TNGRF - BHP Group: Focus On The Outlook

Summary

- BHP Group Limited's half-year earnings report isn't as bad as it seems, as there is a disparity between the firm's realized performance and its prospects.

- Lower rainfall could result in ramp-ups across the board. Moreover, slower core and non-core inflation will likely establish a lower cost base for BHP.

- Although we think journalists have overplayed the China reopening factor, BHP's general supply vs. demand outlook has improved in recent months.

- Offloading existing coal assets and venturing into greenfield projects is in the offing, as illustrated by BHP's Jansen potash venture.

- BHP Group Limited's dividend remains highly lucrative despite a reduction by the company. Investors need to consider that dividend decreases might be uniform and that BHP's cut is not due to structural issues.

BHP Group Limited 's ( BHP ) fiscal 2023 first half financial results are out, and the question beckons: will there be an investor exodus after the firm's disappointing half-year earnings report?

Although not encouraging, BHP Group's H1 financial results were not surprising, as much of the half-year events were incrementally revealed by the company. Nevertheless, an earnings decline remains a critical risk that many investors might be unwilling to tolerate.

However, as we all know by now, we need to leverage information asymmetry to gain an edge in the financial markets. In our opinion, BHP Group's latest earnings report provides an ideal information asymmetry opportunity, as many market participants might be looking at matters in arrears instead of understanding the company's trajectory. Moreover, prevalent risks are currently embedded in the mining stock sphere, which could act as a help-in-hand to investors seeking value gaps.

Despite its soft H1 earnings report, we remain bullish on BHP Group; here is why.

Earnings Release and Outlook Disparity

I wanted to skip coverage of BHP's headline earnings, as it is already widely distributed. Readers can find a summation on Seeking Alpha, linked above.

Let us get stuck into the details of BHP's recent operations.

BHP Group's 28% year-over-year drop in EBITDA was primarily caused by bad weather, softening commodity prices, and resilient input costs. However, there seems to be a critical inflection point.

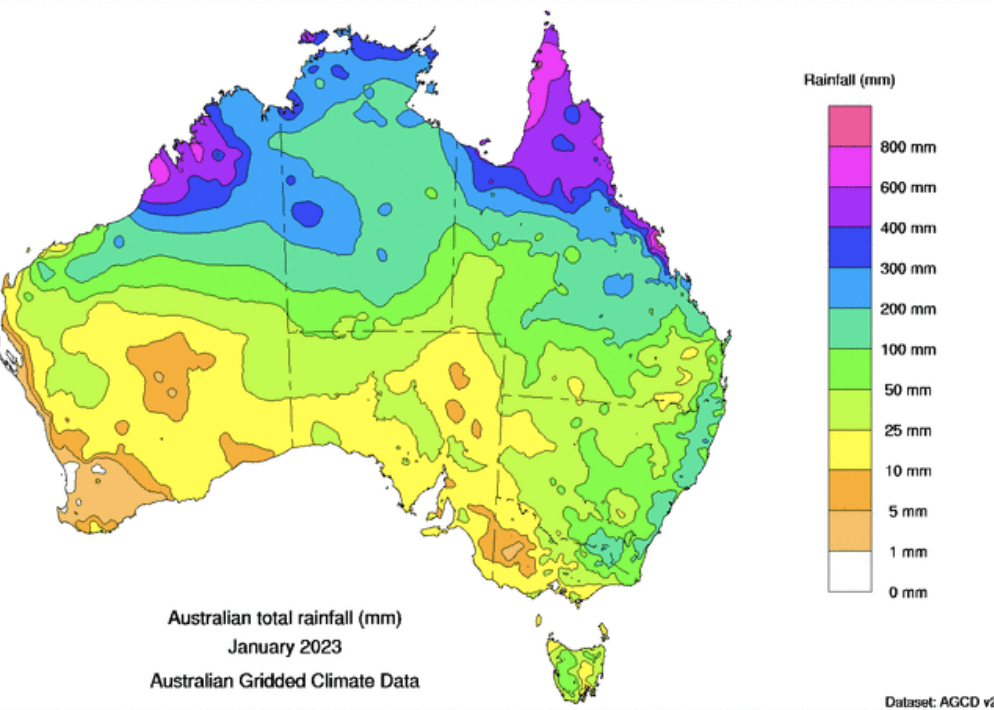

Rainfall has tapered in Australia, especially towards the West, where many of BHP's operations are situated. More importantly, it is forecasted that Australia could soon shift from three years of above-average rainfall to one of the hottest and driest years in decades during 2023.

