LAMR - Billboard REITs: We're Paying Attention (Lamar Vs. Outfront)

Summary

- From the bright lights of Times Square to the iconic signage on LA's Sunset Strip, advertising billboards have been an inescapable fixture of the typical American commute for decades.

- Billboard REITs own a commanding share of the nation's 500,000 outdoor advertising displays - a surprisingly resilient business that has seen revenues and profitability fully recover to pre-pandemic levels.

- Unlike other increasingly-cluttered digital formats, there's "only one channel" on the highway. These Billboard REITs are well-positioned to capture the steadily growing share of marketing spending towards Out-of-Home ("OOH") advertising.

- We like the clear supply constraints and the importance of scale in the billboard business – granting these billboard REITs a meaningful competitive advantage and economic moat - as the majority of existing billboards are grandfathered-in as "legal non-conforming" uses.

- The gradual conversion of static displays to digital displays – which are getting both cheaper to make and improving in display quality – remains a compelling catalyst to drive mid-single-digit same-store revenue growth and margin expansion through the decade.

REIT Rankings: Billboards

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on February 14th.

{kind=link}

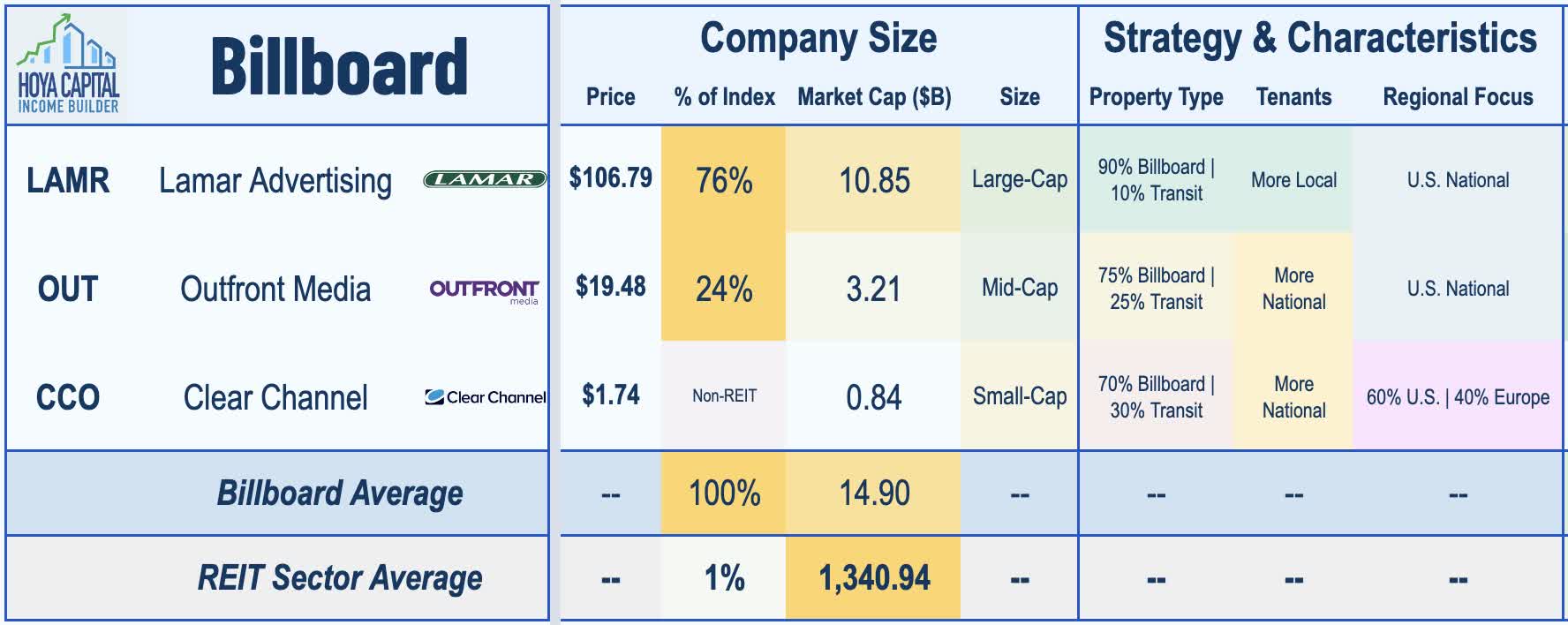

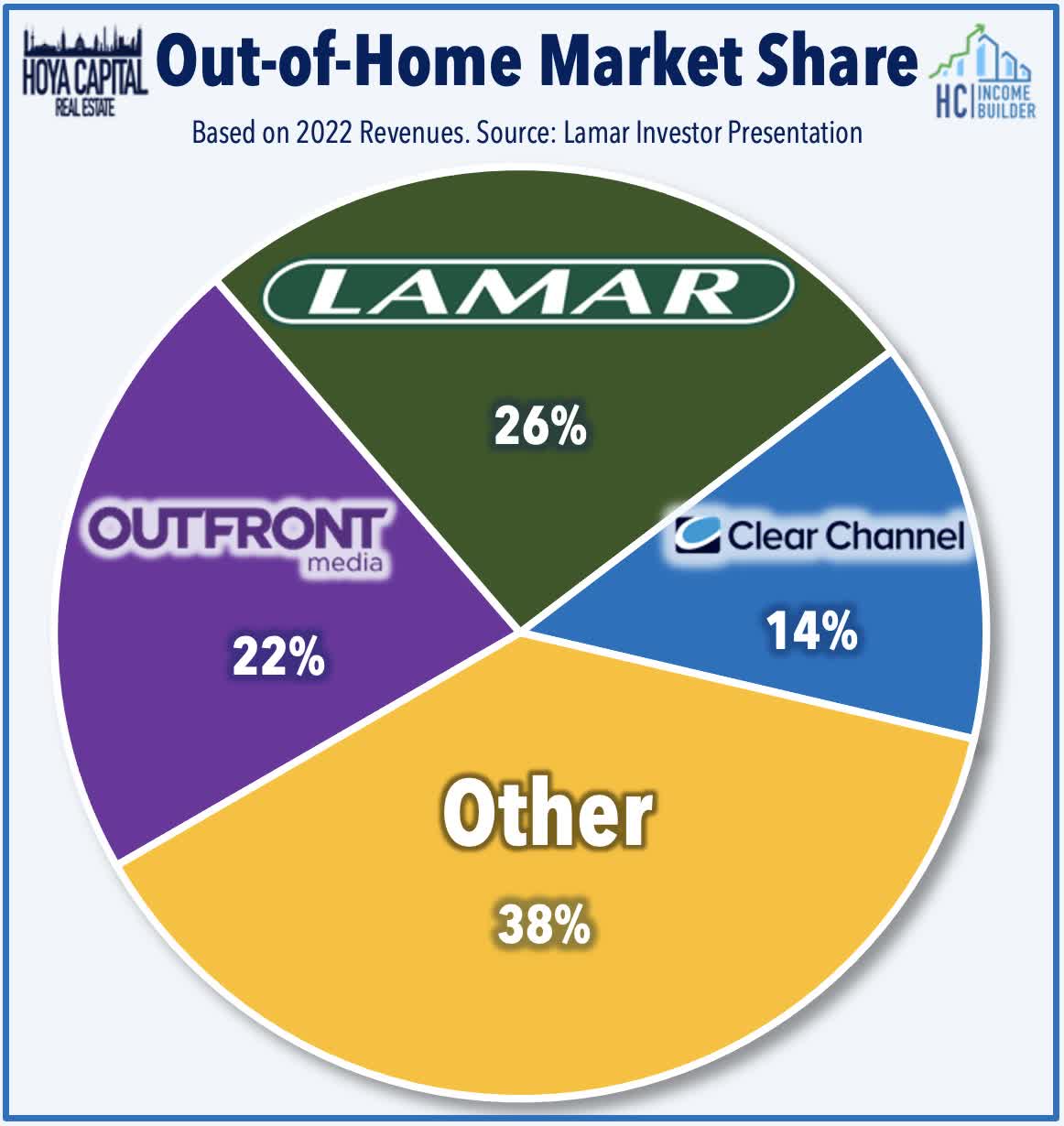

From the bright lights of Times Square to the iconic signage on LA's Sunset Strip, advertising billboards have become a symbol of American consumerism and an inescapable fixture of the typical American commute. In the Hoya Capital Billboard REIT Index , we track the two billboard REITs, which together own nearly half of U.S. billboards and account for roughly $15 billion in market value: Lamar Advertising ( LAMR ) and Outfront Media ( OUT ). We also track non-REIT Clear Channel Outdoor ( CCO ), which is the third-largest billboard operator. Still very much a niche sector, Billboard REITs comprise roughly 1% of the broad-based commercial Real Estate ETF ( VNQ ).

