BIGC - BigCommerce: Don't Trust The E-Commerce Platform That's Not Growing (Rating Downgrade)

2023-07-16 10:42:03 ET

Summary

- Despite a promising start, e-commerce company BigCommerce has seen a significant downturn, with slowing revenue growth and increasing debt.

- The company is struggling to compete with larger rival Shopify, which is growing at a faster rate, leading to concerns about BigCommerce's future relevance.

- In spite of a 20% increase in stock value this year, BigCommerce's growth trajectory is dire.

- Its only appeal is a cheap ~3x forward revenue valuation, but due to limited prospects the company is a value trap in my opinion.

Amid a skyrocketing stock market and surging optimism for a lower interest rate environment, it's difficult to remember that many companies are still battling a fundamental recession. Consumer spending and confidence is down, hurting e-commerce companies.

In this backdrop, BigCommerce (BIGC) has seen a massive reversion in its luck. A big hyper-growth story during the pandemic, BigCommerce has suffered from the underlying slowdown from its retailer clients. Year to date, the stock has jumped ~20%, roughly matching the performance of the S&P 500, but the company's financials have turned south.

Previously bullish, then neutral on BigCommerce, I am now bearish on BigCommerce's prospects through the remainder of the year. Though the stock may appear cheap, I consider BigCommerce to be quite a sour value trap.

Here, in my view, are the key risks that BigCommerce faces:

- Despite a large TAM, BigCommerce is unable to show substantial growth. The company cites a large $28 billion TAM, but despite being less than 1% penetrated into this overall market, the company's revenue growth has slowed down to the single digits - indicating a lackluster brand and weak execution.

- Outclassed by its much larger competitor, Shopify. Being smaller in any given industry often indicates a company that has more room to grow and take market share. But Shopify, which is approximately 20x BigCommerce's scale, is also growing faster than BigCommerce - worrying many investors that BigCommerce will eventually become irrelevant.

- Steep cash burn. BigCommerce's free cash flow profile is at a -30% margin. This is normal for an early-stage business, but with BigCommerce's growth having slowed to the single digits, it's unlikely that the company can achieve the scale necessary to grow toward profitability.

- Net debt position. And unlike many other small-cap tech companies, BigCommerce is in a net debt position, which further complicates its sharp cash flow losses.

From a valuation perspective: at current share prices near $10, BigCommerce trades at a market cap of just $772.3 million. After we net off the $282.4 million of cash and $338.0 million of debt on the company's most recent balance sheet, BigCommerce's resulting enterprise value is $827.9 million.

