BIGC - BigCommerce: Nearing An Inflection Point

2023-11-11 05:18:29 ET

Summary

- BigCommerce's shares fell after presenting Q3 results, despite making progress in terms of cutting costs.

- The company is focused on the enterprise market segment, with strong growth in annual recurring revenues.

- BigCommerce is nearing profitability, with declining expenses and a positive operating income margin possible for FY 2024.

- Shares are a bargain relative to Shopify. BigCommerce may even become an attractive acquisition target for Shopify given the strength in enterprise.

BigCommerce Holdings ( BIGC )’s shares slumped 11% directly after the e-Commerce company presented results for its third fiscal quarter. Although the firm managed to deliver earnings and revenues that broadly matched the consensus estimates, the e-Commerce firm still has not been profitable in Q3'23 and revenue growth overall slowed. However, BigCommerce is making progress in building out its enterprise market positioning and the company is seeing strong momentum in this regard. I believe BigCommerce could see positive operating income next year. Shares remain widely undervalued relative to Shopify and I continue to see favorable e-Commerce tailwinds for BigCommerce!

Previous rating

I rated BigCommerce a strong buy after the presentation of Q2’23 results in August -- Strong Buy After Impressive Q2 Results -- due to top line momentum and narrowing losses. I believe BigCommerce could soon reach an inflection point and report positive operating income.

Strong positioning in the enterprise market

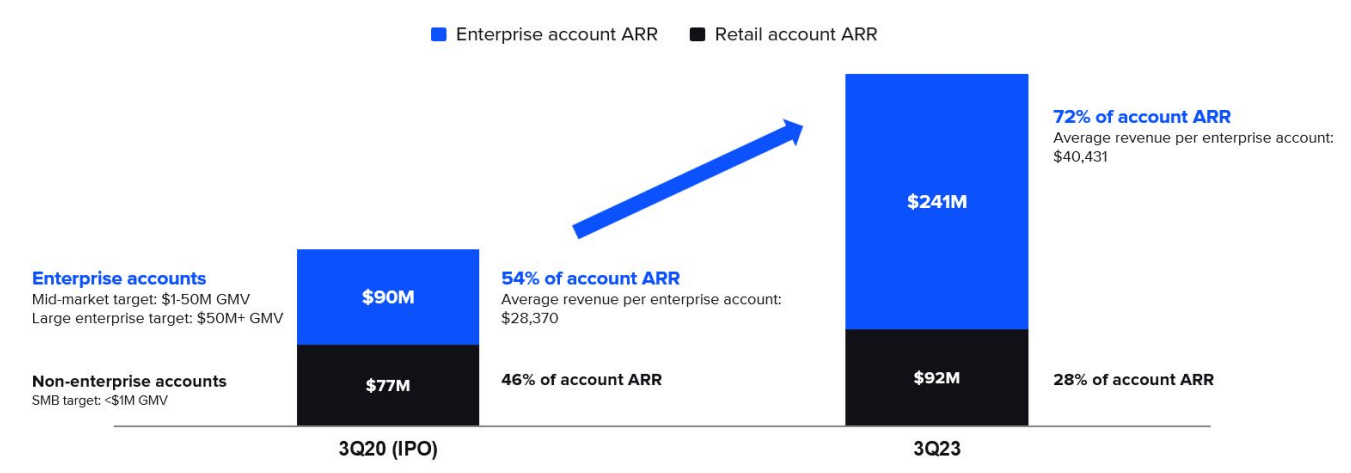

Whereas Shopify ( SHOP ) focuses chiefly on retail merchants that sign up for the e-Commerce company’s online store plans, BigCommerce is more focused on the enterprise segment of the merchant market and this segment continued to produce results for the firm: BigCommerce generated $241M (72%) of its annual recurring revenues/ARR from the enterprise segment in Q3'23 which include mid-market customers that achieve $1M-50M per year in gross merchandise value/GMV.

Gross merchandise value is an important metric for e-Commerce companies because it shows the total dollar amount that flows through an e-Commerce platform on an annual basis. Growth in GMV translates to growth in annual recurring revenues for BigCommerce's revenues.

About $92M, or 28% of total annual recurring revenues, were achieved in the non-enterprise market segment… which includes those accounts that achieve less than $1M annual in gross merchandise value.