{kind=link}

Billboard REITs - an often overlooked niche segment of the real estate industry - own a dominant share of the advertising signage across the United States, controlling more than half of the nation's 500,000 outdoor ad displays - a surprisingly resilient business that has seen revenues and profitability fully recover to pre-pandemic levels by mid-2022 after an abrupt decline early in the pandemic. One of the newer REIT sectors, Outfront was the first billboard REIT, emerging in 2014 from a spin-off from CBS Outdoor, and converting to a REIT soon thereafter. Lamar went public in 1996 and operated as a traditional c-corp before it announced a conversion to a REIT later in 2014. Clear Channel remains a non-REIT corporation but has explored a REIT conversion at various points in the last half-decade and notably, began providing REIT-specific metrics (including AFFO) in its most recent quarterly report.

{kind=link}

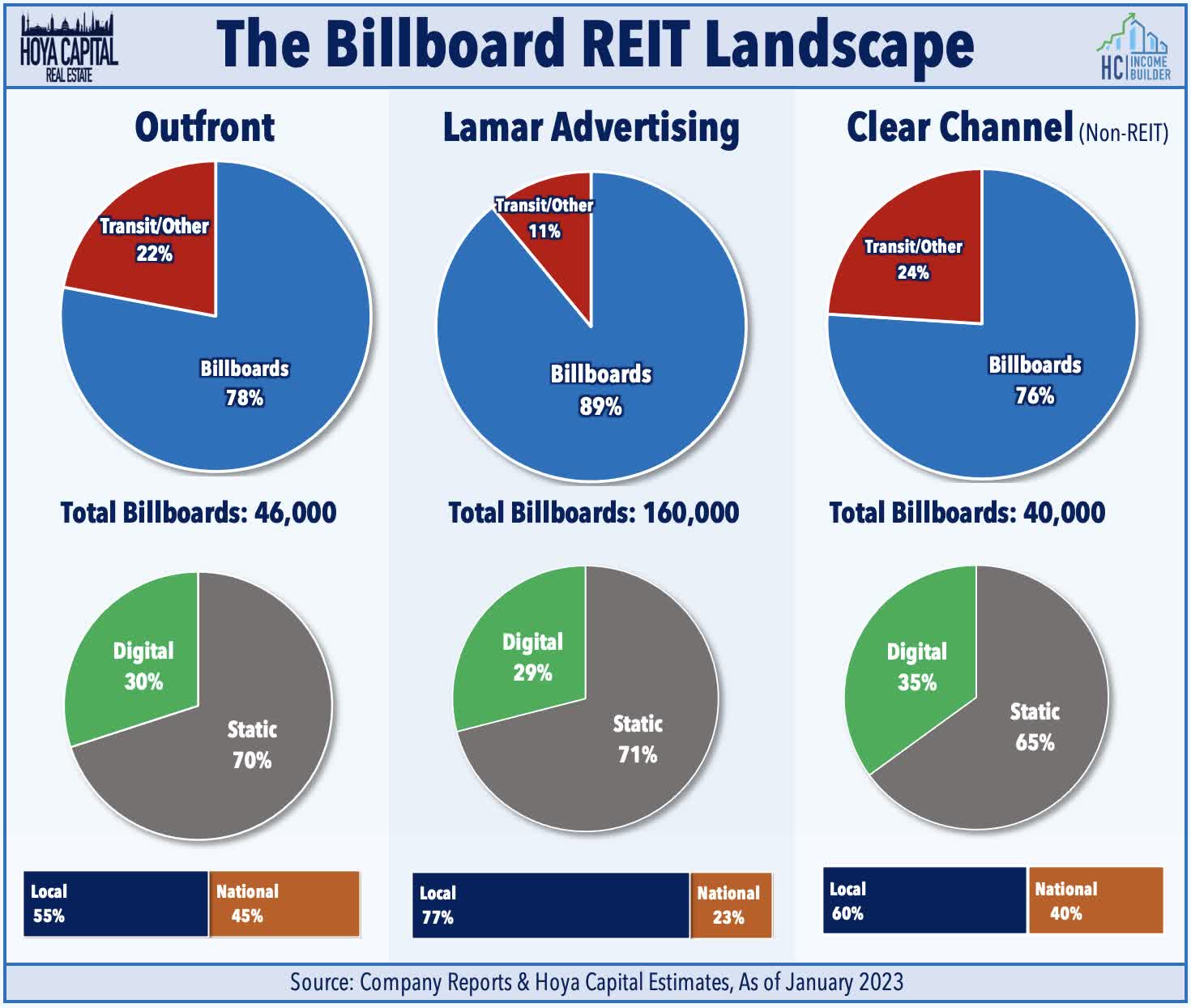

These Billboard REITs derive around 75% of their revenues from traditional large-format billboards with the balance through transit advertising and other advertising signage. Lamar operates as the most "pure-play" billboard company of the three - deriving over 90% of its revenues from signage along U.S. highways and interstates - while Outfront has a large transit-oriented business, underscored by the company's massive transit deal with the New York Metropolitan Transportation Authority. While the two REITs operate almost exclusively in the United States, Clear Channel has a significant international presence with roughly 40% of its revenues coming from European and Asian markets. Local businesses account for roughly two-thirds of billboard ad spending - and upwards of 80% on traditional large-format highway billboards - while national brands account for 30% of industry revenues - but comprise the majority of spending on digital displays and transit advertising.

