BIGC - BigCommerce: New Product And Pricing Strategy Should Help Improve Business Fundamentals

2023-06-15 01:38:29 ET

Summary

- I believe BIGC is well-positioned to capture market share in the growing e-commerce market, particularly in the Enterprise sector.

- The company's focus on improving its Enterprise solution and competing for larger opportunities demonstrates the effectiveness of its product strategies.

- The recent price increase and positive response from retail customers are expected to boost cash flow and profitability, with management projecting positive EBITDA by 4Q23.

Description

I still recommend buying BigCommerce ( BIGC ). The overarching bull thesis is that ecommerce still has a long runway to grow, and within in, BIGC still has plenty of opportunities to capture market share, especially in the Enterprise market. A more robust financial model, thanks to better unit economics and higher retention rates, should result from BIGC's increasing presence in the Enterprise market. Nonetheless, I would still highlight the biggest headwind for BIGC, which is that it continues to operate in a challenging environment while refocusing its sales efforts on the large enterprise sector. The improved pipeline quality, however, makes this a worthwhile sacrifice. This growth plan is made possible by BIGC's investment in and strong position within the mid-market, where management anticipates realizing unit economics competitive with those of the enterprise and benefiting from shorter sales cycles. Encouragingly, BIGC's management has reiterated its previous projection of positive EBITDA by 4Q23 and increased its EBIT guidance for 2023.

Macro continue to weigh on Enterprise-target strategy

Multiple metrics show slowing growth, including ARR growth of 12.9% versus 16% in the previous quarter and enterprise ARR growth of 21.1% versus 29.6% in the previous quarter. The same challenge I warned about before still exists in the form of the longer sales cycles maintained by larger Enterprise customers. However, despite the deteriorating macro and focus shift, it is encouraging to see that retail ARR increased from $87.7 million to $87.9 million on a net dollar basis. Seeing this gives me confidence that BIGC will be able to "farm" the mid-market for cashflow and invest in product iterations even as sales cycles level off. Considering the high resource requirements of the Enterprise market, the decision by management to make their GTM strategy for small businesses more self-serve in order to increase LTV to CAC makes a lot of sense. Since Enterprise deals tend to have a longer sales cycle, I expect this trend to put pressure on sales in the near future. When things get back to normal, however, the larger sales ticket and higher profits from Enterprise customers will greatly benefit BIGC's unit economics.

Product strategies

Given the company's management's unwavering commitment to bettering its Enterprise solution, I have high hopes for BIGC's future in the Enterprise market. New enterprise functionality continues to positively affect win rates, as reported at the TMC conference in May . Customers' satisfaction with the most up-to-date enterprise features, such as multi-store and multi-inventory support, remains high. Biggest evidence that BIGC's strategy is paying off: the company is now able to compete for RFPs for larger opportunities thanks to the half of their leads that come from their partner network (enterprise functionality). I believe bigger companies are showing interest in and enthusiasm for the platform, which should serve as a further tailwind as the presence of trustworthy, established businesses on BIGC raises the latter's profile and attracts even more companies to it.

Pricing

Recently, BIGC implemented a price increase, giving customers the option to save money on their service by signing up for a year's worth of service in advance and paying the full amount. Since the implementation of the new pricing structures, management has observed a healthy uptake on annual upfront prepay plans from retail customers, who are typically SMEs with less than $1M in GMV. On June 1st, the plan went live for the entire install base, which I expect to be a massive tailwind to cash flow in 2H23 and beyond (which can be used to reinvest into the Enterprise market immediately). I am more enthusiastic about this price hike because of the positive effect it will have on profits. Management now expects to achieve EBITDA breakeven by end of Q3, which literally means a positive adj. EBITDA in 4Q23. Considering management did not plan for any additional cost containment measures, they should have some wiggle room to improve margins even further, so there is a good chance they will reach this target.

Long-term trend

I still believe that BIGC will benefit from the secular trend over the long term. In my opinion, BIGC is at the forefront of the second wave of SaaS solutions entering the e-commerce market. The second wave is distinguished by improved malleability, customization, and compatibility. BIGC is at the forefront of this revolutionary change by providing a platform that gives retailers more freedom of action, more room for personalization, and more power in terms of integration.

Valuation

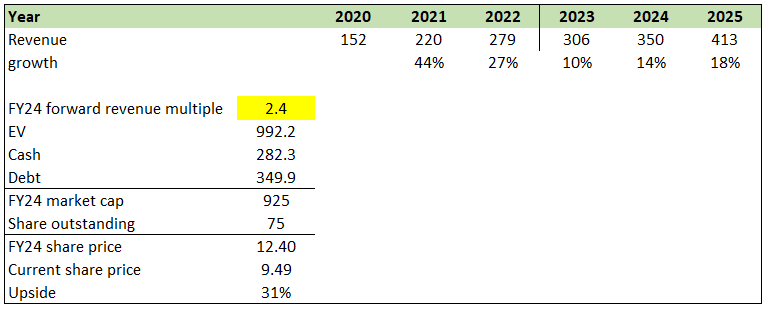

Based on model, I see a 30% upside to BIGC stock at 2.4x forward revenue multiple and consensus estimates. The variable factor here is the multiple that BIGC should trade at when growth starts to inflect back to 18% and more than 20% moving forward. I remind readers that BIGC used to trade in the ~10x forward revenue range before, so the possibility of reaching back to the mid-single digits level is not impossible. If we comp against similar peers like Squarespace, BIGC trades at roughly 50% discount despite growing at similar rates. Hence, while I expect 30% upside based on 2.4x, I think there is a bull case in which multiples inflect further.

{kind=link}

Risks

BIGC faces intense competition in an industry that is only expected to become more cutthroat in the years to come. BIGC's main rivals in the SMB market are Shopify ( SHOP ) and Block ( SQ ). The likes of Salesforce ( CRM ) and Adobe ( ADBE ) are among BIGC's mid-market rivals. BIGC also competes with market leaders like Oracle ( ORCL ) and SAP ( SAP ) in the enterprise sector. The common theme about these competitors is that they have a very strong balance sheet that allows them to continue investing aggressively, if need the ROI is attractive. Suppose BIGC were to figure out a new product/solution that works really well, these competitors may replicate it by dumping hundreds of millions into it.

Summary

I maintain my recommendation to buy BIGC stock based on its strong position within the growing ecommerce market and its potential to capture market share, particularly in the Enterprise sector. Despite operating in a challenging environment and facing longer sales cycles with larger Enterprise customers, BIGC's improved pipeline quality and focus on the mid-market are things to be positive about. The company's investment in enterprise functionality and its ability to compete for larger opportunities demonstrate the effectiveness of its product strategies. Moreover, the recent implementation of a price increase and the positive response from retail customers are expected to boost cash flow and profitability.

For further details see:

BigCommerce: New Product And Pricing Strategy Should Help Improve Business Fundamentals