BH - Biglari Holdings: Sum-Of-The-Parts Valuation Implies Significant Upside

2023-07-10 14:01:46 ET

Summary

- Biglari Holdings is currently trading at a 69% discount to our current sum-of-the-parts valuation, following an assessment of its insurance, oil and gas, restaurant, and investment operations.

- The company is under-followed and misunderstood with multiple upside catalysts.

- Highly successful cash harvesting strategy at oil and gas operation with upside potential in Permian and Delaware Basin assets.

- We anticipate $40 million in cash distributions from Steak n Shake to the holding company in 2023 through existing cash and sale of closed restaurant real estate.

In this article, I will review how Biglari Holdings (BH) has quietly assembled a diverse portfolio of wholly owned companies and investments and develop a sum of the parts valuation for the company. Where investors once bid up the stock to 3.00x book value, Biglari Holdings is currently trading at 31% of our sum of the parts valuation.

Insurance Operations

First Guard Insurance Company

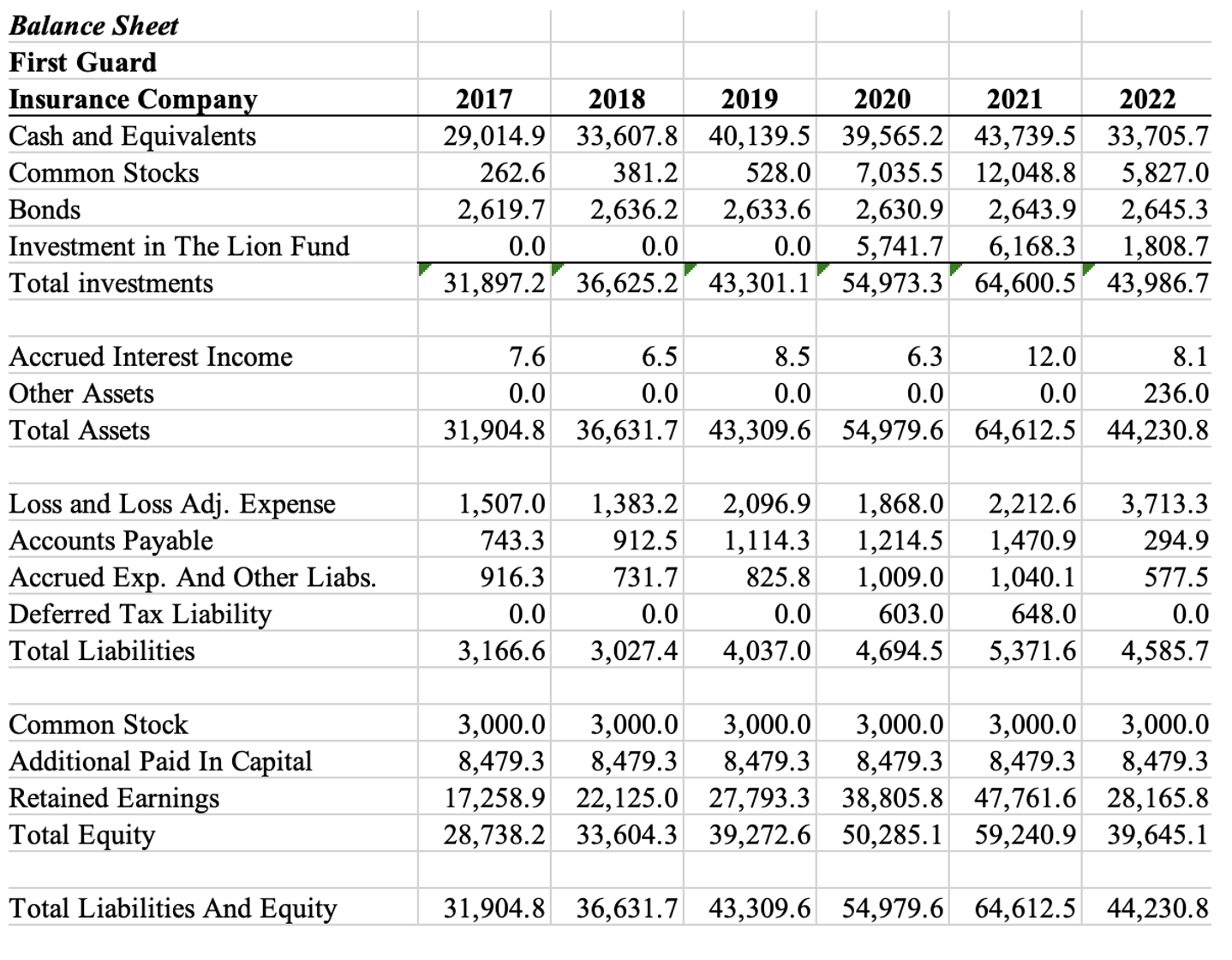

Biglari Holdings entered the insurance industry with its acquisition of First Guard Insurance Company in March 2014. Founded in 1937, it is a direct underwriter of commercial trucking insurance selling physical damage and non-trucking liability insurance to long haul owner-operator truckers. By selling direct to the end user (think GEICO for truckers) the company is able to bypass independent agents and brokers and operate as a low-cost provider with extraordinary efficiency.

Despite a $22 million distribution in 2022 for the Abraxas Petroleum acquisition, statutory financial statements show exceptionally strong liquidity, low leverage and outstanding operating efficiencies. Although the company’s product line is narrow, its extensive expertise in the trucking physical damage market, coupled with an experienced management team led by Ed Campbell and Drew Toepfer, as well as a disciplined risk management system, has resulted in consistently favorable loss development and a long, consistent track record of successful operations.

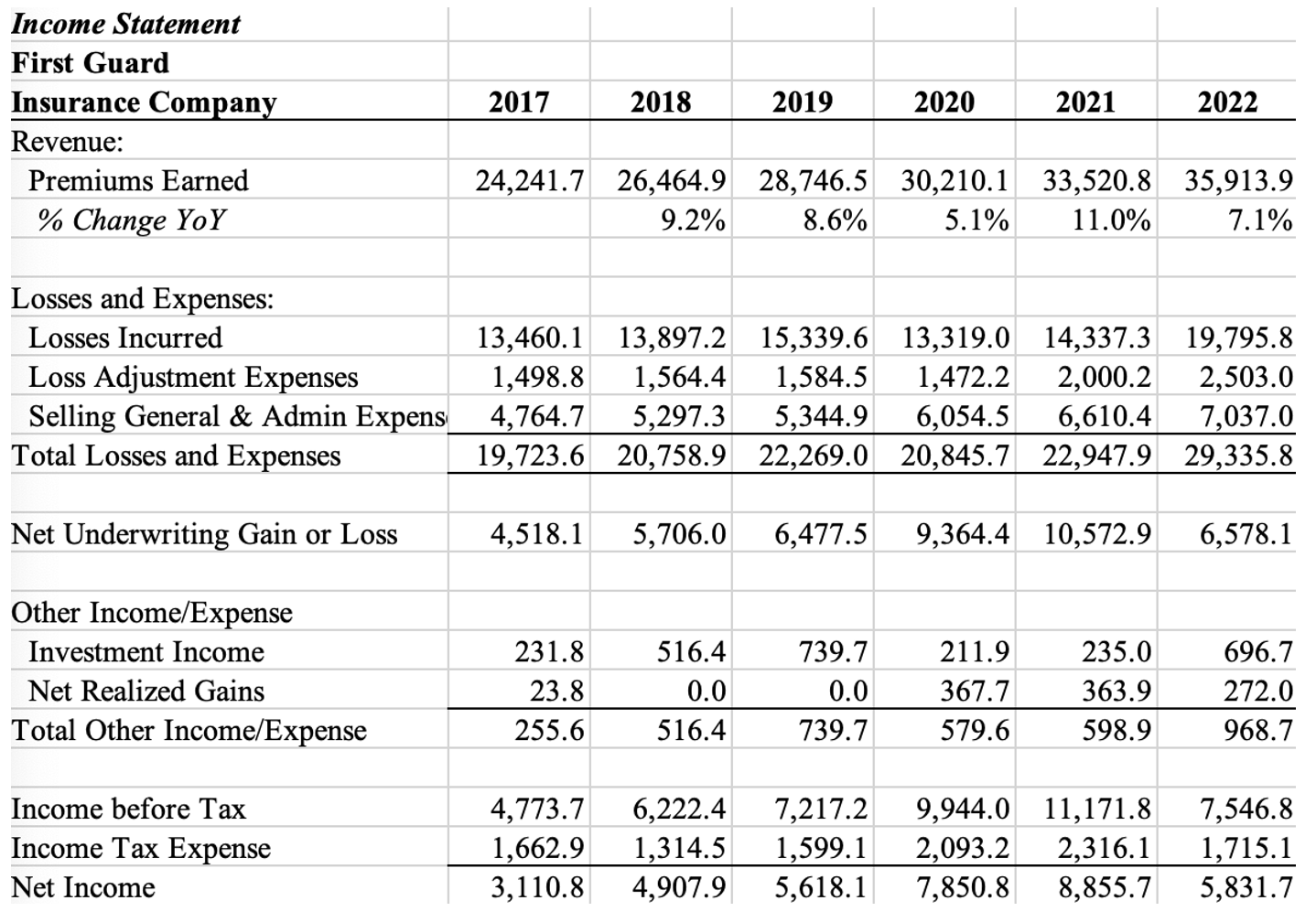

Historic financial performance is detailed below. Management projections provided with 2022 statutory statements anticipate revenues growing 9.2% in 2023 to $36.8 million and net profit before taxes of $8.0 million driven by improved loss rates.

