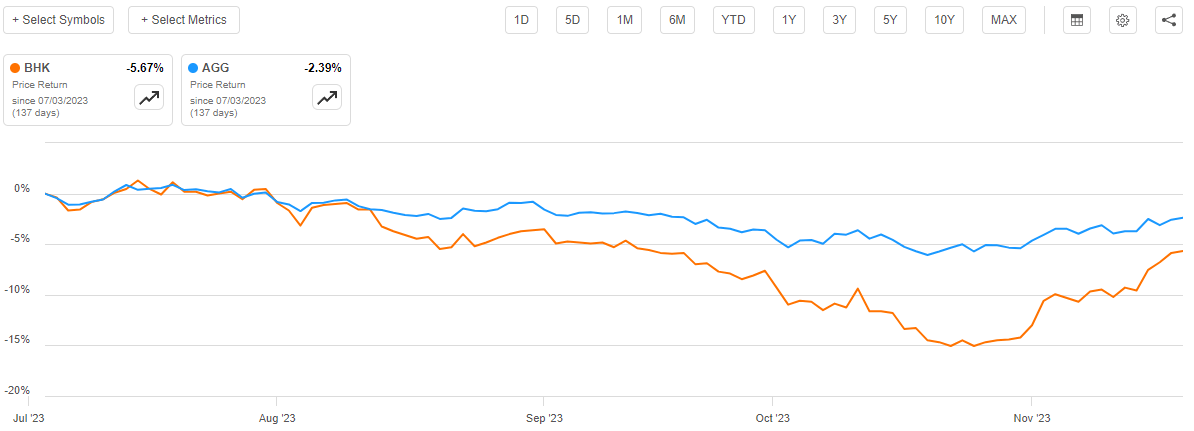

As regular readers may remember, we last discussed the BlackRock Core Bond Trust in early July. At that time, it appeared as though the market was overly optimistic with respect to near-term interest rate cuts and was bidding up bond prices to correspond with this belief. That proved to be correct, as very shortly after that article was published, the market began to sag, and long-term interest rates began to go up. This naturally had a negative impact on the fund’s share price. The fund’s share price has declined 5.67% since the date that my prior article was published, which is quite a bit worse than the 2.39% decline of the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

The fund has done a bit better when we incorporate the distribution into its results, as investors in the fund have received some payments that have helped to offset the decline in asset prices. When this is done, we see that investors in this fund have only lost 2.12% since the date that my prior article was published. Investors in the iShares Core U.S. Aggregate Bond ETF have only lost 1.29% over the same period so the index has still performed a bit better, although the difference between the BlackRock Core Bond Trust and the market index is less pronounced.

There may be some reasons to believe that the market is once again being overly optimistic about the trajectory of interest rates and if that proves to be the case then the recent gains that this fund has experienced are likely to be erased. Thus, it could be riskier to purchase this fund today than it was a few weeks ago, especially since the shares are not trading at a large discount to net asset value.

About The Fund

According to the fund’s website , the BlackRock Core Bond Trust has the primary objective of providing its investors with both current income and capital appreciation. Bonds are by their nature income vehicles so the current income objective is understandable, but it is much more difficult to see how any bond fund can provide capital appreciation. As I pointed out in my previous article on this fund:

Bonds provide their investment return primarily in the form of direct payments to the investors. In fact, this is going to be the only return delivered over the life of the bond. This comes from the fact that an investor purchases a bond for its face value at issuance, receives regular payments from its issuer over the life of the bond, and then receives the face value back when the bond matures. A bond has no inherent link to the growth and prosperity of the issuing entity, so there is no built-in capital gains potential.

The only realistic way that a bond fund could provide capital appreciation consistently is if interest rates decline indefinitely. That is unrealistic since nobody will ever buy a bond with a negative nominal yield unless they are forced to by the government or other authority. Thus, realistically any capital gains will only be come about by exploiting price changes that accompany fluctuations in interest rates. These are not going to be consistent in the long term, as we have seen quite clearly over the past three years.

