HFRO - Big Fat Yield But Worth The Risk? HFRO

Summary

- We provide an update on a black sheep in the HDO Model Portfolio.

- It had a great 2022, but its checkered past means we're maintaining a Hold status on HFRO for now.

- Is the big discount to NAV worth investing in, or a fool's errand?

Co-produced with Treading Softly.

We have recommended Highland Income Fund ( HFRO ) as a "Hold" in our portfolio since management attempted to convert from a closed-end fund ("CEF") to a holding fund – a move that would dramatically restrict shareholder rights.

Fortunately, shareholders were able to band together and prevent this move. Yet, once lost, trust is very hard to rebuild. We like the assets, we like the potential, and we like the performance through a really tough year.

Today, we take a deeper dive into HFRO. Explaining why we are holding it, and why we aren't willing to endorse buying more.

Market-Beating Returns, But You Shouldn't Buy More

Have you ever known someone who can do a great job, they're very skilled, but you simply can't trust them when left alone?

They know how to do the work.

They are exceptional when they actually do it completely.

Yet, they are untrustworthy enough that they won't do it right unless your presence is known.

It's my biggest pet peeve to have to babysit a skilled individual. Some people simply need that hovering oversight to get the job done right.

When it comes to investing, we often benefit from placing our capital into the skilled hands of others to do the work for us. They make the trades. They manage a portfolio. They pay us the required distributions from their taxable income. Benefiting from the skill of management is one of the main attractions of investing in closed-end funds.

Yet at times, some managers try to pay games to keep more for themselves or potentially shirk responsibilities tied to operating a fund.

High Dividend Opportunities came toe to toe with one such fund and manager who continues to post solid returns and results but is now one of those "need babysitting" type investments we usually do not like to hold.

Which Fund Requires Babysitting?

Highland Income Fund trades at a deep discount to its net asset value. One of the main draws for a closed-end fund is getting a great deal. However, not all discounts and premiums on funds are created equal. Management trust and fund positioning can play a critical role in determining what is a good value when investing in a fund.

In more recent memory, investors might remember that HFRO tried to convert from a registered investment company to a diversified holding company. Investors shot that proposal down, and HFRO withdrew the plans. They tried again and, after delaying the vote, finally scrapped their plans. While that isn't a negative in itself necessarily, HFRO is a type of fund that you want to get as much transparency as possible.

Fortunately, despite HFRO's issues, the discount at this time is looking rather tempting as it's trading at a level that factors in the issues for this fund. That helps compensate for the riskier profile of this fund and its management shortfalls. Let's evaluate where HFRO stands now to see if this temptation is worth investing in, or a fool's errand.

Performance Was Attractive in the Last Year, but a Caveat

One area that stands out is HFRO's relatively attractive results through 2022. That was when most other investments were struggling, whether you look at equity or fixed-income investments. Unless you were heavily invested in energy - which a truly diversified portfolio would have some allocation - chances are you experienced some losses.

When comparing HFRO to the S&P 500 ( SPY ) and the general bond market ( BND ), we can see clearly that HFRO must have been doing something right.

{kind=link}

However, this is where the caveat comes into play. The fund is most heavily invested in real estate. They listed that as 72.8% of their portfolio at the end of Q3, 2022. Source .

HFRO Fact Sheet

You might now be thinking, wait, real estate was down last year quite meaningfully. You'd be right, too, of course. Vanguard Real Estate ETF ( VNQ ) can help represent the overall real estate space. That exchange-traded fund ("ETF") dropped over 26% on a total return basis in 2022.

So how did HFRO navigate such a large drop? It came down to their portfolio being primarily allocated to private investments or level 3 securities. These are securities valued with "significant unobservable inputs." Essentially, they are valued as best as they can be but aren't necessarily exactly what one would be willing to pay.

Blackstone ( BX ) provided a bit of a taste of that. Investors flooded them with redemptions for their non-listed BREIT fund because the NAV was holding up so well that publicly traded investments looked a lot more tempting. They wanted to cash in on assets that retained their valuation through what was a terrible year for publicly traded REITs. The imbalance between these investments helped to trigger these redemptions.