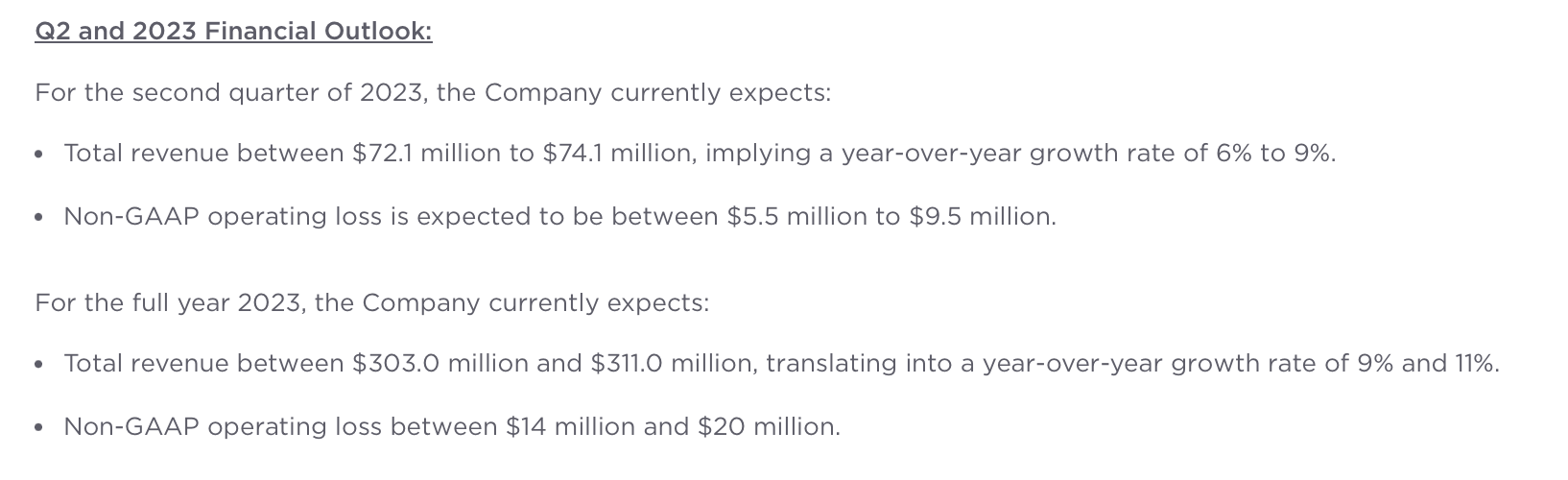

For the current fiscal year, meanwhile, BigCommerce is guiding to $303-$311 million in revenue, representing just 9-11% y/y growth (considering Q1 revenue growth clocked in at just 8.6% y/y, this is arguably already an aggressive forecast):

{kind=link}

This puts BigCommerce's revenue multiple at 2.7x EV/FY24 revenue - which may appear cheap at face value, but in my view appropriately values a company with minimal growth catalysts to scale at a healthy pace.

The bottom line here: especially with the stock's >20% appreciation year to date despite souring fundamentals, it's a great time to lock in gains on BigCommerce and invest elsewhere.