{kind=link}

Source: BigCommerce

Almost all of BigCommerce’s growth since its IPO in 2020 has happened in the enterprise market segment.

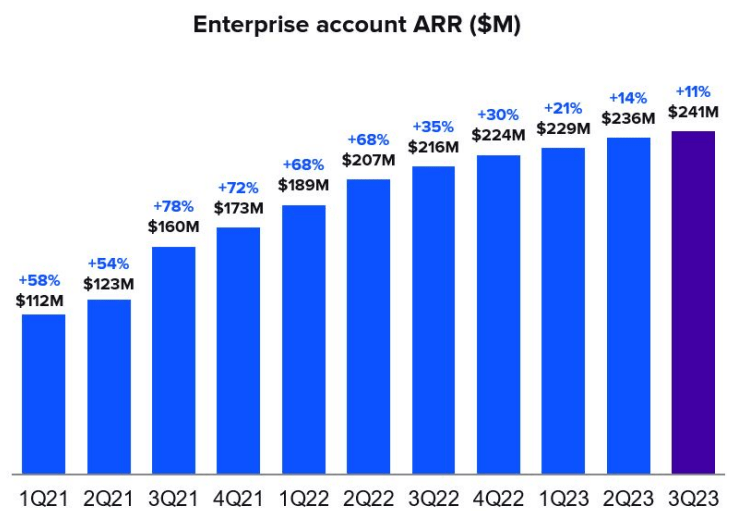

BigCommerce’s business strength can be seen in the revenue ramp chart in the enterprise segment below. Although top line growth has consistently moderated since Q3’21, the e-Commerce company has been able to grow its annual recurring revenues in the enterprise market steadily. In the third-quarter, enterprise ARR grew 11% year over year to a record $241M. Total ARR, which includes revenues from smaller merchant accounts, totaled $332M, showing 9% year over year growth.

{kind=link}

Source: BigCommerce

Customer retention translates to organic revenue growth

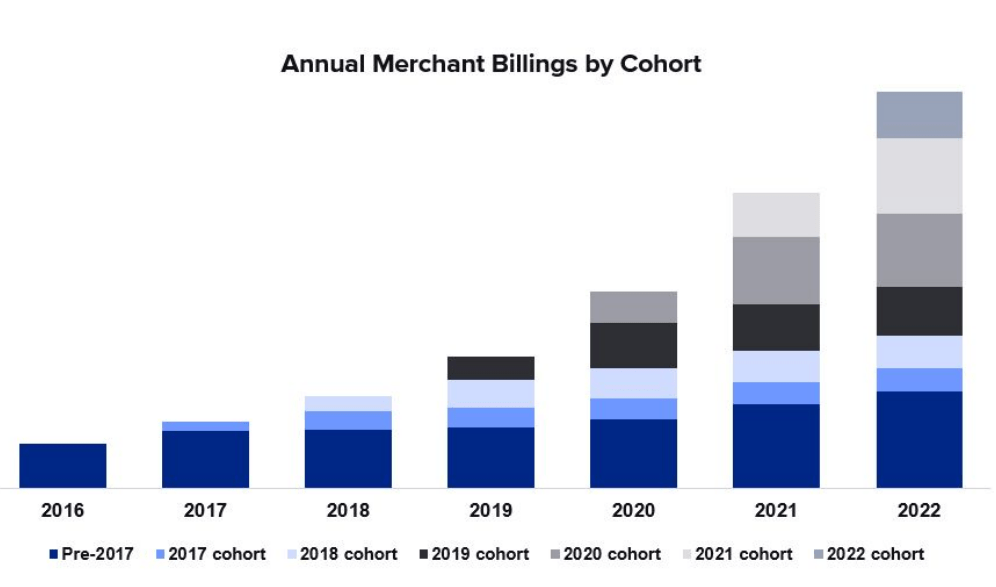

Merchants that use BigCommerce’s online store tools are growing their product spend over time, as the following chart shows. A breakdown by customer cohort (by year) shows that merchants are increasing their product-spend considerably with time which also means that older merchant cohort have stronger product-spend than newer cohorts. For BigCommerce, growth in merchant accounts is therefore not the only source of revenue growth.

