RTNTF - BHP Group And Rio Tinto Group: Let's Build An All-Weather Portfolio

2023-10-19 18:46:30 ET

Summary

- Ray Dalio has shaped our thinking at a fundamental level.

- Now is a good time to build an all-weather portfolio due to macroeconomic and geopolitical uncertainties.

- I will explain why BHP Group Limited and Rio Tinto Group can be substituted for commodities in an all-weather portfolio for a number of good reasons.

- They offer active income, relatively stable profitability, and also a favorable potential for share price appreciation.

- As a plus, both Rio Tinto Group and BHP Group Limited also offer geographical diversification, another key concept in Dalio's approach.

Ray Dalio's All-Weather Portfolio

The thesis of this article is twofold. First, I will argue that now is a good time to build an all-weather portfolio given the current macroeconomic and geopolitical uncertainties. Second, I will explain why two leading commodity stocks, BHP Group Limited ( BHP ) and Rio Tinto Group ( RIO ), can be substitutes for commodities in an all-weather portfolio for several reasons. We are covering two leading commodities stocks to provide a broader view of the sector for better representation. The use of one stock can sometimes provide a very distorted and biased view of a sector.

The first argument has been detailed in a series of blog articles . The gist is essentially this: diversification should NOT start with picking different stocks. It should start with allocation among different asset classes that respond differently to different macroeconomic forces. Ray Dalio's all-weather model portfolio provides an excellent template, with holdings reacting differently to different fundamental market forces (deflationary, inflationary, et al). We feel the ongoing macroeconomic and geopolitical risks combine to make now an especially good time to build such a portfolio. In our view, the macroeconomic environment will be heavily influenced by persisting high inflation, elevated interest rates, and the ongoing war in Ukraine and between Israel and Hamas. By investing in a mix of different asset classes, an all-weather portfolio can provide investors with exposure to various sources of return, which can help to improve the overall performance of their portfolio over the long term.

Moving onto the second part of the thesis. I see BHP and RIO as good substitutes for the commodity holdings in an all-weather portfolio. In the remainder of this article, I will elaborate on my following key considerations:

- They provide exposure to commodities without the need to invest directly in the commodities themselves. Investing in commodities can be complex and expensive, and it can be difficult to store and transport some commodities. Commodity stocks, on the other hand, can be bought and sold like any other stock, making them a more accessible and convenient way to invest in commodities.

- They can provide investors with dividend streams even in periods when commodity prices are falling. In contrast, holding commodities not only does not generate active income, but also typically involves management fees, trading fees, et al.

- Finally, in addition to exposure to commodities and providing active dividend income, I will argue shares for both BHP and RIO are well poised for price appreciation as well due to their stable fundamentals and compressed valuation.

