SLP - Big Pharma's AI Ambitions: The Countdown For Simulations Plus Begins

2023-10-26 13:38:28 ET

Summary

- Simulations Plus reported strong Q4 2023 results, with an 11% YoY revenue growth and a 33% increase compared to the previous quarter.

- The company's valuation is high compared to its financials and growth prospects, and it faces intense competition from generative AI.

- There are no potential catalysts on the horizon that could significantly boost the company's results or competitive position in my view.

Simulations Plus ( SLP ) is an intriguing company specializing in software for the pharmaceutical industry. It recently reported its FY 2023 figures , showing revenue growth of 11% year-over-year and a 33% increase compared to Q4 2022. The quarter performed well across the board, aided by the acquisition of Immunetrics , which introduced the company to the immunology and oncology segment.

However, after evaluating the business and the financials of Simulations Plus, I believe a SELL rating is appropriate. My investment thesis is based on two key factors:

- The valuation is notably high compared to the current financials and growth prospects.

- The company is seriously threatened by the advent of generative AI, which is drawing intense competition backed by far more substantial capital than what Simulations Plus can allocate to R&D.

Moreover, there don't seem to be potential catalysts on the horizon that could substantially boost the company's results or competitive position enough to justify its valuation.

Simulations Plus: Business Model

Simulations Plus offers a wide range of software for the pharmaceutical industry, but its core product remains GastroPlus®. GastroPlus® is a simulation software used to study a drug's interaction with human metabolism depending on its intake mode: oral, intravenous, ocular, inhalation, and so forth. What percentage of the active ingredient will be genuinely absorbed? How quickly? How will it interact with our body's cells? GastroPlus® addresses these questions using its internal artificial intelligence and machine learning system. Considering the challenges, duration, and costs of conducting clinical trials, having such predictive software is undeniably beneficial.

After the 2017 acquisition of DILIsym , the company also emerged as a specialist in predictive models for the treatment of nonalcoholic fatty liver disease (NAFLD). Over time, acquisitions have become the primary growth driver for the company, which generally uses its cash on hand for dividend distributions and M&A activities. In contrast, in-house product development isn't a focus for the management, which might limit their capacity to innovate on a new winning product like GastroPlus®. There's no limit to the value a company can create through innovation. However, in acquisitions, getting a deal at a price far below the actual value of the acquired asset is challenging.

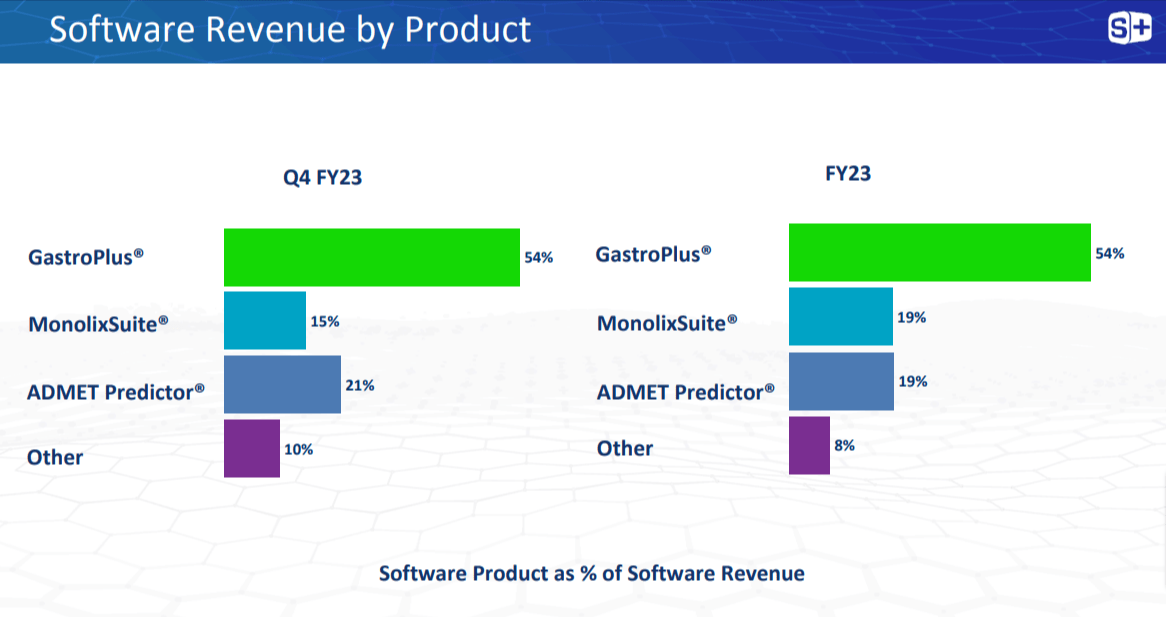

Apart from software, the company also provides consultancy services to firms that may lack the expertise or interest to conduct the simulations independently. Currently, 60% of the revenue comes from the software segment, with the remaining 40% from services.

