PFIX - Bidenomics Set For Showdown With Bond Vigilantes Bill Ackman Places Monster Short Bond Bet

2023-08-06 09:23:56 ET

Summary

- Fitch downgraded the US government's credit rating from AAA this week, and famed investor Bill Ackman placed a huge bet against long-term US Treasury bonds.

- Yields are threatening to take out their 2022 highs, and Ackman believes that the 30-year Treasury will hit 5.5%.

- Bond vigilantes are back in full force, and historically large Biden administration deficits are on a collision course with the bond market.

- The stage is set for an epic showdown between Bidenomics and bond vigilantes.

"I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody."

-James Carville

If you don't eat all day and then start knocking back margaritas, you're about to have a terrible hangover. And when governments try to ramp up spending without raising taxes to pay for it, it creates problems. As long as buyers trust that they're likely to get an inflation-adjusted return on their money, government spending can be financed by borrowing. But trust is fragile. When investors get nervous, they start demanding more and more interest to compensate them for the risk of holding government debt. Of course, the government can (sometimes) have the central bank print money to buy the debt instead, but then you start to run the risk that people don't want to take your currency either. When investors start demanding higher interest rates in response to government deficits, they're referred to as "bond vigilantes," because they vote with their keyboards and force governments to cut spending or raise taxes.

Throughout history, governments have battled bond markets that decide to stop financing unsustainable spending. Generally, the market wins by a landslide. George Soros famously made £1 billion betting against the Bank of England in 1992. The Clinton administration was rocked by a bond market revolt in 1994 , and the Obama administration similarly faced a 2009 reckoning on spending that forced it to pare back on bold spending plans. The bond market doesn't particularly care whether you call yourself a conservative or liberal, either. Less than a year ago, conservative PM Liz Truss attempted to cut taxes and boost spending with no money to pay for it , and the ensuing bond market meltdown made her the shortest-serving prime minister in UK history. These kinds of bond market showdowns happen all of the time for smaller countries that don't have reserve currencies, and they barely make headlines.

The Biden administration submitted its updated debt sale plans to the market last week, and the market was not pleased. US Treasury yields rose sharply, threatening to take out last year's highs. The 30-year fixed mortgage hit 7.2%, while jumbo mortgages hit 7.23% . Fitch downgraded US debt to AA+ from AAA, prompting everyone from Warren Buffett to Elon Musk to Bill Ackman to weigh in on the state of the US Treasury and whether it poses a risk to owners of Treasury bonds. The rollercoaster continued on Friday with bonds gaining back much of the losses, but the warning signs are clear.

Bill Ackman's Big Short

Bill Ackman took the boldest stand , sharing on the online platform formerly known as Twitter that he was short 30-year Treasuries ( TLT ) "in size" and offering a 5.5% yield target for the 30-year Treasury. Lest we forget, Ackman made an estimated $2.6 billion betting on credit default swaps during early COVID, declaring on CNBC on March 13th, 2020 that " hell is coming ." This time, Ackman is highlighting structural changes in the economy in backing up his monster short bet:

...de-globalization, higher defense costs, the energy transition, growing entitlements, and the greater bargaining power of workers. As a result, I would be very surprised if we don’t find ourselves in a world with persistent ~3% inflation.

Ackman goes on to say that inflation is likely to average 3% going forward and that investors are likely to demand a 2.5% risk premium on top of it, roughly the historical average. Historically speaking, this isn't that crazy. Inflation has compounded at a 2.56% rate in the US since the turn of the century. That's only 44 bps from Ackman's forecast. TIPs markets are projecting roughly 2.27% inflation over the next 30 years. There's nothing radical in Ackman's inflation forecast– the factors he's citing make it plausible that inflation could be 3%, although my own research suggests a number closer to 2.5%. The trouble is that there's always the risk that the world changes or politicians do something really dumb and inflation is 10% or more annually. We can hope that risk is low, but that's where the risk premium comes in.

