BLRDY - Billerud AB: My Firm Initial Stance Is A Buy

2023-04-24 03:54:54 ET

Summary

- I recently got assigned several thousand shares of Billerud from an options play that I set at a strike of 100 SEK/share. On Friday, those options went ITM.

- Normally, I'd consider rotating - my options trading is primarily done for interest for cash, but all of my options are theoretically attractive companies at good prices.

- Billerud is a superb company - I'm keeping my shares, and assigning "BUY". Here is why.

Dear readers/followers,

I use options trading, specifically long-dated conservatively-priced cash-secured put options to enhance my returns by targeting a 9-14% yield on my cash over time. So far, in 2023, I have a success ratio of around 94.5% (meaning options that expire OTM) - Billerud was one, however, that recently went ITM and gave me a 1.5% Billerud position to "play" with.

In this article, I'll update you on Billerud and explain to you why I'm keeping my shares. I may go ahead and write some covered calls on the company at this time - or I might just keep it and add more over time.

This is a great company, and there are a few reasons not to "go" for it here.

Let's review!

Billerud AB - Qualitative packaging

I've actually invested in Billerud ( BLRDY ) a few times before, profitably. It's been a volatile company, but an investment with great potential at the right price. As a rule of thumb, whenever you see a double-digit share price , that's your signal to really pay attention.

That's why I put my contracts at the 100 SEK level, and that's why I'm pretty excited to be assigned. I could, technically, sell the position off at a profit (my actual cost basis is closer to 97 SEK thanks to good premiums) if I wanted to, but for the time being, I'm actually keeping it.

So what is Billerud?

Billerud is a sustainable packaging company. Over 90% of sales come from fresh fiber packaging materials, which is made from natural cellulose pulp wood. The company has an appealing asset base from the south to north of Sweden, with its production close to its raw materials. Billerud is a leading supplier of high-quality liquid packaging board, containerboard, carton board, graphic paper, kraft and specialty paper, and sack paper, and these products are primarily used to package food and consumer products , so timeless essentially.