Coal

An inward look shows that BHP's coal operations were significantly influenced by rainfall in 2022, with the BHP Mitsubishi Alliance project and New South Wales Energy Coal suffering as a consequence. To add more color, the prior had maintenance and operational delays, which were both rainfall-induced, and BHP has since upgraded its outlook for the asset. In addition, New South Wales Energy Coal suffered from lower production, also induced by rainfall.

As our Thungela ( TNGRF ) article mentioned, we are bearish on coal assets, as coal prices are on a severe downward trajectory. However, BHP's operational recovery could offset some of its coal segment's price pressure. The company currently generates approximately 20% of its revenue from coal, which we believe to be a slight risk; however, as mentioned before, an operational recovery might be priced by the stock market.

{kind=link}

Iron Ore

Let us move along to BHP Group's Iron Ore activities.

The company's iron ore division suffered from two critical headwinds in 2022, namely high input costs and lower grades. A uniform observation implies that input costs are tapering as fuel prices , labor disputes, and general material costs are decreasing. Of course, this could also be disadvantageous to BHP Group, as its materials might sell for lower prices. However, the company's historically wide profit margins imply that its input costs are more vulnerable than its top line.

During its latest half-year, BHP's Western Australia Iron Ore suffered from higher-than-expected unit costs. Nevertheless, costs could taper in 2023, as diesel prices and higher-than-normal wage increases were the culprits for higher general costs. And as mentioned before, the general trajectory of both is downward sloping.

BHP undoubtedly suffered from lower ore prices in 2022. However, as most know by now, China's reopening, an abated recession in the EU, and higher-than-expected GDP growth in the U.S. are all seen as factors that could rejuvenate base metals in the coming quarters.

An important idiosyncratic feature to highlight is that BHP's South-Flank ramp-up is commencing as planned, with the potential to add significant value in the coming year. Only the firm's updated geophysical report can tell us how broad-based throughput will end up, which we, unfortunately, do not have direct access to; however, in our opinion, it cannot go much worse for BHP than it did last year.

Copper

Copper's supply and demand profile is much the same as iron ore due to its industrial application and cumbersome mining process. As such, BHP Group's copper throughput suffered for the same reasons as its iron ore operations during 2022. Similar to iron ore, we anticipate unit costs to decrease for systemic reasons.

Escondido is struggling with throughput due to lower grades and concentrator feeds. We do not have much to add apart from the fact that China's reopening could support copper prices and that a recovery of BHP's Spence mine might add value. Furthermore, Spence struggled from delayed shipments in the company's previous half-year due to a fire at Port Mejillones; however, this is a non-core event, and we think there will be evening out in the coming quarters, which will probably coalesce with the promising performance of BHP's underground operation at Olympic Dam to stimulate the firm's copper business.

