NSA - Big Yellow: Sluggish Macros Indicate Near Term Weakness

2023-12-15 09:42:58 ET

Summary

- Big Yellow Group's stock might have seen a significant 9% uptick at the last close, but it's still trading a tad below even its pre-pandemic highs.

- A softening in revenue growth and divided verdict on various market valuations risk keeping the stock in limbo at best and fluctuating at worst.

- Over the long term, it has much promise as online sales continue to grow, increasing demand for business storage in particular. But a soft UK economy suggests caution for now.

The UK-based self-storage real estate investment trust [REIT] Big Yellow Group (BYLOF) saw its biggest gain year-to-date [YTD] of 9.15%, presumably after it got the planning permission for a 58,000 square-foot storage cente r in London recently. This is a marked change in the stock's performance, which had seen just a 3% uptick YTD until yesterday.

But the key question now is whether the latest update is the pivotal shift required to get the stock rallying again, considering that in the post-pandemic come-off, the stock is still trading a tad lower than early 2020 highs (see chart below).

Price Chart (Source: Seeking Alpha)

{kind=link}

A promising business market

To get a perspective on Big Yellow, the first point to note is the potential in the business self-storage segment. While self-storage for personal use brings in the bigger part of the company's revenues, revenues from the business at 33% of the company's total sales as of its last financial year (2023, ending March 2023) is not small by any stretch either.