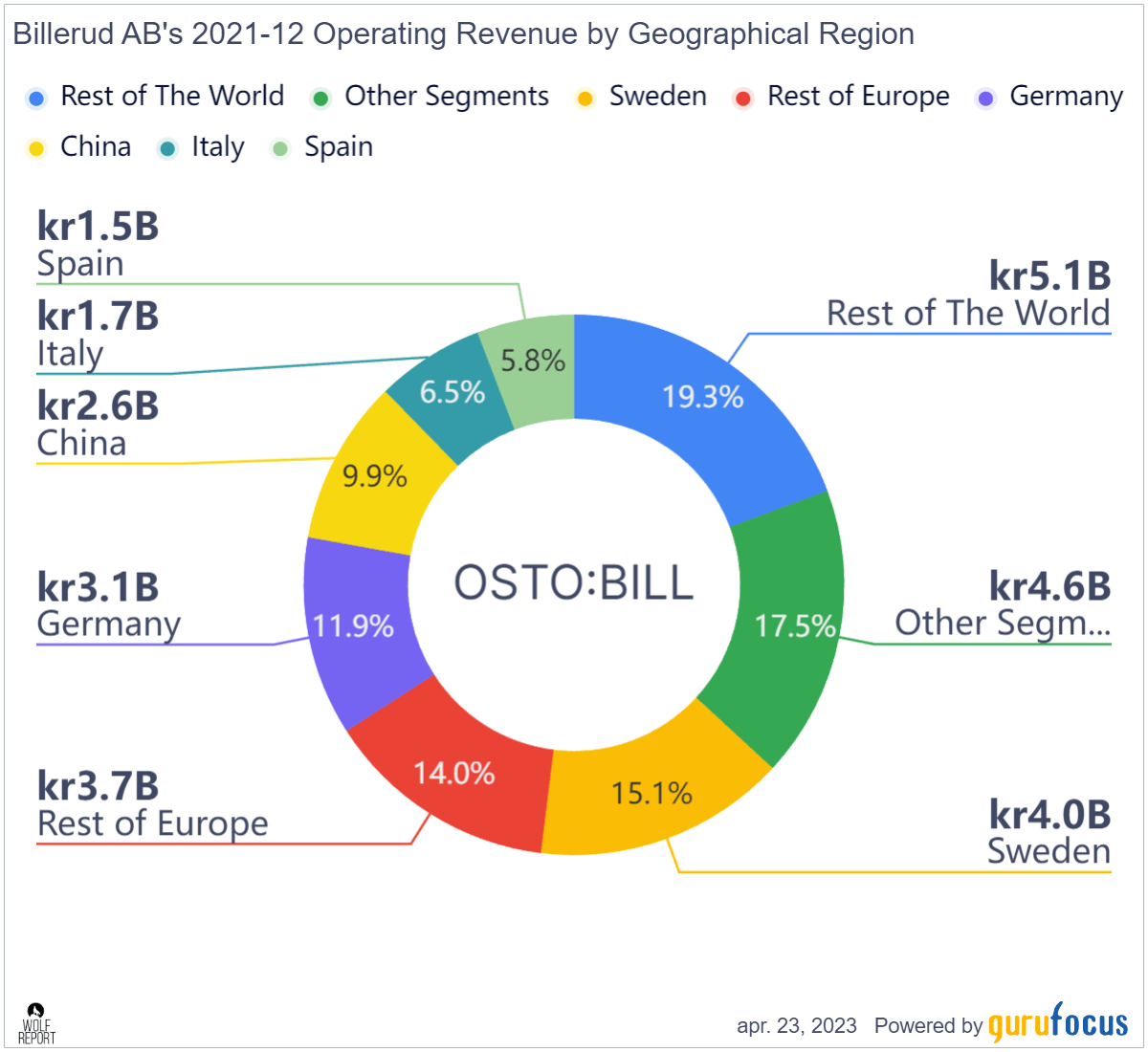

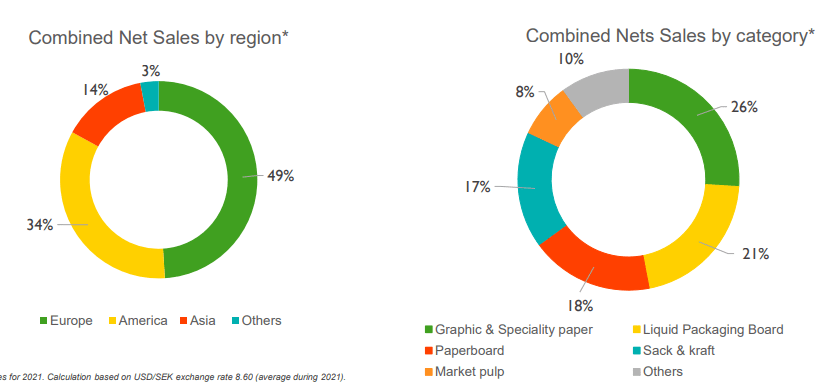

Billerud is technically speaking, mostly an EU-focused company. Here's the current sales mix, which as you can see, comes with a very EU-heavy exposure. it does have NA sales and operations/representation, but it's mostly EU for the time being.

Billerud Revenue Mix (GuruFocus)