BHP, RIO, and commodities

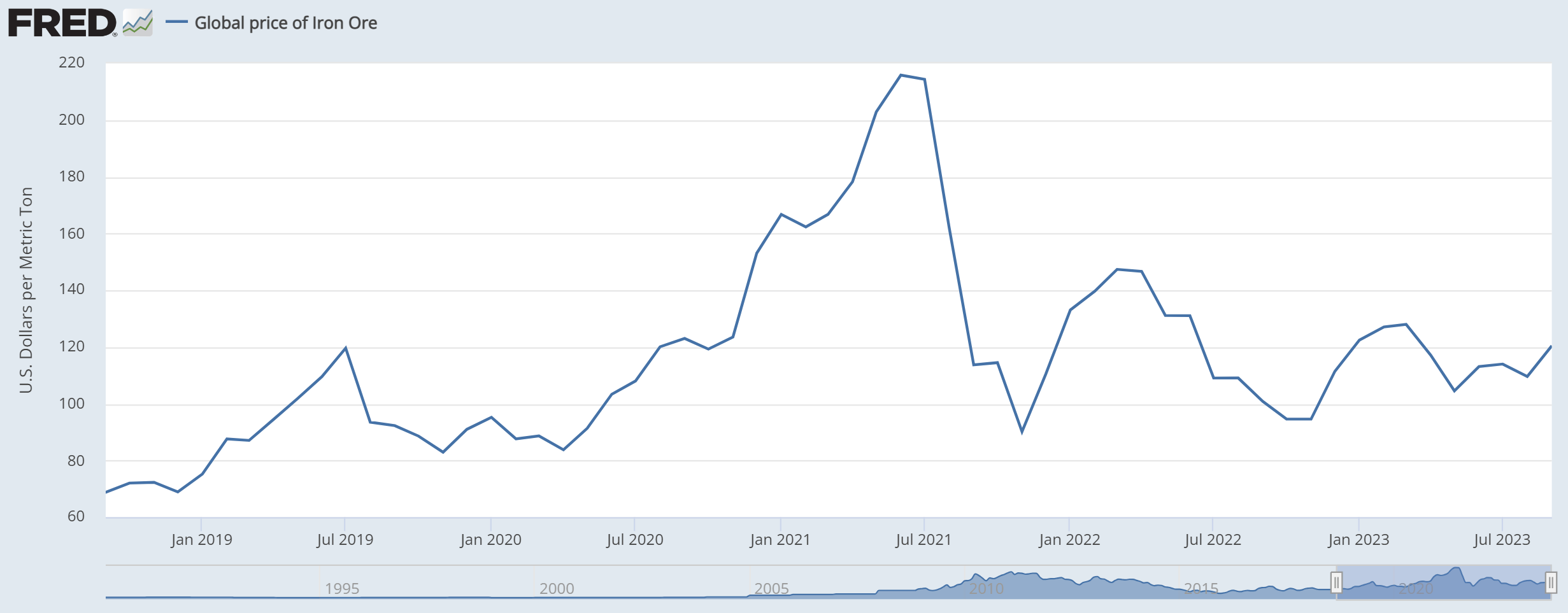

Commodity and commodities stocks are notorious for their large volatilities and highly cyclical behavior. As an example, the chart below shows the price of iron ore, a major commodity that has contributed substantially to both BHP and RIO's revenues, over the past few years. As seen, in the past 5 years alone, the price has more than doubled between 2019 and 2021 (from around $80 per metric ton to over $200 per metric ton in October 2023) and then approximately halved to the current level of ~$120 per ton.