As a private investment, they have limits for redemptions to stop forced liquidations. So the actual redemptions didn't have anything to do with weakness in BREIT, but its strengths. BX wasn't alone, as Starwood Capital Group had also hit redemption limits.

Back to HFRO more specifically, though, in their last report , they listed that around 70.65% of their portfolio was in level 3 securities. That's massive and is one of the largest weightings to level 3 securities we've seen in the entire CEF space.

This is another case where on its own, level 3 securities aren't a detriment. In fact, that's one of the benefits of CEFs, to invest in these more illiquid securities. However, the Highland management team has had an issue with valuing these securities in the past.

HFRO hasn't run into this issue specifically, but the sister fund, Highland Global Allocation ( HGLB ), has. It was more specifically in their highly concentrated TerreStar investment. They misstated the NAV, and that error caused a miscalculation in the fund's NAV.

TerreStar is a position in HFRO as well. It is several positions as they hold common shares and several loan positions. The cost of the common stock position was listed at $3,093,276. The fair value at the end of June 2022 was listed at $9,670,015. Based on the end of September N-PORT , this fell only a touch, showing the value was $9,578,573.

Certain of the Fund’s assets are fair valued, including the Fund’s investment in equity issued by TerreStar Corporation (“TerreStar”). TerreStar is a nonoperating company that does not currently generate substantial revenue and which primarily derives its value from licenses for use of two spectrum frequencies, the license with respect to one of which was granted a conditional waiver by the FCC on April 30, 2020. The fair valuation of TerreStar involves significant uncertainty as it is materially dependent on estimates of the value of both spectrum licenses.”

Still, it's these types of positions that make the portfolio so uncertain. TerreStar produces no services or products. Instead, they have licenses for two spectrum frequencies. That's despite the wording of "does not currently generate substantial revenue..."

Their HGLB annual report states differently. In their report, they list that TerreStar "does not currently generate revenue and primarily derives its value from holding licenses in two wireless spectrum assets." It is also mentioned that management is assigning the valuation with a high probability of success. Given the cost of the TerreStar investment for HFRO relative to the current valuation they assign the position, I'd say it is quite optimistic.

The idea of the investment is great. It's one of the more compelling reasons to own HFRO or even HGLM. Spectrum is a rare resource, but TerreStar is having difficulty capitalizing and executing on it at this point.

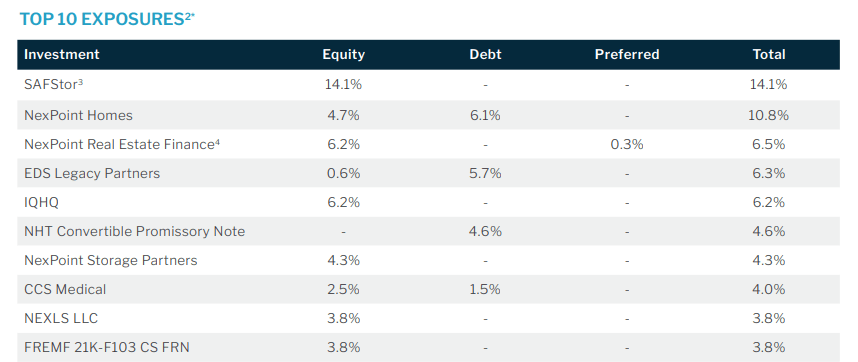

High Concentration in Affiliated Names

Speaking of highly concentrated holdings, that's a common trait with HFRO. Another reflection of why the fund's discount is large. With higher concentration, management needs to get it right more often than not to perform well. The top two positions alone make up almost 25% of the fund.

{kind=link}

I would also note that they carry several NexPoint investments. That includes NexPoint Homes, NexPoint Real Estate Finance, Inc. ( NREF ), NHT Convertible Promissory Note, NexPoint Storage Partners, and NEXLS LLC. Five of the top ten names here are affiliated investments through NexPoint, with NexPoint Asset Management as HFRO's fund sponsor.