{kind=link}

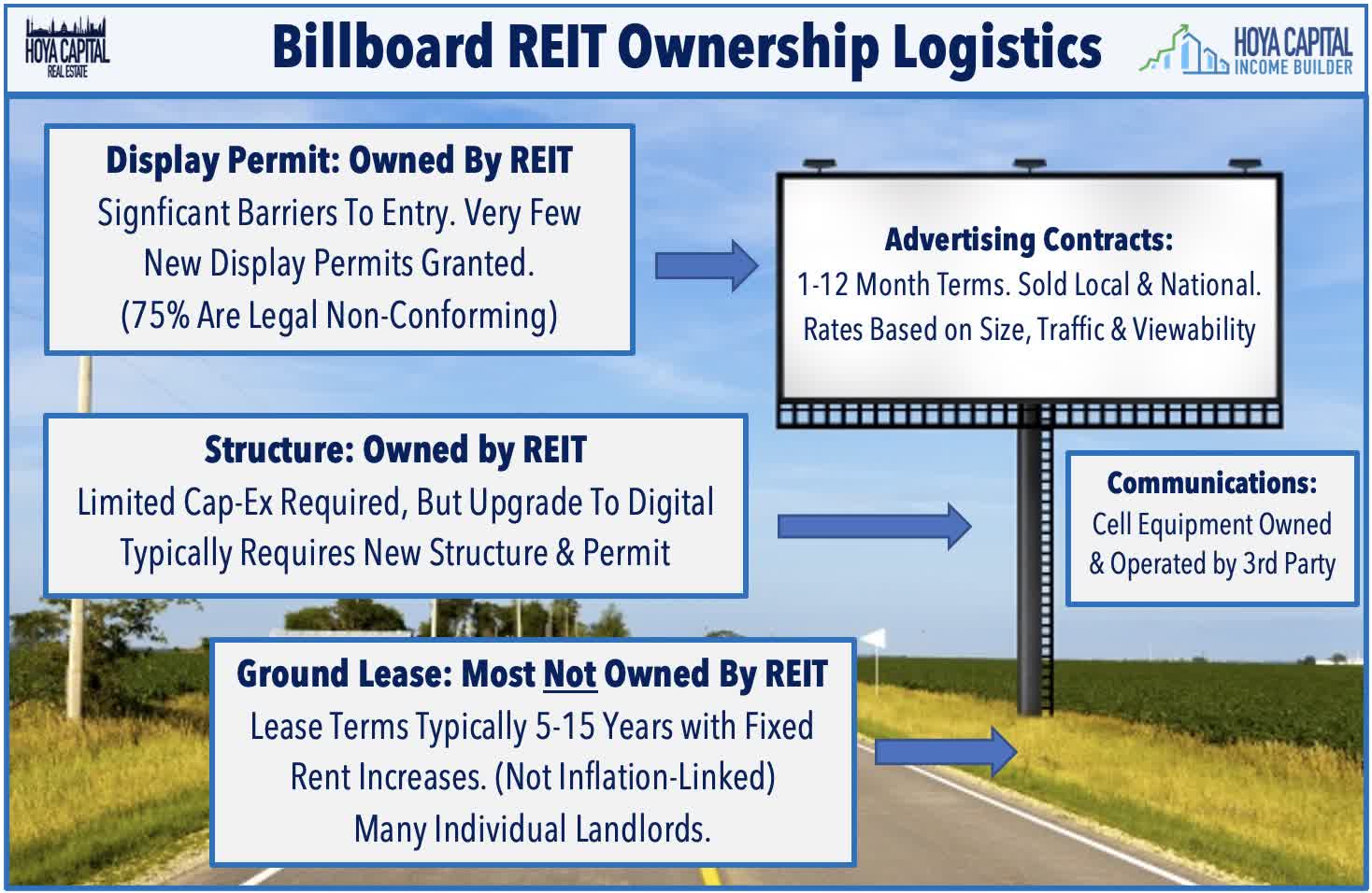

Barriers to entry are significant as signage remains one of the most highly regulated industries dating back to a 1965 law that limited new billboards along federal highways. We like the clear supply constraints of OOH real estate as the majority of existing billboards are grandfathered-in as "legal non-conforming" uses, and we see the gradual conversion to digital displays – which are getting both cheaper and higher display quality - as a catalyst to drive mid-single-digit same-store revenue growth and margin expansion throughout the decade. Sharing similar characteristics to the cell tower REIT industry (and in fact, many billboards host cellular equipment), billboard REITs own the display structure and the use-permit but not the land underneath, leasing it from thousands of individual landowners for terms of 5-15 years.

{kind=link}

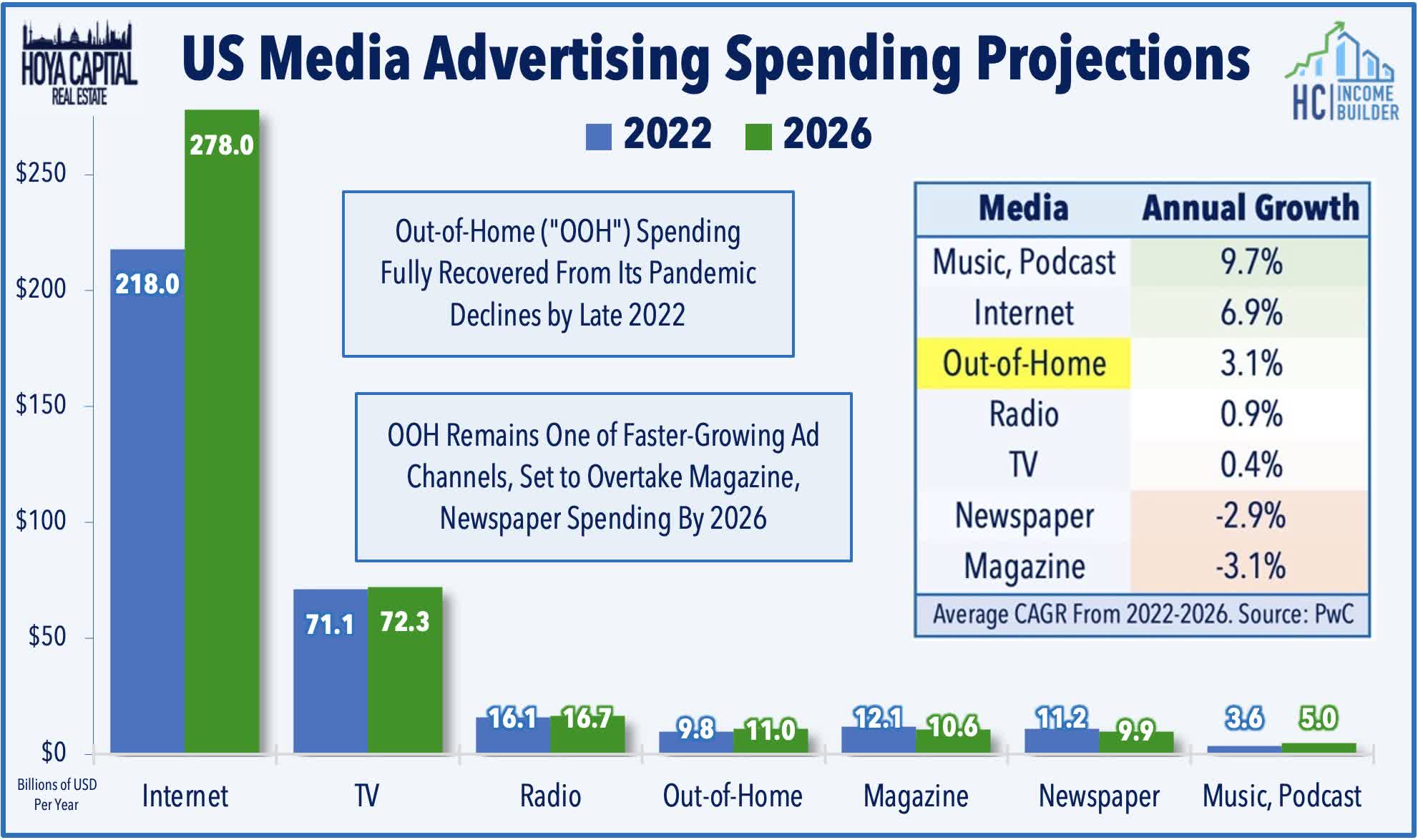

Unlike other media, there's "only one channel" on the highway. In the era of highly personalized advertising, advanced tracking, and ad-conversion metrics, OOH remains an attractive and cost-effective medium for mass-market and local advertisers as ads can't be skipped, blocked, fast-forwarded, or consumed by "bots." Spending on OOH advertising remains a small, but steadily growing segment of the advertising landscape. A report from PwC showed that spending on OOH is expected to fully recover by the end of 2022 and will have grown at a roughly 3% annual rate between 2019 and 2026, the third-strongest rate of growth behind internet advertising. Notably, the PwC report projects that OOH spending is set to overtake magazines and newspapers as the fourth-largest advertising channel by 2024.

