BH - Biglari Holdings: Very Unpredictable And Lacking Any Solid Direction

2023-10-05 01:33:07 ET

Summary

- Biglari Holdings has a low P/E ratio, but its financial metrics and revenues have deteriorated over the years.

- The company has a strong cash position and no debt, but its working capital ratio is at the minimum acceptable level.

- The company's investments in equities have led to a fluctuating bottom line, and its revenues have been affected by the pandemic.

Investment Thesis

I wanted to take a look at Biglari Holdings ( BH ) as its low PE attracted my attention. The company's financial metrics are slightly under my requirements, and the company's revenues show enormous deterioration over the years, with a slight bottom forming in recent quarters. The company's bottom line fluctuates because of the company's investments in equities. I assign a hold rating until I see improvements in revenues and equity investments reverse their downtrend.

Briefly on the company

Biglari Holdings primarily operates in the restaurant business in the US. It owns brands like Steak n Shake and Western Sizzlin. The company also is an underwriter of commercial trucking insurance and operates oil and gas properties off the Gulf of Mexico, however, the largest revenue generator is the restaurant segment which accounted for around 66% of total revenue as of FY22.

Financials

As of Q2 '23, the company had around $31m in cash and $88m in short-term investments, against zero debt. Always a good position to be in. It looks like the management has taken priority in getting rid of all the debt, which lets the company be more flexible in its operations without having the burden of paying annual interest on that debt, which lowers available capital for further expansion of the company.

