BIGC - BigCommerce: Rating Downgrade As Growth Outlook Is Weak

2023-12-15 10:42:08 ET

Summary

- BigCommerce's growth is decelerating, particularly in the ARR metric, raising concerns about its future performance.

- The competition with Shopify is a concern.

- BigCommerce's management is focusing on driving profitability by adjusting its go-to-market strategy and downsizing the team, but the success of these efforts remains uncertain.

Investment action

I recommended a buy rating for BigCommerce (BIGC) when I wrote about it the last time (12 Sep 2023), as revenue growth remained robust and management continued to stay focused on driving profitability upward. Contrary to my expectations, growth did not remain robust, albeit profitability improved.

Based on my current outlook and analysis of BIGC, I recommend a hold rating. I am now concerned that BIGC’s growth will continue to decelerate in the coming quarters. Even though turning profitable is a focus, I am not willing to take the risk that BIGC permanently loses its share. Especially with the uncertainty of the change in go-to-market strategy, growth is even more uncertain in the near term.

Review

On November 8, 2023, BIGC reported its 3Q23 results. BIGC's 3Q23 total revenue came in at $78 million, representing a growth of 7.8%. The growth was driven by Subscription revenue growth of 10.3% to $58.7 million and Partner and Services revenue growth of 0.9% Y/Y to $19.3 million. In the quarter, gross margins remained flat at 77.3%, but operating margins came in at -1.5%, which was better than the consensus estimate. Notably, adj EBITDA came in at -$102k, which was a major step towards breakeven. Balance sheet-wise, BIGC exited 3Q23 with $266.5 million in cash and liquid assets and $339.8 million in debt, netting off to $73.3 million in net debt.

{kind=link}

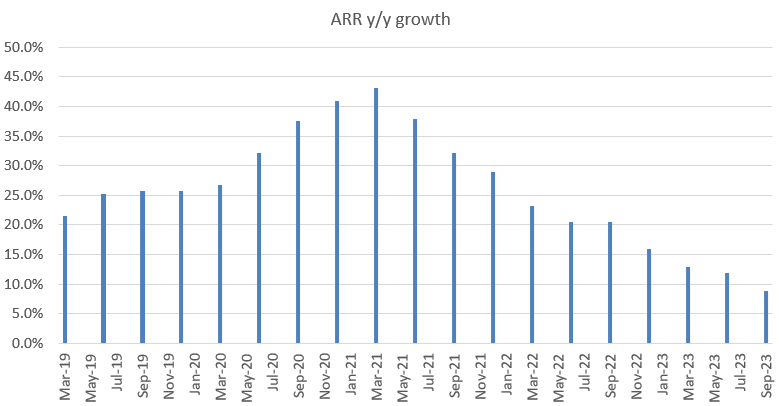

The problem with BIGC's latest result is that it has shown signs of growth fatigue, especially in the ARR metric, which is closely monitored by investors. In 3Q23, BIGC reported a total ARR of $332.2 million, representing 8.8% growth, which is 310 bps slower than 2Q23. If we plot the y/y growth over the past 10 quarters, growth has decelerated in every single quarter, which paints a very negative growth outlook. Even more depressing is that ARR softness was seen across both Enterprise and non-enterprises. Non-Enterprise ARR grew 2.6% y/y, a slowdown from 5.9% y/y growth in 2Q23. Enterprise ARR grew 11.4% y/y, which was also a slowdown from the 14.4% y/y growth in 2Q23. ARR growth performance has confirmed that BIGC is still facing multiple headwinds, and I do not see them easing anytime soon. I now believe top-line growth in 4Q23 is going to remain pressured due to two reasons:

- With the macro environment remaining sluggish, BIGC will continue to see longer sales cycles as businesses scrutinize budgets and tighten their spending.

- 4Q23 is going to be a weak quarter as new customers are electing to move launches to 1Q24.

- Enterprise ARR is unlikely to reaccelerate in 4Q23, as management expected Enterprise ARR growth to finish the year in the low teens (mentioned in the 2Q23 call ). FY22 enterprise ARR was $835 million, assuming the low-teens is 12%; this implies a 4Q23 enterprise ARR of $230 million, or 2.7% y/y growth. This actually implies another quarter of growth deceleration.