{kind=link}

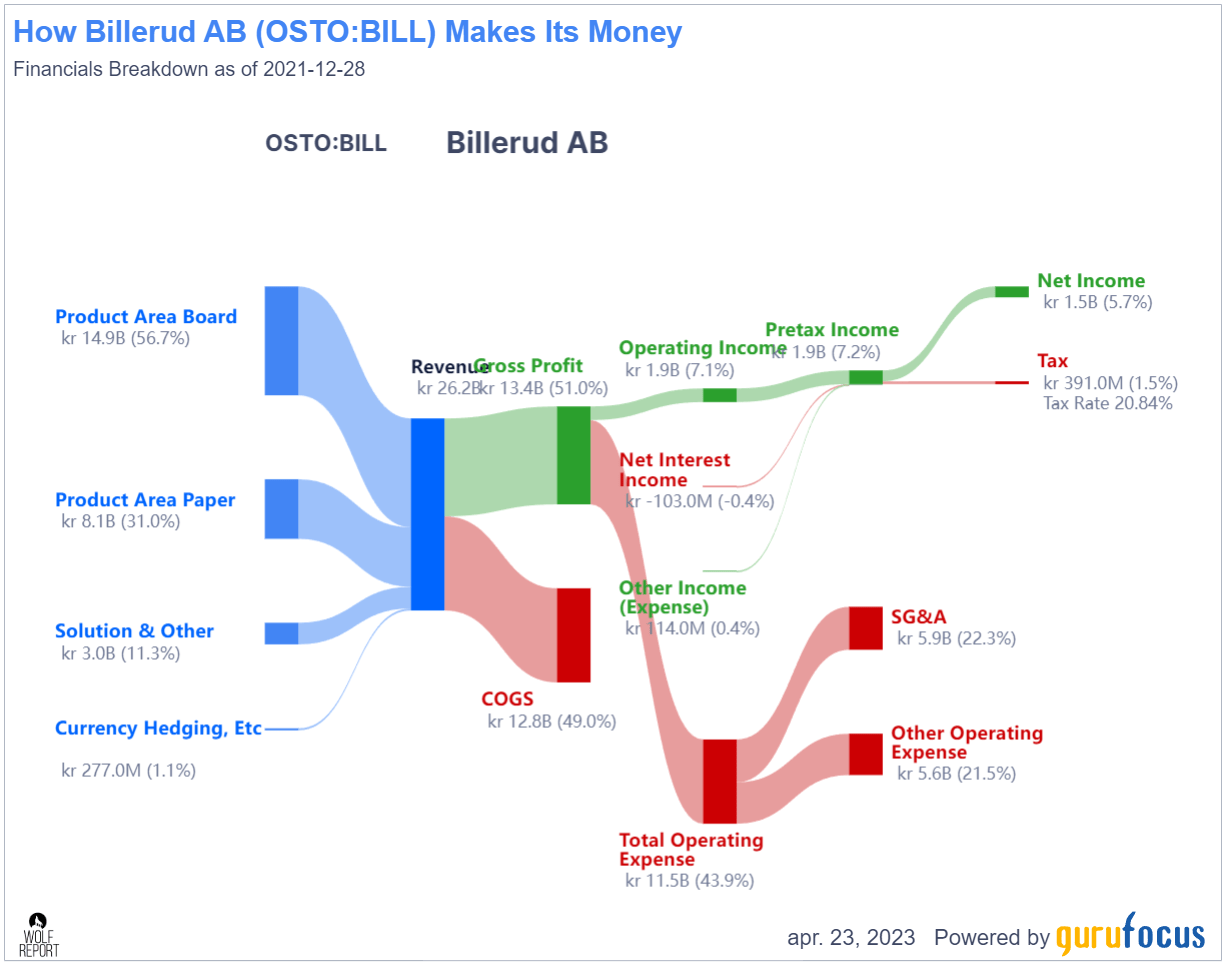

In terms of product mix, around 57% is board, 31% is paper, and 11.3% is solutions and other things. Here's an overview of how the company goes from sales to net revenue, and explaining its around 6% net margin.

{kind=link}

What do I like about Billerud, other than how the company's margins are actually decent? I like that Billerud has shown its ability to go from high debt to lower debt and significant profitability. 2022 was a record year for the company. Do not expect that result to be recurring - it's going down again, I'm sure of that. However, 2022 results have enabled Billerud to go to record net sales and profit, with an all-time ROCE high, as well as net debt to EBITDA of 0.6x.