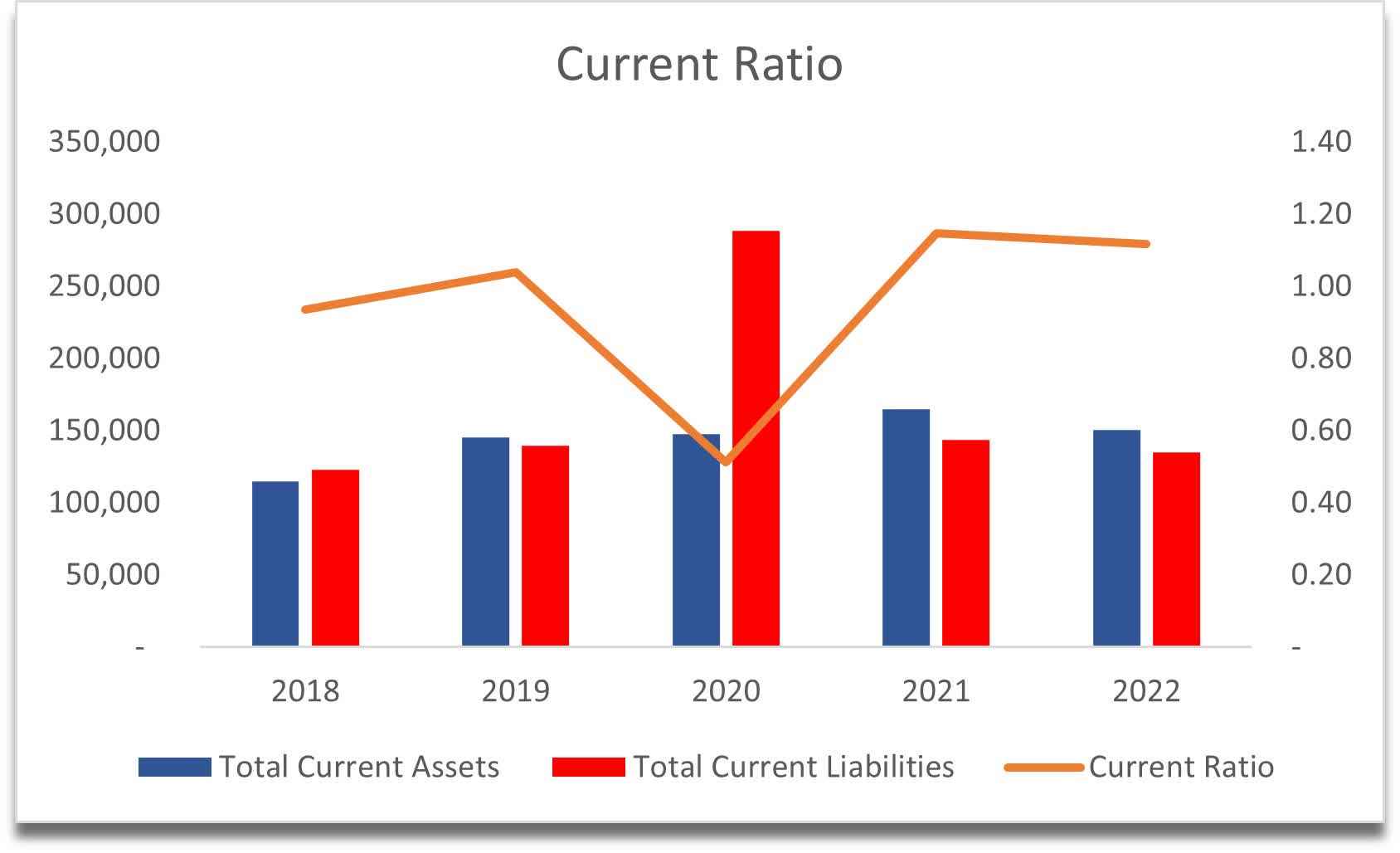

The company’s working capital ratio has been just about at the minimum acceptable ratio of about 1. I would prefer to see a ratio of around 1.5-2.0, which is what I like to call an efficient ratio because it tells me the company has plenty of liquidity to cover short-term obligations and still has capital for growth initiatives. As of the latest quarter, the current ratio improved to around 1.26. It is safe to say the company has no liquidity issues.