General Guidance

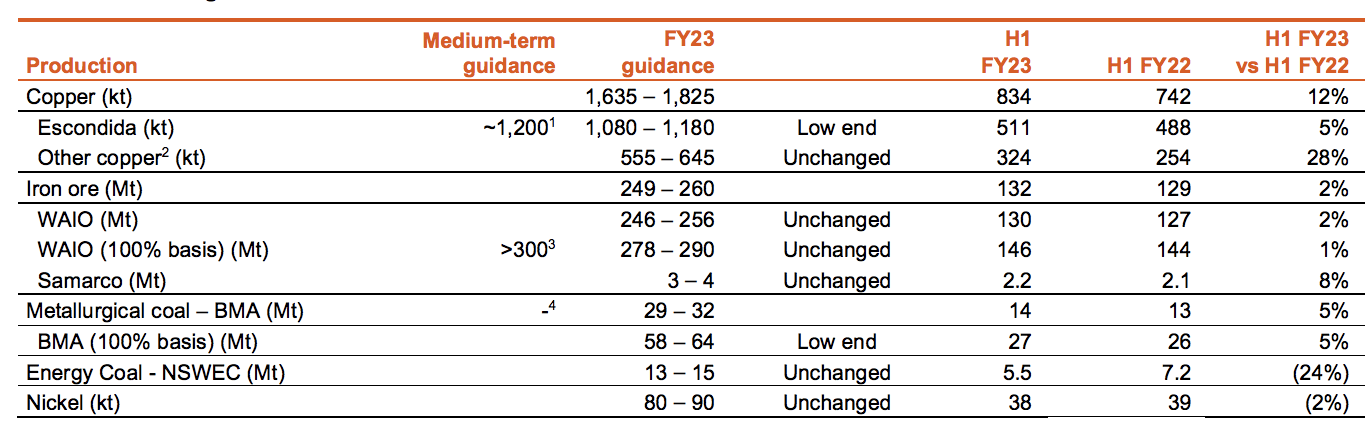

Below is a summary of BHP Group's general guidance and ex-post production. As mentioned, we expect coal volumes to recover and offset lower value. Moreover, we are optimistic about higher volume and value in sales from iron ore and copper.

{kind=link}

A Subtle Change In Direction?

As many might have noticed, BHP Group is altering its operational trajectory. The company has chosen to offload additional coal mines , namely Daunia and Blackwater. In our opinion, this is a move to avoid political pressure. Although coal was critical to many during the past two years, acting as a stop-gap to energy shortages, the global political landscape is fighting against using coal as an energy source, which could alter the supply and demand outlook. Thus, we think this is a clever move by BHP Group.

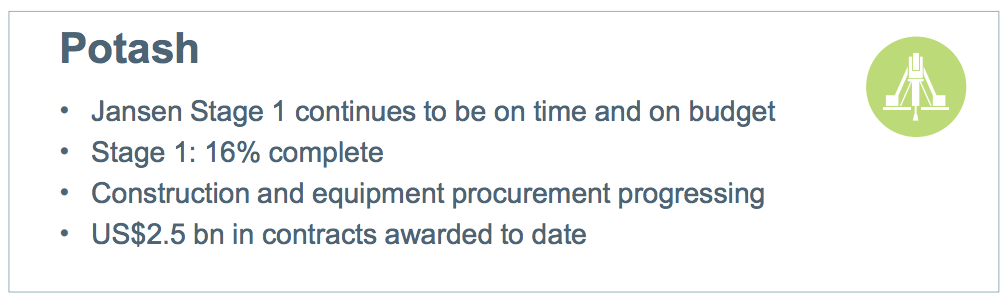

Furthermore, BHP has stated that it will increase its spending on the Jansen Potash mine. The Jansen project is projected to deliver in 2026, and although not expected to be a significant part of BHP's revenue mix, it signals a changing trajectory of the firm's operations, which investors will likely price as a progressive move.

{kind=link}

Valuation & Dividends

I wanted to do a free cash flow-to-equity model for you. However, BHP Group Limited's unwanted negative change in working capital distorted the model. Thus, I decided to keep things simple and look at the stock's price multiples.

It must be admitted that the asset's price-to-book multiple of 3.04 is elevated, especially as it is in line with the firm's cyclical average during a period when recession risk is rife. However, on the other end of the spectrum, BHP's P/E ratio of 9.21 is accommodated by a PEG ratio of merely 0.64, which implies that the company's earnings growth has outpaced its P/E multiple, leaving a potential value gap.