{kind=link}

Company Statutory Financial Statements

{kind=link}

Company Statutory Financial Statements

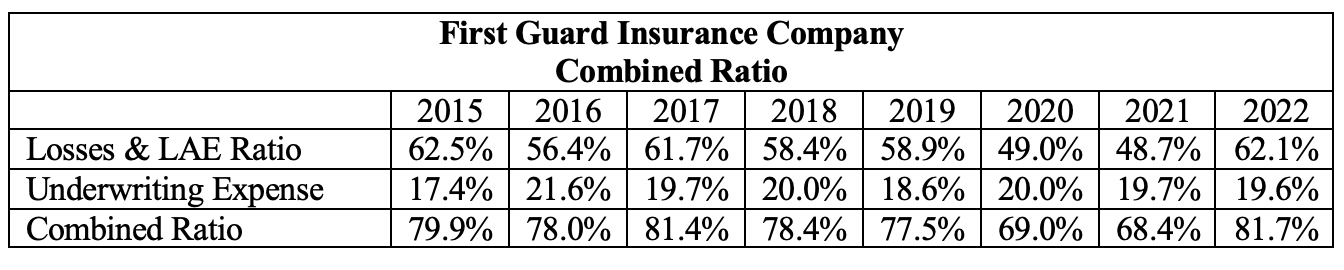

A company’s combined ratio is the traditional measure of underwriting profitability used in the property casualty insurance business representing the ratio of net losses and loss expenses and underwriting expenses to net premiums.

{kind=link}

Company Statutory Financial Statements

First Guard’s historic underwriting results have been outstanding, driven by the company’s low cost, direct-to-the-trucker business model and strong underwriting discipline. Loss experience was distorted in 2020 and 2021 due to the COVID lock downs. Losses increased in 2022 due to higher average repair costs due to higher inflation. Management projects the combined ratio falling to 79% in 2023, consisting of a Loss & LAE ratio of 59.2% and an Underwriting Expense ratio of 19.8%.

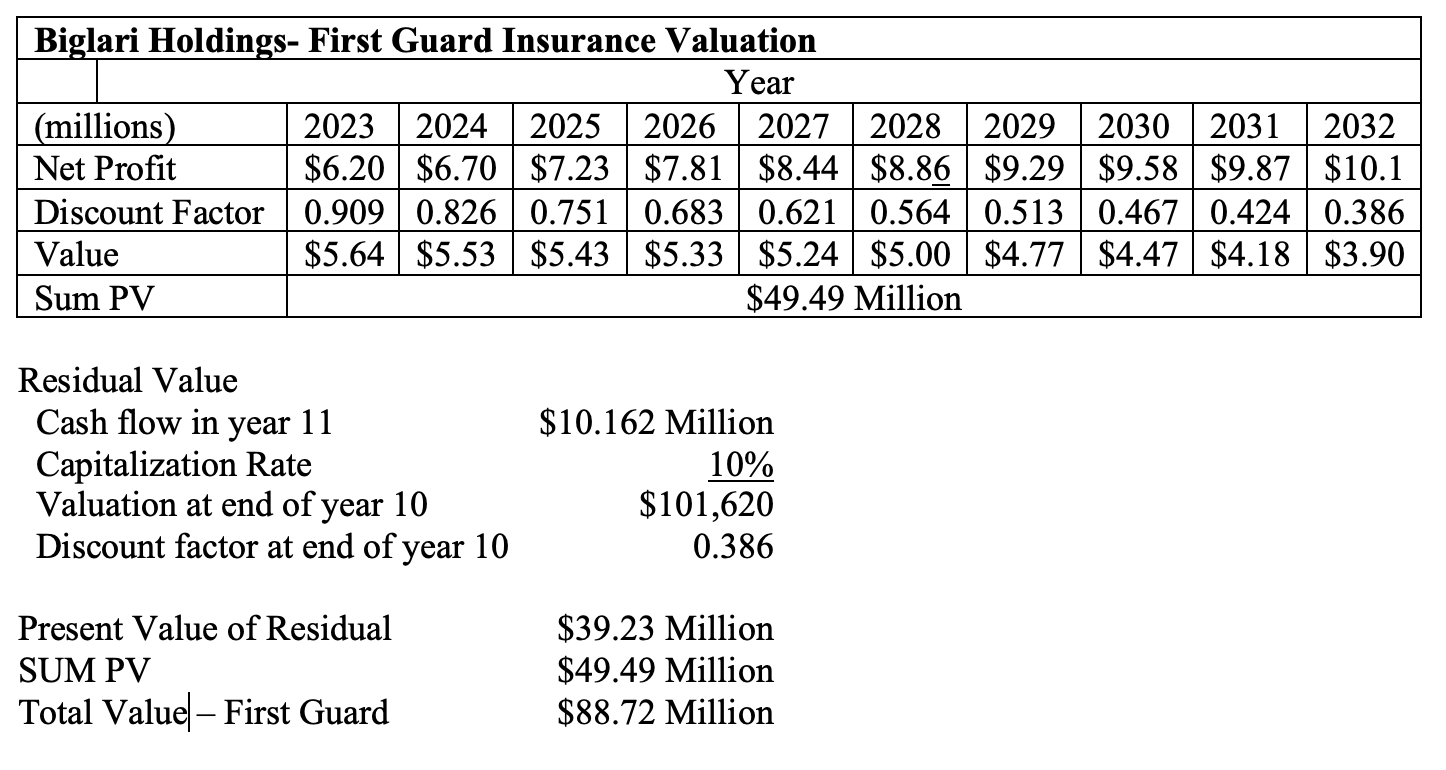

Valuation – First Guard Insurance Company

Typically, we would use a balance sheet multiple to establish a valuation for an insurance company, but given First Guard’s long-term outstanding financial performance and the distortion of the recent distribution, the two-step discounted cash flow method is more applicable in this case.

Given First Guard’s long history of converting net profits to cash and investments, we will use projected net profits for our cash flows. We project 2023 profits of $6.2 million, increasing by 8% through 2027, 5% in 2028 and 2029, 3% in 2030 through 203,2 and 0% thereafter. We use a 10% discount rate to make things easy.

{kind=link}

Projections prepared by author

Biglari paid $34.1 million for First Guard in March 2014 when the company had a total book value of $18.3 million, sales of $7.7 million and net profits of $1.4 million. Since that time, book value has grown to $39.6 million (not counting the $22 million distribution), sales of $35.9 million and net profits of $5.8 million. The estimated value of $88.72 million would appear reasonable based upon these results and future growth opportunities.

Sardar Biglari shared high praise for First Guard and its management team at the 2023 annual meeting saying it is best-in-class in terms of claims management, operations and data analytics and that Ed Campbell and his team are deeply experienced and of the highest integrity. Biglari was particularly excited about a new growth opportunity being developed by Drew Toepfer, the company’s chief executive officer.

Trucking companies typically provide owner operators insurance coverage for liability and cargo contents for owner operators. This cost can be expensive and First Guard is currently developing products tailored to meet this need as a full package of insurance coverage including physical damage and liability at a lower cost for the operator.

Using First Guard’s deep data analytics, the target customer base will be existing clients. They plan on starting out slow with 15 policies a month. If things go as planned, management indicates this launch could have a material impact on the company’s earnings. Biglari shared that First Guard currently insures 17,000 trucks and trailers. If the company is successful in converting just 1,000 units to the new coverage, revenues could increase by 50%. This could have a material upside impact on the estimated value of the company.