{kind=link}

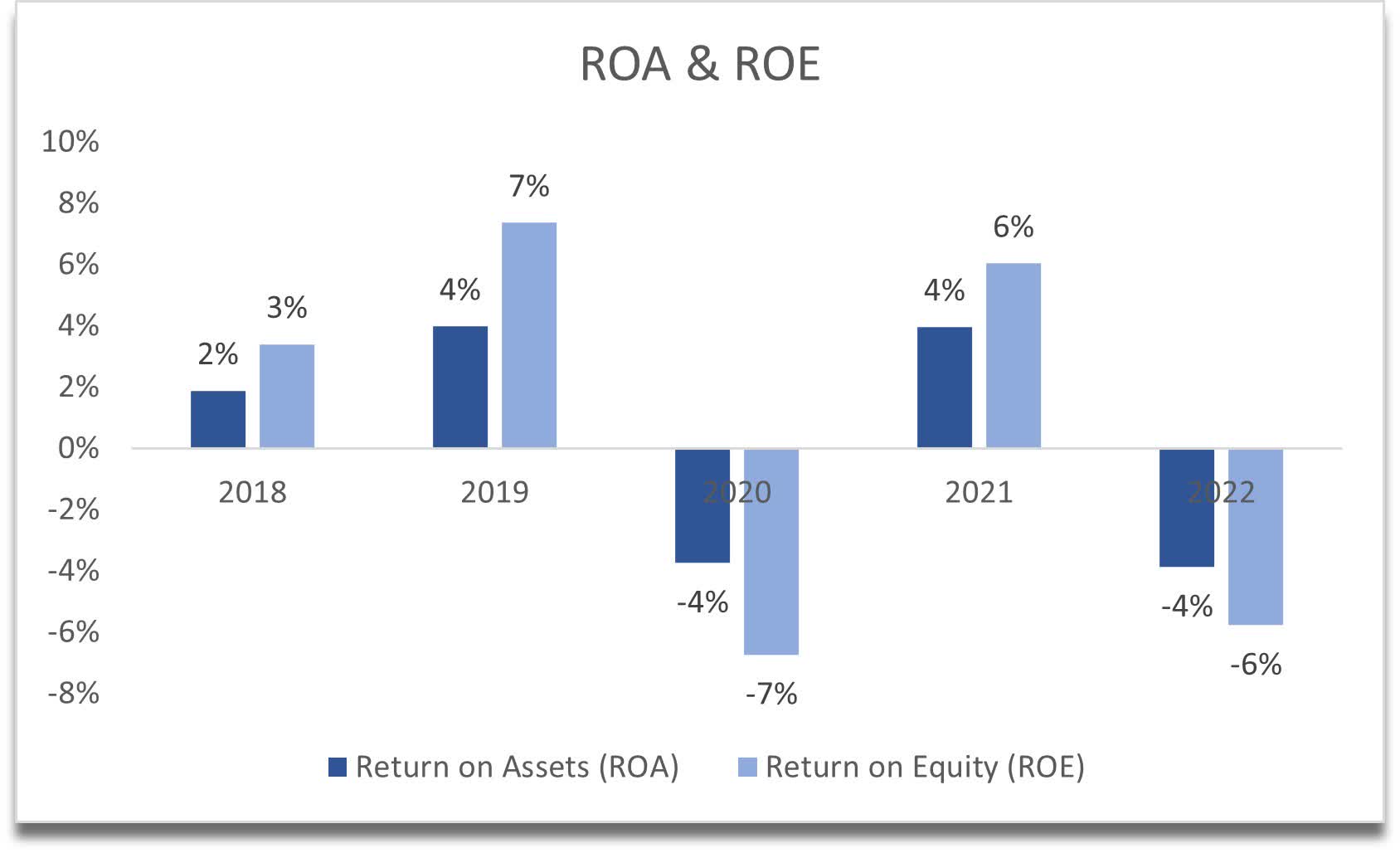

In terms of efficiency and profitability, the company’s ROA and ROE have been subpar for my liking and tend to fluctuate also because of the company’s inconsistent bottom line. I would like to see a consistent return of over 5% for ROA and 10% for ROE.

{kind=link}

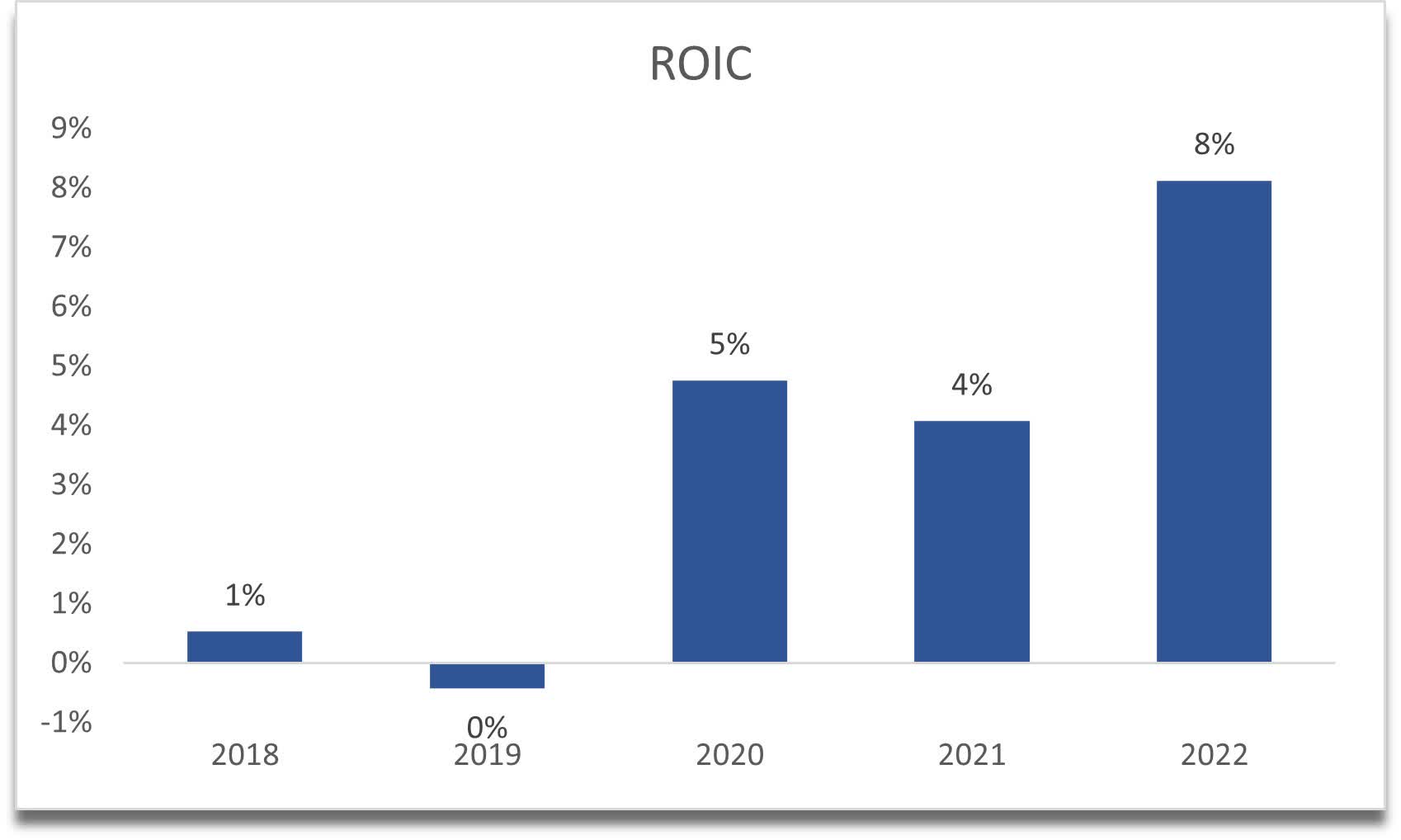

BH had a decent return on invested capital as of FY22, which exhibited quite an improvement from the lows of FY19. I would like to see this go over the 10% mark in future reports, as that is what I would like to see in an investment. To me, 10%+ tells me the company has some competitive advantage as the management can reinvest in profitable projects and build on its moat.