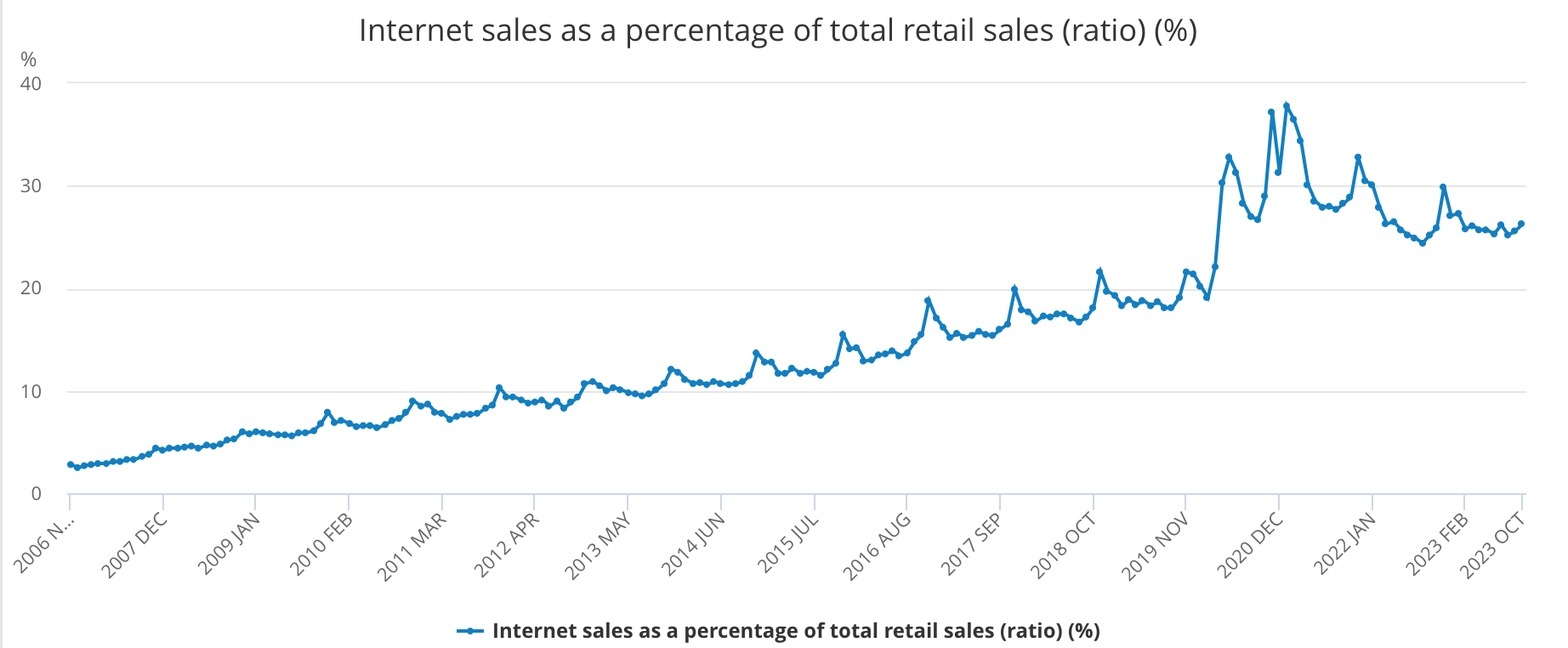

The company sees promise in the segment for several reasons, the key among which is the growth in digital shopping. This was made most obvious during the pandemic, as online retail sales share in total sales reached a peak during the time in the UK. But going by the trends post-pandemic, it's clear that there has likely been an upward shift in the online retail demand curve for good. The share of internet sales is still strong at 26.3%, a significant increase from the pre-pandemic numbers (see chart below).

Source: Office of National Statistics, UK

{kind=link}

Big Yellow also notes opportunities in the self-storage market due to limited penetration in urban areas, and limited new supply and demand for flexible business warehouse spaces (see Pg 2 of the link). Further, businesses tend to rent areas 3x bigger than those required for personal storage and their demand tends to be stickier too.

Softening revenue growth, good profits

However, for now, the company's demand is actually softening, with revenue growth at just 6% year-on-year (YoY) for the first six months of the current financial year (H1 2024), down from 10% for the full year 2023.