{kind=link}

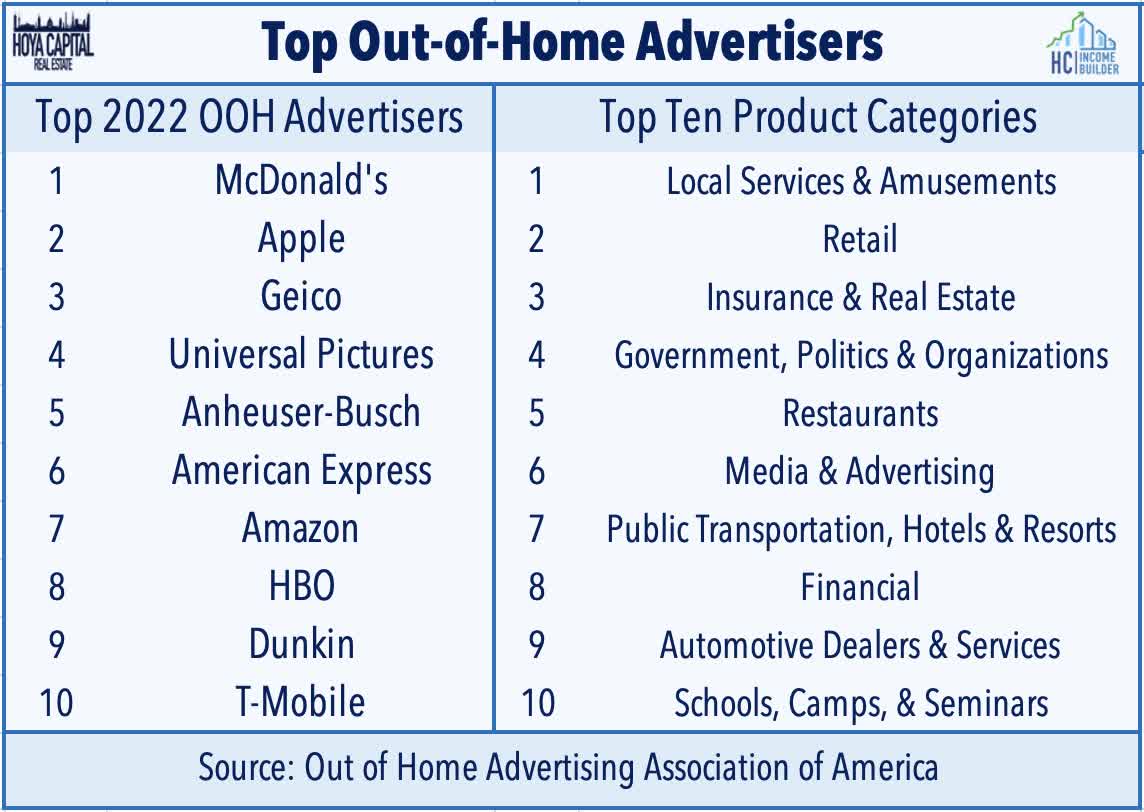

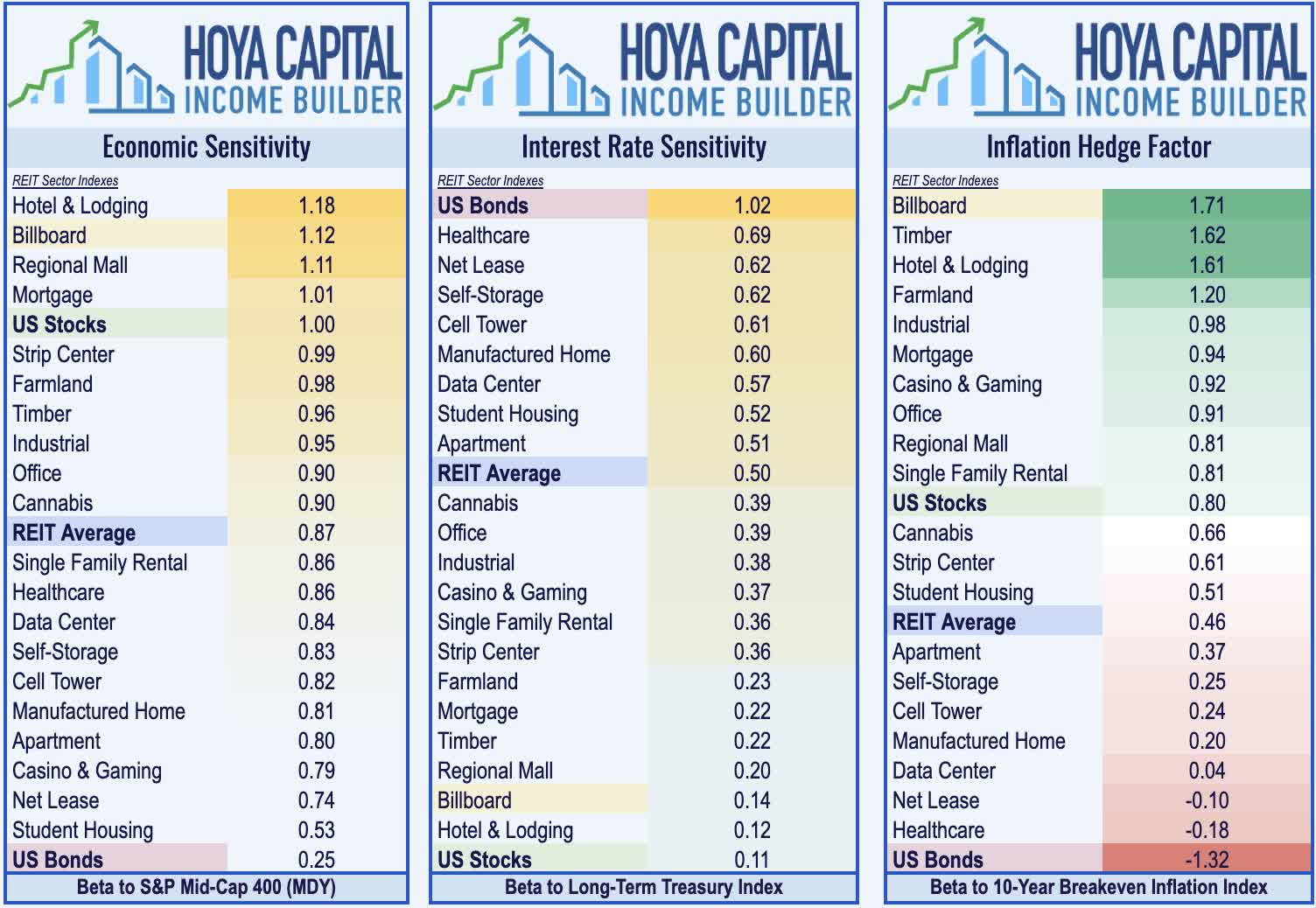

Advertising contracts on OOH displays typically run for 1-12 months and pricing is based on the billboard's size, viewability, and impressions. Somewhat ironically, many of the heaviest users of OOH advertising are technology companies including Apple ( AAPL ), Amazon ( AMZN ), AT&T ( T ), Netflix ( NFLX ), and Facebook ( FB ). As it relates to total OOH spending, the top ten product categories include local services, retail, professional services, politics, and fast-food restaurants like McDonald's ( MCD ). Ad spending is one of the first line items that businesses cut when times get tough, so naturally, Billboard REITs are one of the most economically sensitive REIT sectors, an attribute that has was on full display during the pandemic.

{kind=link}

On a "cost-per-impression" or CPM basis, OOH advertising consistently ranks as the cheapest advertising medium and is especially effective for national mass-market brands and for local services (restaurants, gas stations) in the immediate proximity. These three companies combine to control more than half of all billboards and transit displays in the United States, but the remaining third is quite fragmented with thousands of individual landowners and permit-holders. These REITs are in the process of converting many of the highest-value locations from static billboards into digital display boards, which can bring in 2-4 times more revenue than typical static display boards because of their dynamic messaging and pricing capabilities and typically require significantly less ongoing labor expense compared to static signage.

{kind=link}

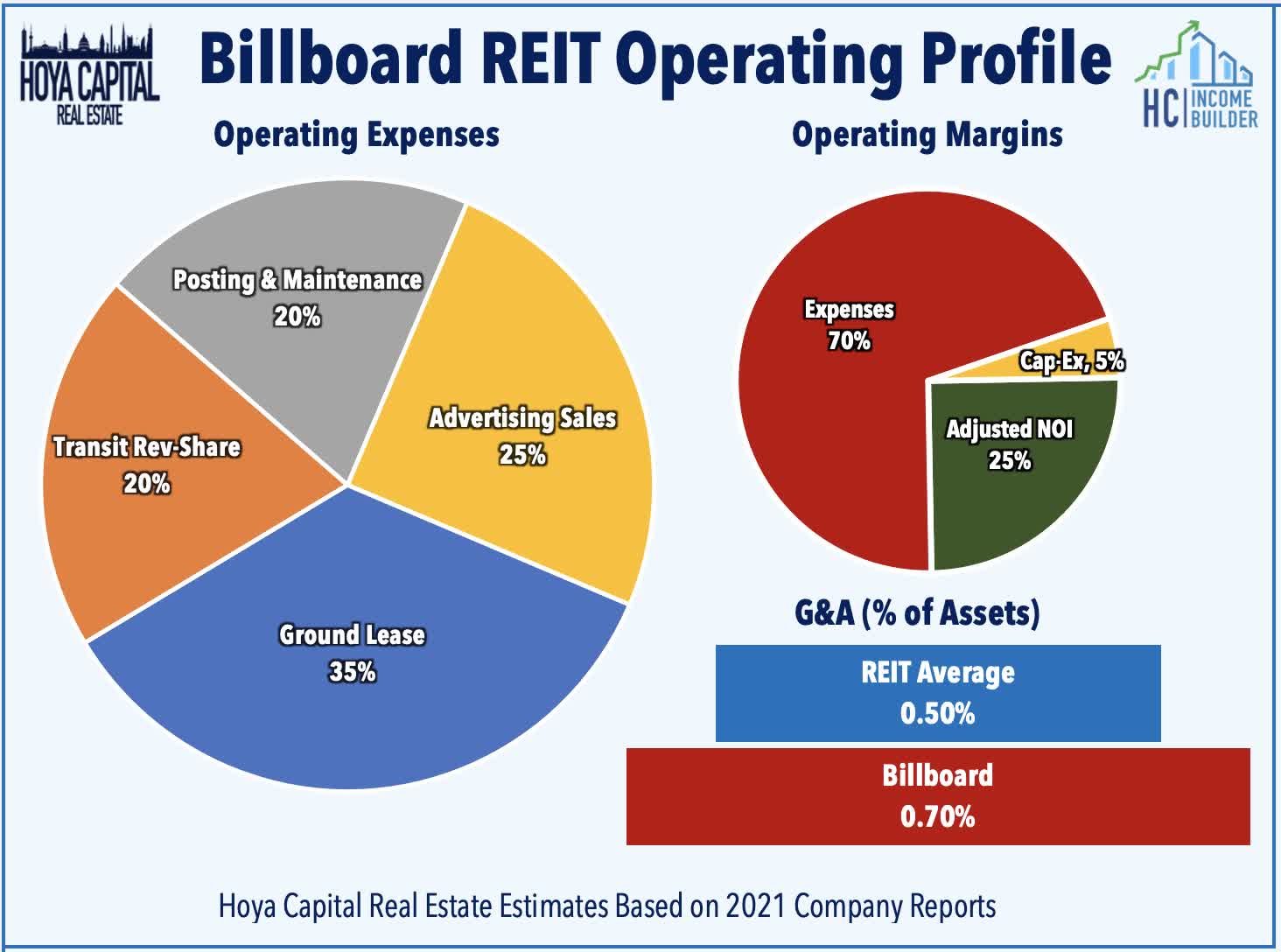

While the conversion to digital is helping to improve its margin profile, billboard ownership is still a relatively operationally-intensive business that requires a large advertising salesforce and continual maintenance in the form of posting and maintaining static signage. Operating margins are below 30% compared to the 65-70% REIT sector average and, as seen on full display during the pandemic, these businesses operate with a high degree of operating leverage due to the long-term nature of their ground lease liabilities and the short-term nature of their advertising contracts.

