PFIX - Bill Ackman Covers Short Treasury Bet For Massive Profit: What's Next For Bonds?

2023-10-25 11:05:04 ET

Summary

- Hedge fund manager Bill Ackman made a successful short bet against the US Treasuries market, likely earning over $1 billion in profit.

- Ackman decided to close his bet, indicating that he believes the economy is slowing faster than recent economic data is showing.

- Why he opened the bet, additional reasons why I think he closed it, and what it means for the outlook for interest rates going forward.

- Did Ackman leave money on the table? From an expected-value perspective probably, but what's a billion dollars among friends?

Come bonus time, I'm gonna show you enough love, you could start a third family.

-Bobby Axelrod, Billions .

Famed hedge fund manager Bill Ackman appears to have hit a home run with his short of long-term Treasuries ( TLT ) this summer. He timed the meltdown in Treasuries beautifully and recently posted on Twitter that he'd covered his position, citing growing concerns about the U.S. economy. This isn't the first time Ackman has pulled off a coup like this, most famously declaring in a CNBC interview that " hell is coming " in March 2020 and profiting $2.6 billion on a short bet that he closed shortly after. We don't know exactly what Ackman's Pershing Square Capital made on this short Treasury trade, but we can make an educated guess from other recent bets that it's north of $1 billion and possibly much more. Life imitates art, and Bobby Axelrod (the main character in Showtime's Billions ) would certainly be jealous of Ackman's haul here. To these points, let's break down Ackman's TLT trade, the reasoning behind it, whether he might be leaving some money on the table, and the outlook for TLT.

Why Ackman Went Short This Summer

The first thing to note is that as an activist investor, you generally have the right to say whatever you think about a stock. If you're super famous and the public piles their money in to agree with you, you auto-profit from this in the short run, whether you're right or wrong in the long run. This is doubly true if you're going with the existing momentum (i.e., saying Dogecoin to the moon). However, the US Treasury market is simply enormous. This makes it difficult to get enough money in to affect the price, no matter how famous you are. However, Ackman's trade coincided with a sort of perfect storm in the Treasury market, and he correctly predicted factors that caused Treasuries to sell off shortly after.

On August 3, Ackman announced on Twitter that he placed a massive short bet against the US Treasuries market.

His back-of-the-envelope math:

So if long-term inflation is 3% instead of 2% and history holds, then we could see the 30-year T yield = 3% + 0.5% (the real rate) + 2% (term premium) or 5.5%, and it can happen soon. There are many times in history when the bond market reprices the long end of the curve in a matter of weeks, and this seems like one of those times.

I would quibble with his long-term fundamental methodology here, but the price target of 5.5% for the 30-year Treasury is fairly reasonable if Congress refuses to slow down spending. More important than the fundamental methodology were the technicals here- lots of forced sellers (mainly the US Treasury), and no natural buyers. The bet worked, Treasuries sold off about 85 basis points, and Ackman now has covered his short for a huge profit.

This was a brilliant trade for many obscure technical reasons :

- The Bank of Japan was forced to relax its yield curve control, cutting a key source of demand for US Treasuries. Japanese investors historically buy a lot of US Treasuries and when government bonds in Japan had negative yields in the 2010s and early 2020s even more so.

- US budget deficits came in worse than expected.

- Data on growth and inflation came in higher than expected. This blocks the Fed from easing to accommodate the economy (not that they necessarily can anyway).

- Fitch downgraded the United States' credit rating, leading to a ton of media coverage. Ackman timed it well here.

- Finally, the momentum was firmly against Treasuries and had been so for the better part of two years. Sellers are more likely to panic in such a situation.

For these reasons, Ackman's Treasury short was nearly a wire-to-wire success.

Why I Think Ackman Decided To Close His Short Bet

If you're a hedge fund manager who made a trade and you're staring at a billion-dollar profit, I wouldn't blame you for taking the money and running. While your expected value is generally higher from holding, you've already won. For this reason, you should read far more into what fund managers buy than what they sell. A lot of times they'll just be up a boatload of money and selling locks in their profits.

There's a fun 2000s romantic comedy called A Good Year where Russell Crowe plays a London bond trader who inherits a vineyard from his uncle in the South of France. As you would, he ends up leaving his job in London and falling in love with a French girl. His final trade in London is legal but ethically questionable and draws a regulatory inquiry for market manipulation. In what's likely the most realistic scene in the movie, Max takes a severance package with "a lot of zeros" as a result.