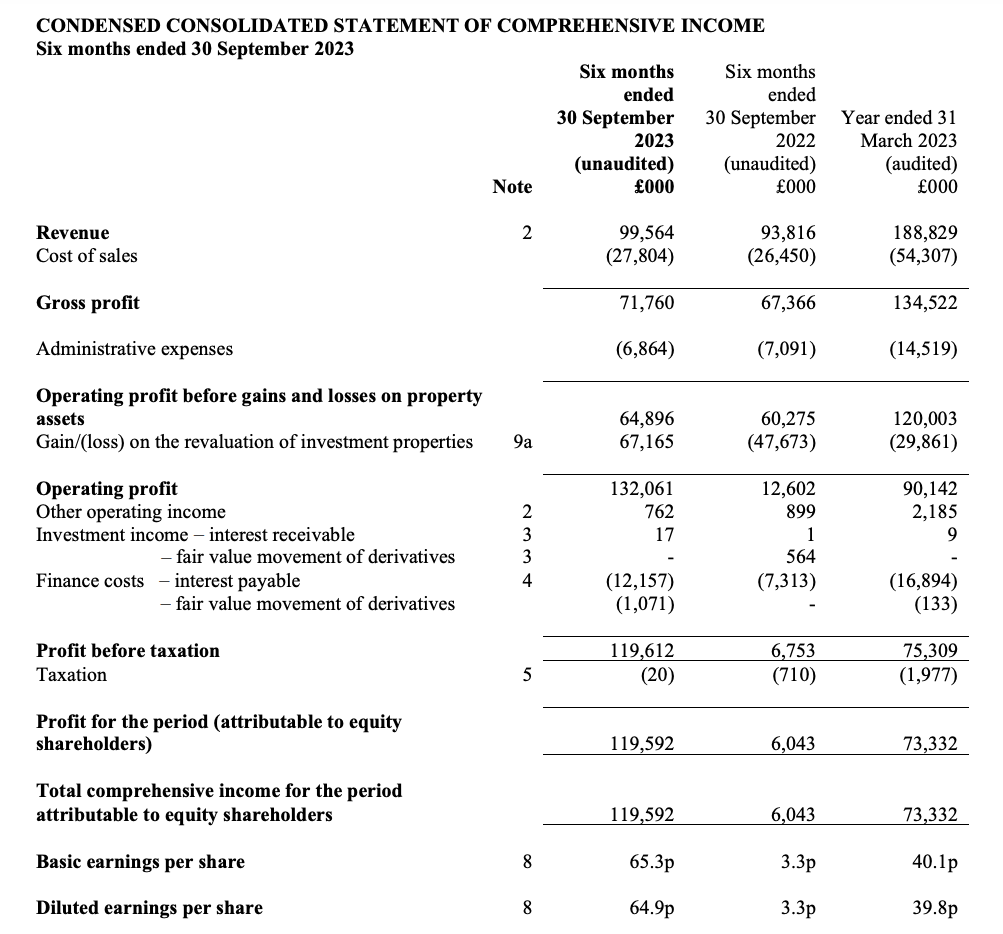

The profits are noteworthy, though. The net profit attributable to shareholders is higher than total revenues due to huge gains on the revaluation of investment properties (see chart below). As a result, the diluted earnings per share [EPS] have risen by almost 20x YoY.

{kind=link}

The market multiples

For this reason, however, it’s imperative to consider an alternative market multiple for Big Yellow for now to ensure the reading on the stock isn’t skewed. Its price-to-operating income ratio is at 23.4x, which objectively doesn’t look small, but it also doesn't look overvalued compared to its self-storage REIT peers by market capitalization. The US-based National Storage Affiliates Trust ( NSA ) and CubeSmart ( CUBE ) have a ratio of 23.65x and 26.9x, respectively. At the same time, especially in comparison with NSA, it doesn't have much upside either.

Another alternative valuation, which is the comparison with the tangible book value per share, indicates fair valuation too. The number is at USD 15.05 as of September 2023, which is a bit lower than its last closing price of USD 15.36.

A third alternative valuation, price-to-funds from operation (P/FFO) which is key for REITs, however, shows a substantial 25% potential upside for Big Yellow. This is because the stock is trading at 12x on a TTM basis, which compares with 13.83x for NSA and 16.4x for CUBE.

