BIGC - BigCommerce: Attractive Price But Caution Should Be Exercised

2023-05-12 12:42:12 ET

Summary

- BigCommerce's focus on enterprise has dampened its growth outlook as the economic downturn slows down the larger deal cycle.

- E-commerce market growth should continue to benefit the stock. The stock is down +50% YoY and +12% YTD, providing a buying opportunity.

- BigCommerce's seemingly lack of long-term vision presents a potential risk. Investors should exercise caution.

BigCommerce ( BIGC ), a company providing an e-commerce platform for retailers, has experienced significant growth in recent years, capitalizing on the expansive opportunities presented by the booming e-commerce industry. The widespread adoption of online shopping, fueled by changing consumer behavior and the convenience of digital transactions, has provided a favorable environment for the company to thrive.

Since its IPO in 2020, BigCommerce has shifted its focus to expand and concentrate more on serving enterprise clients. The move has resulted in a dampened growth outlook today, where the larger deal cycle has been slowing down due to the ongoing economic downturn. It is expected that BigCommerce will continue to see a challenging business environment at least until the end of FY 2023.

Currently trading at +$7 per share after having down +50% YoY and +12% YTD, I must admit that there is an attractive buying opportunity. However, I would view it with a grain of salt and assess the opportunity from both a quantitative and qualitative lens.

In general, I believe that the business should continue to benefit from the e-commerce industry growth and potentially reaccelerate as the economic downturn subsides probably in FY 2024. The initiative to improve profitability and achieve adjusted EBITDA breakeven in the midst of a slowdown is also commendable.

Yet, I view the lack of substantial and visionary moves may hinder the company to achieve more significant scalable growth to balance out the rather expensive enterprise-focused go-to-market activities.

I seek to monitor BigCommerce's progress on those fronts going forward and maintain a neutral rating for the stock at the moment.

Q1 2023 and Financial Highlights

The recap of the recent Q1 results is as follows:

-

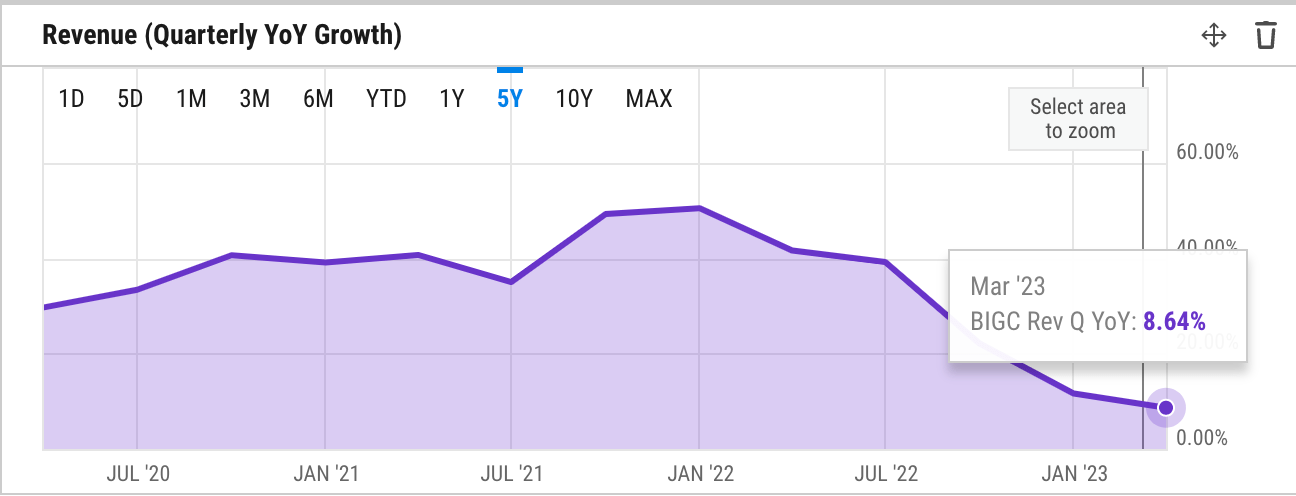

Q1 revenue of $71.76 million beat estimate by $0.29 million, showing a YoY growth of 8.6%.

-

As of March 31, 2023, the total annual revenue run-rate reached $316.7 million, marking a 13% increase compared to March 31, 2022.

