BIGZ - BIGZ: A Growth Fund That Also Provides Monthly Distributions

2023-05-08 05:53:47 ET

Summary

- BIGZ hasn't provided anything to be too excited about since its launch, as growth took a plunge shortly after it entered the market.

- The fund's discount remains attractive if one is looking for a growth-oriented fund with a monthly distribution.

- With limited capital gains, further distribution cuts could be in the future, but as a CEF, it is likely always to distribute something to investors.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 6th, 2023.

To say BlackRock Innovation and Growth Term Trust ( BIGZ ) has had a rough history so far would be an understatement. This was one of my 'BIG' mistakes as I bought into this fund early. With a launch in early 2021, there was much momentum in the area this fund was looking to invest in. The fund was designed to invest in private and smaller growth companies, the exact sort of investments that were taking off after the Covid pandemic.

However, as we know now, the fund launched right in time as the bubble was popping. After the fund held steady for a bit after launch, the fund then dropped precipitously, along with all the other growth names in 2022.

The drop was swift, and while the fund utilizes a covered call strategy as well, that did little to soften the blow. At the same time, BIGZ could perform better as the Fed is expected to be nearer to the end of higher interest rates. While the mega-cap tech names have received lots of love this year, it might still be surprising to see that BIGZ hasn't participated in the upside.

Of course, as I've said previously, this type of fund still carries a lot of risks. This is more of a speculative play. Perhaps this year's performance helps highlight this. Even when the broader tech space was booming, it hasn't helped BIGZ to a material level.

The Basics

- 1-Year Z-score: 0.93

- Discount: 14.75%

- Distribution Yield: 11.08%

- Expense Ratio: 1.36%

- Leverage: N/A

- Managed Assets: $1.985 billion

- Structure: Term (anticipated liquidation date of March 26th, 2033)

The objective of BIGZ is to "provide total return and income through a combination of current income, current gains and long-term capital appreciation."

The fund attempts to achieve this objective by focusing on "mid- and small-capitalization growth companies that are "innovative." These are companies that have introduced or are seeking to introduce, a new product or service that potentially changes the marketplace. The Trust utilizes an options writing (selling) strategy in an effort to generate current gains from options premiums and to enhance the Trust's risk-adjusted returns."

Since our last update , the fund had a minor name change . The name was formerly BlackRock Innovation and Growth Trust. The added "term" helps identify that this fund is a term-structured fund. It's important to note that there were no other investment policy changes; this was a name change only. The majority of funds launching from around 2018 and later are all these CEF 2.0 launches. However, this should help clarify this, as BlackRock changed their other term fund names to include this identifier as well.

At this point, the fund has quite a while before we have to worry about the term structure, as it is anticipated to liquidate in early 2033. The main advantage of the term structure is that a fund shouldn't trade perpetually at a discount as older CEFs can for years and decades. This is because with a term structure, upon the contingent liquidation, the investor will receive the NAV per share at that time, whatever it shall be at that time.

Performance - Discount Continues To Look Attractive

Since our last update, which has been quite some time as it was in April 2022, the fund's results help show how much the last year was tough for the fund.

BIGZ Performance Since Prior Update (Seeking Alpha)

Helping to minimize some of the losses on a total return basis was the fund's distribution.

A look at 2022 specifically showed the fund had a total share price loss of -47.74% and a total NAV loss of -41.11%. That would have pushed the fund's discount wider through the year, but heading into the year, it was already looking at a wider discount too. As growth had some of a recovery so far on a YTD basis, the fund's discount has actually narrowed from the depths it was at previously.

Ycharts

At the same time, the fund's discount still appears quite attractive if one wants exposure to growth plays overall. As a newer fund, there isn't too much of a guide in terms of historical discount level. The fund launched and enjoyed a premium for some time before being dropped significantly to a deep discount as the investments plunged.

However, it should also be noted that if you are exceedingly bullish on growth going forward, BIGZ might not be a great bet because of the covered call strategy.

Currently, the fund's overwritten portion is 11.77%; that isn't overly aggressive and being an actively managed fund, they have a lot of discretion in how overwritten they want to be. That being said, should growth continue to skyrocket in their underlying portfolio, the covered call strategy could limit the fund's upside.