Q1 download

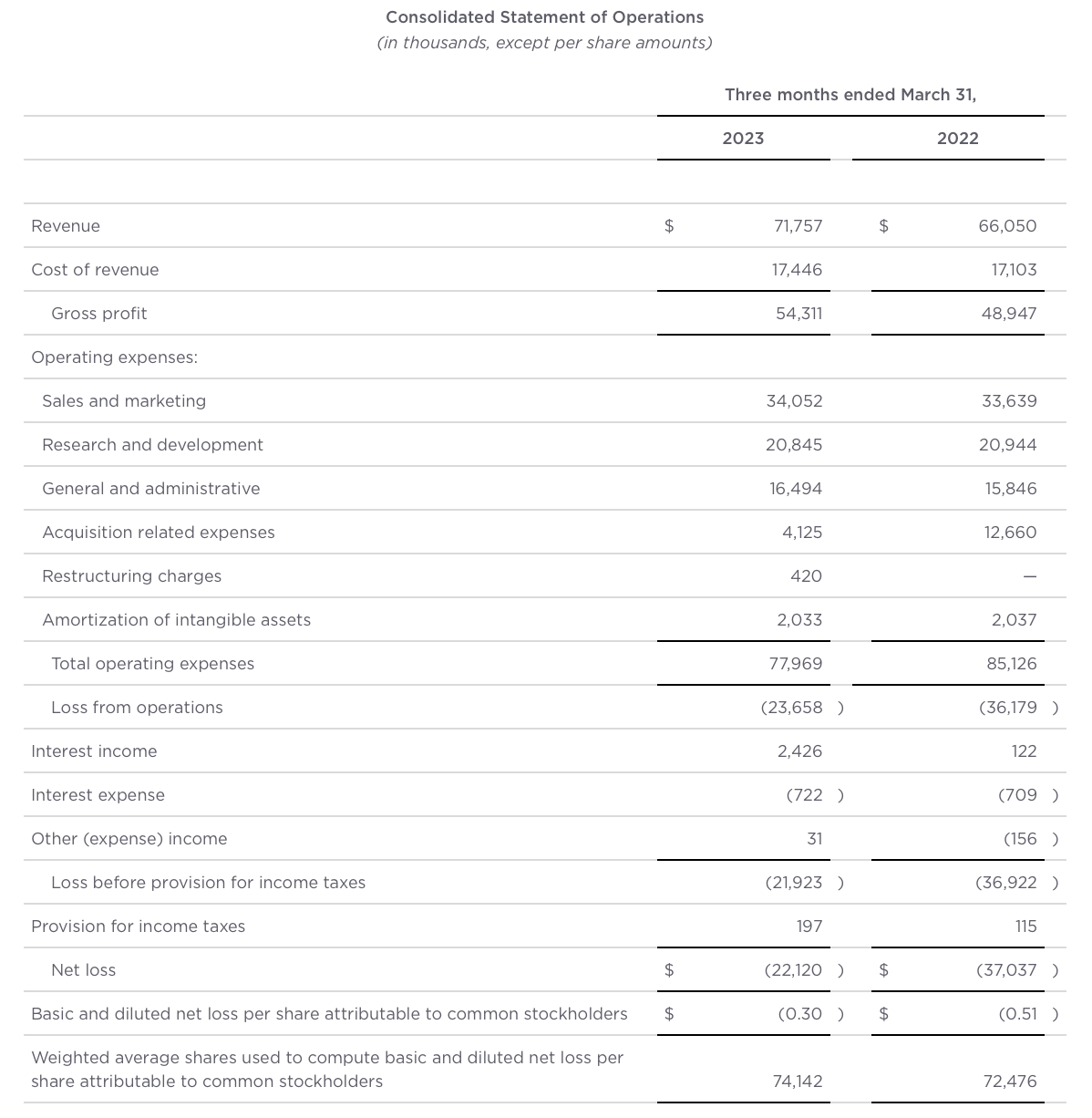

Let's now go through BigCommerce's latest quarterly results in greater detail. The Q1 earnings results are shown below:

{kind=link}

Revenue grew just 9% y/y to $71.8 million, essentially in-line with Wall Street's expectations of $71.5 million (+9% y/y). Growth decelerated sharply, however, relative to 12% y/y growth in Q4.