{kind=link}

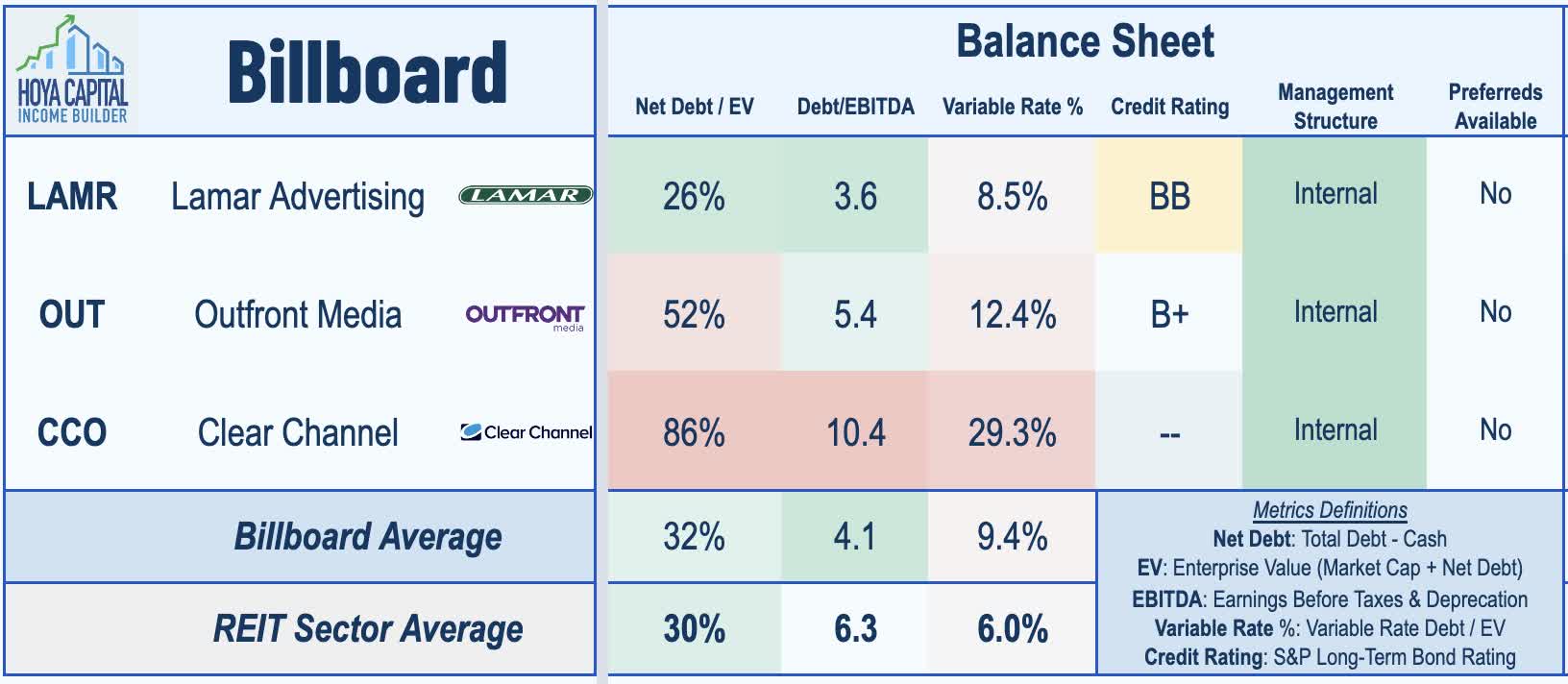

Capital expenditure needs, however, are relatively low at roughly 5% of revenues. The transition to digital should help to improve long-run operating margins but will result in elevated cap-ex as displays will need to be updated periodically with newer display technology to achieve the highest potential revenue. Access to capital - and cost of capital - will be especially important as these REITs invest in the digital transition. Lamar's balance sheet - with a debt ratio that is below the REIT sector average - is in healthier shape than that of Outfront's , but OUT's debt load is more manageable than the metrics suggest on the surface with a relatively well-laddered maturity profile and, notably, a similar percentage of variable-rate debt as LAMR.

{kind=link}

Billboard REIT Fundamentals

The lack of a commute for many Americans early in the pandemic slammed these REITs in 2020 as far fewer eyeballs were looking at Out-of-Home advertising displays. The mass transit segment of the OOH market was hit particularly hard amid a plunge in ridership, and while the traditional billboard segment has now seen a more-than-full recovery to pre-pandemic levels with spending levels now 15% above 2019-levels, transit spending remains about 30% below pre-pandemic levels. Spending from local advertisers bottomed at about 30% below pre-pandemic levels in 2020 but has now fully-recovered to 2.3% above 2019-levels. National brands pulled back more significantly at the depths of the pandemic with spending levels that were 50% below 2019 levels in 2020, but have since pulled-even with pre-pandemic spending.