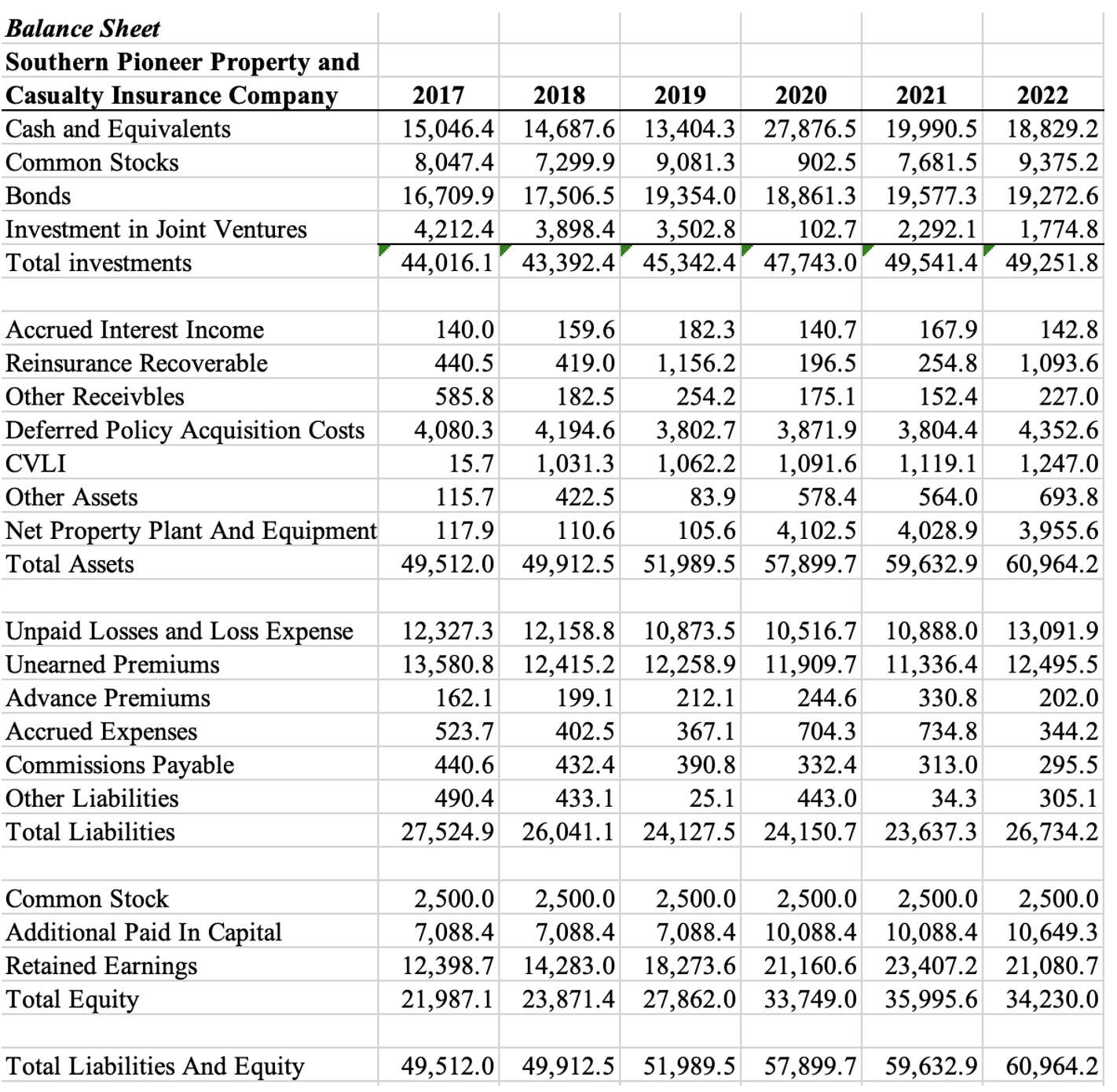

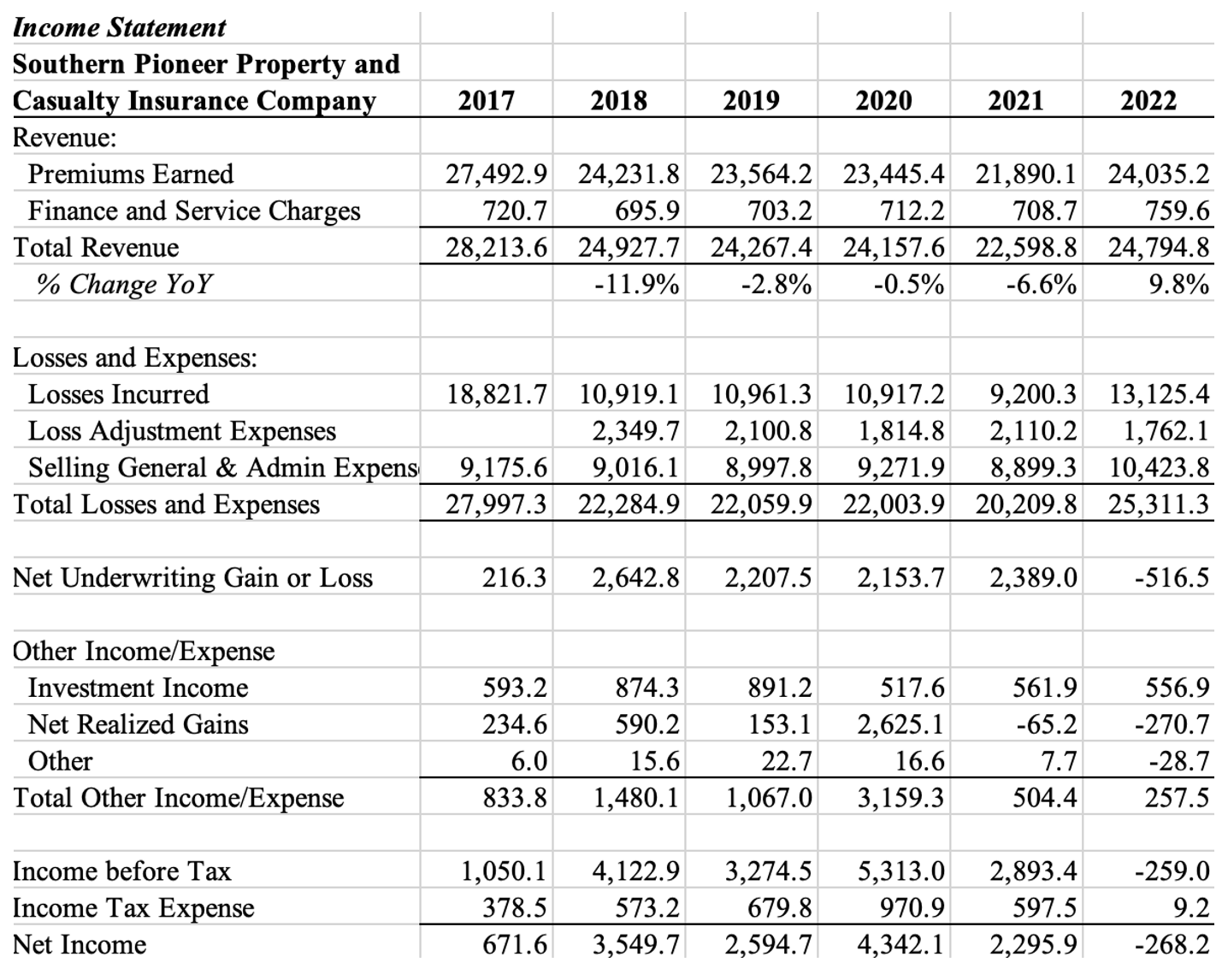

Southern Pioneer Property and Casualty Insurance Company

Southern Pioneer was founded in Jonesboro, Arkansas, in 1981 by brothers Ben and Hal Heyman and provides specialty insurance products including garage liability for non-franchised auto dealers, commercial property, homeowners, dwelling fire, collateral protection, liquor liability and other miscellaneous insurance products.

Biglari announced the acquisition of Southern Pioneer in March 2020. The purchase price was $45.5 million and included $4.06 million for the company’s real estate owned in a separate partnership, resulting in a price to tangible book value of 1.42x.

Premiums earned for Southern Pioneer increased $2.1 million or 9.8% in 2022 driven by liquor liability and collateral protection lines business. Net worth grew consistently between 2017 and 2021; however, capital declined in 2022 as a result of underwriting losses related to elevated weather activity, unrealized capital losses related to the stock market, increased costs due to the implementation of a new IT system for the agent network as well as higher losses on bar and tavern liquor liability. Selling and General Administrative expenses are anticipated to fall to 40% in 2023 from 42% the previous year as a result of the completion of the IT implementation.

Southern Pioneer shows significant liquidity and modest leverage. Cash and investments totaled $49.3 million at 2022 with an appropriate investment mix for a long tail type insurer. Bonds are carried as available for sale and are relatively short duration at 1.8 years while cash is invested largely in short term treasuries. Common stock investments primarily represent holdings in Biglari investments, Ferrari, Taiwan Semiconductor, Jack in the Box, and Alibaba.

{kind=link}

Company Statutory Financial Statements

{kind=link}

Company Statutory Financial Statements

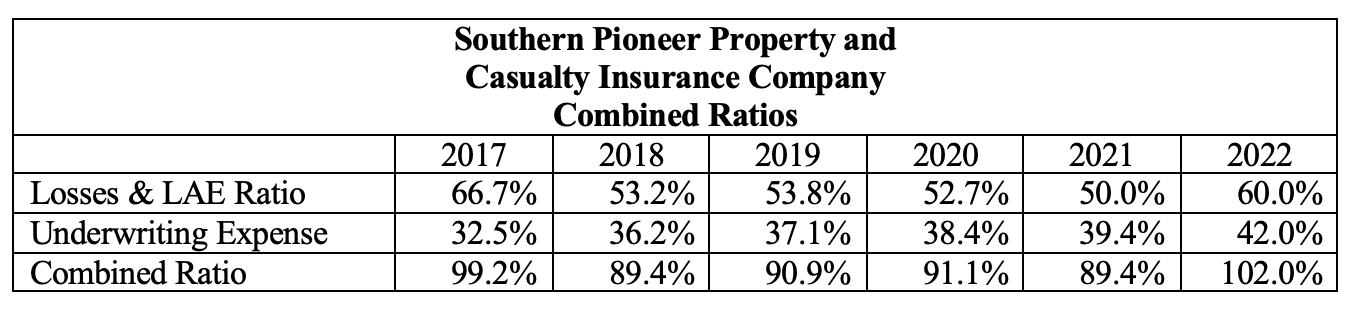

Southern Pioneer’s combined ratio was fairly consistent from 2018 to 2021 before jumping to 102% in 2022 primarily due to two major CAT weather events and the liquor liability segment. Given recent pricing actions as well as anticipated lower underwriting expenses, the combined ratio should show significant improvement in 2023.

{kind=link}

Company Statutory Financial Statements

Valuation – Southern Pioneer Property and Casualty Insurance Company

The best valuation method for a traditional insurance company like Southern Pioneer is a multiple of tangible book value. With expectations that performance will improve back to historic levels in 2023, the original purchase multiple of 1.42x should still be valid. Based on 2022 tangible book value of $34.23 million, Southern Pioneer’s valuation is estimated at $48.6 million. Combined with the First Guard valuation of $88.72 million yields a combined valuation for Biglari’s insurance operation of $137.3 million.