Real Yields 1954-2008 (St Louis Fed)

The inflation risk premium for US treasuries is historically about 2-3% . As recently as the Bush and Obama administrations, there were times when real yields on long-term Treasury bonds were 2% or more plus inflation. But after getting burned in the 1970s, gun-shy bond investors demanded much more– and for decades. I don't think Bill Ackman's projections here for a 5.5% 30-year yield are particularly unreasonable if the administration keeps its spending and tax plans in place. After all, that's only 120 bps more than the bonds are currently trading for. And if the market happens to agree with Ackman here, he'll probably make another billion bucks on the trade. I don't know what Ackman means by "in size" but he's clearly playing with the house's money at this point. One feature of macro bets is that many of them are reflexive, i.e. recession bets drive yields lower, which supports the economy. This bet, however, has positive feedback– the more people who believe Ackman's thesis and sell bonds, the more incremental funding pressure it puts on the principal and interest payments the Treasury has to make.

Everyone at the highest levels of society is talking about this, either for or against Ackman's view. Elon Musk tweeted that US Treasury bills are a "no brainer," but did not respond to a Bloomberg request for comments on longer-term bonds. Warren Buffett offered a similar outlook to CNBC .

Berkshire bought $10 billion in U.S. Treasurys last Monday. We bought $10 billion in Treasurys this Monday. And the only question for next Monday is whether we will buy $10 billion in 3-month or 6-month T-bills.

But like Musk, Buffett isn't commenting on the long end of the curve. These aren't exactly ringing endorsements of the US Treasury's borrowing plans. On the bright side, if you believe the government will raise taxes to fix the deficits, then the 30-year bond is offering a reasonable level of long-term compensation.

Why The Bond Market Might Crush Bidenomics

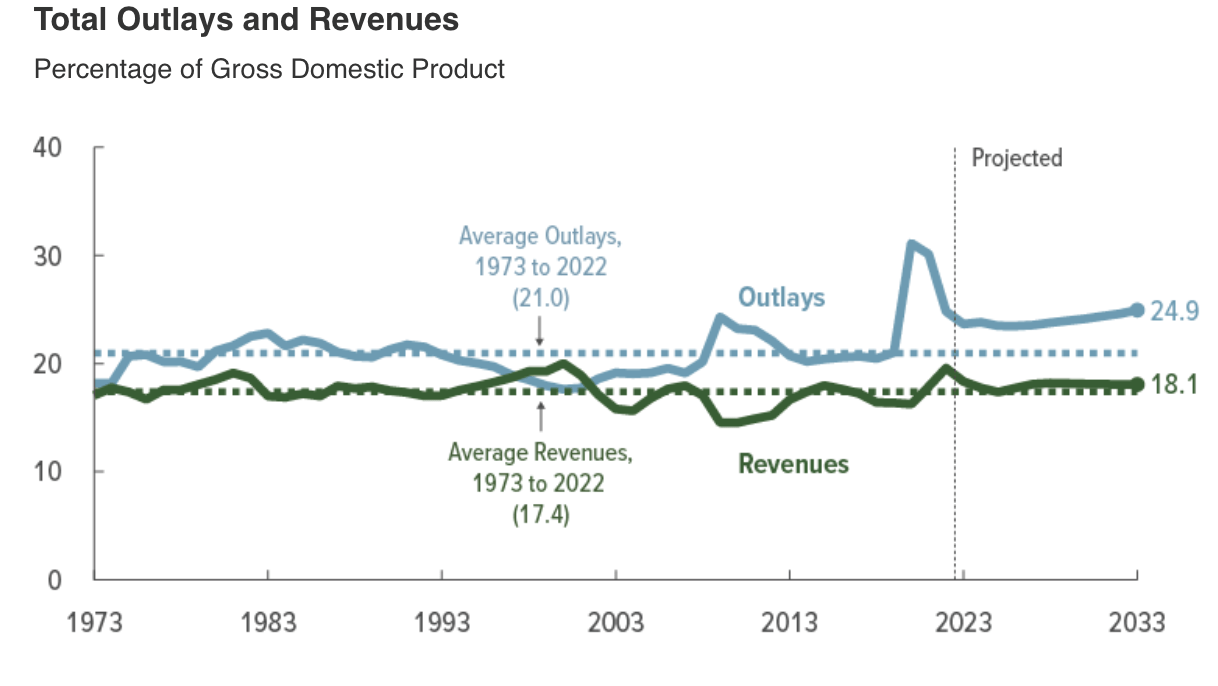

Below, we have February's projections for US Federal government revenues and outlays. We can see that outlays during COVID were the highest in 50 years, while revenue was about average. Spending is still higher than typical, while revenues are actually below their 50-year average. In all, the CBO projected a deficit of $1.4 trillion for FY 2023 in February. That's about 5.2% of GDP, which is a historically high and unsustainable level. A rough guide for the sustainable level of spending is the blue dotted line below.