{kind=link}

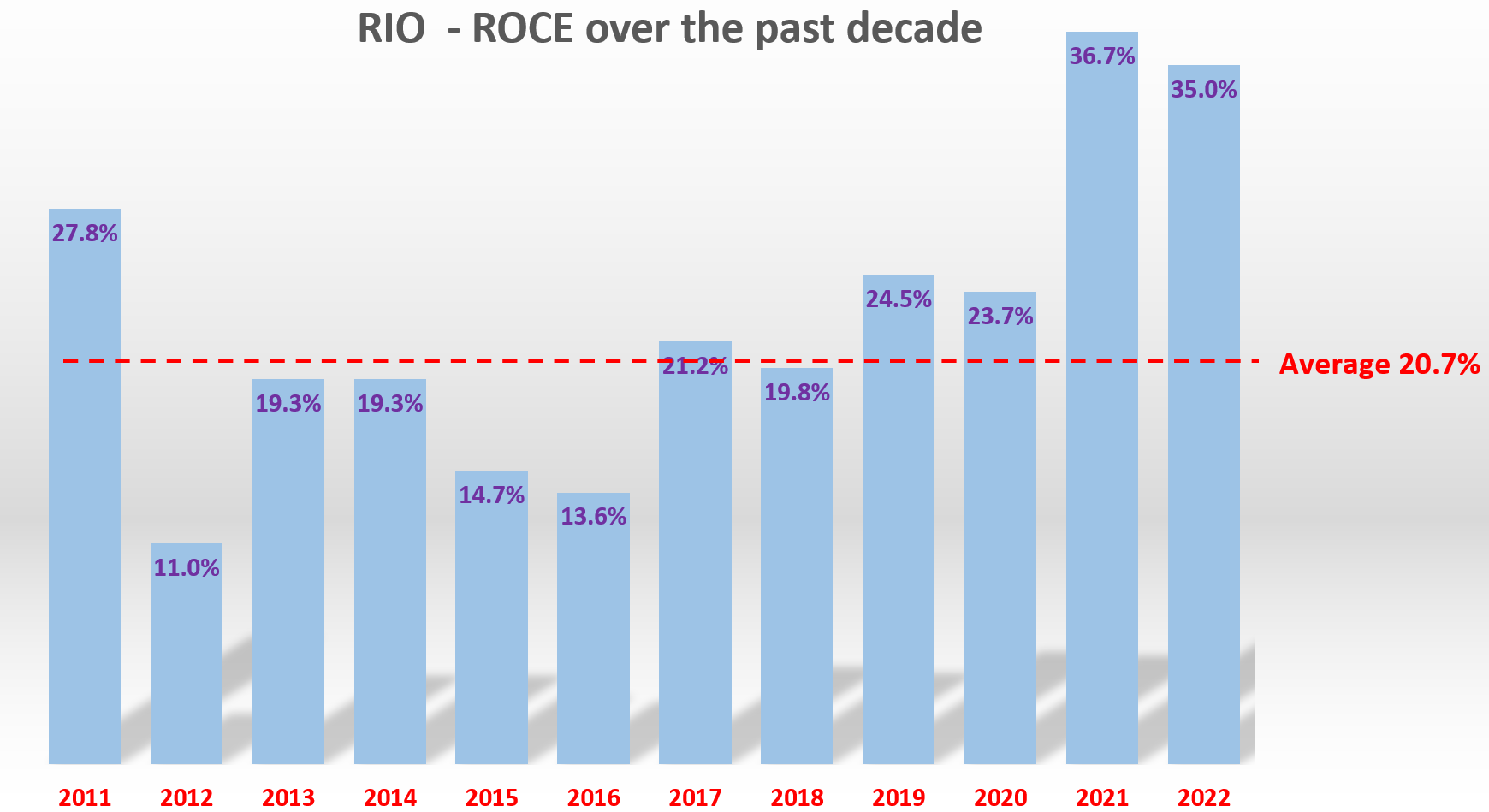

Against this backdrop, several advantages of using leading stocks like BHP and RIO as substitutes for commodities become clear. First, their profitability can be less volatile and cyclical than commodity prices. As an example, the next chart shows RIO's ROCE (return on capital employed) over the past decade. As seen, despite the rollercoaster behavior of iron ore prices shown above, the ROCE for RIO has stayed relatively stable with a very robust average of around 20.7%. The ROCE for BHP is essentially the same with a slightly higher average of 21.3%.

Second, my view is that the current commodity cycle is close to its bottom, and I expect the recovery phase to start. As a result, I expect healthy earnings growth and price appreciation potential from both stocks as elaborated on next.

Author Based on Seeking Alpha data

{kind=link}

BHP and RIO: well-poised for growth

For a traditional business like BHP and RIO, the two fundamental drivers for growth are: A) the ROCE analyzed above; and B) their plowback ratio ("PBR"). ROCE measures how much profit they can earn on $1 of capital, and PBR measures how much capital they can keep investing into the business.