{kind=link}

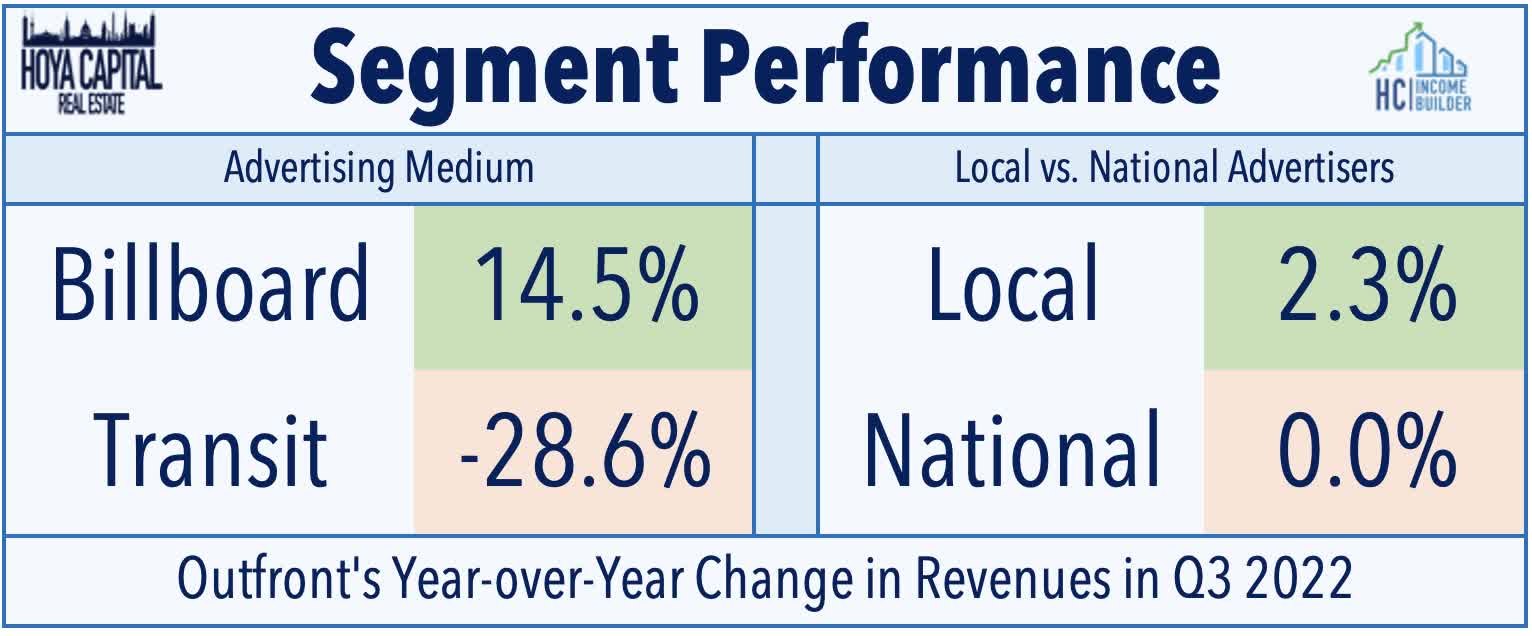

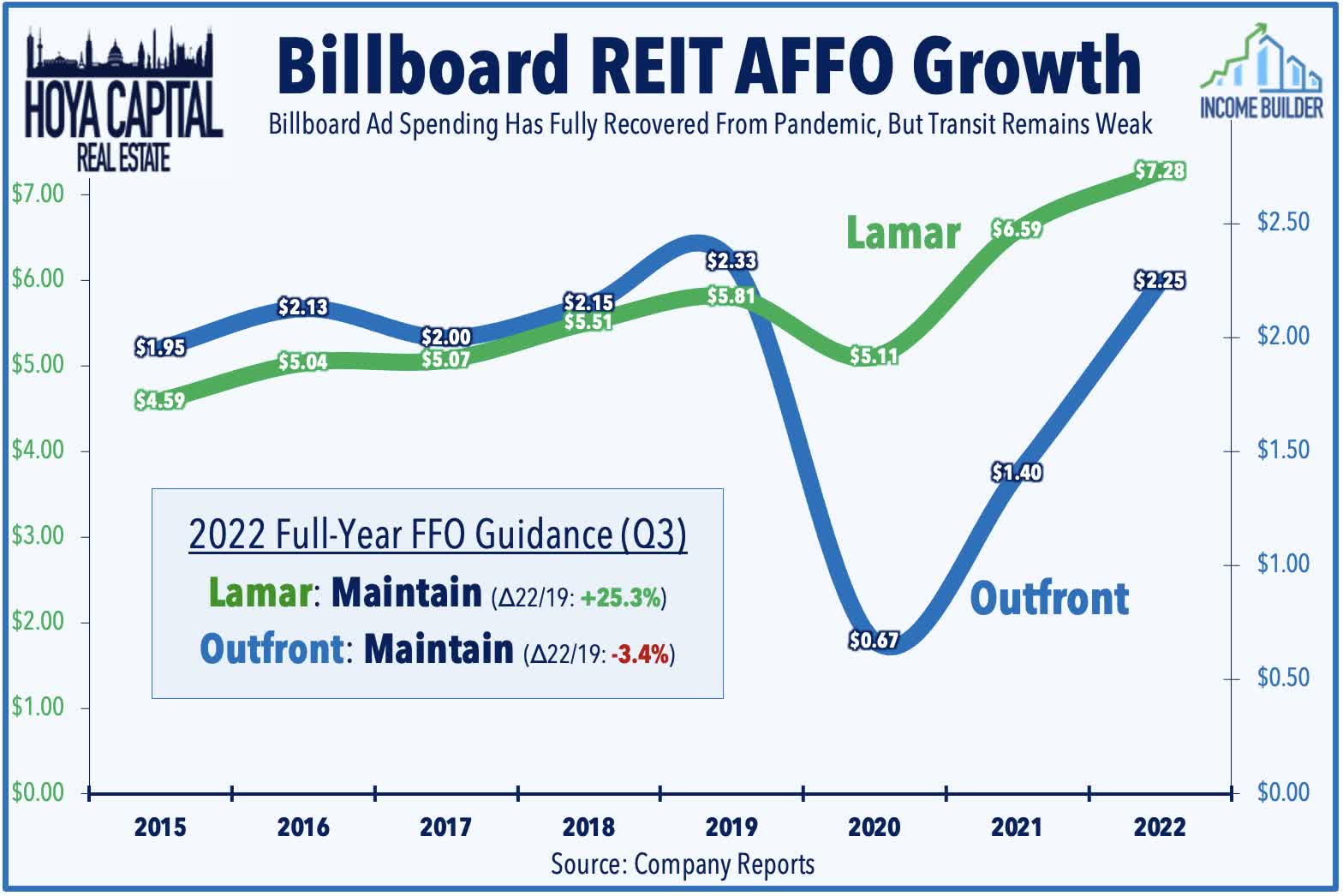

As discussed in our REIT Earnings Recap , Lamar Advertising ( LAMR ) remains further ahead in its post-pandemic recovery due to its more billboard-heavy portfolio. In its latest report, LAMR noted that it's "tracking to the top of our guidance range" which would raise its full-year FFO to levels that are 25% above 2019-levels. LAMR cited strong political ad spending as a key driver of revenue growth in Q3 and into early Q4, contributing 210 basis points of the total sales growth of 7.6% in October. LAMR did note relative weakness in demand from national brands with its national/programmatic segment growing just 0.3% in Q3 while its local business grew 6.4%. Outfront ( OUT ) - which has been burdened by its more transit-heavy portfolio - also reiterated its full-year FFO outlook which would bring its AFFO to within 4% of 2019-levels.

{kind=link}

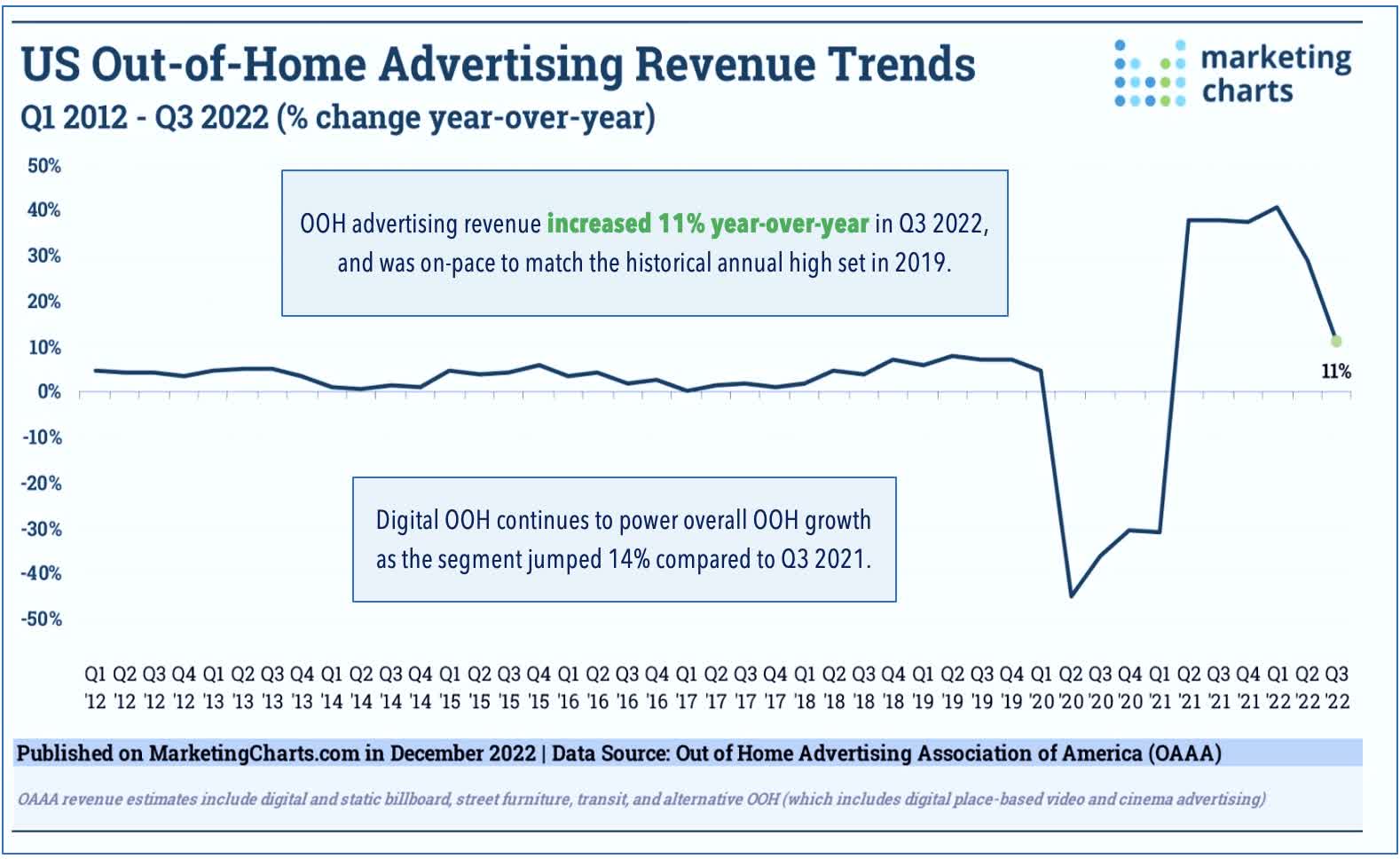

Data earlier this month from the Out of Home Advertising Association of America (OAAA) showed that OOH advertising revenues in Q3 2022 grew by 11% year-over-year (y-o-y), with revenues reaching $1.94 billion and for 2022 year-to-date, OOH spending is comparable with the historical YTD high set in 2019 at $6.4 billion. OAAA’s data also showed that digital OOH spending continues to outpace the traditional static format as Q3 digital spending rose by 14% year-over-year. Notably, 79 of the top 100 OOH advertisers increased their spending in Q3 while 32 of the top 100 more than doubled their spending according to the OAAA report. Of note, spending in the Media & Advertising segment grew 32% - driven by streaming and internet services - while spending from Hotels and Resorts grew 26%. Political spending rose to a quarterly record high of $134 million ahead of the midterm elections.