{kind=link}

Source: BigCommerce

Nearing an inflection point

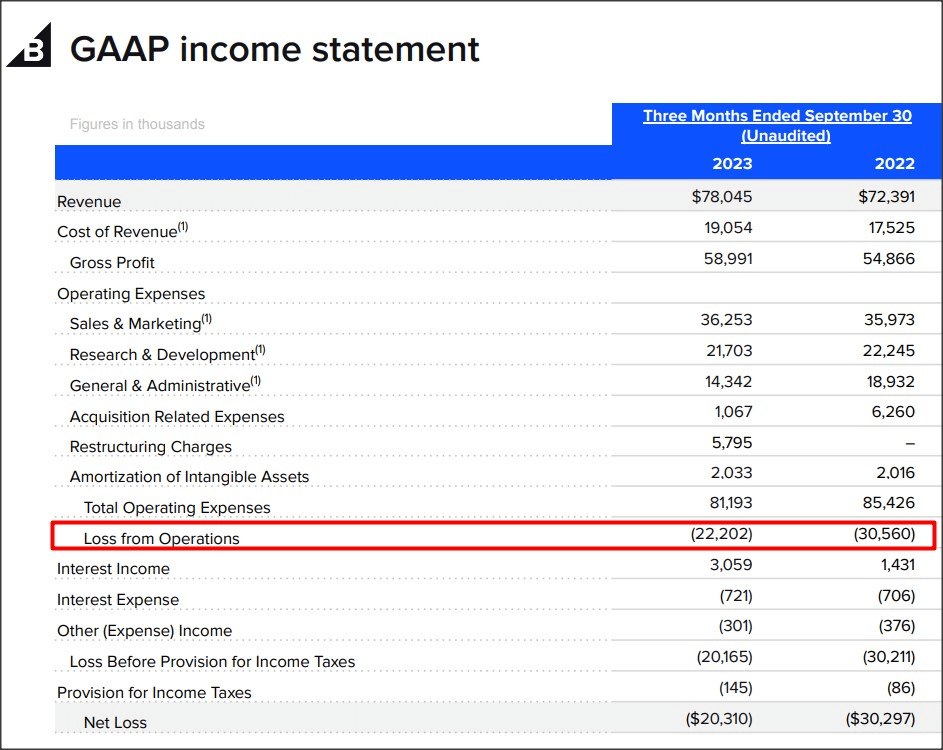

BigCommerce is still not profitable and it is this factor that I believe has weighed on the company’s valuation more than anything since the company's IPO in 2020. But losses are narrowing, indicating that the e-Commerce firm is on a stable trajectory and could soon report operating income profitability: BigCommerce generated an operating loss of $22.2M compared to $30.6M in the year-earlier period, showing a decline of 27%.