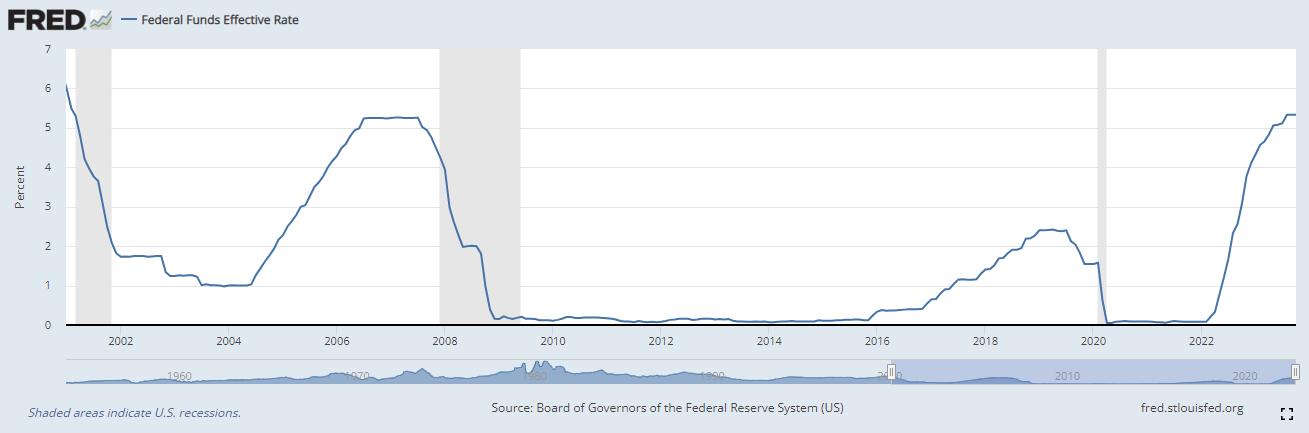

As everyone reading this is certainly well aware, the Federal Reserve has been aggressively raising interest rates since March of 2022. This is an effort to reduce the incredibly high inflation rate that has been plaguing the American economy in the post-pandemic period. As of right now, the effective federal funds rate sits at 5.33%, which is the highest level that we have seen since early 2001:

{kind=link}

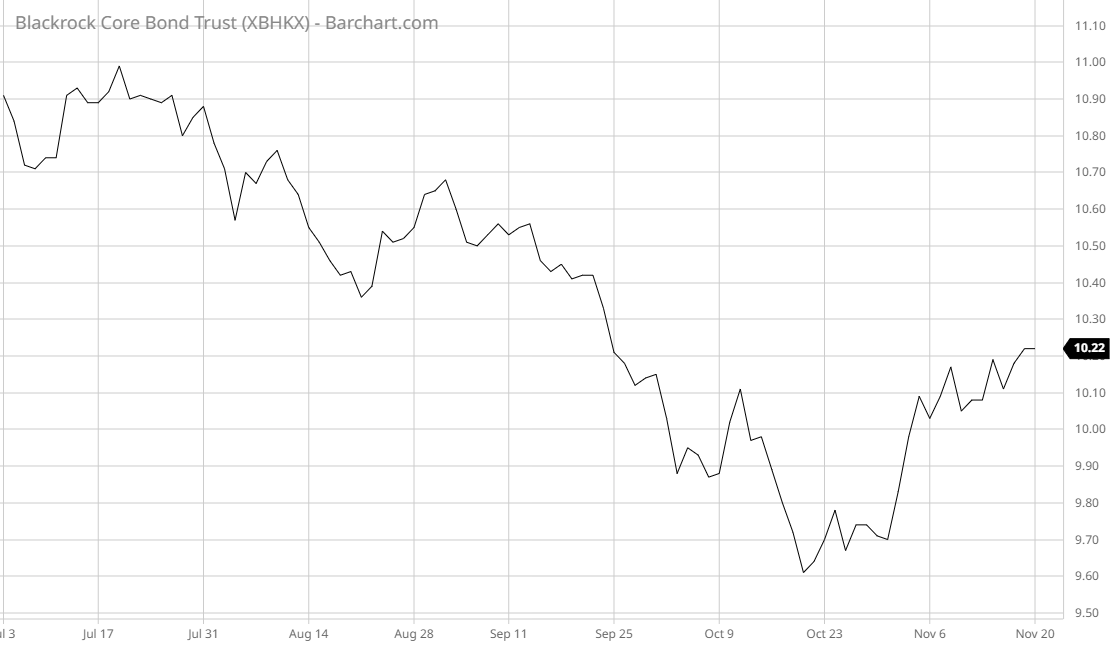

This is actually higher than the 5.08% effective federal funds rate that prevailed in the market at the time that my prior article on this fund was published. As such, this was one of the factors that caused the fund’s shares to decline over the past four months, as shown in the introduction. After all, the rising interest rate caused the coupon offered by brand-new bonds to increase over the period. The price of existing bonds had to go down in order for those securities to deliver competitive yields, which reduced the fund’s net asset value. Indeed, as we can see here, the fund’s net asset declined by 6.32% over the period, going from $10.91 per share to $10.22 per share:

{kind=link}

As the fund’s price performance in the market usually correlates with its net asset value, it should be easy to see why the fund’s share price went down.

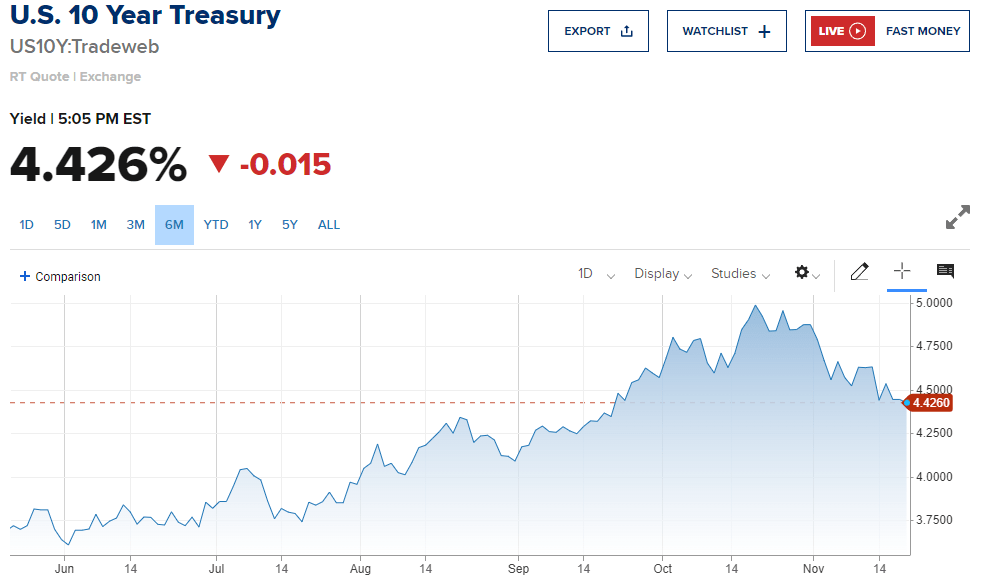

Perhaps more important than the rising federal funds rate is the fact that long-term interest rates went up over the period. This is apparent by looking at the ten-year U.S. Treasury yield, which acts as the benchmark interest rate for many long-dated loans and other debt securities. As we can see here, the ten-year U.S. Treasury yield went up over the trailing six-month period, although it has recently begun to decline:

{kind=link}

This explains the fund’s performance quite well, as its net asset value has roughly mirrored the ten-year U.S. Treasury. That is exactly what we would expect to see from a bond fund that invests primarily in higher quality debt, as this one does.

According to the fund’s website,

BlackRock Core Bond Trust’s investment objective is to provide current income and capital appreciation. The Trust seeks to achieve its investment objective by investing at least 75% of its assets in bonds that are investment grade quality at the time of investment. The Trust’s investments will include a broad range of bonds, including corporate bonds, US government and agency securities, and mortgage-related securities. The Trust may invest directly in such securities or through derivatives.