SLP Earnings Presentation | Q4 2023

{kind=link}

A Look at the Financials

Below is a table presenting the primary financial data for Simulations Plus (figures in $ millions, sourced from Seeking Alpha until 2022. For 2023, data has been sourced from the FY earnings presentation).

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| Revenue |

| 4.1 |

| 29.7 |

| 34 |

| 41.6 |

| 46.5 |

| 53.9 |

| 59.6 |

| Revenue growth |

| -39.71% |

| 624.39% |

| 14.48% |

| 22.35% |

| 11.78% |

| 15.91% |

| 10.58% |

| Gross profit |

| 17.8 |

| 21.7 |

| 24.9 |

| 30.9 |

| 35.9 |

| 43.1 |

| 47.9 |

| Operating income |

| 8.9 |

| 10.3 |

| 10.6 |

| 11.6 |

| 11.3 |

| 14.9 |

| 8.7 |

| Net income |

| 5.8 |

| 8.9 |

| 8.6 |

| 9.3 |

| 9.8 |

| 12.5 |

| 9.9 |

| Total debt |

| 0 |

| 0 |

| 0 |

| 0.9 |

| 1.3 |

| 1.4 |

| 0.9 |

| Cash & Equivalents |

| 6.2 |

| 9.4 |

| 11.4 |

| 49.2 |

| 37 |

| 51.6 |

| 57.5 |

| Dividend per share |

| $0.20 |

| $0.24 |

| $0.24 |

| $0.24 |

| $0.24 |

| $0.24 |

| $0.24 |

Guidance for the upcoming year, released alongside the FY 2023 results, forecasts revenues in the range of $66-69 million. This confirms the company's current annual growth rate hovering around 10%, which isn't much for a software firm connected to artificial intelligence.

What surprises me most is that the R&D investments have been under $5 million over the past 12 months, despite the wide range of software the company manages and especially considering the buzz in the AI segment.

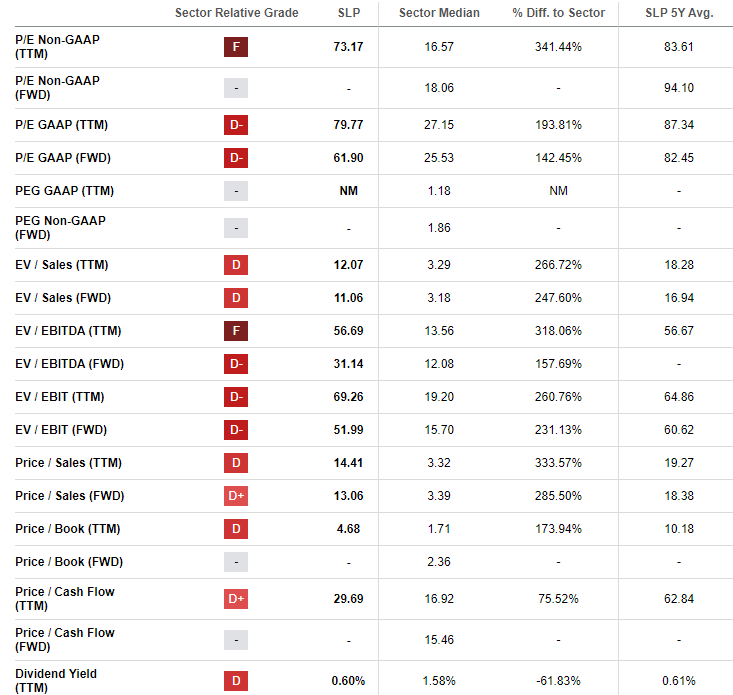

Valuation

Over-valuation is a core theme buttressing my investment thesis. Hence, it's unsurprising that the stock plummeted following the Q4 2023 data release, despite the company essentially hitting its targets. The valuation data from Seeking Alpha will further elucidate this.

{kind=link}

As evident, Simulations Plus has been overvalued not only recently but consistently over the past five years. Employing a DCF model to analyze this firm seems redundant. The AI domain is in a state of rapid flux, and projecting the sector's prospects over the next decade for a company like Simulations Plus seems impractical.

However, my estimation suggests that, given the current risk-free rate and using the stock's average Beta over the last five years for volatility measurement, the WACC stands at around 13.60%. Justifying the company's valuation based on cash flows, with such a high weighted cost of capital and a current price/FCF ratio of 29.89, is indeed challenging. It's highly likely that the discount rate for cash flows will exceed the growth of free cash flow, indicating a need for a considerably lower price/FCF ratio to validate the company's valuation or even justify using a DCF model for analysis. The valuation screams of a growth company, but the annual growth figures don't support it, and there are no positive catalysts on the horizon in my opinion.