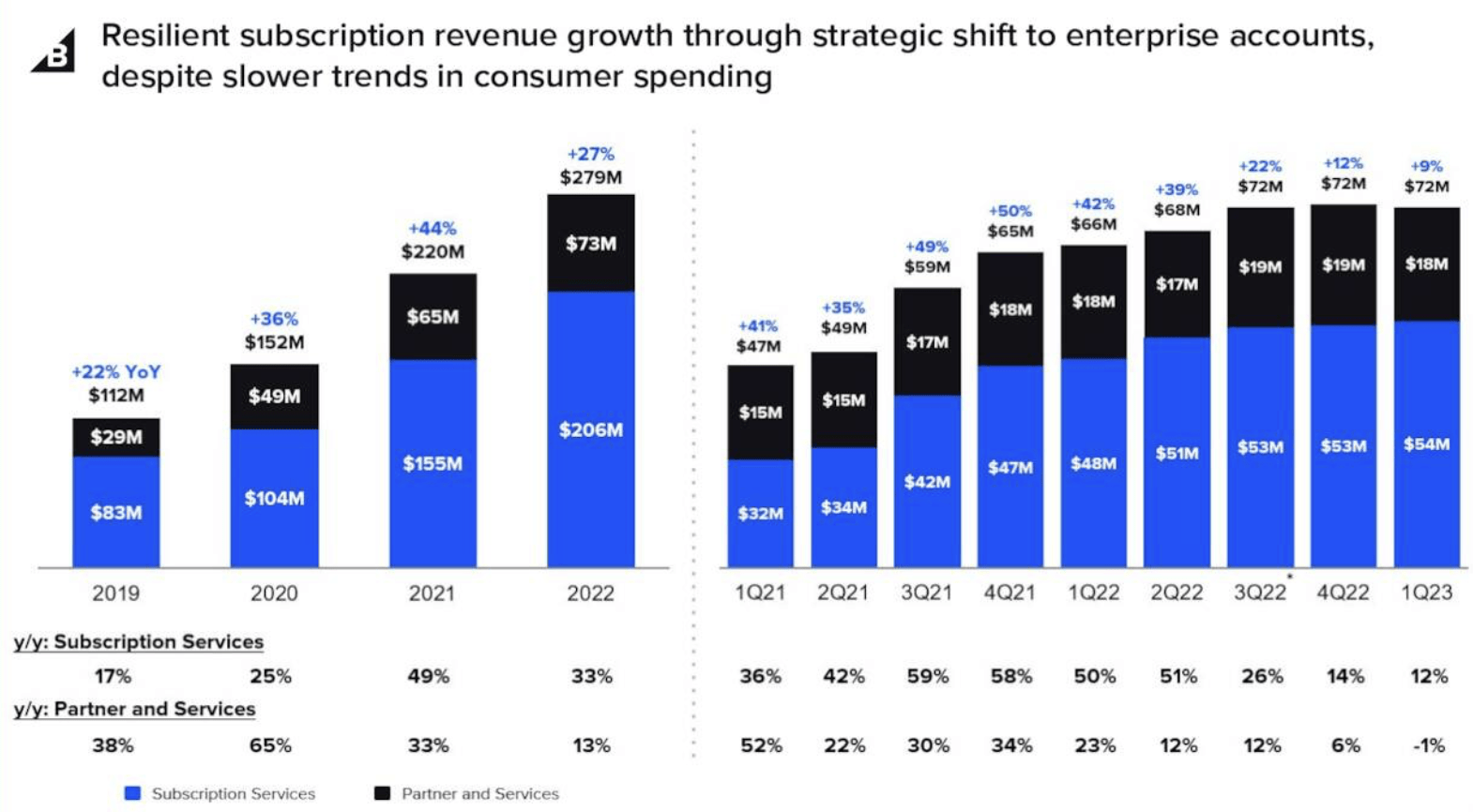

The chart below showcases the steep change in fortunes for BigCommerce since the pandemic. At its height in 2021, BigCommerce was growing at a ~50% y/y pace, falling steadily throughout last year to finally land at a single-digit growth rate this quarter. Deceleration was equally noticeable in both subscription revenue as well as add-on services, which declined -1% y/y in the current quarter.