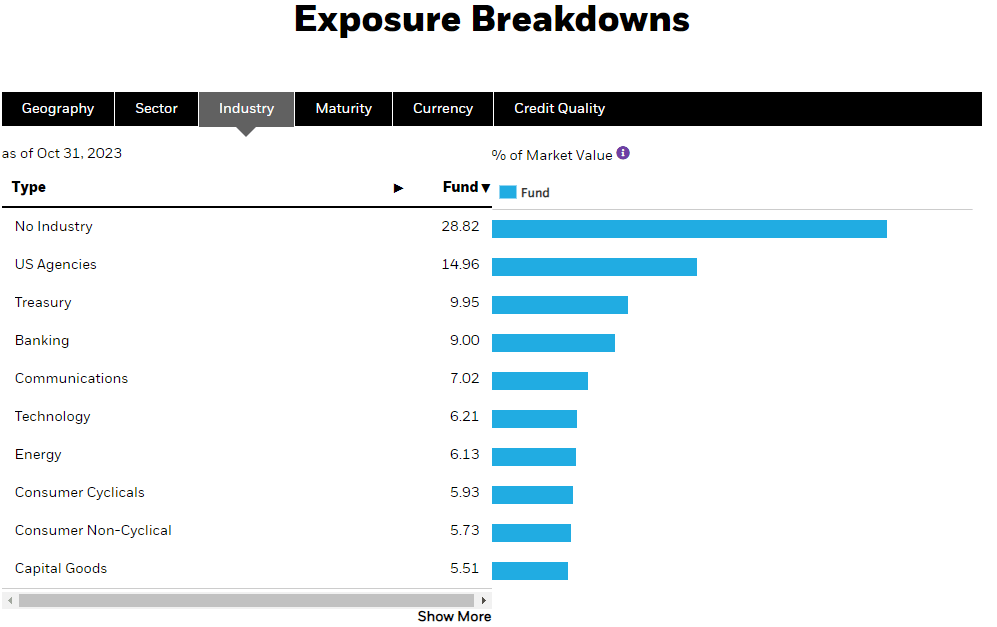

By far the largest issuer of investment-grade debt securities in the United States is the U.S. Treasury and various government agencies. We would therefore expect these securities to have a fairly prominent position in the fund’s holdings. However, that is not really the case. As we can see here, U.S. Treasury securities only accounted for 9.95% of the fund’s total assets as of October 31, 2023. U.S. Government Agency securities accounted for a larger 14.96%:

{kind=link}

This is very different from the weightings that we see in the broader Bloomberg U.S. Aggregate Bond Index. The index currently has a 42.17% allocation to U.S. Treasuries, but only a 0.83% allocation to US Government Agency securities. Thus, the fund is significantly underweight Treasuries relative to the index, although its agency position is much larger.

This actually makes a great deal of sense. U.S. Treasuries generally have the lowest yields of any bonds in the U.S. market. After all, the ten-year U.S. Treasury bond is considered to be the “risk-free” asset, so it should have no risk premium. Everything else in the bond market should have a higher yield than Treasuries in order to compensate investors for assuming default risk. As such, a fund that is seeking to earn a high level of income for its shareholders will not want to purchase Treasuries. Rather, it will invest in investment-grade corporates and similar bonds that have a higher interest rate than Treasuries.