{kind=link}

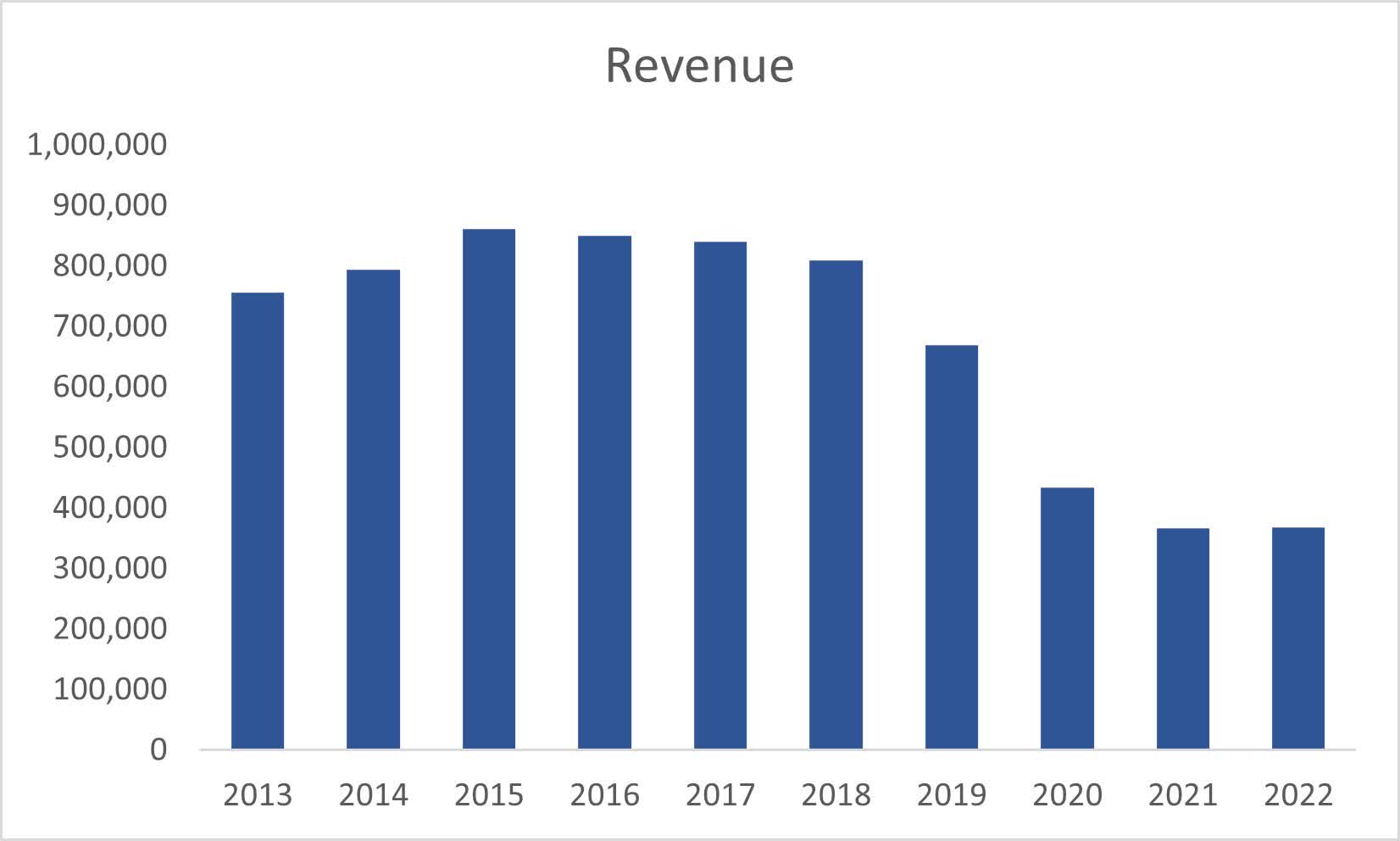

In terms of revenues, the company has been majorly affected by the pandemic, but the revenues were coming down before that too, which is troubling. In FY22, the revenues stayed relatively flat, which may signal the bottom and the company will see a rebound going forward, however, it is hard to tell until I get more information. Looking at the first 6 months of the year, the company saw an increase of around 3% in revenues, which isn’t much, but certainly promising.