{kind=link}

Source: BigCommerce

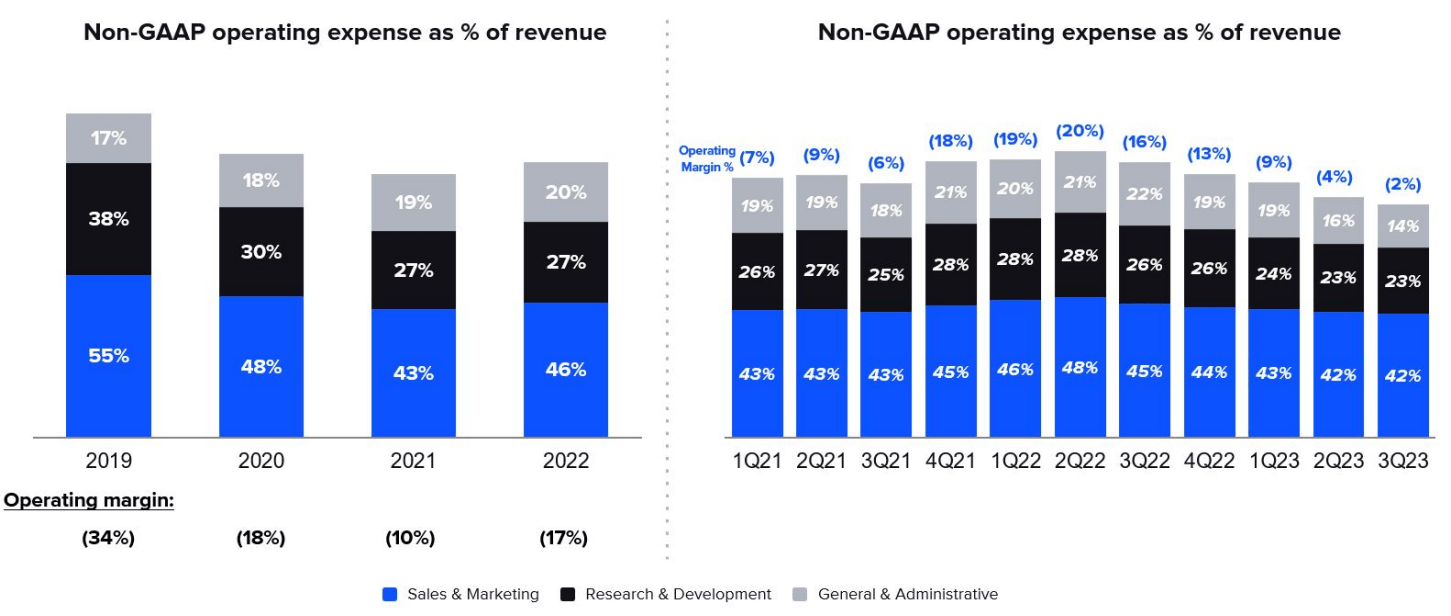

The trend is definitely going in the right direction and this is because management has brought a stricter cost focus to its e-Commerce operations.

Non-GAAP operating expenses declined rapidly: BigCommerce’s non-GAAP operating expenses declined for five straight quarters in Q3’23 and resulted in a 2% negative operating income margin. BigCommerce has guided for a non-GAAP operating loss of $6.9M to $9.9M for FY 2023, but expects to see $1.1M to $4.1M in operating income in the fourth-quarter, meaning the e-Commerce firm is just about to turn profitable.

{kind=link}

Source: BigCommerce

BigCommerce’s valuation

Shopify is a market leader and a proven innovator in the space for e-Commerce online store solutions and the company is significantly higher valued than BigCommerce. Shopify achieves 25X higher revenues than BigCommerce and has a market cap 121X higher than its smaller e-Commerce rival. Given the much larger size and valuation of Shopify, I actually see BigCommerce as a potential takeover target.

BigCommerce is expected to generate $337.6M in revenues next year which compares against a revenue volume of $8.3B for Shopify and the latter is expected to grow its top line about twice as fast as BigCommerce. With regards to valuation, Shopify is trading at a P/S ratio of 9.4X which is ~5x larger than BigCommerce’s valuation ratio of 1.9X. I down-graded Shopify after Q3'23 results due to the firm's stretched valuation: Strong Growth, But No Bargain .

Big Commerce has traded at a P/S ratio of ~2.8X in the past which I believe is a reasonable multiplier under the assumption that BigCommerce achieves operating income profitability. The implied fair value, assuming a 2.8X revenue multiplier factor, would be ~$13.

Risks with BigCommerce

BigCommerce is growing rapidly, but the company is still not profitable and investors are increasingly less willing to invest in start-ups with mounting losses. BigCommerce needs to show that it can run its e-Commerce platform at scale and profitability. Slowing top line growth and a potential delay in the profitability timeline due to e-Commerce (consumer spending) headwinds in the industry would likely negatively impact BigCommerce’s valuation factor. A delay in operating income profitability would also likely be a negative stock catalyst.

Final thoughts

I believe the market’s reaction to BigCommerce’s third-quarter earnings card is exaggerated since the e-Commerce company continued to make a lot of progress. BigCommerce is steadily moving towards operating income profitability and the company's top line in the enterprise market keeps growing at double digits. Given the success the company has had in lowering its non-GAAP operating expenses, I believe BigCommerce could achieve operating income profitability in FY 2024. The valuation, at least in comparison to Shopify, is very attractive and BigCommerce, in my opinion, could actually be interesting to Shopify as an acquisition target given the similarity in its business model and BigCommerce's strength in the enterprise segment!

For further details see:

BigCommerce: Nearing An Inflection Point