US Budget Deficit Projections (CBO)

{kind=link}

Since February, the revenue picture has deteriorated. Now, CBO is projecting a budget deficit of about 5.8% of GDP. And this is why the bond market is repricing yields higher. The Treasury is now having to sell hundreds of billions more in bonds, and the market isn't lapping them up. It's an important question here because the Fed is selling $90 billion per month in bonds, and the Treasury is having to sell another $120+ billion per month. Where is the money going to come from to finance the debt? Who's going to buy all of these bonds, and at what price?

In the past 10 years, much of the money came from Europe, Japan, and China, but now Europe and Japan have also raised interest rates. They're now not as keen to pump money into the US. Japan has begun to abandon its yield curve control policy , which turns off the faucet on a huge source of demand for US bonds. For decades, the Bank of Japan kept interest rates at 0% and pushed down long-term interest rates, so Japanese institutions ended up buying US Treasuries and US mortgages instead. I looked for a bit and couldn't find the study, but one source suggested that US mortgage APRs were about 50 bps cheaper than they would have been in the 2010s because of Japan. If you throw in Europe and its experiment with negative interest rates in the 2010s, it's quite possible that US bonds and mortgages would have been about 200 bps more expensive this whole time. If Ackman is right about the 30-year trading to 5.5%, then it's likely that 30-year fixed mortgages would rise further to 8.5% or so. I wouldn't even rule out rates hitting 9% for more economically-sensitive 30-year jumbo mortgages.

This is actually exactly what's supposed to happen when governments try to spend money without raising taxes. Printing money isn't a magic trick, so massive government spending " crowds out " investment in the rest of the economy by raising interest rates. In this case, huge spending on entitlements, defense, and green energy must be financed as there aren't nearly enough taxes to cover it. This could drive interest rates to levels that most people don't even know are possible. This happened last September in the UK, and the result was a crisis that forced the government to cut spending and raise taxes to calm the market.

At each press conference, one reporter or another asks Fed Chair Jerome Powell whether he'll monetize the debt and simply print money to buy the Treasury's debt issuance. In June, Powell was a little more short, simply replying with a one-word "no" to a follow-up question. It's an interesting question– if interest rates do skyrocket due to government dysfunction, then will Powell step in and monetize it? It's possible, but history says probably not. Andrew Bailey and the Bank of England didn't rescue Liz Truss last year, and Alan Greenspan certainly didn't rescue Bill Clinton in 1994.

From a 2011 piece in The Atlantic on bond vigilantes.

Democrats wrestling with the legacy of Ronald Reagan’s deficits resented the influence of what the analyst Ed Yardeni had dubbed “the bond vigilantes”: the investors who enforce fiscal and monetary discipline when governments won’t. If your political system inflates its currency, or fails to align its spending with its tax revenues, the bond vigilantes will raise your interest rates until you either get it together … or catapult into a crisis.

Markets are flashing serious warning signs about the sustainability of Bidenomics here. While current levels of US spending might be justified, the administration needs to raise taxes to pay for its spending, and right now it can't. If you do quick math on income taxes as well, it's incredibly obvious that trying to load all of the taxes on the rich won't work either. The only real way out of the US debt problem is broad increases in income and payroll taxes at every income level or to replace the current system of sales taxes with a euro-style 20% VAT tax. That's where we're headed, but it may take a crisis for us to get there.

Investors who want to coattail Bill Ackman's trade here could consider Simplify's Interest Rate Hedge ETF ( PFIX ), or buying puts on TLT. PFIX is a simpler play, but buying ATM puts on TLT offers roughly a 5-1 payoff if Ackman is right about the 30-year hitting 5.5% by January 2024.

Bottom Line

Janet Yellen and the Treasury have a boatload of US Treasuries to sell over the next 12 months, and the likes of Bill Ackman and the bond market believe they may have some trouble selling it. This isn't about Democrats or Republicans as much as it is about math. Big spending plans need to be matched by taxes, and they aren't. Every $100 billion in additional debt the Treasury has to offload brings the situation closer to a showdown with the bond market. And at this pace, that's roughly what the Treasury will have to offload every 2 weeks. We live in interesting times.

For further details see:

Bidenomics Set For Showdown With Bond Vigilantes, Bill Ackman Places Monster Short Bond Bet