{kind=link}

Billboard REIT Stock Performance

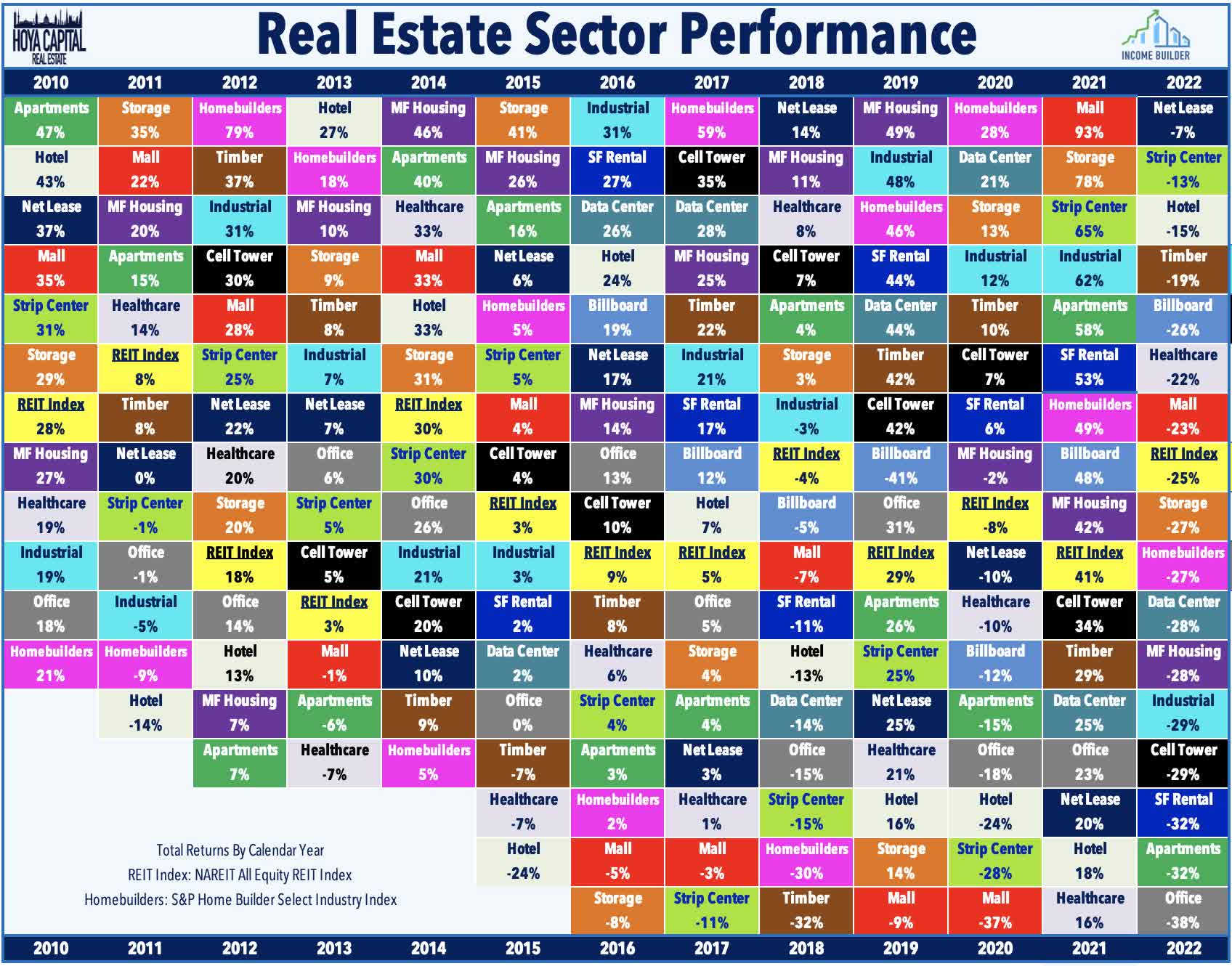

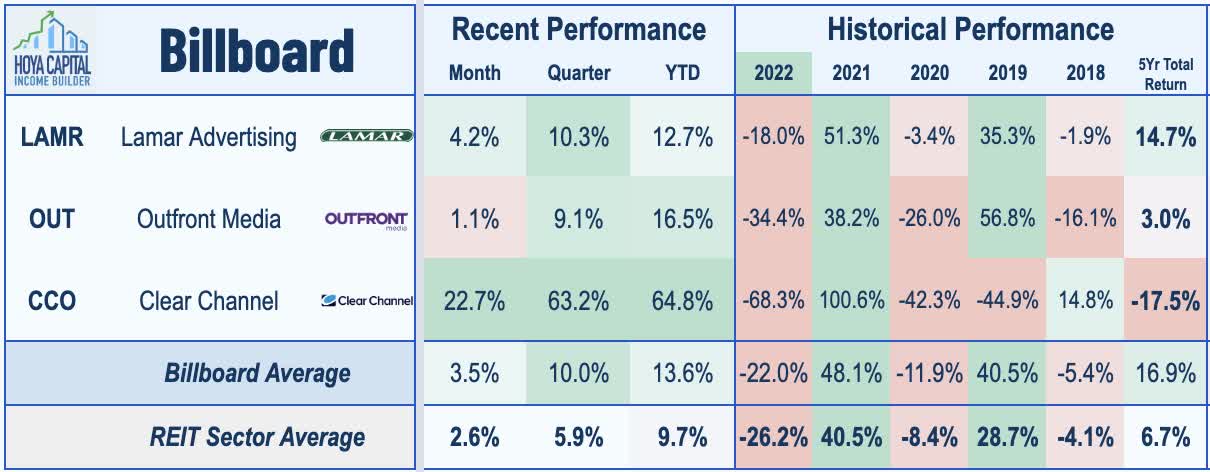

Billboard REITs were slammed harder than any other property sector besides hotels during the depths of the pandemic, plunging more than 65% from peak to trough in March 2020, but ended 2020 with rather modest declines of just 12% on average and have been among the better-performing property sectors since the start of 2021. The Hoya Capital Billboard REIT Index - a market cap-weighted index - outperformed the broader REIT index in 2021 with returns of nearly 50% and outperformed again in 2022, posting more-muted declines of 20% compared to the -25% decline from the Vanguard Real Estate ETF ( VNQ ) and roughly matching the declines from the S&P 500 ETF ( SPY ).

{kind=link}

Lamar's relatively conservative balance sheet and more pure-play focus on the higher-margin traditional billboard business has been rewarded by investors over the past five years, delivering average annual total returns of 14.7%, well above the REIT average of 6.7% during that time, and certainly, well above its peer Outfront , who's outsized exposure to transit advertising has resulted in comparable annual returns of only 3.0% during that period. Both REITs have significantly outperformed Clear Channel over most recent measurement periods, which has been burdened by a high debt load and a similar transit-heavy portfolio mix as Outfront.