Consider long-term total returns

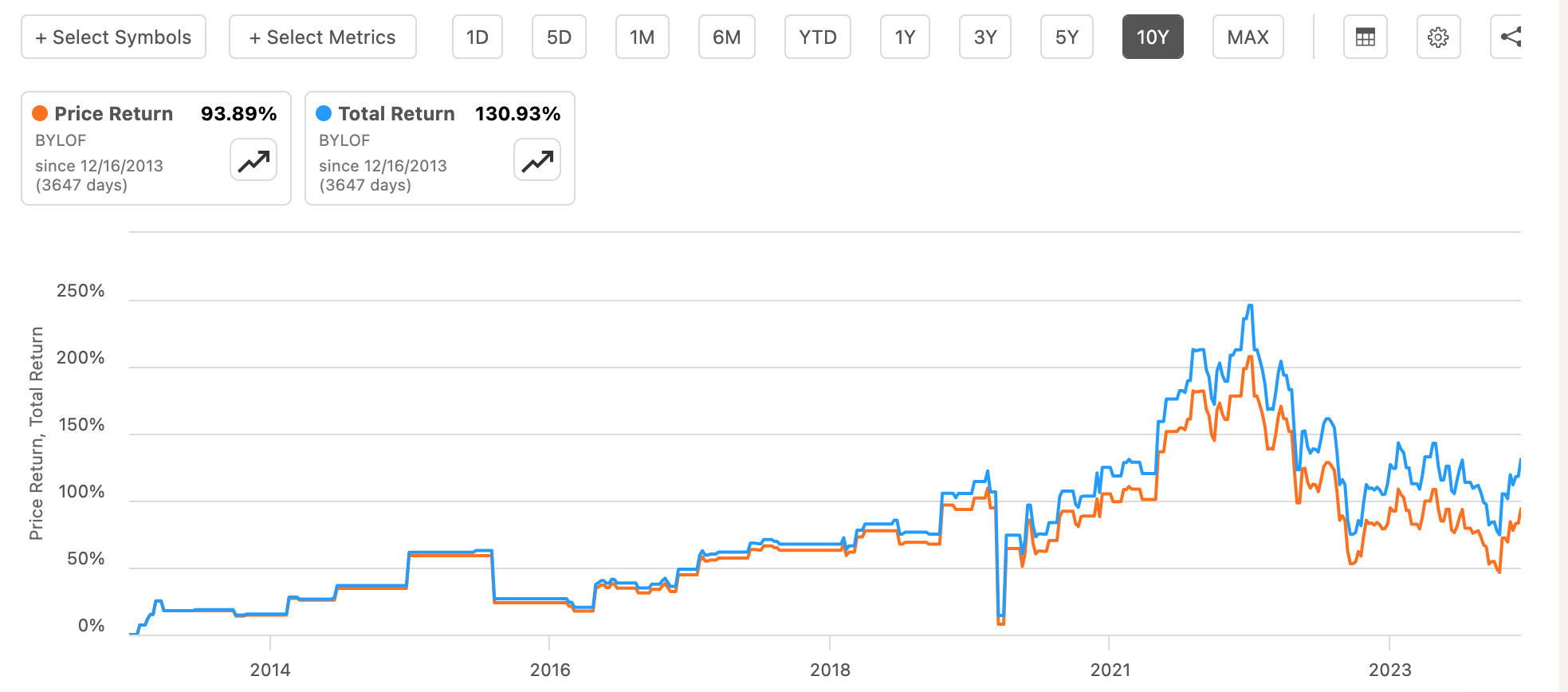

The stock’s total returns are worth considering too, more than just the potential price gains. Over the past decade, the total returns have been at 131%, which is 37 percentage points higher than just the price returns (see chart below).

Price and Total Returns, 10y (Source: Seeking Alpha)

{kind=link}

This is directly related to the company’s healthy dividend yield of 3.15%, on average, over the past four years. Its forward yield also looks fine at 4%. It is, however, lower than the industry average forward yield of 4.7%, which indicates that there could be better returns elsewhere in the sector.

The macro risk

I’m also uncomfortable with the recent trends in the UK’s retail sales. In October, the rolling three-month sales volumes declined by 1.8% YoY . At the same time, the value rose by 3.5% reflecting continued inflation in the market. More specifically, it indicates that consumers could buy less because prices have risen as much as they have in recent years, which isn't a good sign.