However, I see a bigger headwind over the medium and long term. In the 3Q23 call , management specifically called out the competition with Shopify ( SHOP ) in the mid-market segment. Comparing SHOP 3Q23 growth performance against BIGC, the delta is extremely huge. SHOP grew 25.5% in revenue, and BIGC non-enterprise ARR only grew 2.6%. While non-enterprise ARR is not the majority of ARR, it is still ~30% of total ARR. SHOP is a very well-run business that has a stronghold in the small-and-medium business [SMB] vertical. Unlike BIGC, all their research and development dollars are invested to make the lives of SMBs easier. Moreover, SHOP is a much bigger business that has already turned EBITDA positive. They have sufficient balance sheet capacity to replicate whatever BIGC offers in the mid-market segment. My worry is that SHOP will continue to chip market share away from BIGC, and BIGC will continue to see growth headwinds for the long term.

The good news for BIGC shareholders is that management continues to focus on driving profitability upward. While growing topline is important, I think balancing growth and profitability should be the focus now. To do this, management is adjusting its go-to-market [GTM] strategy with a focus on:

- Land and expand,

- Multi-product sales

In other words, the goal seems to be increasing ARPU by cross-selling and upselling products. This makes sense as the customer acquisition cost [CAC] is already spent. It is cheaper and more efficient to upsell more products as the relationship is already built (i.e., the sales pitch is easier than convincing a new business to adopt BIGC). The bull case here is that growth will start to reignite as BIGC could identify spots in existing customers' operating processes to upsell certain products. This, along with lower CAC, will drive operating leverage, pushing BIGC further into profitable territory.

With the change in GTM strategy, I also felt positive about management making the right decision to downsize the team. Management announced another round of RIF by 7%, representing the second RIF in the last 12 months. In this round of cuts, the sales team is expected to see the greatest reduction in headcount. Now that the GTM strategy is to focus on driving up ARPU and not chasing new customers, it makes sense to have fewer boots on the ground. This reduction should serve as another boost to driving BIGC profit margins upward. On expectations, management commented that this RIF could add between 5% and a high single-digit percentage to adj EBITDA margin in 2024. Put together, there is a very high chance for BIGC to turn profitable in FY24.

Overall, I think the 3Q23 results dealt both positive and negative cards to me. On the positive side, BIGC is very likely going to be profitable in FY24, supporting my view that BIGC has the potential to sustain positive adj EBITDA. On the negative side, growth is weak and is likely to remain weak with competitive headwinds. I like that management is balancing growth and profit, but I am downgrading my rating to a hold rating as I want to monitor how successful the new GTM strategy is. If the new GTM strategy works and shows signs of growth acceleration (negating the macro and mid-market competition headwinds), then I will be happy to jump back on the ship again.

Valuation

Author's work

The 3Q23 results have forced me to be more conservative about my estimates and beliefs. I now expect growth to be subdued in FY24 given the headwinds I mentioned above, followed by a potential recovery in FY25 as BIGC successfully streamlines its GTM strategy and drives reacceleration in growth. Specifically, I expect FY23 to grow at 10% ($307 million as management guided), and FY24 to grow at 5%, and FY25 to grow at 10%.

SHOP is trading at 11.5x forward revenue, while Squarespace is trading at 3.8x forward revenue. I continue to see BIGC trading at a discount to these peers as it expects relative growth to remain weak. From a historical perspective, this is near the lowest that BIGC has ever traded, and I believe the market will continue to price this at the current 2.3x forward revenue until BIGC shows that growth can match peers' level of high-teens to 20+% growth.

With my revised assumption, my target price is now $9.60.

Risk and final thoughts

The upside risk is that BIGC could see growth reaccelerate in FY24 if the GTM strategy turns out to be very successful. The improved growth profile will drive higher revenue with lower marketing costs, driving substantial EBITDA growth. Not only that, but sentiments will also surely turn for the better as BIGC will not be viewed as a shared donor.

To end this post, I am downgrading my rating from buy to hold. While the company demonstrated positive steps towards profitability in 3Q23, I now have concerns regarding its decelerating growth. The new GTM strategy should drive a balance between growth and profitability, however, this also brings uncertainty that I am not comfortable with at the moment. The potential for profitability in FY24 is promising, yet the competitive landscape and macroeconomic environment may continue to hinder short-term growth.

For further details see:

BigCommerce: Rating Downgrade As Growth Outlook Is Weak