{kind=link}

Billboard REIT Dividend Yield

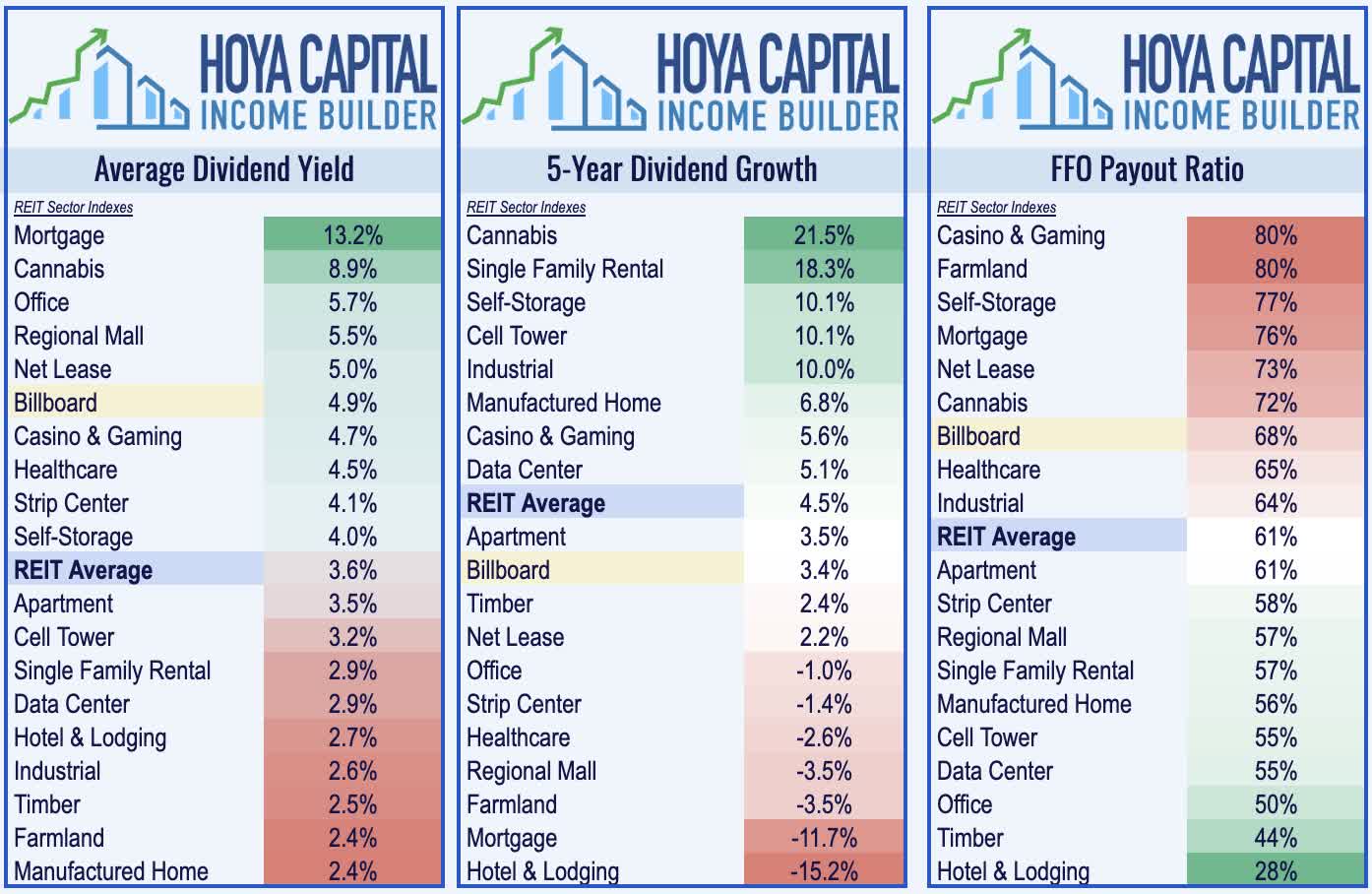

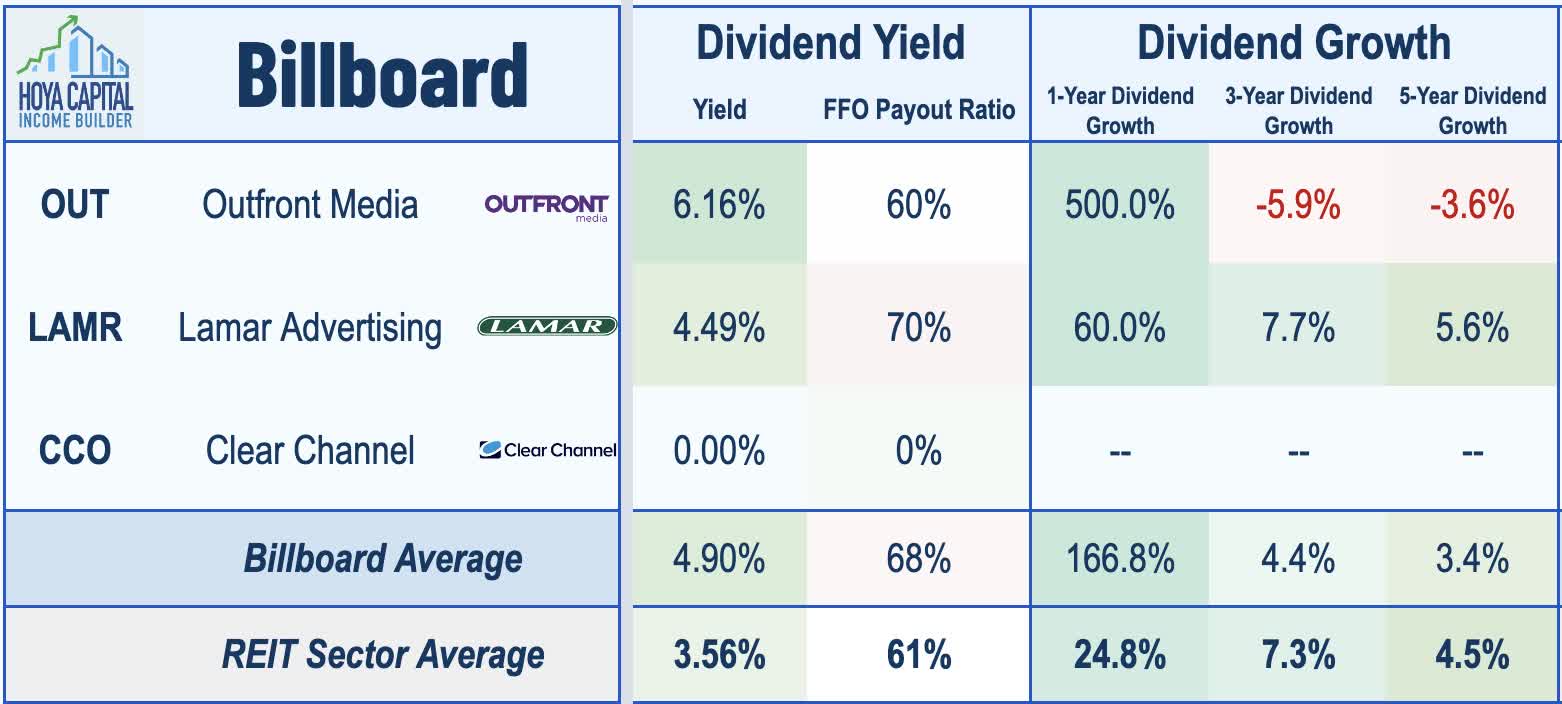

Before the pandemic, billboard REITs were among the highest-yielding REIT sectors but were briefly in the basement of the REIT sector after Lamar cut its dividend by 50% and Outfront slashed its dividend entirely in 2020. Lamar's strong operating performance over the past year has enabled it to restore its dividend back above pre-pandemic levels, but Outfront's dividend remains about 10% below its pre-pandemic level. On average, billboard REITs pay an average dividend yield of 4.9%, well above the REIT sector average of 3.6%.

{kind=link}

Lamar indicated in its third-quarter earnings call that it expects to raise its quarterly payout again this year to a $1.25/share rate, which would be 30% above its 2019 payout rate of $$0.96/share. LAMR also paid a $0.30/share special dividend on top of its regular quarterly dividend in December. After hiking its dividend in early 2022 to $0.30/share, Outfront has held steady at this level, amounting to a dividend yield of 6.16%. Given the relatively low payout ratio of 60%, we believe that OUT is likely to fully restore its dividend to pre-pandemic levels for its 2023 payouts.

{kind=link}

Key Takeaways: We're Paying Attention

Sharing similar characteristics to the cell tower REIT industry - a supply-constrained sector that is dominated by a small handful of asset owners - we believe that a high-single-digit annual FFO growth run rate is achievable over the next half-decade - absent any further pandemic-like hiccups - driven by 3-5% same-store revenue growth, a 1-2% contribution from margin improvement driven by digital conversions, and a 1-2% contribution from accretive acquisitions - a growth profile that is especially compelling for REITs trading with 4.5%-6% dividend yields and with a rather unique investment characteristics as one of the least-sensitive REIT sectors to interest rate movement and the single-best sector in our Inflation Hedge Factor metric. We still see some upside left in Lamar, but now see more significant potential in Outfront , which trades at single-digit Price-to-FFO multiples while paying a hearty and well-covered dividend with a yield of over 6%.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Billboard REITs: We're Paying Attention (Lamar Vs. Outfront)