{kind=link}

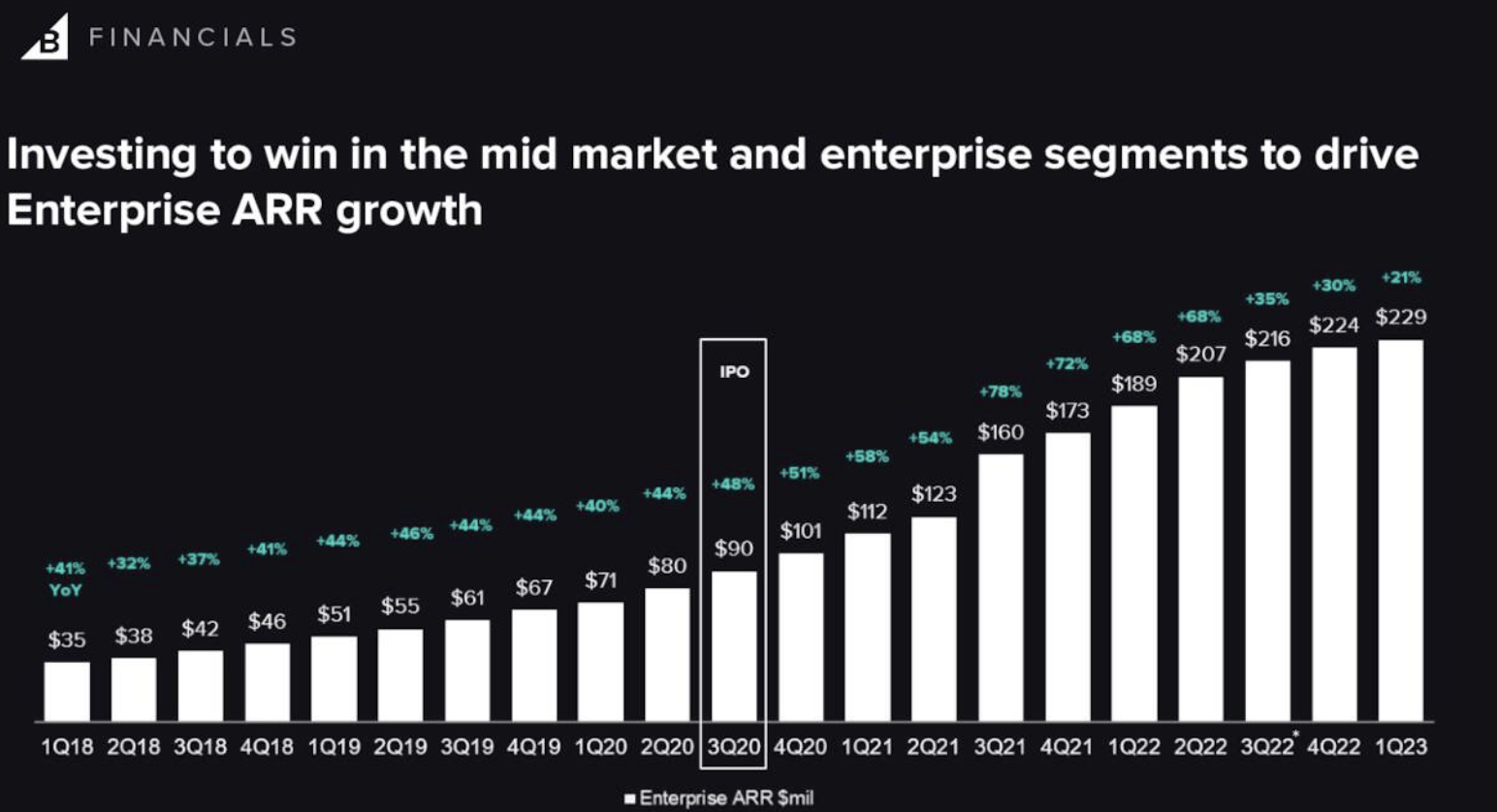

It's also worth noting the fact that BigCommerce's enterprise ARR has all but flatlined. The company had a strategy of chasing larger enterprise clients to stabilize its revenue base, but over the past few quarters as shown in the chart below, enterprise ARR has flatlined at ~$220 million, barely adding ~$5 million in net-new ARR per quarter (versus quarterly adds of $20 million or more over the past several years).

{kind=link}

The company notes, similar to other software companies, that sales cycles have elongated since the recession began - in BigCommerce's case, 50 days longer. Per CEO Brent Bellm's remarks on the Q1 earnings call :

Our shift of go-to-market focus from small business to the enterprise segment is showing positive results. Sales pipeline as of the start of Q2 for this segment is approximately 20% higher than where we were at this time last year. Win rates remain strong. Sales cycle times in the lower end of this segment are largely unchanged, while larger enterprise opportunities have seen an increase of approximately 50 days between first engagement with the merchant and close compared to this time last year [...]

We are responding to the sales cycle time dynamics I mentioned previously by further prioritizing channels and products that deliver strong ROI with faster time to close. We are increasing our investment in lead generation with our agency partners and in the mid-market segment, as these opportunities tend to have shorter sales cycle times and a strong LTV to CAC."