That's just on the surface. The SAFStor position is held within NFRO REIT SUB, LLC. In total, they listed that over 70% of the fund is invested in affiliate investments; "Affiliated issuer. Assets with a total aggregate fair value of $738,886,730, or 70.5% of net assets, were affiliated with the Fund as of June 30, 2022." That nearly matches the same to level 3 securities.

This means that while not being able to convert away from a CEF, HFRO's management has been actively investing in their own private-type holdings and using level 3 observations to determine their value.

Potentially Worth Considering for Several Reasons

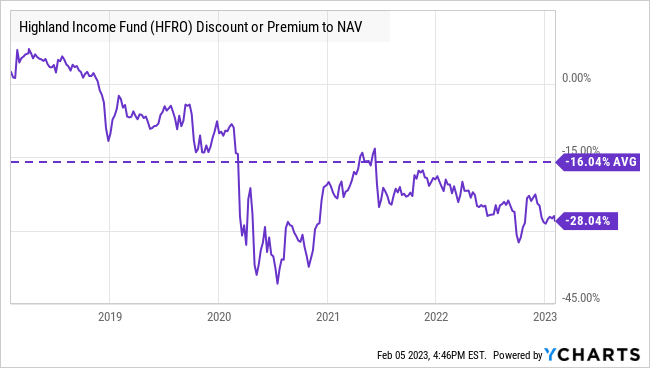

Touching on the topics above, reflect why the fund trades at a deep discount. It helps reflect why discounts on closed-end funds can exist in the first place. It's our job to find out if it is still worth holding such a position in the end, and that answer is yes. A big reason is that the current discount has already factored in these risks.

The only time the fund traded at a wider discount was during the COVID crash when CEF discounts widened significantly across the board. It's trading well below its average discount, going back more than five years.

{kind=link}

An additional catalyst for the fund can come from Credit Suisse Group AG ( CS ) paying HFRO what it is due. This has been a long-running case because CS keeps it going instead of paying the $121 million that is due. At least, that was the amount due as of June 28. That amount is subject to change and potentially increase as it accrues interest. Source .

The total aggregate award, which, as of June 28, stood at $121 million, consists of damages and prejudgment interest. The award will continue to accrue interest until the appeals process is exhausted. Any final judgment amount would be reduced by attorney fees and other litigation-related expenses. The net proceeds would then be allocated to the Funds based on respective damages (approximately 82% to HFRO). As legal proceedings are ongoing and all recoveries remain contingent, no award amount has been recorded in the Funds’ net asset values at this time.”

The amount of HFRO's allocation is approximately 82%. That would be around $99.22 million for the fund. Shares outstanding were roughly 68.036 million. That would increase NAV for HFRO to jump by $1.46, given the latest data. It ultimately would lead to NAV being $15.67 based on the last NAV reported, extending the fund's discount from an already generous 28% to nearly 35%.

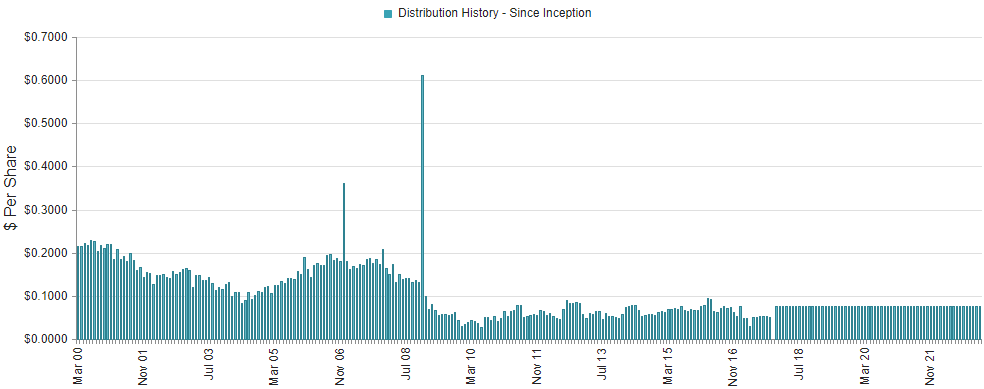

Steady Dividends for the Foreseeable Future

An income investor can also benefit from this as an income play. This is one steady dividend you can get in a market that's been quite volatile. They pay $0.077 per month and have for several years. Prior to this, they paid a variable distribution but have provided this much more predictable amount.