-

Subscription revenue for Q1 was $53.8 million, demonstrating a YoY growth of 12%.

-

Accounts with at least one enterprise plan contributed to an Annual Recurring Revenue ((ARR)) of $228.8 million as of March 31, 2023, reflecting a YoY growth of 21%.

-

Enterprise Accounts represented 72% of the total ARR as of March 31, 2023, up from 67% as of March 31, 2022.

-

The GAAP gross margin for Q1 was 76%, compared to 74% in the same period of 2022. The non-GAAP gross margin was 77%, a slight improvement from 75% in Q1 2022.

-

Q2 Revenue is projected to range between $72.1 million and $74.1 million, a YoY growth rate of 6% to 9%.

-

The expected non-GAAP Q2 operating loss is estimated to be between $5.5 million and $9.5 million.

-

FY 2023 revenue to range between $303.0 million and $311.0 million, representing a YoY growth rate of 9% to 11%.

-

FY 2023 non-GAAP operating loss for 2023 is anticipated to fall between $14 million and $20 million.

As a result of the lengthening deal cycle at the enterprise and mid-market segment, BigCommerce will experience a weak growth outlook for the full year. Enterprise clients today make up over 70% of the business , up significantly from 54% a few years ago post-IPO. Given the relatively significant enterprise/mid-market share of the revenue mix, the impact of the economic downturn has been very pronounced in BigCommerce.

YCharts - Quarterly Revenue BIGC

{kind=link}

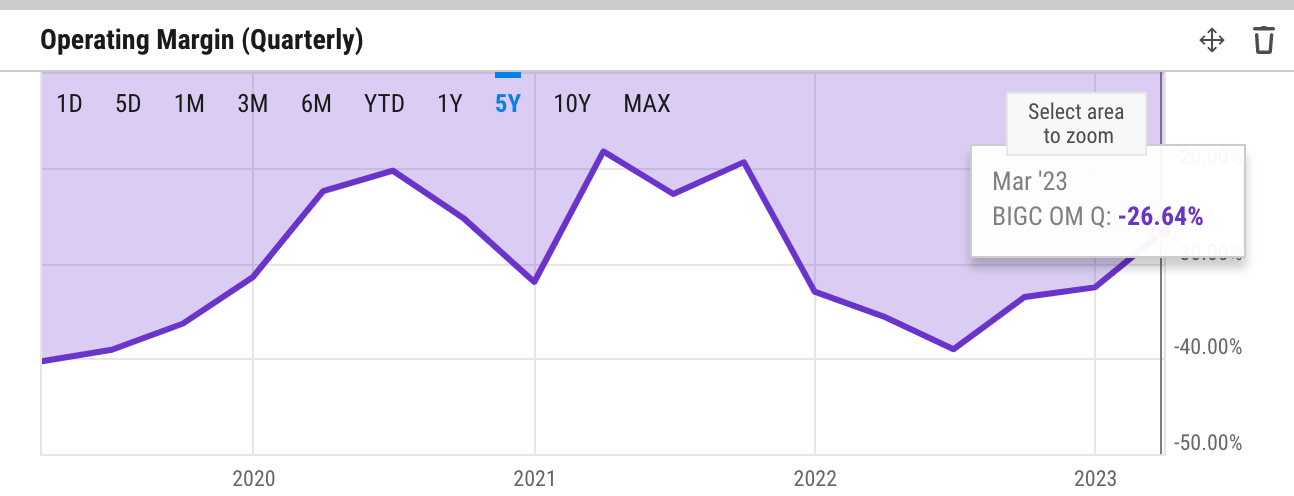

The slowing revenue growth has been apparent since Q2 last year. In previous years, revenue growth was solid and even accelerated from 36% to 44% between 2020 and 2021. There was a slight improvement in profitability outlook, especially with Q1 gross margin improving to 77% from Q4 last year, most likely due to the declining growth in the lower-margin segment, Partners and Services - that segment saw a 1% decline YoY.

YCharts - Operating Margin BIGC

{kind=link}

Despite the management's suggestion that adjusted EBITDA will be at break-even point at the end of the year, as we zoom out, there seems to be a lot of work to do in terms of bringing the business to breakeven, at least the operating level. The operating loss margin has been between 20% to 40% since 2020, though narrowing to ~26% as of Q1. Nonetheless, it appears that enterprise growth remains expensive for BigCommerce as it continues to spend ~45% of its revenue towards S&M/sales and marketing. Without any non-GAAP adjustment, it is still far away from profitability. Meanwhile, operating cash flow/OCF and FCF have also been consistently negative, though looking at the pattern and magnitude, BigCommerce still has them under control.