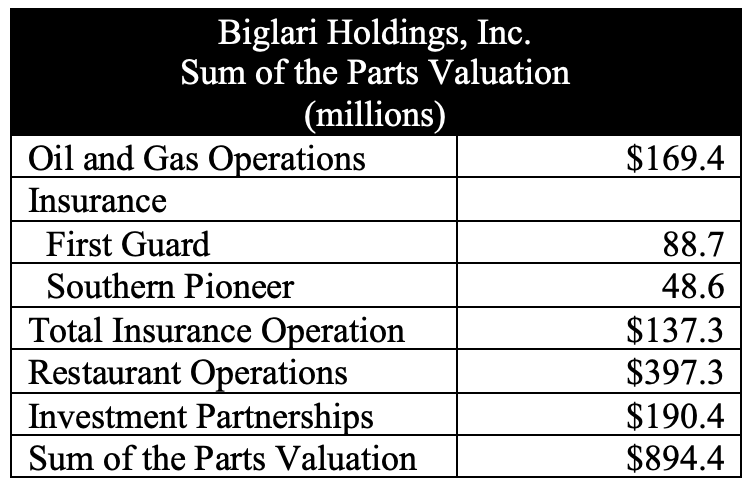

Total Valuation of Biglari’s Insurance Operations- $137.3 Million

Oil and Gas Operations

Biglari’s oil and gas operations do not engage in risky exploration or drilling activities but rather seek to benefit as a liquidator of other companies’ capital expenditures. This has created a gusher of cash flow coming out of the ground which is being pumped back to Biglari for investment outside of the oil industry.

In line with this philosophy, the company has made two material acquisitions since 2019.

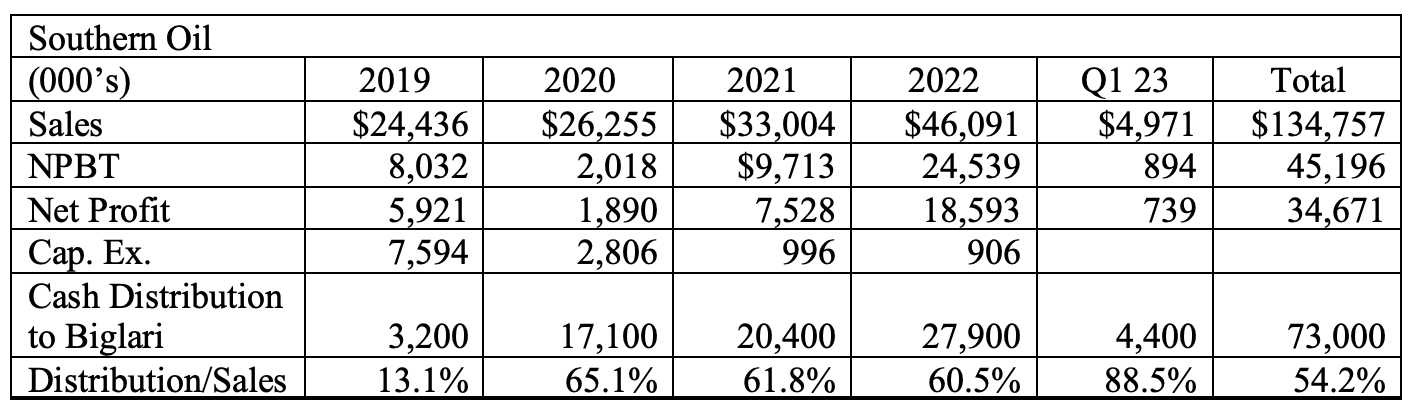

Southern Oil

RAAM Global Energy Company filed for bankruptcy in October 2015. Senior secured lenders acquired the assets under a newly formed entity in April 2016, which was then sold to a private equity firm. In 2019, the PE firm made the decision to exit the fossil fuel industry due to ESG considerations. The private equity firm proved to be a motivated seller, and Biglari was an opportunistic buyer, acquiring Southern Oil in September 2019 for $51.5 million in cash.

At the time of the acquisition, the company operated 13 producing wells and developed pipelines from 10 platforms in the shallow waters of the Gulf of Mexico. Expenses and workforce were significantly reduced to focus exclusively on maximizing production on existing wells and ongoing maintenance.

Biglari measures the economic performance of the oil companies not by the amount of oil produced or the level of profit, but from the cash generated relative to the capital invested. Historic results since acquisition have been outstanding.

{kind=link}

Company Financial Information

Southern Oil has generated $134.8 million in revenue and pumped $73 million in cash distributions back to Biglari Holdings since acquisition. Required capital expenditures over the last two years to maintain production have averaged less than $1 million per year. Revenue and profits were down in Q1 23 due to decreased oil prices compared to last year as well as decreased production from two wells during the period due to geologic pressure problems. Biglari believes these issues will be corrected but that production volume and cash flow will naturally decrease over time.

Looking to future production, a reserve analysis prepared by Netherland, Sewell & Associates as of 12/31/22 shows proved producing oil equivalent reserves of 1,411.3 MBBL. For the sake of simplicity, we will assume a future price of oil of $75 and total future revenues of $105.8 million. Cash distribution conversion at Southern Oil has averaged 62.5% from 2020 through 2022. Assuming that rate drops to 50% due to reduced well efficiency, it is reasonable to assume an additional $45 million to $55 million in cash distributions to Biglari over the remaining useful life of the wells.

Abraxas Petroleum Corporation - We’ve Seen This Movie Before

In January 2022, Abraxas Petroleum announced a restructuring of its existing debt through a multi-part interdependent de-levering transaction consisting of the sale of its oil and gas assets in the Williston Basin of North Dakota, pay off of its first lien debt obligations from the proceeds of the sale, and a debt for equity exchange with its second lien debt holder, Angelo Gordon & Co. The investment group was owed a total of $145 million, including a $10 million exit fee, which was exchanged for a new preferred stock representing 85% ownership in the company. Shortly after the restructuring, Angelo Gordon made the decision to exit the fossil fuel industry due to ESG considerations. Once again, a motivated seller meets an opportunistic buyer.

Biglari sent the investment firm a one-page offer sheet for the preferred stock on September 5, 2022, for $80 million and nine days later they closed the transaction. Shortly after the closing, the preferred stock was converted into 90% ownership in the common stock and Abraxas was consolidated with Biglari Holdings.

At the time of the acquisition, Abraxas had $25.1 million in cash on the balance sheet and a corporate headquarters building that has subsequently been sold for $5 million, effectively reducing Biglari’s purchase price by $30.1 million to $49.9 million. For this price, the company acquired prime acreage and 66 producing wells pumping 2,100 barrels of oil equivalents a day in the lucrative Permian and Delaware Basins with proved producing reserves valued in excess of $100 million .

After the acquisition, Biglari pulled out the Southern Oil playbook, parting ways with the company’s CEO and Chief Financial Officer, while significantly reducing costs and headcount to focus exclusively on maximizing production on existing wells and ongoing maintenance.

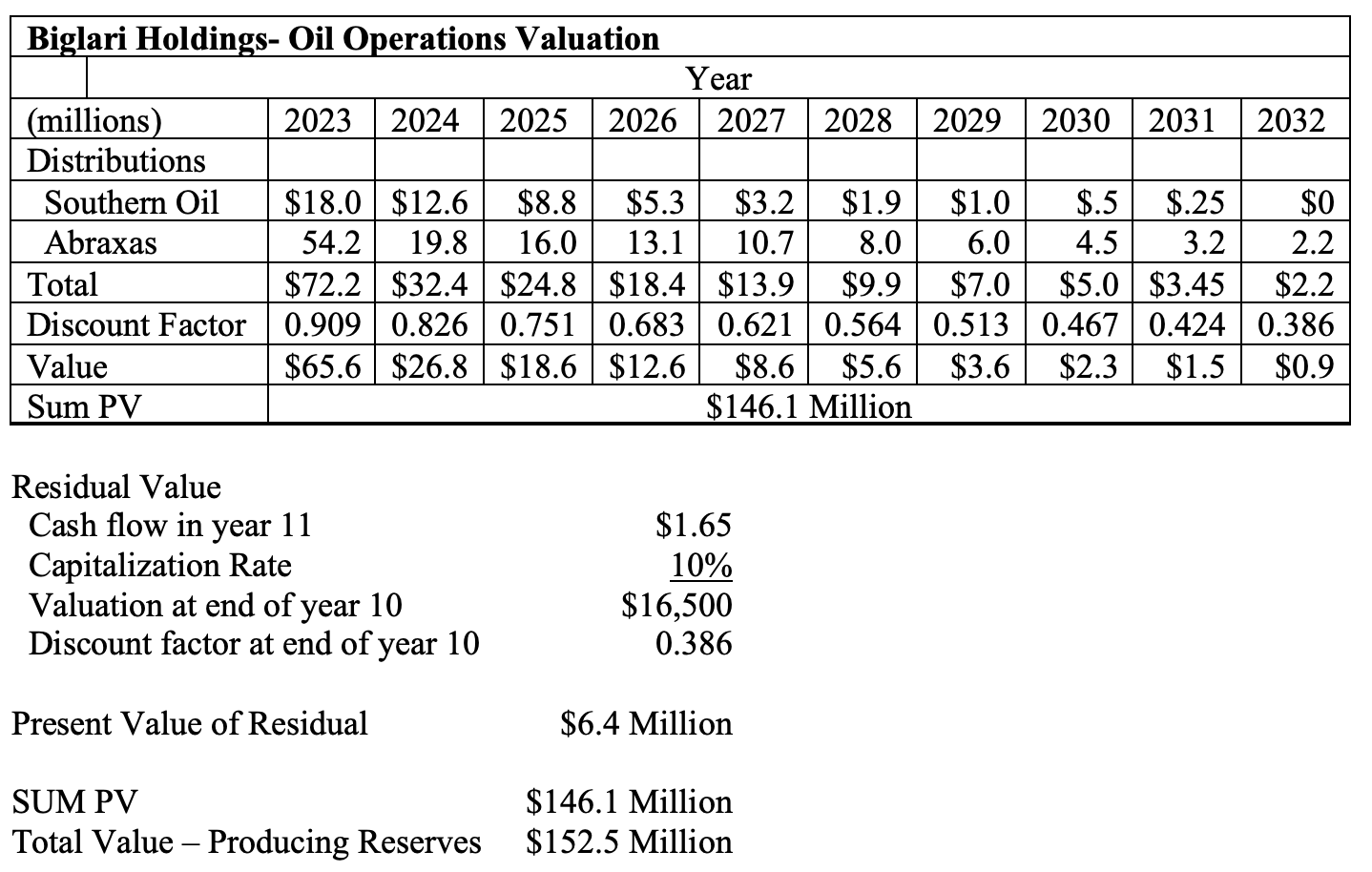

Oil and Gas Operations – Discounted Cash Flow Valuation Method for Producing Wells

Southern Oil’s historical performance provides critical insight for approximating future cash distributions from both Southern as well as Abraxas and we will use the two step discounted cash flow method for the valuation.