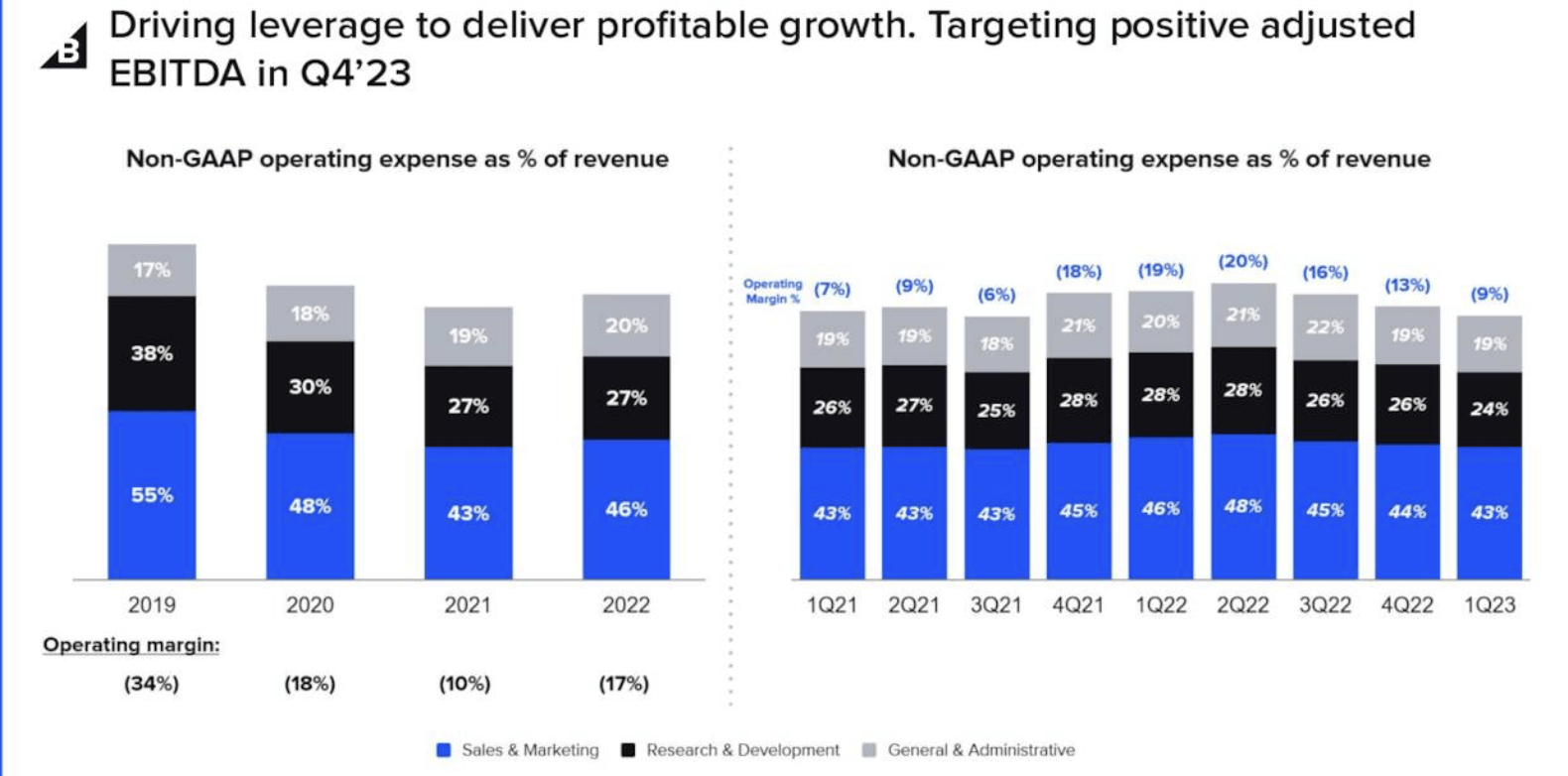

The one piece of good news is on profitability, as BigCommerce has focused on cost reductions. Pro forma operating margins in the first quarter were -9%, ten points better than the year-ago quarter, and it's expecting to cross the breakeven mark by the fourth quarter this year.

{kind=link}

This being said, however, BigCommerce's ability to generate meaningful profits will ultimately be capped by its sluggish sales growth. In my view, Shopify's superior >20% y/y revenue growth despite its much larger scale is a telling signal of BigCommerce's eventual trajectory.

Key takeaways

With sluggish growth, a tough macro environment for e-commerce companies, consistent outpacing from its largest rival Shopify, and sharp cash burn amid a concerning net debt position, there's not much incentive to stay invested in BigCommerce. Steer clear here and invest elsewhere.

For further details see:

BigCommerce: Don't Trust The E-Commerce Platform That's Not Growing (Rating Downgrade)