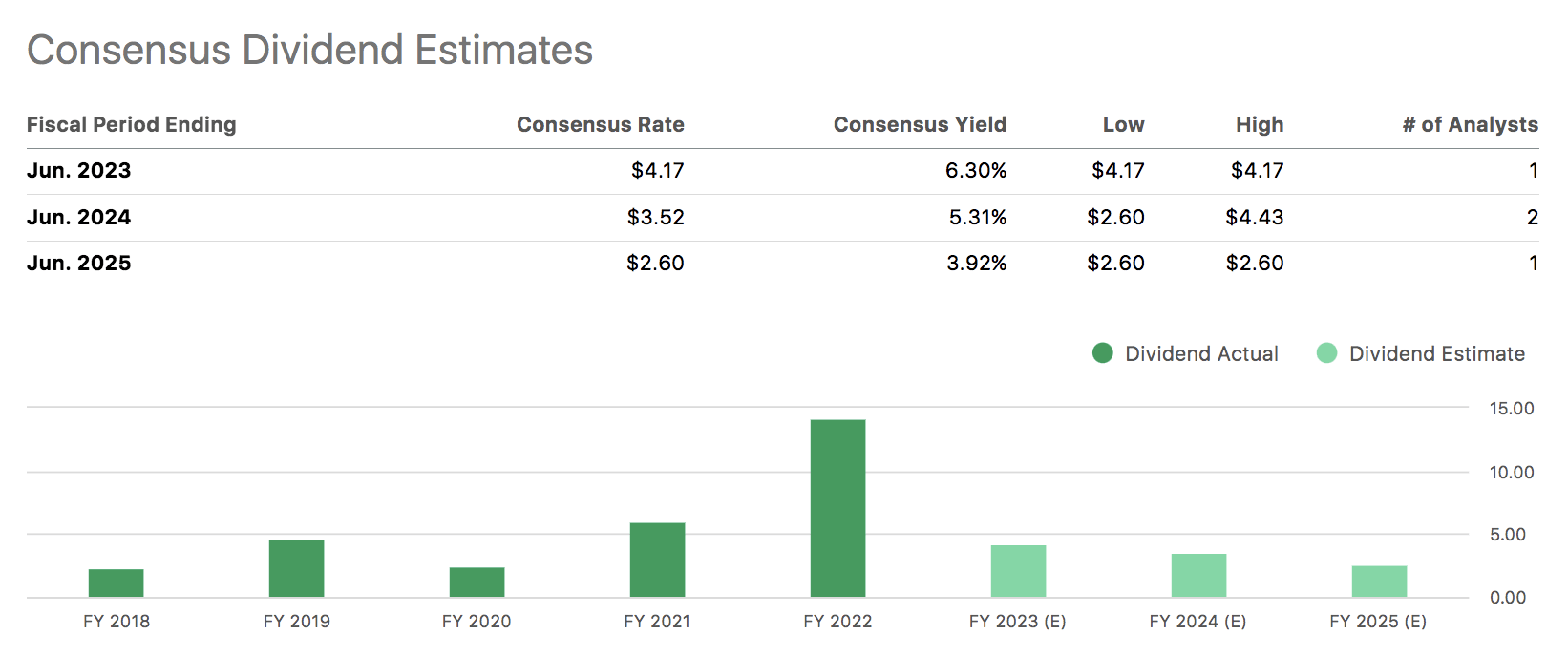

Following its subdued quarter, BHP Group slashed its dividend to 90 cents per share . Analysts' estimates suggest that further dividend decreases might be in the cards as cyclicality plays its hand. However, even the lower bound of BHP's dividend estimate remains alluring. Consider that lower dividends will likely be uniform if the economy resumes its downward trajectory. As such, BHP's dividend might still appeal on a relative basis.

{kind=link}

Noteworthy Risks

Most of BHP Group Limited's risks are outward. Nonetheless, let us first discuss a few inward risks.

BHP's riddance of brownfield coal assets and pivot to greenfield projects such as its Jansen potash mine might be seen as unfavorable by some investors. As a mature stock with an alluring dividend profile, BHP's investor base is probably not the type that is looking for innovation. In reality, most market participants are invested in BHP as a high-quality/dividend play. Will a pivot into greenfield projects cause many of the firm's loyal investors to divest? It is highly possible.

Furthermore, although the China reopening debate holds substance, the media can often overplay such events. It is critical to note that global recession risk remains elevated. Thus, investors should not focus on China's (or Ukraine's) situation in isolation.

Lastly, additional outward-looking risks remain. Cyclical assets, including BHP, have experienced an excellent year-to-date return. However, we could see a reversal in the coming months amid persistent inflation uncertainty in the U.S. and across the globe.

{kind=link}

Final Word

BHP Group Limited 's soft half-year earnings report is disappointing; however, non-structural reasons were involved that caused harm, which might be phased out in the coming quarters.

Although coal price pressure persists, lower rainfall will likely re-ignite BHP's energy operations, offsetting most of the segment's price-related risks. Moreover, an inflection point has been reached concerning inflation, meaning input costs are likely to taper soon.

Furthermore, higher demand for both ferrous and non-ferrous metals could stimulate BHP's prospects during a period when ramp-ups at critical assets are on the horizon. Although we feel the China factor is overplayed, an improved supply/demand framework is highly possible for BHP.

Lastly, it has been announced that the company will pay a lower interim dividend, and BHP Group Limited's price-to-book value is in-line with its cyclical average. Although some might see these variables as discouraging, we argue that dividend decreases will be uniform in today's economy and that BHP remains a "best-in-class" mining stock, which phases out a lot of price risk.

With numerous factors considered, we retain our buy rating on BHP Group Limited stock.

For further details see:

BHP Group: Focus On The Outlook