We assume Southern Oil corrects the geologic pressure issues that impacted production at two wells during the first quarter and cash distributions drop to $18 million in 2023 from $27.9 million the previous year. We project cash distributions dropping by 30% per year through 2025, 40% per year from 2026 through 2028, 50% per year from 2029 through 2031 and zero in 2032. Total cash distributions are projected to be $51.55 million.

Biglari indicated at the 2023 annual meeting that he expects cash distributions from Abraxas of $90 million over the next three years. We further know that $30 million was realized at closing with cash on the balance sheet and the sale of real estate. We assume $24.2 million in additional cash distributions from Abraxas operations in 2023 for a total of $54.2 million. We project cash distributions to drop by 18% per year through 2027, 25% per year from 2028 through 2030 and 30% per year in 2031 and 2032. Total cash distributions for the ten-year period are $137.7 million. We use a 10% discount rate consistent with our First Guard Insurance valuation.

{kind=link}

Projections Prepared by Author

The projected future cash distributions at Abraxas may prove to be conservative in light of Biglari’s track record at Southern Oil where distributions actually increased during the first four years of ownership. Our projected value of $152.5 million for the producing wells seems reasonable with upside potential should cash flow exceed expectations.

As Steve Jobs would say, “But Wait, There’s One More Thing”

The typical oil and gas company invests a significant amount of capital in risky exploration and drilling operations to expand its reserve base. Any CEO who fails to do so would likely lose their job. However, Biglari does not come from the oil and gas industry so he approaches the business from a completely different perspective. Costs are held at a minimum and capital expenditures are only used to maximize production from existing wells.

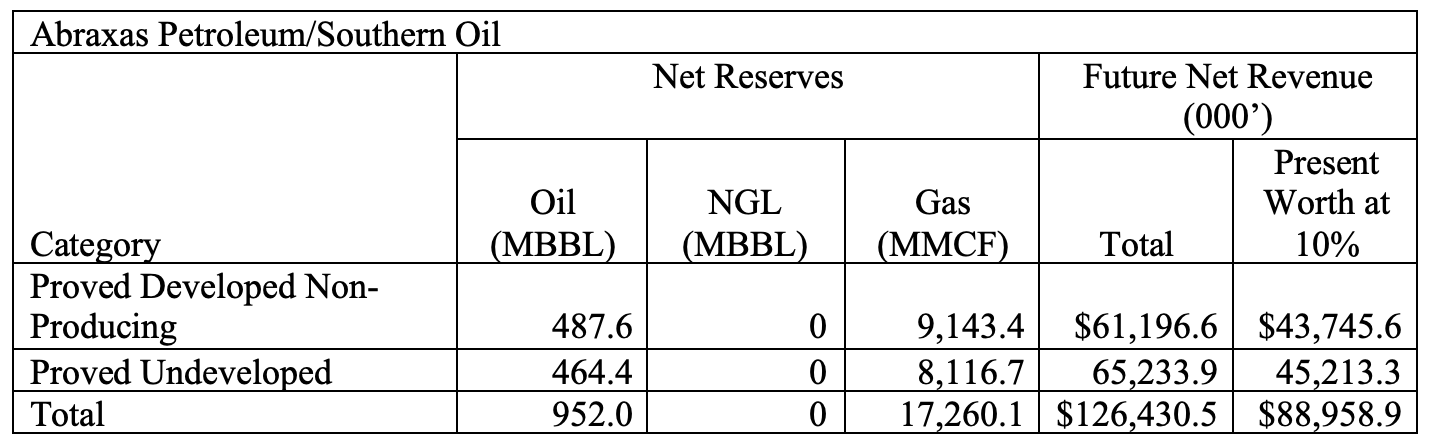

Because Biglari has made the decision to only focus on the production of oil from existing wells and not engage in the riskier exploration and development of new wells, Proved Developed Non-Producing Reserves and Proved Undeveloped Reserves are not included on the balance sheet.

{kind=link}

Reserve report for combined Abraxas Petroleum and Southern Oil to Biglari Holdings as of 12/31/22 dated 2/24/23 from Netherland, Sewell & Assoc.

That does not mean these reserves do not have meaningful value. Proved Developed Non-Producing Reserves are those for which the well-bore exists and the reserves are identified but are not currently producing. Proved Undeveloped Reserves are on undrilled acreage offsetting producing wells that are reasonably certain of production when drilled.

Biglari owns developed energy infrastructure, undeveloped leases, existing geologic support, and reserves located in the lucrative Permian and Delaware Basins. While nothing is currently in the works, the properties make for an enticing joint venture opportunity with an established E & P company. This will serve to shift the capital requirements and risks associated with development while sharing in the potential rewards. For valuation purposes, let’s say these reserves are worth 25% of the present value of future net revenue ($88,959), or $22.2 million.

Finally, it is anticipated that Biglari will buy out the minority shareholders in Abraxas at some point. The stock no longer trades on any exchange and the holding is totally illiquid. We will assume $5.0 million to buy the remaining shares. Total valuation is ($152.2 million + $22.2 million - $5.0 million)

Total Valuation of Biglari’s Oil and Gas Operations- $169.4 Million

Restaurant Operations - Western Sizzlin

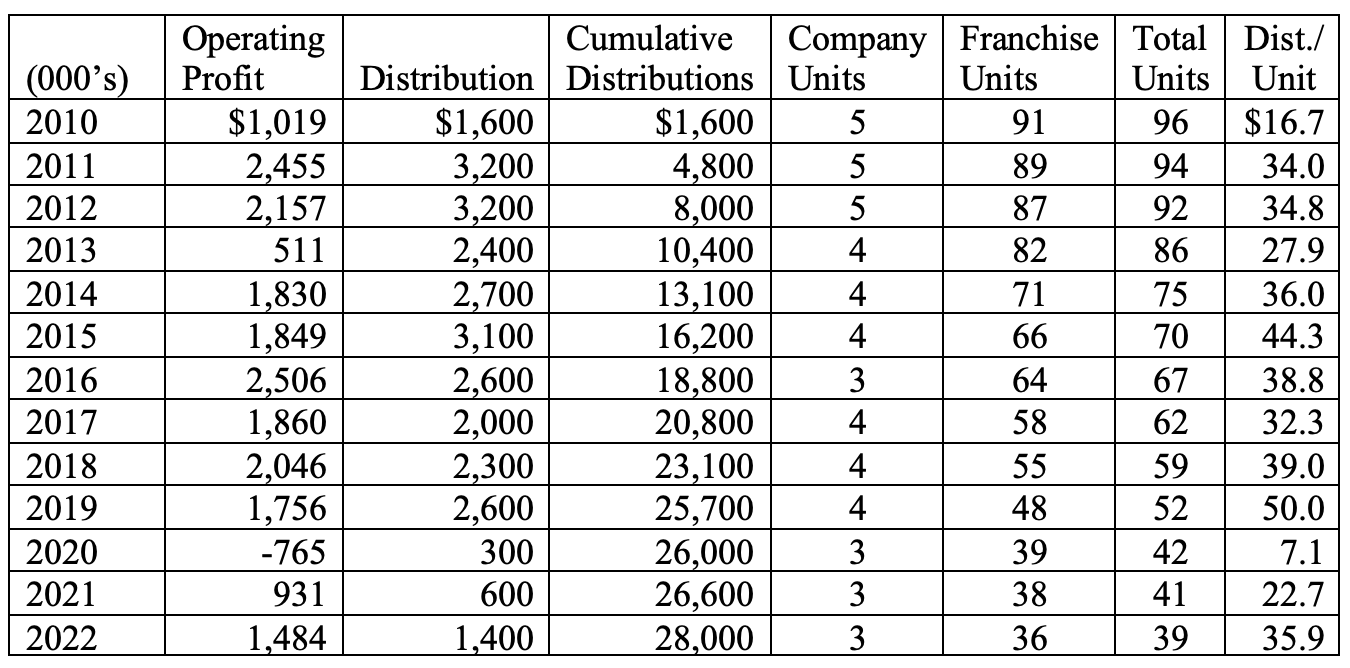

Biglari Holdings acquired Western Sizzlin in March 2010 for an effective purchase price of $21.7 million , which included $2 million in marketable securities and 11.4 acres of commercial vacant land in San Antonio, Texas.

Results since acquisition have been quite remarkable. Biglari realized that Western Sizzlin was a mature concept/brand deep in the decline stage of its business lifecycle. From the outset, the intent was to pursue a cash cow strategy generating cash distributions to the holding company rather than reinvesting capital back into the business with slim hopes for market returns.