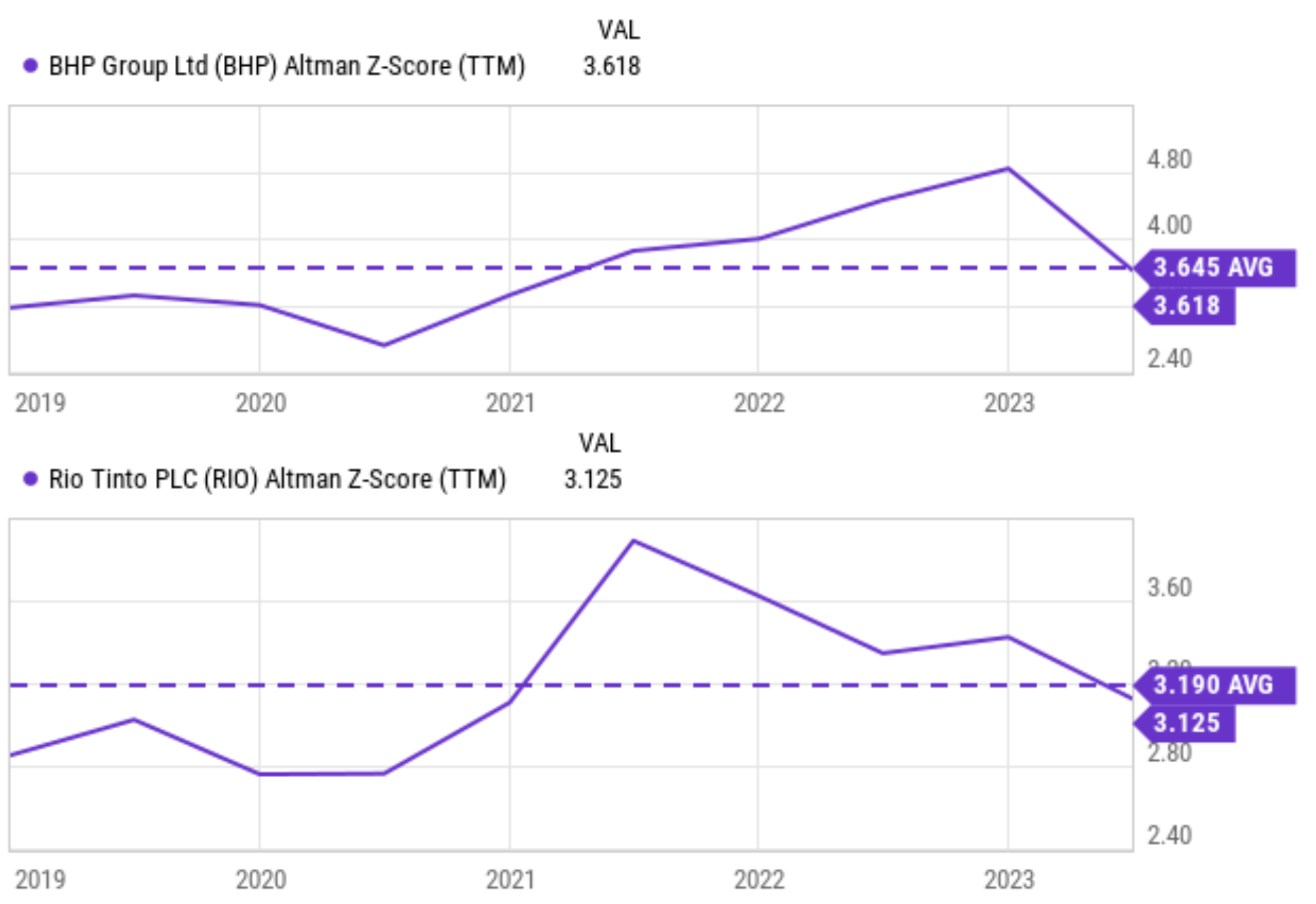

The chart below shows RIO and BHP's Altman Z score in the past few years. For readers new to the concept, the Altman Z-score is a metric that reflects the overall financial health of a business (by considering multiple factors across different financial statements). As a general rule of thumb, for manufacturing businesses such as BHP and RIO, a score near 3 or above has been correlated with a strong financial position.

Against this background, you can see that the Altman Z scores of both RIO and BHP are currently above 3 (3.6x for BHP and 3.1x for RIO). Both of their scores are also near their own historical averages. To me, these scores suggest that they are in a solid financial position overall and can afford a healthy level of PBR to drive growth, as elaborated on next.