Risk

A key risk consideration for BigCommerce is the need to diversify its business model to better absorb the potential economic shock and capture a larger share of the overall Gross Merchandise Value/GMV transactions of its clients. While the e-commerce sector offers a massive TAM and significant growth potential, BigCommerce is currently not equipped with the best business model to capture the most value from that tailwind.

It is true that the enterprise shift provides opportunities to land higher deal sizes, but as it stands, regardless of the potential reacceleration of the segment post-FY 2023 and its risk, the overall long-term vision and roadmap at BigCommerce has been at best moderate.

The best way to really put things in perspective is to highlight the fact that BigCommerce is a 14-year-old e-commerce company generating $279 million of annual revenue last year, while its competitor Shopify ( SHOP ) was raking in ~$5.6 billion.

Overall, BigCommerce's current reliance on subscription fees and recurring partner services as part of its core business model limits its ability to participate in the full revenue generated by its clients. For instance, BigCommerce today recognizes the share of payment fees received by its payment gateway partner, but this form of partnership produces too little take rate that does not seem enough to move the needle. That is not the case with Shopify.

A notable example is Shopify's launch of its payment system in 2013, which allowed the company to earn a percentage of GMV as revenue. Today, this revenue stream constitutes approximately 70% of Shopify's business, surpassing the earnings from platform subscription fees alone.

Catalyst

On the flip side, the enterprise will still remain a key growth driver that can move the growth needle for BigCommerce. The go-to-market here has been largely effective, with the company continuing to land enterprise deals and expanding internationally carefully even during the downturn.

In the Q1 earnings call, we learned just one of the key benefits of serving the enterprise clients aside from the larger deal size and purchasing power - many of them have international operations, which enable BigCommerce to strategically leverage that relationship and experience to identify and design the best international strategy before making expansions. In Q1, we saw how BigCommerce continued to land some of these potentially strategic deals:

Tottenham Hotspur, one of the world's top football clubs, is leveraging BigCommerce's platform to further enhance its popular online store's capabilities and fan experience not only at home in the UK, but also in APAC and North America where the club has a significant and growing fanbase. ASSA ABLOY, a global leader in door-opening solutions used in many of the world's locks and security installations, is revolutionizing its customers' experience by integrating its broad product catalog and using our B2B Edition solution to customize the shopping experience.

On the other hand, the strategic partnership with large marketplace players, such as Amazon ( AMZN ), or with any large B2B (business to business) companies with access to enterprise businesses with retail digital and e-commerce transformation demand, may just provide the right opportunities for BigCommerce to efficiently land key accounts.

Overall, I feel that the right execution of these strategies post FY 2023 can alleviate pressure on S&M spending and drive enterprise ARR growth at better unit economics. Combining that improving outlook and BigCommerce's market cap of just ~$540 million today, I would also consider revisiting the idea of BigCommerce being acquired by one of its larger strategic partners. Before its IPO in 2020, there was a rumor that Intuit ( INTU ) expressed an interest in acquiring BigCommerce for $1.5 billion - considering the financial and strategic values that can be realized through the combination, this would not be an unattractive proposition today.