Through 2022, Western Sizzlin has generated total distributions of $28.0 million. When combined with the marketable securities ($2.0 million) and raw land ($8.2 million tax valuation), shareholders have realized $38.2 million in value from the investment, and cash is expected to continue flowing to the holding company for some time to come.

{kind=link}

Company Financial Information

Western Sizzlin also highlights the considerable profitability of a franchise-based business model. While the company has experienced a 60% reduction in unit count since acquisition, cash distributions per year held relatively stable leading up to the pandemic. COVID impacted 2020 and 2021; however, results improved in 2022, and cash distributions per unit returned to its normal average at $35,900.

The restaurant count will continue to decline going forward but historic results suggest that there is still a significant amount of cash to be generated from the operation.

Steak n Shake

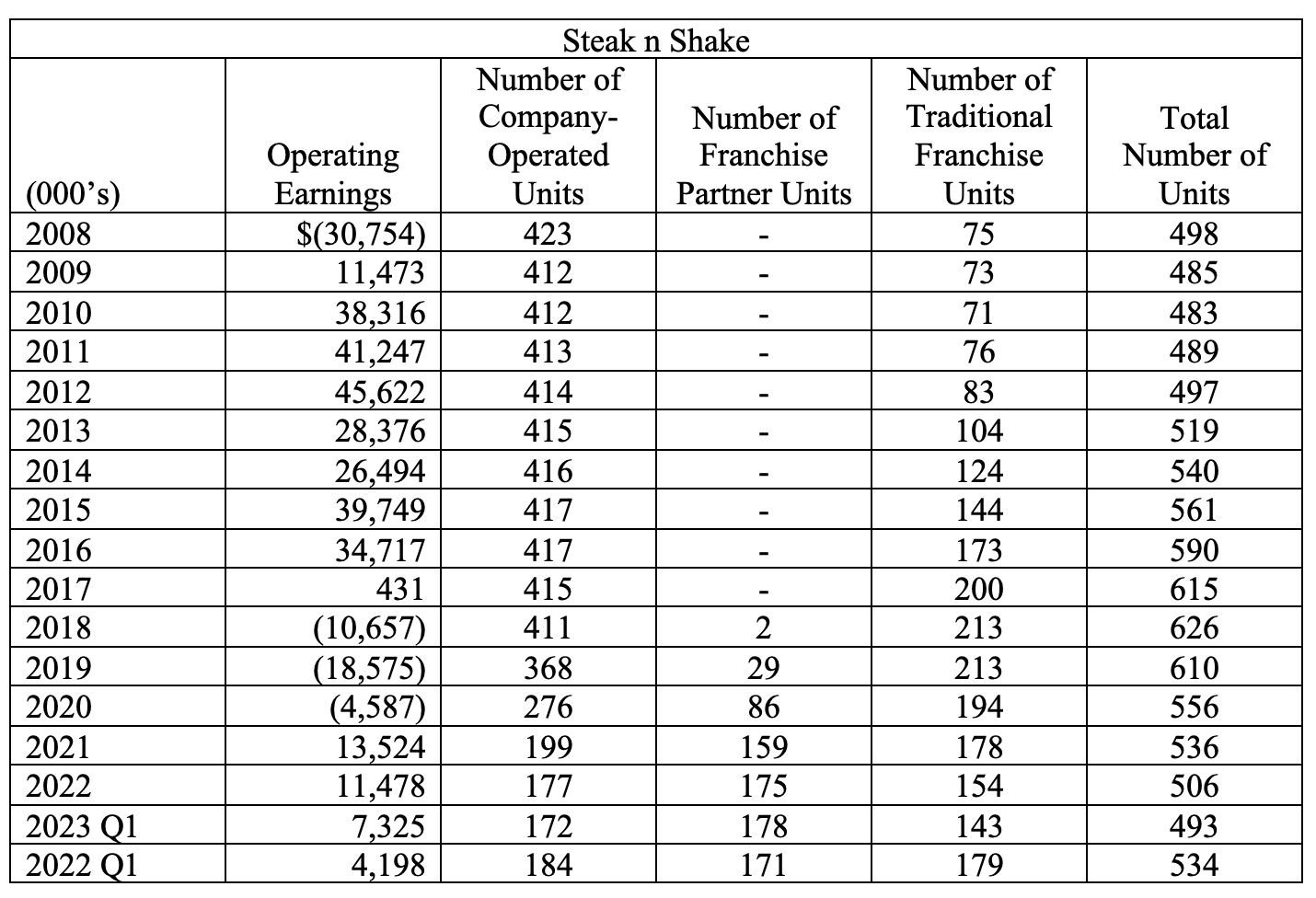

Steak n Shake showed steady profits and growth for the first eight years of Biglari's ownership. Unfortunately, cracks in the turnaround story were starting to develop. Same store sales turned negative in 2016 and fell for three consecutive years after seven years of positive growth. Steak n Shake reported its first operating loss of $10.7 million in 2018 after nine years of profitability. The company acknowledged service levels were slow which was having a material impact on customer satisfaction. Outdated equipment and a kitchen design that was ill-suited for volume production resulted in high-cost, labor-intensive slow service. While production and delivery systems could be overhauled and streamlined in order to gain value and speed, there was still one important missing ingredient.

Sardar Biglari is a keen student of the restaurant industry and it is apparent he closely follows Chick-fil-A. The company operates primarily as a franchisor with total system-wide sales of $18.8 billion in 2022 and average annual sales per restaurant in excess of $8.0 million. Although the Chick-fil-A chicken sandwich may attract considerable attention, the company’s unique franchising model is often recognized as a key contributor to its success.

Unlike many restaurant franchises that require steep upfront capital investment for a new restaurant, Chick-fil-A only requires an upfront payment of $10,000. Chick-fil-A provides the equipment, real estate and start-up costs for store operators and in return receives 15% of sales and 50% of any profit. Most franchisees are limited to operating only one Chick-fil-A restaurant and are required to be involved in the day-to-day management of the restaurant. Chick-fil-A looks for an ownership mindset in all of their store operators.

Steak n Shake Franchise Partner Program

Company owned restaurants, irrespective of the brand, have historically underperformed compared to a franchise unit, managed day to day by an onsite owner/manager. In 2018, competition for top managerial talent was fierce and turnover was high. Leadership continuity at the restaurant level suffered. To make matters worse, Steak n Shake was a minimum wage employer and restaurant staff was poorly motivated.

Unfortunately, in 2018, Steak n Shake operated 413 company owned restaurants, of which 25% of the locations were failing to meet customer service expectations and underperforming financially. The company maintained a significant capital investment in the restaurant operation through the ownership of 153 Steak n Shake restaurant locations and equipment, delivering substandard returns on capital.

Biglari realized . “No amount of technology or equipment could create a winning restaurant chain." The key missing ingredient was the right leadership in every restaurant unit. To achieve this goal, the company had to build a culture of ownership at the unit level so that operators would think and act like owners.

In August 2018, Biglari announced the Franchise Partners Program patterned after the highly successful Chick-fil-A franchise model. New franchise partners would make an upfront investment totaling $10,000. Steak n Shake would provide the real estate, equipment and start-up costs in return for 15% of revenues and 50% of any profit.

Biglari stated, “The best way to create wealth for ourselves is to first create wealth for our franchise partners.” Franchise partners would be limited to one restaurant and would be required to manage day to day operations as hands-on operators. Potential franchisees would be carefully screened based on entrepreneurial attitude, passion and the ability to deliver on the Steak n Shake brand promise. All corporate owned restaurants would be converted to the new program.

In 2019, Steak n Shake temporarily closed 107 company owned restaurants to fix issues that led to operating shortfalls. The combination of labor-intensive, slow production with high-cost table service had led to overall labor costs 6 to 8 percentage points above the competition. The locations would be reopened with counter service rather than table service under the new Franchise Partner Program.

In 2020, the pandemic necessitated the conversion of all units to the quick-service model. Instead of ordering at the table or even at the counter with an attendant, guests would now initiate their transactions at a kiosk. In 2021, the company invested between $100,000 and $200,000 per restaurant for remodeling, new point-of-sale systems and self-order kiosks.

The changes represented a radical transformation. Add a pandemic to the mix, and the turnaround became even more challenging. Biglari noted at the 2023 annual meeting that they had experienced an 11% turnover in franchise partners in 2022, or approximately 19 operators. He felt the number was too high and indicated that they have paused new franchise conversions until they can course correct and fine tune the model to ensure success. He also acknowledged the continued decline in the traditional franchise restaurant base noting that the same issues impacting company-owned restaurants have also impacted franchisees. The historic model does not match the current operating environment and there are currently 32 traditional franchised restaurants that still offer table service and have not converted to the new model. These operators are at risk and could lead to even fewer traditional franchisees in the future.

{kind=link}

Company Financial Information

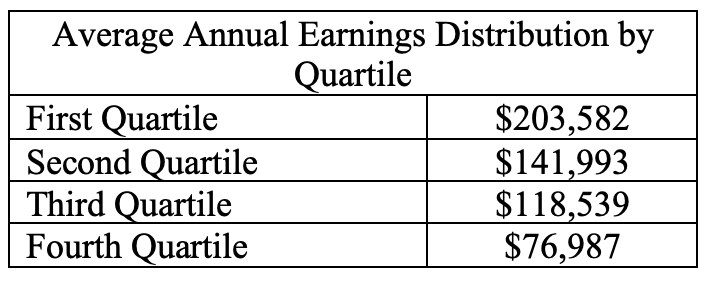

The Franchise Partner program’s early stage notwithstanding, the results are encouraging. Steak n Shake’s 2021 franchise disclosure form for the Franchise Partner program reported that the highest annual franchise partner earned $297,243 and the lowest earned $48,980. Average annual earnings were $128,383 and 34 out of 84 franchise partners, or 41%, met or exceeded the average earnings over the two-year period.