Interest Rate Trends

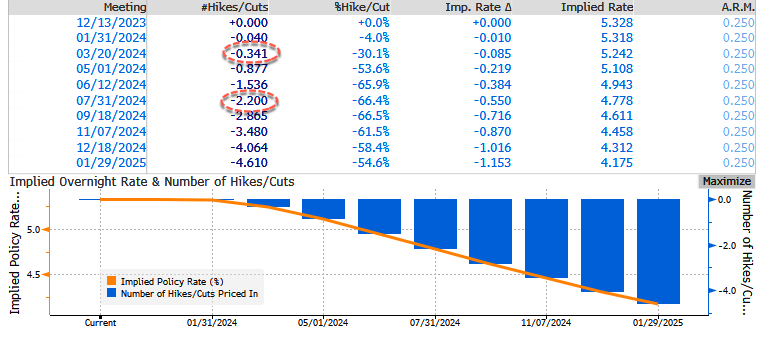

Over the past few weeks, American markets have become incredibly optimistic about the potential that the Federal Reserve will reduce interest rates in the very near future. As I pointed out in a recent article , the market is currently anticipating that the nation’s central bank will reduce the federal funds rate by 100 to 125 basis points by December 2024. This is evident simply by looking at the federal funds futures market:

{kind=link}

It is this optimism about interest rate cuts that has been responsible for the surging asset valuations that we have seen since the final week of October. This surge in asset valuations was shown earlier in this article in the fact that the ten-year U.S. Treasury yield has declined from a peak of 4.9880% and the fact that shares of the BlackRock Core Bond Trust are up 8.44% since November 1, 2023.

The members of the Federal Open Market Committee, which sets the central bank’s target for the federal funds rate, do not believe that the federal funds rate will decline anywhere near this quickly. The median estimate of the committee members is that the effective federal funds rate will be at 5.10% at the end of 2024. That is far higher than the market’s implied rate as shown above.

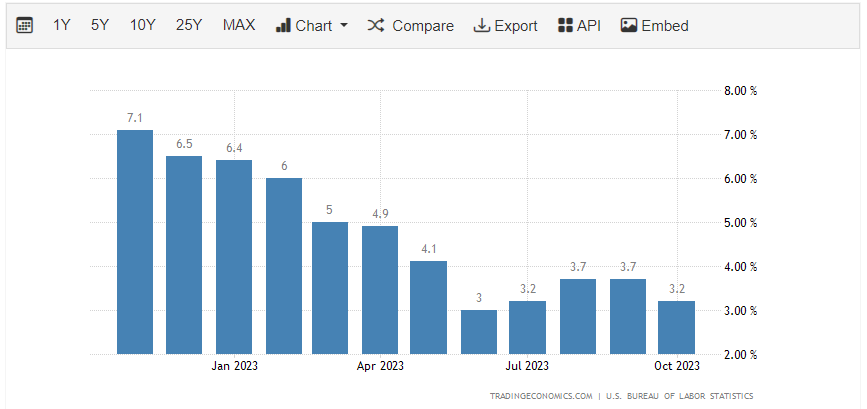

Another reason that the market may be overly optimistic can be found in the inflation data. The entire case for the surge in interest rates since the start of 2022 has been the Federal Reserve’s fight against inflation. The most recent inflation report from the Bureau of Labor Statistics shows that the consumer price index went up by 3.2% year-over-year:

{kind=link}

That is actually a larger increase than we saw in June, and it is still far above the Federal Reserve’s target of 2% year-over-year. Chairman Powell has been very consistent in his statements that the Federal Reserve will not cut interest rates until inflation is on a very clear path to the central bank’s target. That does not appear to be the case right now, and in fact, the recent market optimism has loosened financial conditions and undone a lot of the progress that was being made in September. We can see this by looking at the Goldman Sachs Financial Conditions Index:

{kind=link}

A higher value indicates that financial conditions are tightening, which is exactly what the Federal Reserve is trying to accomplish with its interest rate hikes. We can clearly see that the trend since mid-October has been exactly the opposite of what the central bank wants to accomplish.

It is always a challenge to predict interest rates or the actions of the Federal Reserve. However, recent market action seems to be increasing the possibility that the central bank will hike rather than cut interest rates.

Obviously, anything that suggests that the market is wrong about the Federal Reserve’s action on rates will have an adverse effect on anyone who buys the BlackRock Core Bond Trust at the current level. Indeed, even if the Federal Reserve does cut interest rates next year, it could still prove to be a negative for bonds that are pricing in a larger rate cut. As such, the gains in the fund’s share price since November may have actually increased the risks faced by buyers.