The company’s other ventures in insurance and oil and gas seem to be very promising and growing rapidly. Oil and gas revenues grew around 33% CAGR since the company began reporting it, while the insurance premium business grew at around 24% CAGR. These two segments still make up a relatively small amount compared to the restaurant business; however, the growth is phenomenal.

{kind=link}

The company’s margins naturally took a hit because of the pandemic and the company's investments showed a large loss for the year of ’22. So far, the company is showing around $69m in investment gains for the year, which is up from -$111m the year before. It is hard to predict how this income/loss will evolve, but I will have to approach it with conservatism in mind.

{kind=link}

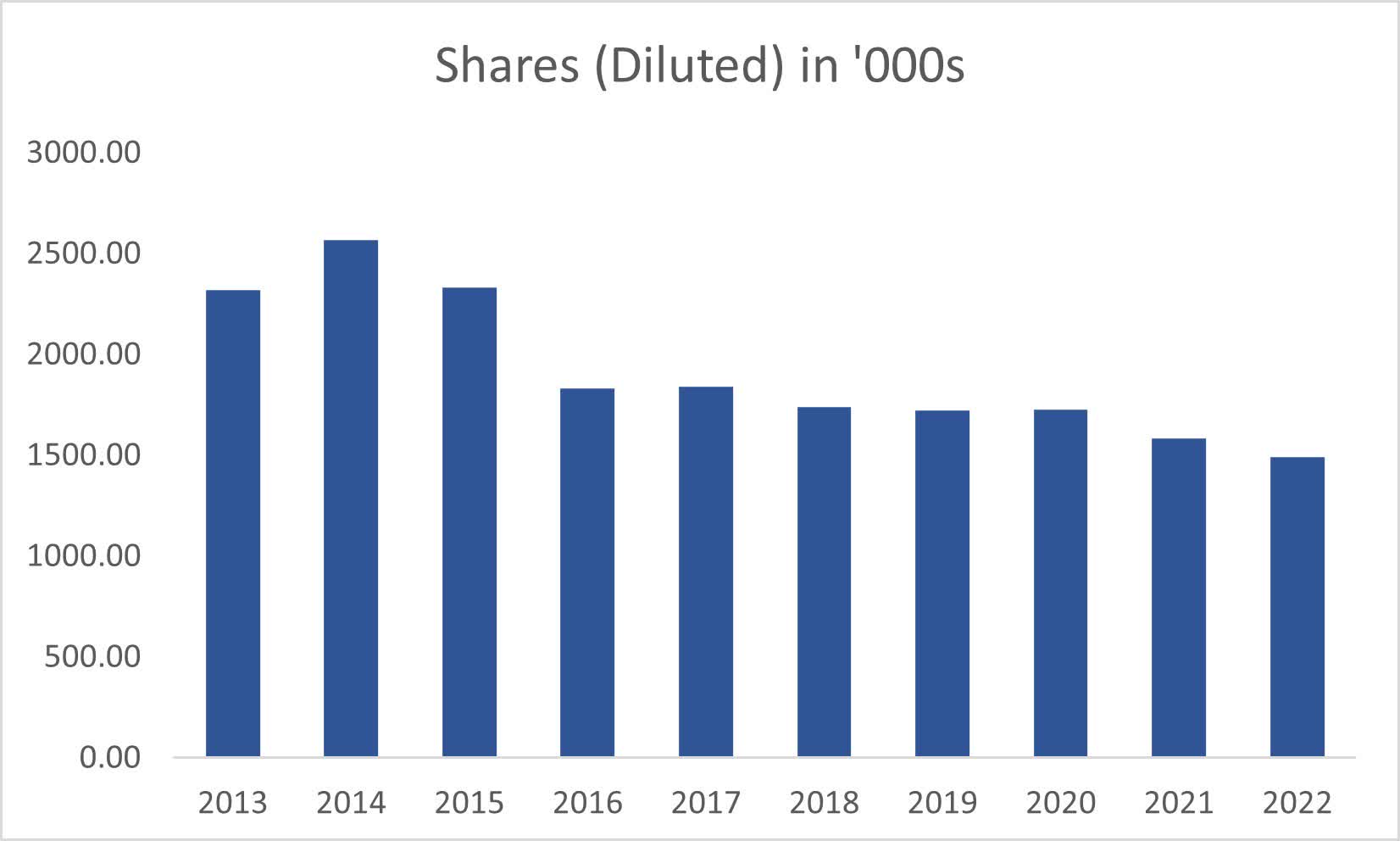

The management has been buying back shares at a reasonable pace over the last decade, which is a good sign if the company’s share price was considered undervalued or at its fair price in the past. If it wasn’t, then I think the capital could have been used in some other ventures that would benefit shareholders in the long run, like strategic growth initiatives.

{kind=link}

Overall, I see a company that is very unpredictable in my opinion. The investments the company has in its portfolio seem to fluctuate quite a bit and that affects the company’s bottom line drastically. Just look at the company’s Q1 report , where it reported EPS of $44 a share of Class B shares which has the ticker BH. The trend in revenues is also still very unclear and I would like to see further earnings to see how these develop in the future.

Investments

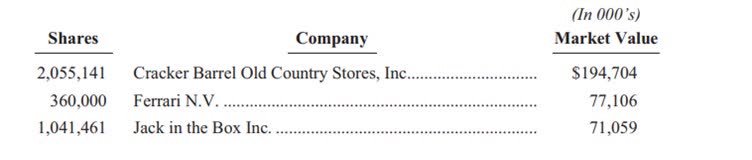

The major investments I found on the company’s annual reports are a large investment in Cracker Barrel ( CBRL ), Jack in the Box ( JACK ), and Ferrari ( RACE ).

{kind=link}

The company controls around 9% of CBRL as of FY22, which is a substantial amount. These investments tend to fluctuate quite a bit over time because of their nature, which is restaurants and luxury sports cars. Restaurants were affected by the pandemic quite a bit and still haven’t recovered fully. For CBRL, the share price is close to the pandemic bottoms and is down 54% over 5 years.

CBRL performance (Seeking Alpha)

{kind=link}

With a forward PE ratio of 12, it seems that the company may be trading cheaply, however, it is very risky.

A very similar situation can be seen in JACK's performance. It's been coming down after reaching $100 a share and it seems to be on a plummet since August of this year, which will affect the company's bottom line the next time it reports financials.