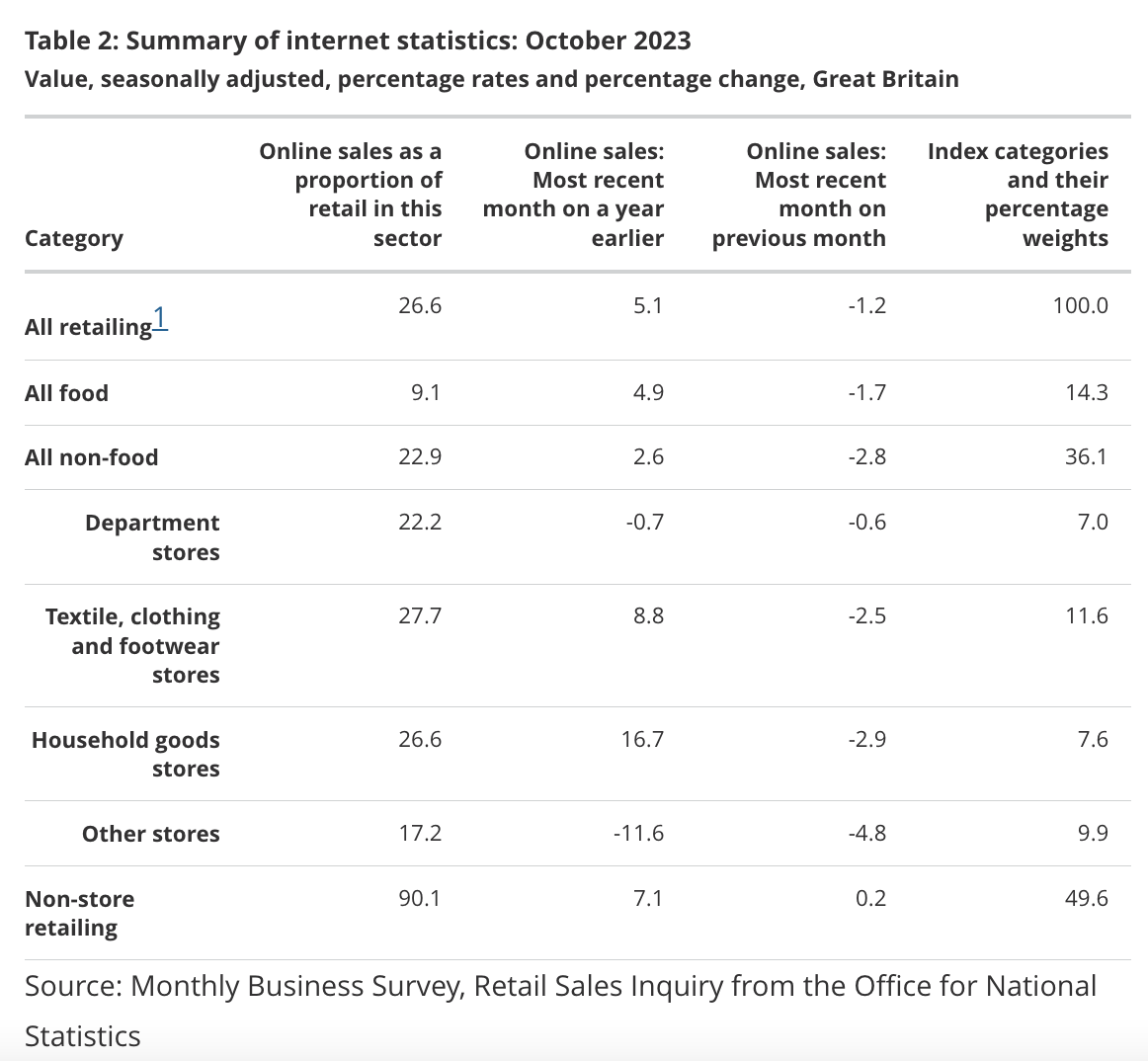

Zoning into online sales reveals that on a seasonally adjusted basis, sales in October declined by 1.2% month-on-month in value terms as well. They’ve done much better on a YoY basis (see table below), but it’s evident that the segment isn’t seeing a clear uptrend. Essentially, future growth in the business segment for Big Yellow looks uncertain for now as a result.

Source: Office of National Statistics, UK

{kind=link}

Further, the weakness in the retail sales data is also reflected in the latest GDP numbers for the economy, which has shrunk MoM in October. While the UK is still expected to show 0.6% growth in 2023, this is a small number. And 2024 isn’t expected to be much better at 0.7%, though the numbers can vary across forecasters. A weak economy as such might be detrimental to not just business, but personal self-storage requirements as well.

What next?

Weak retail sales trends, coupled with muted forecasts for the UK economy indicate caution on Big Yellow. Additionally, its fair valuation compared to peers on both price-to-operating income and in comparison with tangible book value per share indicates limited upside.

On the other hand, its P/FFO does point to a healthy upside. Further, over the long term, however, it still has a lot going for it. It’s in the right industry at the right time with a broadly rising share of online sales in total sales over time, which in particular indicates potentially increased demand for business storage. Along with this, the company’s dividends have resulted in nice returns over the past ten years.

On balance though, to go back to the initial question, I'm not entirely convinced if the stock is at a point where it can see a continued rise, despite the P/FFO indicating as much. For a long-term investor, now might be as good a time as any to buy the stock, but some caution is required for the short to medium term. For this reason, I'm going with a Hold on Big Yellow Group.

For further details see:

Big Yellow: Sluggish Macros Indicate Near Term Weakness