Which, it should be pointed out that the last time we covered BIGZ, they were similarly at a low 10.34% overwritten portion of their portfolio. This indicates that the fund managers were either more bullish this whole time or aren't really being too active in the options strategy. In their material, they note that they intend to write options at "30% to 40% of its net assets."

So this is worth noting that they haven't generally been near this target, which was to the fund's detriment in the previous year, where the fund could have collected more option premiums.

The fund's NAV started off with a bang but has since slipped. In fact, the fund is now only managed some slight total NAV return gains on a YTD basis.

Ycharts

This was similar to the trajectory of ARK Innovation ETF ( ARKK ). Below we can see that the Technology Select Sector SPDR ETF ( XLK ) provides the best YTD returns of this trio. XLK's top two holdings are Microsoft ( MSFT ) and Apple ( AAPL ), which make up nearly 50% of the ETF. That reflects the significant pull that the mega-cap tech names have been doing most of the heavy lifting, with a significant amount of 2023's performance being driven by a narrow few names.

Ycharts

Distribution - Cautious On Current Distribution Yield

The fund launched with a monthly distribution of $0.10. They cut in 2022 to $0.07 per month. While this is an attractive 11.35% distribution yield, on a NAV basis, this works out to 9.68%. However, as with most equity funds, the fund will rely significantly on capital gains to fund the distribution. In fact, this fund doesn't produce any net investment income due to its focus on growth companies. This is unlikely to change at any point as long as the fund remains focused on its current investment policy.

{kind=link}

So in a market with significant losses, it isn't surprising to see a distribution cut. There have been positive returns heading into this year, but as we saw above, it was limited. Therefore, further cuts could be expected.

On a brighter note - if there is one - the options written on the portfolio were able to generate some realized gains in the prior year. It was fairly minimal due to being minimally overwritten, but had it not been for these, the losses would have been even deeper.

BIGZ Realized/Unrealized Gains/Losses (BlackRock (highlights from author))

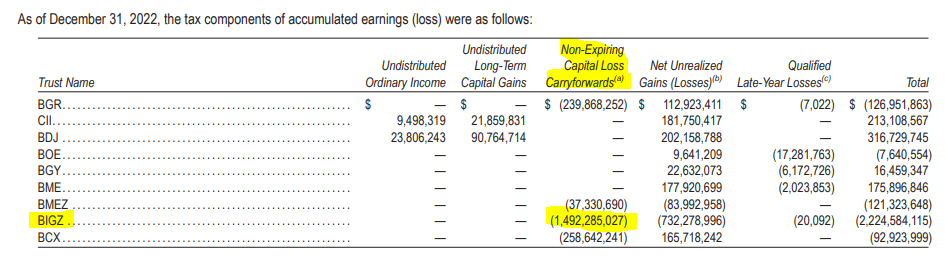

On another bright note, if an investor is looking to invest, there is a good chance that a lot of the distributions going forward will be classified as return of capital. For 2022, 100% of the distribution was classified as ROC. ROC can help defer an investor's tax obligations as it reduces the cost basis rather than being taxed in the year received.

This can happen because the fund has massive capital loss carryforwards due to the losses realized previously. That can be beneficial even if the fund starts rising and starts to technically cover its distribution going forward, as these losses can offset those potential gains going forward.

BIGZ Capital Loss Carryforwards (BlackRock (highlights from author))

{kind=link}

BIGZ's Portfolio

The portfolio's turnover rate for 2022 came to 41%. During the 2021 partial year due to the launch, they had a 55% turnover. That makes this fund fairly active, and we have seen a bit of a shift in the last year when looking at the breakdown.

In total, they carry 89 holdings; within this, they noted that 29 were private investments. That is up only a bit from the 79 holdings listed previously - they noted 25 private holdings then. I believe this is noteworthy because its sister fund BlackRock Science and Technology Term Trust ( BSTZ ), didn't invest in any new private investments in the entirety of 2022. BSTZ is focused on a tech tilt, whereas BIGZ is a similar fund but is open to a broader portfolio of sectors. They aren't limited to tech, even though the fund's heaviest weightings are to tech.