Valuation/Pricing

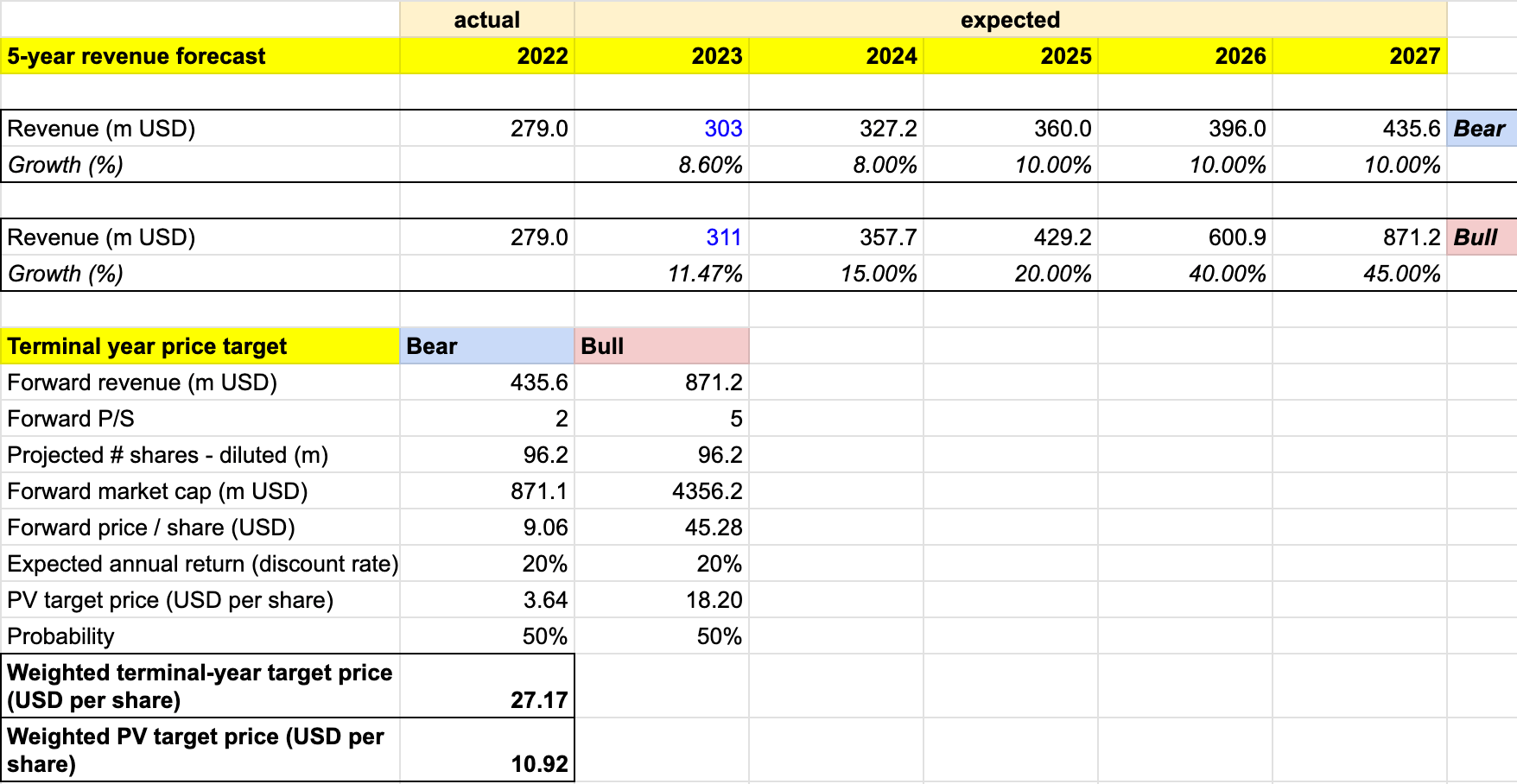

My target price for BigCommerce is driven by the following bull vs bear scenarios of the 5-year revenue forecast:

- Bull scenario (50% probability) - economic downturn to subside towards the end of FY 2023, and the revenue to see 15% and then 20% revenue growth in the next two FYs, driven by the enterprise segment reacceleration. BigCommerce would then enter a new business where it starts generating take rate revenues off e-commerce GMVs from its clients (e.g. payment, managed e-commerce services). I expect the new business to start driving revenue growth to 40% and 45% in FY 2026 and FY 2027, with the company closing in on adjusted EBITDA break-even, but still unprofitable due to the investment into the new business. I also expect a 30% share dilution in FY 2027, the same thing in the bear scenario.

- Bear scenario (50% probability) - economic downturn to prolong into FY 2024. BigCommerce to see merely 8% - 10% revenue growth into FY 2027, driven by the emphasis on optimizing the bottom line and stagnant international growth, especially in APAC, as seen in Q1. This leads to BigCommerce exiting some of those geographic markets. The profitability outlook improves to generate a single-digit positive operating margin, though at a significant expense of growth.