JACK's Performance (Seeking Alpha)

{kind=link}

Ferrari has been performing decently over the last 5 years, which should contribute positively to the company’s performance. I will not go into detail about these companies as that would require an article on each company separately, however, I do think that the restaurant business should see a recovery going forward in the long run. As for Ferrari, it is as " Recession proof as it gets ”. The company performs well in all macroenvironments.

RACE Performance (Seeking Alpha)

{kind=link}

Valuation

For revenue growth on the base case, I went with around 3.5% CAGR. I don’t think that the company is going to continue to lose revenue anymore and will see some growth going forward. For the optimistic case, I went with 5.5% CAGR, while for the conservative case, I went with 1.5% CAGR. This way I will get a range of possible outcomes.

In terms of EPS, I decided to go with around $42 a share for FY23, then for conservatism's sake, I halved it for the next year because it's hard to predict what the investments are going to look like, but I have faith in the company’s operations. After that, the company will see around 7% CAGR of EPS growth per year.

On top of these estimates, I decided to add a 30% margin of safety because of the company's profitability and efficiency metrics, coupled with unpredictable bottom-line growth and the lack of revenue growth so far. With that said, Biglari’s intrinsic value is $162.65 a share, which implies the company is trading at its fair value.

{kind=link}

Closing Comments

The company seems to be trading at a very cheap forward multiple of around 4x according to my calculations. Over the last while, the company’s multiple has been fluctuating wildly, and a 4 PE ratio seems to be sitting close to the top of the range, which means it can come down further in the future.

I assign a hold rating because I have doubts about the company's revenue growth in the future. I will need to see further progress in the coming 2 quarters to see how it has recovered. Furthermore, it is complicated to evaluate the company's long-term investments that affect the bottom line dramatically y/y, however, I could see some investments performing better in the future because these are down still in the last year and are lagging behind the broad markets.

I am very interested to see how the company's other segments besides the restaurant business will fare in the near future. I would like to see the CAGR remain strong, which may require me to reassess in the near future if the revenues become substantial enough.

For further details see:

Biglari Holdings: Very Unpredictable And Lacking Any Solid Direction