Average franchise partner annual earnings distribution by quartile during the two-year period ending 12/29/21 are detailed below. For a majority of the franchise partners, the dine in component of their business was either closed or severely restricted beginning in the second quarter of 2020 and extending through the end of 2020.

{kind=link}

Steak n Shake 2021 Franchise Disclosure Document

Over the three year period ending 12/31/22, the average franchise partner made $137,000 per year .

Starting the program from scratch during a pandemic, it shouldn’t be a surprise to see turnover in the initial group with a large percentage most likely coming from the lower quartile. In some cases, they missed on people or it wasn’t a good fit, but cracking the code in finding franchise partners is key to success and the company deserves credit in moving slowly and judiciously in expanding the program.

During the pause in conversions, they are working to recalibrate and refine their process to ensure they have the right people in the right locations to be successful. Conversions are anticipated to resume in the third quarter with 6 to 10 new franchise partners during the period. Biglari believes that there is an additional $20 million annual profit potential once remaining corporate-owned stores can be converted.

Steak n Shake reported strong results in the first quarter of 2023. Net profit before tax was $7.3 million versus $4.2 million the previous year. More importantly, franchise partner fees grew by 14.6% to $17.9 million or $100,629 per unit versus $91,368 per unit the previous year.

Biglari’s 2022 annual letter to shareholders indicated his intention to reduce Steak n Shake book net worth by approximately $44 million to $150 million through the distribution of cash and the sale of closed restaurant real estate. The company plans to sell 24 locations. Seven are currently under contract to be sold during the second quarter for $11 million while the other 17 units are listed for sale. Three other locations have been leased to Chipotle, Chick-Fil-A and Raising Cains and will be transferred to the real estate development company. Biglari believes the company should earn a 20% pre-tax cash return in 2023 on the remaining capital, or $30 million.

Valuation – Biglari Holdings Restaurant Operations

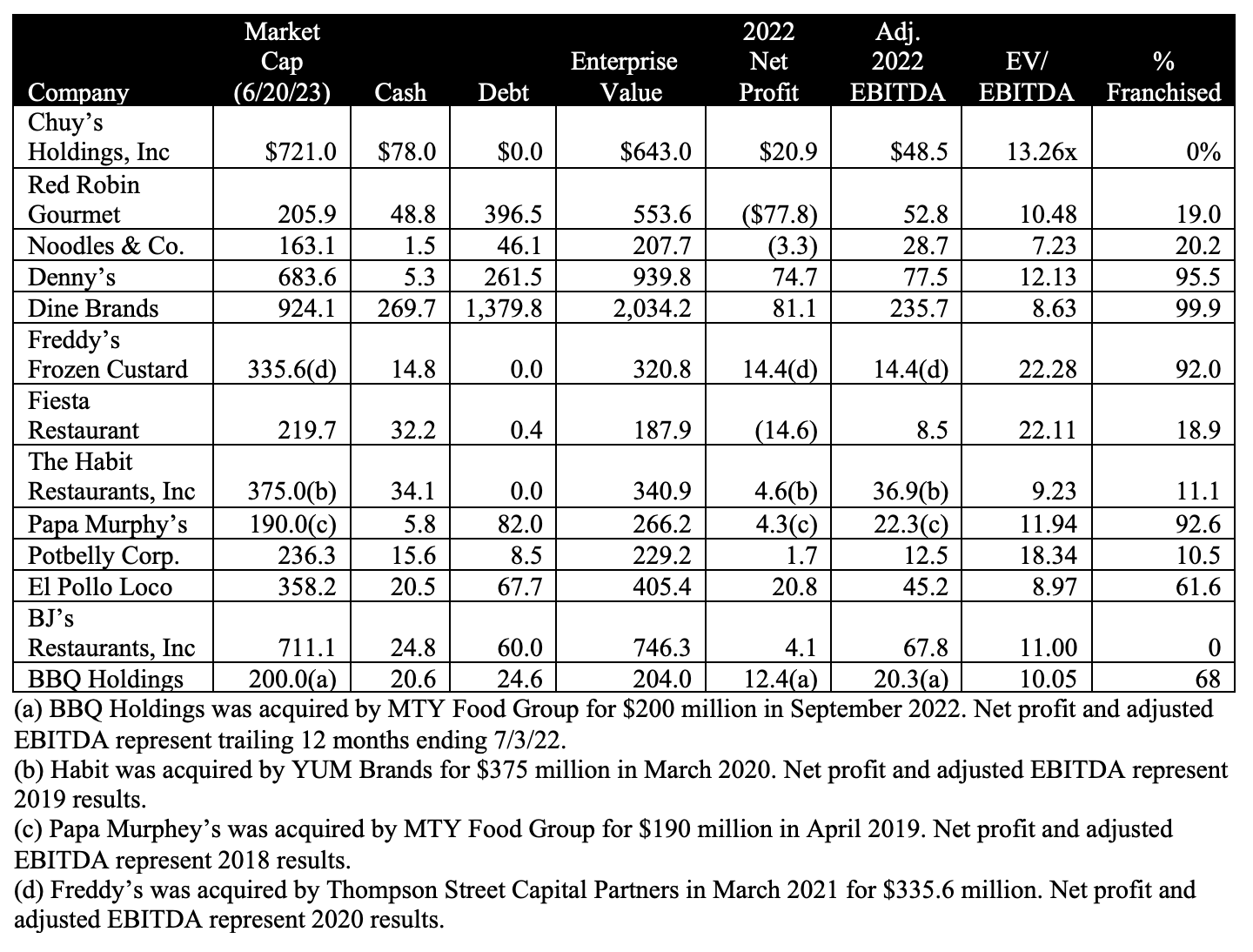

A common way to value a restaurant company is a multiple of cashflow defined as enterprise value to EBITDA. Multiples vary based upon such factors as the company’s size, growth prospects, unit mix of franchise/company owned units, profitability and market conditions. A summary of comparable restaurant companies and multiples is detailed below.

{kind=link}

Company Financial Statements and Franchise Disclosure Documents

If you throw out the high and low multiples, you see that a restaurant company typically trades in a range of between 9 to 13 times enterprise value to EBITDA. Using this methodology, we can derive an approximate value for Biglari’s restaurant operations.

First, we value existing operations using a 9x multiple to be conservative reflecting the declining traditional franchisee base as well as the ongoing transformation of the franchise partner program. Using an adjusted 2022 EBITDA for restaurant operations of $39.7 million, the approximate value is $357.3 million ($39.7 million x 9.0 = $357.3 million) + $40 million from sale of closed restaurant locations = $397.3 million.

Total Valuation of Biglari’s Restaurant Operations- $397.3 Million

Investment Operations

Sardar Biglari acknowledged Press Blakely’s wife, Helen, at this year’s annual meeting and said that the Friendly Ice Cream investment was instrumental in the development of Biglari Holdings. Proceeds from Friendly’s provided funds to purchase Steak n Shake, which provided funds to purchase Cracker Barrel, which provided funds to purchase the insurance and oil and gas companies, which provided funds to purchase additional marketable securities. It is an ever-widening circle of cash and investments.

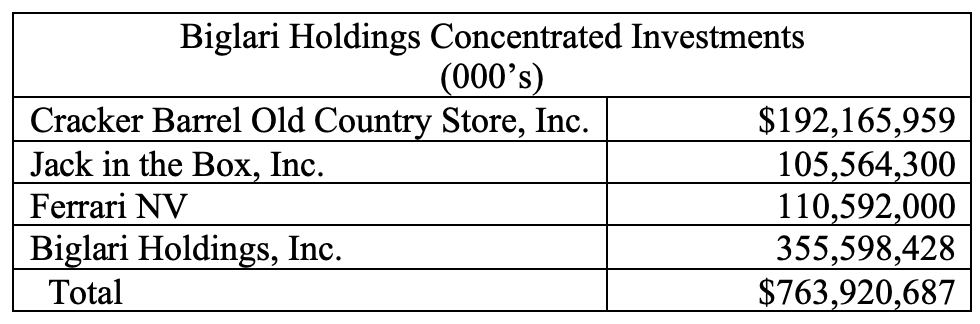

The Lion Fund currently holds four concentrated investments.

{kind=link}

Company Financial Information

These four positions represent 96.7% of the investment partnership’s total investments (assuming share counts from 3/31/23 SEC from 13f and share prices as of 6/21/23) and should provide the investment company $14 million in dividends in 2023.