{kind=link}

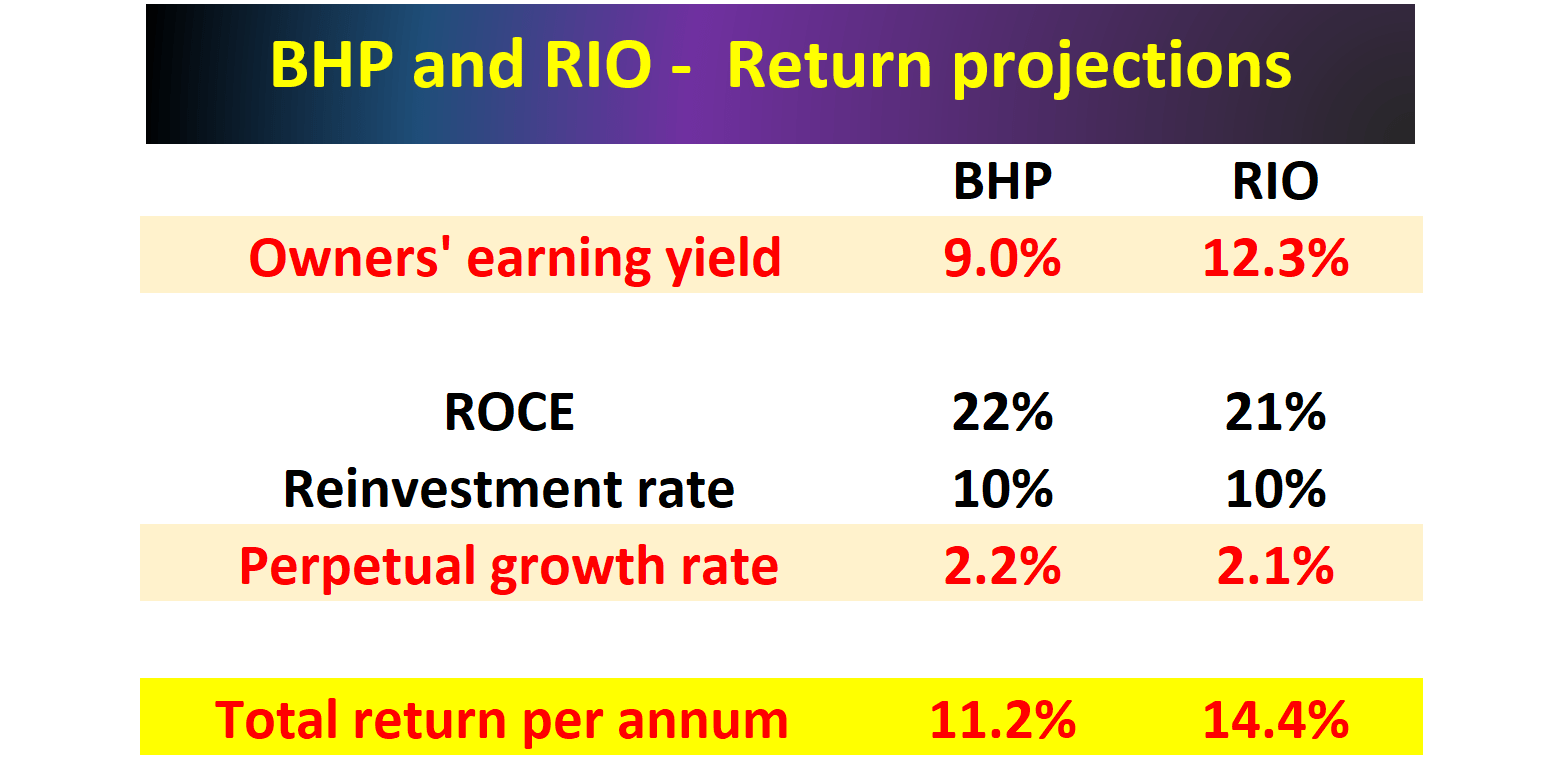

BHP and RIO: growth and return projections

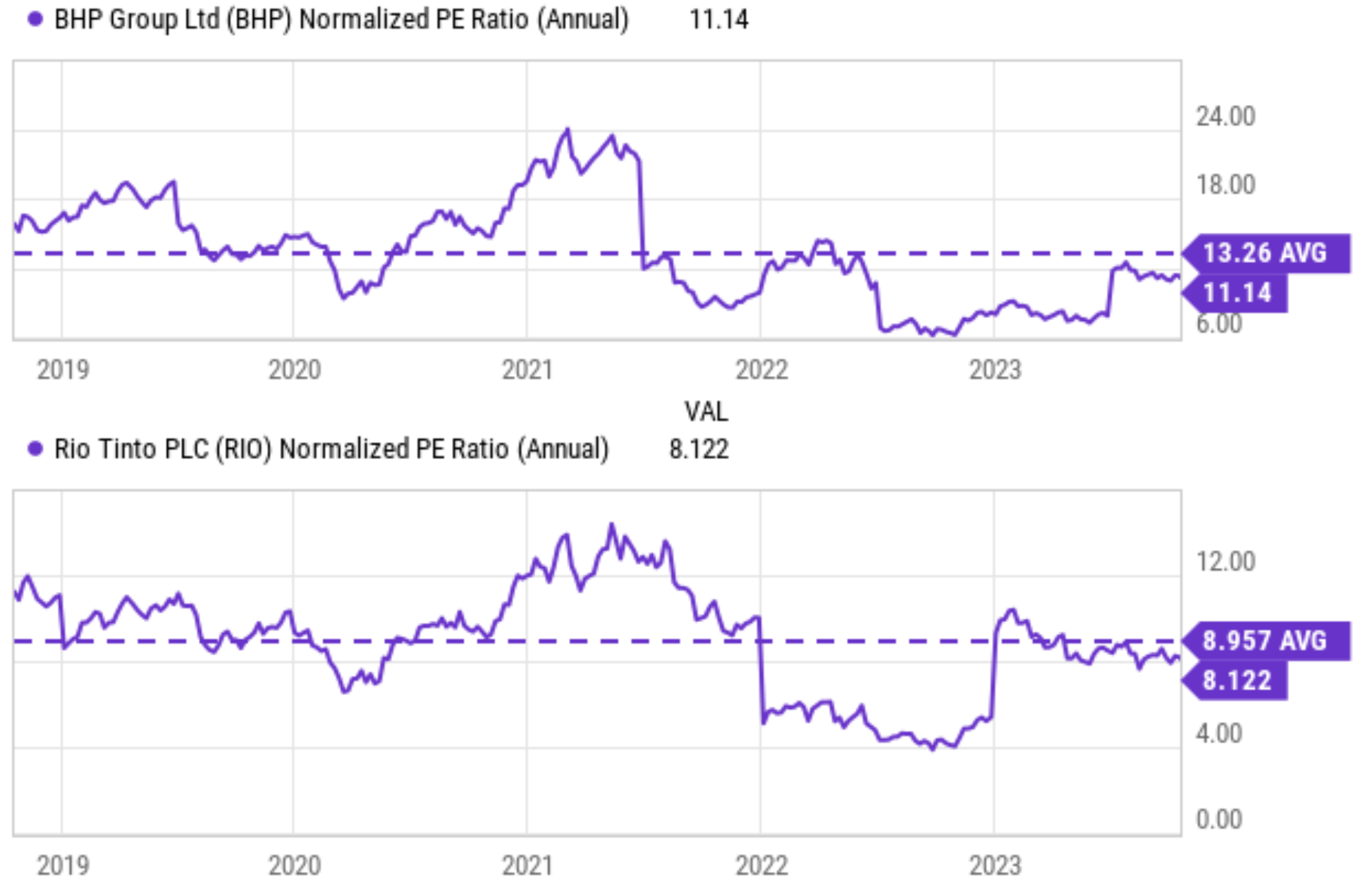

As aforementioned, my view is that iron ore prices (together with a few other related commodities) are currently close to a cyclical bottom. As a result, the valuations of both RIO and BHP are currently at a compressed level, both by horizontal and vertical comparison.

As seen in the top panel of the chart below, BHP is currently priced at 11.1x P/E, about a 17% discount compared to a historical average of 13.3x. And the bottom panels show the same picture for RIO. It is currently priced at 8.1x P/E, about a 10% discount compared to its historical average of about 9.0x.

{kind=link}

The combination of robust ROCE, healthy PBR, and compressed valuation has created an attractive potential for share price appreciation. My projections for their growth and the total return potential are summarized in the chart below. I consider my following projection to be on the conservative side for at least two reasons. First, in this projection, I used the normalized P/E ratio mentioned above to approximate their owner's earning yield, which is a conservative assumption. Second, the growth rate was computed as the product of the ROCE and their PBR (or the so-called reinvestment rates). This calculation gives us the real growth rate excluding inflation, and hence is another conservative assumption.

{kind=link}

Risks and final thoughts

Both BHP and RIO face largely the same risks given the similarities of their exposure, and these risks have been the topic of my earlier articles (and other Seeking Alpha articles, too). Here, I will concentrate more on the risks specific to this article's particular approach.

First, it is important to note that commodity stocks are not a perfect substitute for commodities. For example, commodity stocks are subject to the same risks as other stocks (such as company-specific risks and credit risks), which are not shared by commodities.

Second, a key assumption in my thesis is that iron ore prices (plus a few other key commodities that BHP and RIO mine and market) appear to be near a cyclical bottom now. It is important to note that there are factors that could invalidate such an assumption. Iron ore is the key ingredient in steel, and a large driver for the steel demand is the growth in China and other emerging markets. Whether/how such growth continues is a key variable.

To conclude, the thesis of this article is to explain: A) why now is a good time to build an all-weather portfolio; and B) why BHP and RIO can be used as substitutes for commodities in such a portfolio. There are certainly risks to part B of the argument as mentioned above. However, under current conditions, my view is that the positives easily outweigh the negatives.

To recap, the top positives in my mind are generous dividends to provide active income, relatively stable profitability despite large commodity price gyrations, and favorable total return potential. As a final consideration, another key part of Ray Dalio's thinking involves geographical diversification. Both BHP and RIO can help on this front as well, especially for investors whose exposures are primarily concentrated in the U.S.

For further details see:

BHP Group And Rio Tinto Group: Let's Build An All-Weather Portfolio