Rising Competition: A Major Hurdle

Pharmaceutical firms are increasingly harnessing AI's capabilities for predictive modeling. Here, we're talking about pharmaceutical giants with billions invested in R&D, capable of forging partnerships with leading AI companies. Some notable examples include:

- Pfizer (PFE) is leveraging AI to expedite drug approval processes, mainly by generating data, documents, and tables for regulators.

- Sanofi (SNY) is heavily investing in its AI model, plai, to optimize the drug discovery process and clinical trials.

- Johnson & Johnson (JNJ) is developing an AI model to better understand and address chronic inflammation processes. Janssen even published a blog post titled "Artificial Intelligence is helping revolutionize healthcare as we know it."

- AstraZeneca (AZN) is teaming up with Oncoshot to devise more efficient and meaningful clinical trials using AI.

This list could go on. The commonality here is the novelty; most of these initiatives commenced in 2021 or later. With billions pouring in from venture capital funds eager to invest in AI, I believe we can expect disruptive startups to emerge rapidly over the next 5-10 years.

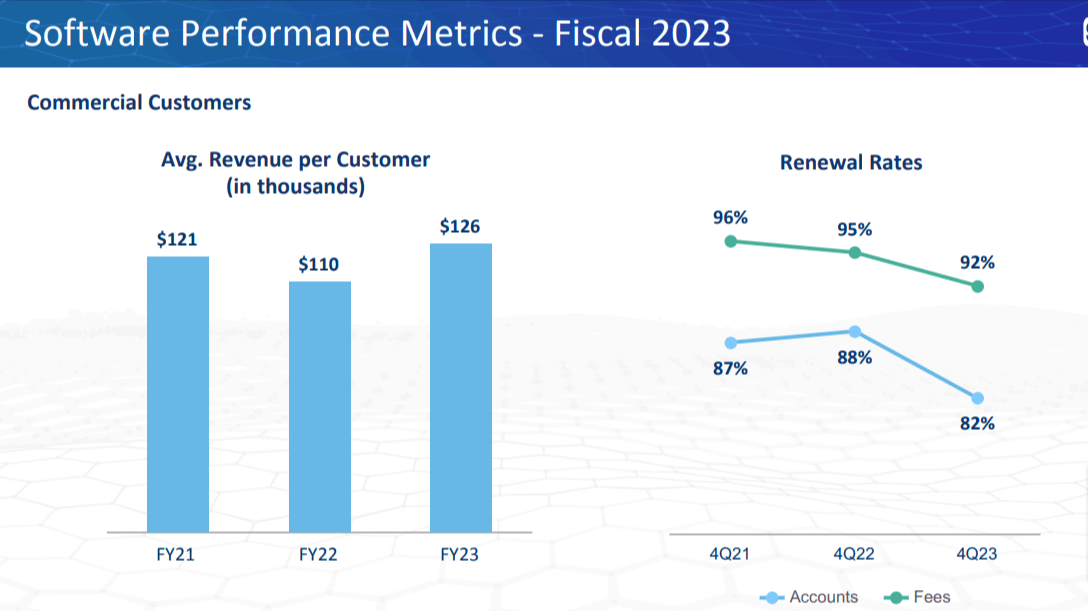

In this evolving landscape, Simulations Plus's software portfolio is on a collision course with the advancements major companies are making in AI. Currently, the only silver lining I see for the company is a potential acquisition by a behemoth wanting to hasten its adoption of predictive algorithms based on machine learning. The company's competitive stance looks bleak in the medium term, especially considering this significant uptick in high-level competition. It's noteworthy that, as per data disclosed in the latest investor presentation, the contract renewal rate has seen a noticeable decline.

SLP Earnings Presentation | Q4 2023

{kind=link}

Concluding Thoughts

With the advent of AI, the lines between pharma and tech are blurring. While Simulations Plus has no inclination to produce its own drugs, its tech segment's growth pace doesn't seem to justify the stock valuation. Simultaneously, big pharmaceutical giants are more eager than ever to integrate a robust tech component into their operations.

I believe Simulations Plus has a window of 2-3 years where its technology will remain a viable acquisition target, especially considering GastroPlus®. The pharmatech boom is in full swing, and I think Simulations Plus needs to be acquired before models from companies like Sanofi or J&J can replicate its functions and more. Otherwise, I predict the company will struggle to stay relevant in the market, and its software will become non-competitive with what future AI can achieve.

For further details see:

Big Pharma's AI Ambitions: The Countdown For Simulations Plus Begins