Valuation of the Investment Operations

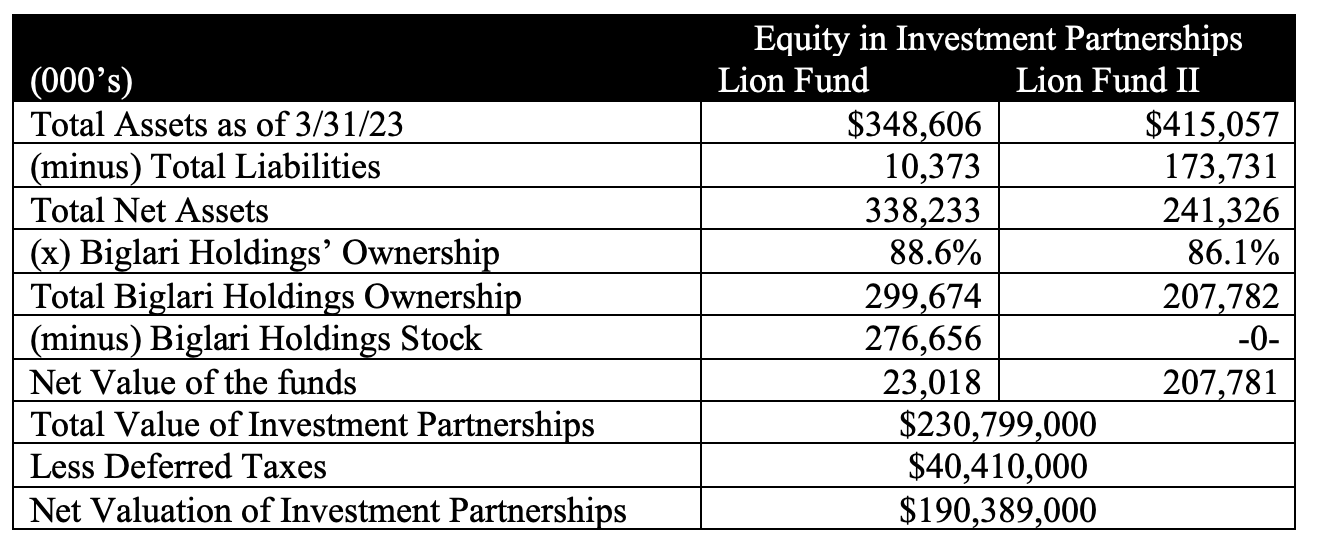

To understand the valuation of Biglari Holdings, Inc. you first must understand the investment partnerships and how their assets feed into the company’s balance sheet. The investment operation holds marketable securities in two funds, Lion Fund and Lion Fund II. Biglari Capital Corp. is the general partner of the investment partnerships and Biglari Capital Corp. is solely owned by Sardar Biglari. The general partner holds an ownership interest in each fund and there are outside investors as well. As of March 31, 2023 Biglari Holdings, Inc. owned 88.6% and 86.1% of the Lion Fund and Lion Fund II, respectively.

To arrive at the value of the Investment Partnerships carried on Biglari Holdings balance sheet, the total assets of the two funds must be reduced by their respective margin debt. The ownership percentage is then applied and in the case of the Lion Fund, the total value of stock held in Biglari Holdings must be subtracted from the total (more on this topic in a moment). Based on this exercise we arrive at a total valuation of the Investment Partnerships of $230,799,000.

Finally, you need to reduce the total value of the partnerships by the deferred tax liability related to the increased value of the marketable securities over their cost basis to arrive at the net valuation of $190,389,000.

{kind=link}

Company Financial Information

Total Valuation of Investment Partnerships- $190.4 Million

Valuation of Biglari Holdings, Inc.

We have now estimated the value of Biglari Holdings’ insurance operations, oil & gas companies, restaurant operations and the investment partnerships. Now we will put it all together for a total valuation of Biglari Holdings and compare it to the company’s current market valuation.

{kind=link}

Author's Estimates

Total Sum of the Parts Valuation of Biglari Holdings $894.4 million

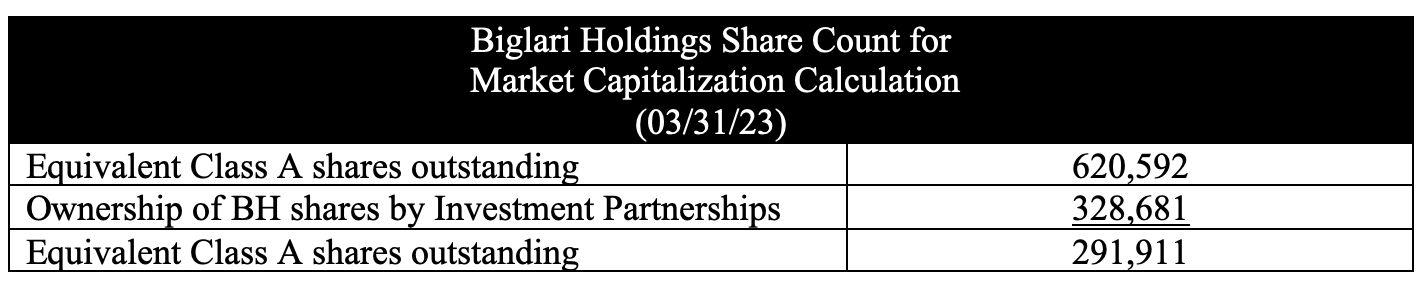

In calculating the current market capitalization for Biglari Holdings it is important to remember the shares it holds in its own company stock. This value is treated much like treasury stock where the amount is subtracted from the investment company assets and basically disappears from the balance sheet. In order to calculate the appropriate number of shares to be used in the market capitalization calculation, the equivalent Class A shares held by the investment partnership must then be deducted from the total outstanding equivalent class A shares. The calculation is detailed below:

{kind=link}

Company Financial Information

Most financial websites report Biglari Holdings’ market capitalization using the total Class A shares of 620,592, or $586.5 million (Class A market price as of 6/21/23 of $945). This is wrong, in our opinion, and significantly overstates the actual market value. You must back out the 328,681 shares Biglari owns in itself. Using the net 291,911 shares outstanding times the current share price yields the correct market capitalization of $275.9 million. Based upon our sum-of-the-parts valuation of $894.4 million, Biglari Holdings currently sells for a 69% discount to our estimate.

Potential Risks to our Analysis

The first complaint you often hear regarding Biglari Holdings is Sardar Biglari’s compensation. As an investor, you must be comfortable with the fact that he will be well paid when the company performs well. Biglari has two incentive agreements, Biglari Holdings and the investment company . Each agreement provides that Biglari will receive an incentive equal to 25% of net profits above a hurdle rate of 6%, over a previous high-water mark (adjusted book value for Biglari Holdings and adjusted investments for Biglari Capital). The agreements eliminate the investment partnership assets, liabilities and income impact from Biglari Holdings to measure each entity separately.

In addition to the two incentive compensation agreements, the company has a service agreement with Biglari entities that provide certain business services to Biglari Holdings, including related personnel, legal, proxy contest, travel, and other related administrative expenses. The fixed payment is $700,000 per month. The Board reviews the costs against the benefits of the service agreement and claims it is an efficient form of contracting. The Board also notes that total general administrative expenses have declined since 2016 and the last two years were more in line with those of fiscal 2007.

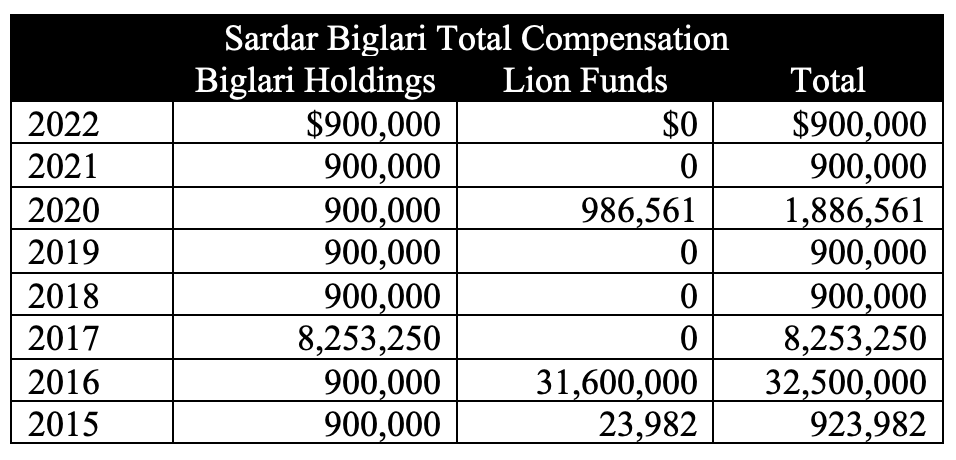

The table below details Sardar Biglari’s total historic personal compensation below.

{kind=link}

SEC 14A Proxy Statement Filings

The large incentive for the Lion Funds in 2016 came from a $281 million investment gain, mainly related to Cracker Barrel. At 12/31/22, the company’s investments in the partnerships totaled $383 million and will need to recover $221.5 million before Biglari is entitled to an incentive. Outside of 2017, Biglari has not received an incentive payment at Biglari Holdings in the last eight years.

Other Risks to Consider

Key Man Risk: Sardar Biglari is solely responsible for making all significant investment and capital allocation decisions at Biglari Holdings. In the event that his services were unavailable for any reason, it could have a significant negative impact on the business.

Controlled Company: Biglari Holdings is a founder-controlled company. While Sardar Biglari has demonstrated a long-term commitment to the company, never selling any Biglari Holdings stock, and having most of his net worth tied up in the company, his interests may diverge from those of the shareholder's.

Reinvestment Risk: Our projections show a substantial increase in cash flow in the upcoming years, which will require reinvestment. It is possible that suitable investment opportunities may be limited, or that future investments might yield lower returns than expected.

Market Liquidity: Investors intending to initiate a position in Biglari Holdings need to use limit orders due to low market liquidity in the stock. It is also advisable to build a position over time.

Final Thoughts

Charlie Munger likes to tell the joke about two economists walking down the street and they see a $20 bill lying on the sidewalk. The first economist says, “Look at that $20 bill.” The second economist says, “That can’t really be a $20 bill lying there, because if it were, someone would have picked it up already.” So, they walk on, leaving the $20 bill undisturbed.

During this year’s annual meeting, Sardar Biglari said that the prospects for the company are better than at any time in its history. He has built the company in his own way on this timeline. No one is paying attention. I think it would be a good idea to pick up the $20 bill.

For further details see:

Biglari Holdings: Sum-Of-The-Parts Valuation Implies Significant Upside