Leverage

As is the case with most fixed-income closed-end funds, the BlackRock Core Bond Trust employs leverage as a means of boosting the effective yield of the assets in its portfolio. I explained how this works in my previous article on this fund:

In short, the fund is borrowing money and using that borrowed money to purchase bonds and similar assets. As long as the interest rate that the fund pays on the borrowed money is less than the yield of the purchased securities, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will normally be the case. With that said, this fund is not going to benefit as much from this strategy today as it did two years ago when interest rates were effectively zero.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since this would expose us to an excessive level of risk. I do not normally like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the BlackRock Core Bond Trust has leveraged assets comprising 35.86% of its portfolio. This is a bit above the one-third maximum that we would like to see, but it is substantially less than the 39.61% leverage that the fund had the last time that we discussed it. As I have pointed out in past articles, fixed-income funds can usually sustain a bit more leverage than equity funds as their assets tend to be less volatile. This is especially true for this fund, as it invests in investment-grade bonds, which are among the safest securities available in the market.

As such, we probably do not need to worry about the fund’s leverage too much, as the balance between risk and reward should be acceptable here.

Distribution Analysis

As mentioned earlier in this article, the BlackRock Core Bond Trust has the primary objective of providing its investors with a very high level of current income. In pursuance of this objective, the fund invests in a portfolio consisting of investment-grade debt securities that deliver the majority of their total investment returns in the form of direct payments to the shareholders. In the current market environment, these securities typically have somewhat decent yields, and the fund controls more securities than it ordinarily could through the use of leverage. These extra securities effectively boost the yield that the fund receives on the overall portfolio. The fund collects all of the money that it receives from the assets in the portfolio and then pays it out to the shareholders, net of the fund’s own expenses. As such, we can probably assume that the fund will have a fairly high yield itself.

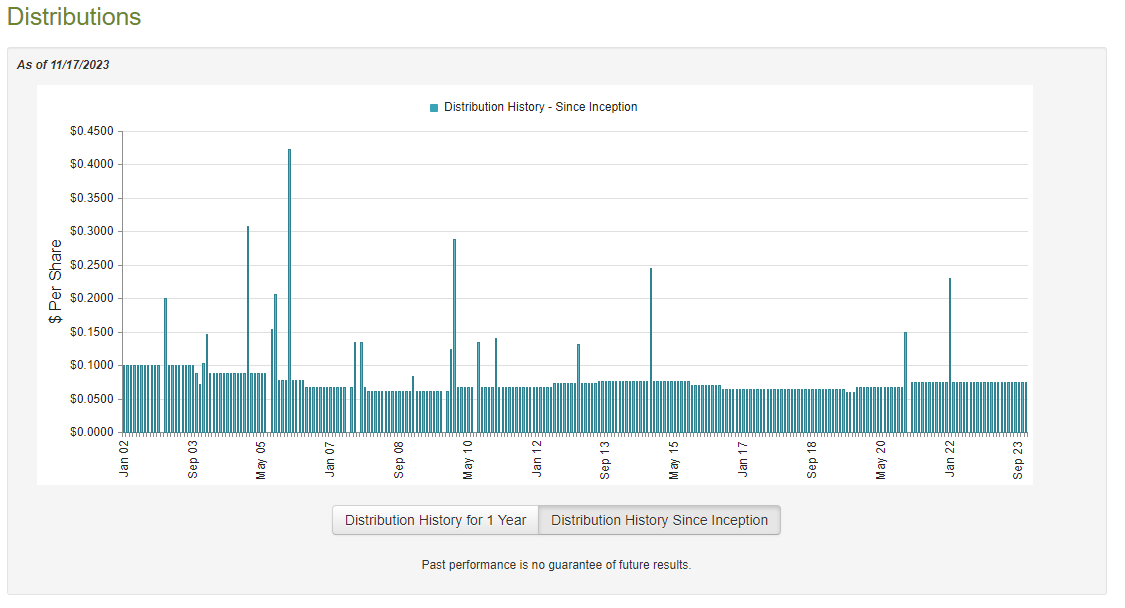

This is certainly the case, as the BlackRock Core Bond Trust pays a monthly distribution of $0.0746 per share ($0.8952 per share annually), which gives it an 8.82% yield at the current share price. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years, as the fund has both raised and lowered its payout fairly frequently over the years:

{kind=link}

This variable distribution is likely to be a bit of a turn-off for any investor who is seeking to earn a safe and secure income from the assets in their portfolios. This may be especially true for investors such as retirees, who cannot afford to have their incomes go down in today’s inflationary environment. With that said though, it is fairly common for a bond fund to have to vary its distribution over time. This is due to the interest rate sensitivity of the assets in the portfolio, which causes the potential returns of its assets to vary based on actions of central banks, government officials, and other entities outside of its control.

Naturally, anyone who purchases the fund today does not need to worry about the actions that the fund has had to take in the past. This is because today’s buyer will receive the current distribution at the current yield and will not be hurt by the fact that the fund changed its distribution in the past. The most important thing for today’s buyers is how well the fund can sustain its distribution going forward. We should investigate this.

Fortunately, we do have a somewhat recent report that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a newer report than the one that we had available to us the last time that we discussed this fund, which is quite nice to see. This report will give us an idea of how well this fund performed during the first half of this year, which was generally characterized by euphoria in the market as investors expected that the Federal Reserve would quickly cut interest rates and bid up bond prices in expectation of that event. It was, in fact, somewhat similar to the current environment. While the market was wrong in its assumptions, the BlackRock Core Bond Trust might have still had the potential to earn some capital gains by selling appreciated assets into such a euphoric market.

During the six-month period, the BlackRock Core Bond Trust received $289,793 in dividends and $25,349,379 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we get a total investment income of $25,754,478 during the period. The fund paid its expenses out of this amount, which left it with $14,991,227 available for shareholders. As might be expected, this was nowhere near enough to cover the $24,175,190 that the fund paid out in distributions during the period. This is something that is certainly going to be concerning, as we normally would like a fixed-income fund to be able to fully cover its distributions out of net investment income.

With that said, the fund does have other methods through which it can obtain the money that it needs to cover its distributions. For example, the fund might be able to sell some appreciated securities in a confident market in order to generate some capital gains. Unfortunately, the fund had mixed results at this task during the period. It reported net realized losses of $27,123,973 but these were offset by $38,629,473 net unrealized gains. Overall, the fund’s net assets increased by $2,321,537 after accounting for all inflows and outflows during the period.

Thus, the fund did technically cover its distribution during the period. It had to rely on unrealized capital gains to accomplish that feat though, and as we all know, unrealized capital gains can be very easily erased by a market correction. As we saw earlier in this article, it does appear that this was the case during the second half of this year, as the fund’s net assets per share are down since July 1, 2023. Thus, it is uncertain whether or not the fund can sustain its distribution, but at the moment it does appear that the distribution is higher than the fund’s actual investment returns and it is destroying its net asset value in the process. That is not sustainable over an extended period.

Valuation

As of November 17, 2023 (the most recent date for which data is currently available), the BlackRock Core Bond Trust has a net asset value of $10.22 per share but the shares currently trade for $10.14 each. This gives the fund’s shares a 0.78% discount on net asset value at the current price. This is an incredibly small discount, and it is substantially worse than the 4.85% discount that the shares have had on average over the past month. As such, it might be possible to get a better price by waiting a bit.

Conclusion

In conclusion, the BlackRock Core Bond Trust has delivered a pretty strong performance over the past few weeks as the market has been anticipating that the Federal Reserve will cut interest rates in the very near future. Unfortunately, the market may be disappointed here as inflation still remains far above the central bank’s target level and the recent optimism has loosened financial conditions, undoing the progress that the Federal Reserve has already made in its efforts to combat inflation. Thus, the risks here may be higher than most people believe.

For further details see:

BHK: Risks May Be Higher Than The Market Believes