BIGZ Sector Breakdown (BlackRock)

When discussing private investments, it's important to note that these are generally going to be level 3 securities. For BIGZ, they listed that nearly 28% of their portfolio at the end of 2022 was categorized as level 3. With level 3 securities, there is always going to be some uncertainty in terms of the valuation. That can lead to some discount on funds on its own with any fund that carries level 3 assets.

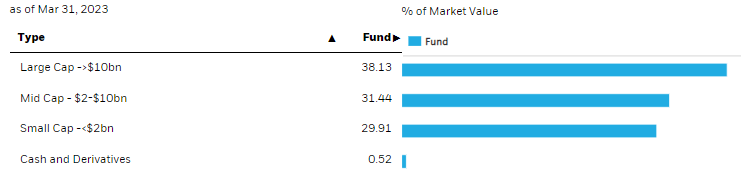

In terms of market cap allocations, we've seen a meaningful increase in the large-cap allocation. This reduced both the mid and small-cap weightings, which were 43.89% and 35.50%, respectively.

{kind=link}

Another way to look at it was that the fund reported that the average market cap in February was $8,366.1 million. At the end of March 31st, 2023, the average market cap of the underlying portfolio was $11,605.8 million.

One thing we saw from its sister funds is when this happened through 2020 and early 2021; it had generally been due to massive increases in valuation.

In this case, it would seem to be a more deliberate shift to larger weightings to de-risk the portfolio potentially. Generally, larger-cap names have better financial stability and therefore offer reduced risks. However, it is only relatively de-risked; this remains a risky fund that should experience quite a bit of volatility.

{kind=link}

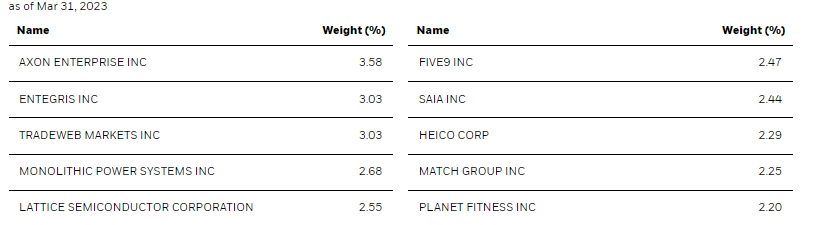

The top ten holdings are all currently publicly traded companies. On a YTD basis, we really can see a wide divergence between the performance of these names. Generally, the top ten have been producing some positive results, which reflects the slightly positive performance the fund has experienced this year. However, we also have a couple of names that continue to struggle, muting the fund's upside. Axon Enterprise ( AXON ) has been a regular in the top ten, which has provided some strong returns this year.

Ycharts

Of course, this is only the top ten, which make up only around 26.5% of the fund. That leaves another three-quarter of the fund's exposure outside of these ten.

Saia ( SAIA ) is a particularly interesting name. It certainly isn't a startup, as it was founded in 1924. This is an industrial play in the cargo ground transportation industry. It wouldn't seem to be a growth play, but the stock's YTD performance would indicate an expectation for serious growth with a ~40% return. In the last year, the name is up around 34%. At the same time, the company is expected to decline in earnings this year before climbing in the following years.

{kind=link}

I think SAIA is a good example of showing how flexible they can get with their investment policy. The management appeared to have made a good decision because it was such a strong performer relative to the other names in the fund. This was a name in the fund previously, too, but the allocation was pushed higher through these strong results. The position also had a bit of a nudge with a higher share count. At the end of 2021, they listed 180,724 shares held, and this was bumped up to 188,175 by the end of 2022.

Conclusion

BIGZ launched at a time when growth was getting into an extended bubble. When it launched, the fund raised over $4.5 billion, which is massive for a CEF. That helps highlight how enthusiastic the overall market was in participating in this area of the market. Unfortunately, it was launching right about as the bubble was going to be popped as the Fed went into a rapid rate hiking cycle. Going forward, the fund remains quite risky, but I believe there still continues to be potential here. The fund's discount is certainly still appealing, even as that has narrowed a bit heading into this year.

For further details see:

BIGZ: A Growth Fund That Also Provides Monthly Distributions