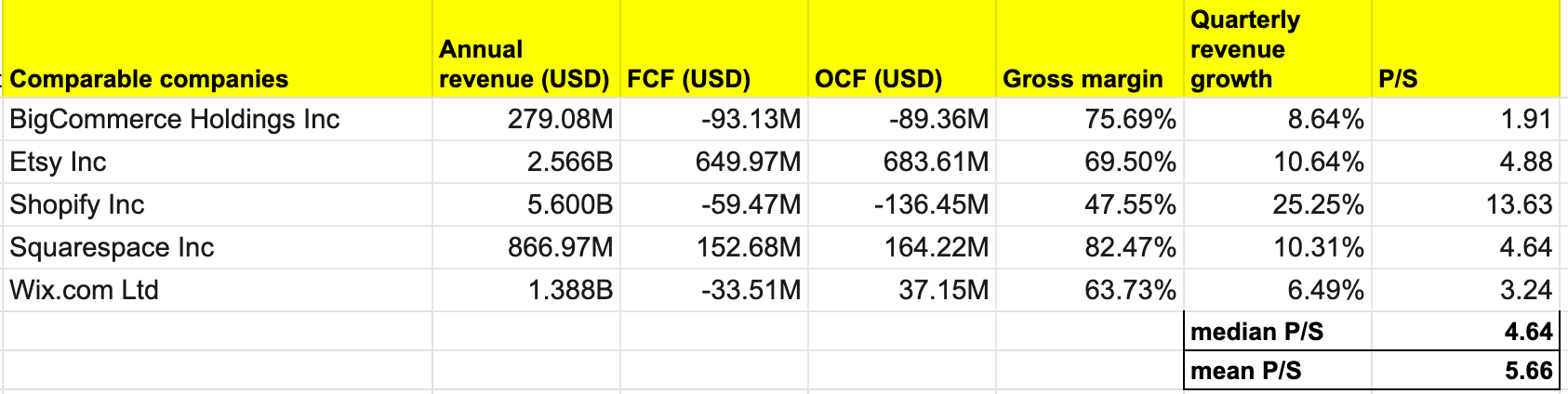

Author's Own Analysis - BIGC Comparable

{kind=link}

In estimating the FY 2027 P/S for each scenario, I consult the overall P/S performance of comparable e-commerce companies. With a revenue of just $279 million, BigCommerce is by far the smallest company in this universe. Yet, it also has the lowest P/S multiple. One possible explanation would be that there is indeed a lower growth expectation for BigCommerce due to its focus on enterprise clients, which require a more complex go-to-market process despite the higher potential deal size. That, in itself, would also be an acceptable way to capture values from the global e-commerce market. However, BigCommerce's relatively weak profitability outlook may also undermine its market valuation.

Aside from BigCommerce, companies in the comparable universe provide an e-commerce solution across all segments, with an emphasis on SMBs. The median P/S of this group is ~6x, while the lowest P/S of 1.9x belongs to BigCommerce. With that in mind, I decide to assign a P/S of 5x for the bull scenario - slightly lower than the group's median - and a P/S of 2x for the bear scenario.

Author's Own Analysis - BIGC Target Model

{kind=link}

Consolidating all the information above into my model, I arrived at an FY 2027 weighted target price of $27 per share in FY 2027. Discounting that target price with a 20% discount rate, I reached a Present Value/PV weighted target price of +$11 per share. The 20% discount rate represents the expected annual return for holding BigCommerce.

In summary, $11 per share is the highest price point at which investors can purchase the stock to realize a projected 20% annual return should my FY 2027 target price of $27 be achieved. At ~$7.4 per share today, BigCommerce trades at a +30% discount to my target price - suggesting that the stock is undervalued.

Conclusion

BigCommerce's focus on serving enterprise clients post-IPO has resulted in a dampened growth outlook as the higher deal cycle slows down due to the economic downturn. The business is expected to face a challenging business environment, at least until the end of FY 2023. While the current stock price presents a buying opportunity today, I would advise investors to exercise caution and view the opportunity from all sides.

The potential for growth exists as the e-commerce industry continues to expand and the economic conditions improve, likely in FY 2024. The company's efforts to improve profitability and achieve adjusted EBITDA breakeven are also commendable. However, the lack of substantial and visionary moves may hinder significant scalable growth potential from capturing higher values from the e-commerce industry growth. Monitoring BigCommerce's progress in these areas is advisable, and adding the stock to a watchlist is a prudent course of action.

For further details see:

BigCommerce: Attractive Price, But Caution Should Be Exercised