Every contemporary finance movie seems to at least touch on the concept of "f*** you money," or the idea that more money isn't that useful when you're already rich, but it's nice to be able to walk away and be comfortably wealthy forever. The dry economics term for this is the utility theory of money.

How might we use this to profitably trade? Former risk manager Aaron Brown points out that he knew no one on Wall Street like Bobby Axelrod, but far more like The Bonfire of The Vanities' Sherman McCoy, with big mortgages on New York City co-ops and kids in private school they have to pay for. Wall Street is famous for small salaries and big bonuses (often with lockups), so many fund managers need to finish the year up or they may end up being cash-poor.

Where am I going with this? Last year was a down year for the market, so many managers won't have been paid any performance fees since 2021. This year, the S&P 500 ( SPY ) is still up 11%, although it's been melting away. If the market gets closer to zero, we could see a cascade of selling as everyone tries to lock in gains for the year so they can get their annual bonuses for the year. If the market were down 5% or something we'd likely see many of these same managers aggressively chasing winning stocks in an attempt to squeak out a profit for the year and earn a bonus. I've published research on how September and October are the most volatile months of the year for stocks, and this might be one more reason why.

Even the Bobby Axelrods and Bill Ackmans of the world are less likely to hold to squeeze the last few percent of value after a position has moved substantially in their favor. Managers just see the zeros and close out to cash in. Also, Ackman may have decided to cover the trade to clear his plate for personal matters.

He did give some economic reasoning on Twitter that I felt was interesting, he said that the economy is slowing faster than recent data suggests. Hedge fund managers are able to pay for high-frequency data on credit card spending, satellite data of store parking lots, and such, giving them an advantage in seeing where the economy is going before official government data says so. He could easily have data that the public doesn't have on spending that suggests the economy is rapidly slowing. We do know that the second month of student loan payments in the US is due the day after Halloween- I think it would be naive to think that this wouldn't cause people to rein in spending.