{kind=link}

Based on this massive discount, investors can collect a steady 9%. The annualized distribution rate on NAV comes to a shallow 6.5%. That's another main benefit of buying highly discounted CEFs; investors receive much more than the fund has to earn.

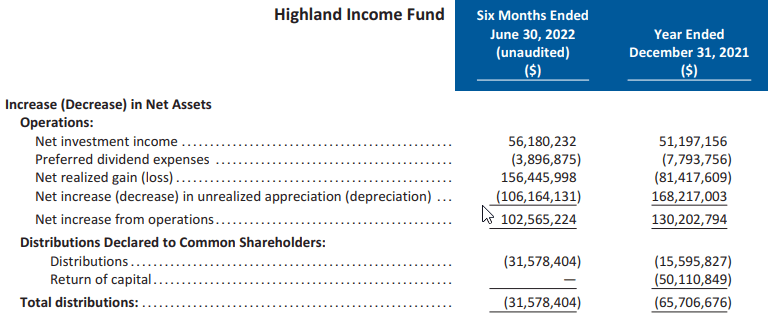

In their latest report, net investment income reached over $56.180 million. That was against the $31.578 million paid, resulting in distribution coverage of 180%. Even factoring in the $3.9 million paid in preferred dividends, coverage was strong.

{kind=link}

At the same time, the return of capital has been a component of the dividend paid to investors. Some investors immediately write off a fund that has any return of capital or ROC in their dividends. However, this is a tax accounting term, not a performance one. We saw above that the fund earns more than enough income to cover the payout to investors.

It benefits new shareholders as ROC payments reduce an investor's cost basis rather than getting taxed when receiving. It is a way to defer tax obligations, potentially for years, if one never sells or realizes a gain. Yet, the income being paid spends the exact same as any other ordinary income.

{kind=link}

The reason for this ROC is quite simple, as they have capital loss carryforwards to offset capital gains.

{kind=link}

They have realized a significant amount of capital gains in the last year, but given the amount of carryforward losses listed previously, they haven't utilized this whole pool.

Conclusion

Not all CEF discounts are what they might first appear. Some reflect uncertainty for any number of reasons. In HFRO's case, the management team is the driving force behind the large discount.

When a management team is shareholder friendly, we can often see CEFs trading at wide premiums to NAV. The fund is rewarded for its friendly management. However, with HFRO, the discount is driven by investors' distrust of management and management's attempts at self-dealing via private investments. The value of which is subjective – we know that when you value your own holdings, often you think they're more valuable than others do.

This is why High Dividend Opportunities continues to rate HFRO as a hold. We do not recommend trusting HFRO's management team with more of your capital, but they have been decent stewards of what may have already been provided.

HFRO's NAV has remained high, they have the pending award from CS, and it is easily covering its current distribution with cash flow. Several of Highland's non-traded REITs have had successful IPOs, like NexPoint Real Estate Finance in which HFRO still holds a large position.

Usually, when management is self-rewarding, we prefer to be higher in the capital stack, such as with The Necessity Retail REIT, Inc. ( RTL ), where we hold positions in the preferred securities. However, HFRO's preferred yields only 6% and is unattractive compared to higher-yielding options in the HDO Model Portfolio.

HFRO has a portfolio that has been performing well. It is covering its distribution, and we can expect that to continue. It does hold assets that could produce upside. It has a pending court case where it will likely get an award that is material compared to its NAV. The only problem with HFRO, is that management tried to pull a fast one. An effort that failed, but we need to remain vigilant that they might try again.

We are continuing to hold but are not willing to put more money in since management has revealed its colors.

For further details see:

Big Fat Yield, But Worth The Risk? HFRO