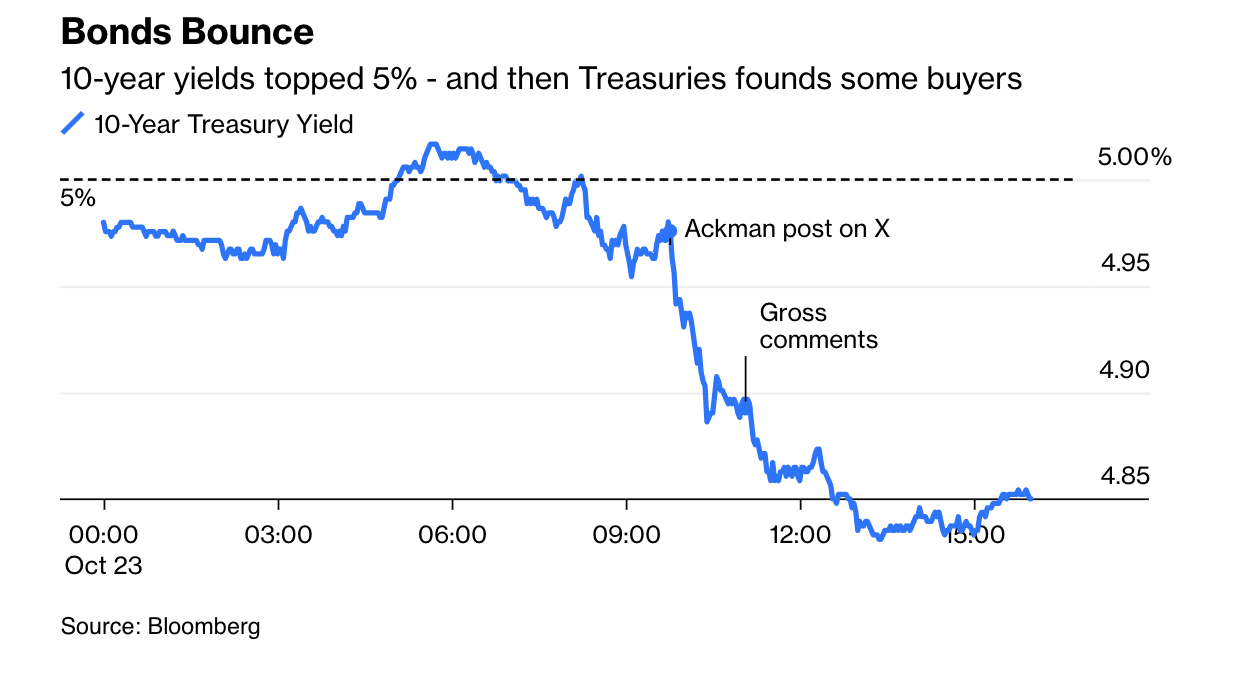

Here's the action in Treasuries before and after Ackman tweeted that he'd covered his position- he seems to have caused a fairly impressive move, which was compounded by former bond king Bill Gross' recession comments shortly after.

{kind=link}

Do hedge fund managers behave in ways that cause them to chase performance fees when they're down for the year and lock in gains when they're up? You bet! But then you realize that the average retail investor now has 40% of their money in just three stocks- Apple ( AAPL ), Tesla ( TSLA ), and Nvidia ( NVDA ). Pro investors locking in gains to get paid doesn't seem so bad in this context.

Did Ackman Cover Too Early? And Is TLT A Buy?

I think Ackman left money on the table here, and some other market observers agree .

Ackman originally had a yield target of 5.5% for the 30-year Treasury. He closed out a little above 5%. I think Treasury yields still go higher here for all of the reasons they've been going up all along, but it's too thin to consider shorting TLT. I think you can start buying TLT around $80, with the idea that there likely isn't a line in the sand, you just buy for value in the long run and accept that it's likely to move against you in the short run. Still, the advantage of TLT is that it's easy to trade, there are many better bond funds out there. Using similar math to Ackman and historical data, we can assume an inflation rate of roughly 2.5% over the next 30 years and a real yield of 2-3.5%, giving a fair value range of somewhere between 4.5% and 6% for the 30-year Treasury. This is in line with long-term averages and I wouldn't be buying for value below 5%.

One reason to consider here is that 10-year inflation breakevens rose from roughly 2.25% in early September to ~2.5% last week. This could be due to the UAW strike, or the Middle East, or from the Fed. The Fed has indicated that they're not hiking rates at next week's FOMC meeting, and the market thinks they're likely done. The Fed may yet again have a problem by trying to be too dovish. JPMorgan CEO Jamie Dimon said he doesn't think it matters if the Fed hikes 25 bps more or not. But the problem with pausing rate hikes is that if it causes inflation expectations to go up, then long-term yields end up going up anyway. The Fed likely won't be able to achieve price stability and reasonable interest rates at the same time. If they prioritize price stability, they'll need to accept mortgages being 8-9%. If they prioritize keeping rates below the free market rate, then they're likely going to get stuck with double-digit inflation.

TLT is kind of a roulette wheel because of the massive amount of duration and volatility it has, I don't see much of a reason to lock in a yield under 5% for 30 years when you could get nearly the same yield for 7-10 years with less than half the risk. The correlation between TLT and SPY so far this year is 0.84 , so TLT is not functioning as a hedge. If you're buying TLT you're only buying for value, and I think you can find better value in shorter term bonds. Historically, TLT should usually not be a better risk-adjusted return than shorter-term bonds because so many institutions are required to buy long-dated government bonds by law. There's a fund that aims to take advantage of this, it's the Simplify Intermediate Term Treasury Futures Strategy ETF ( TYA ), it also generally has better tax treatment than buying Treasuries outright. If you still want to bet against Treasuries they have a short Treasury fund, Simplify Interest Rate Hedge ETF ( PFIX ) that buys long-term options on Treasuries. Betting against Treasuries isn't as attractive now that yields have skyrocketed for nearly two years straight though.

Bottom Line

Hedge fund manager Bill Ackman covered his TLT short, likely making $1,000,000,000 or more in the process. There are still plenty of reasons for yields to go higher, so I'd hold off on buying TLT until it hits about $80. If you're itching to buy bonds now, consider buying shorter-term bond funds that carry roughly the same reward for less risk. Any Vanguard fund will work about as well as the others so long as it has a duration and risk profile that works for you. I wouldn't buy TLT unless you like taking a lot of risk and want to win big if yields decline.

For further details see:

Bill Ackman Covers Short Treasury Bet For Massive Profit: What's Next For Bonds?