{kind=link}

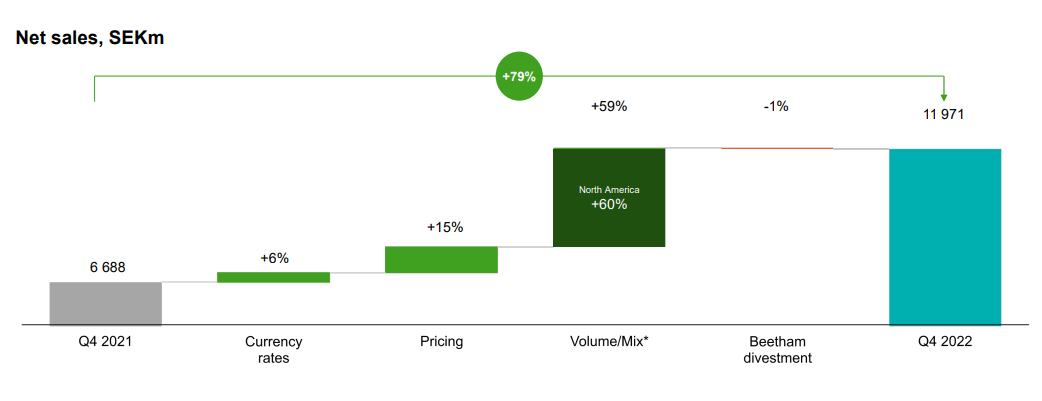

The year came to a 79% reported net sales growth, 14% of which was organic. NA was a heavy contributor, and this is despite excessive cost inflation for Europe especially. Adjusted EBITDA for the last quarter in 2022 was up almost 100%, EPS was up 145%. Net sales almost doubled, that's how good things were.

{kind=link}

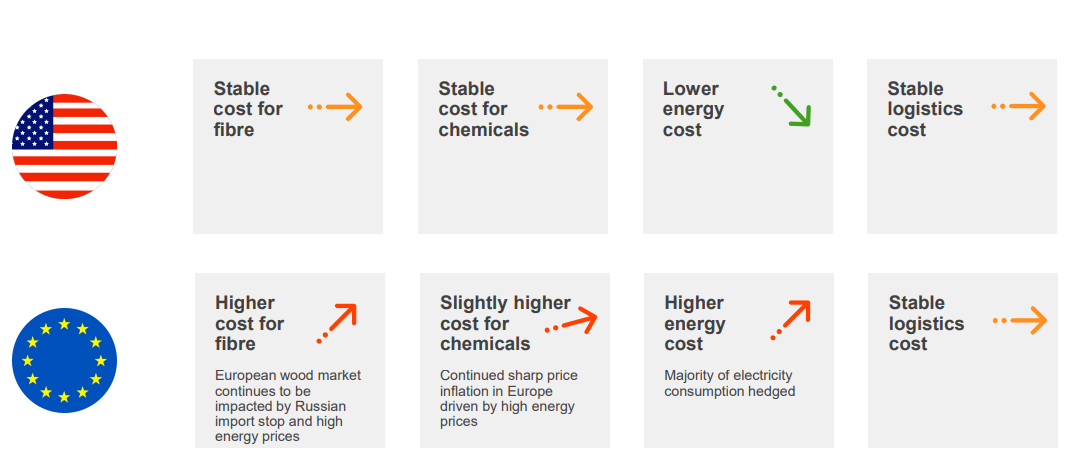

We can't underestimate the sheer impact of raw material and logistics costs. These effects were almost as much as the improvements from NA, over 1B SEK for the quarter. At the time of reporting, Billerud was above 120 SEK. However, the forecast going into 2023 is less positive, with a lot of more challenging dynamics. That is, what I believe, the market is picking up on here and why things are heading down here. NA and Europe are very different challenges, and Billerud unfortunately being EU-heavy, is set to be exposed to some fairly heavy cost increases that are bound to lower earnings for the coming year as well as single quarters.

{kind=link}

So, the company is targeting ambitions to lower costs going forward. Billerud is targeting 1.5B SEK in savings, 400M of which they're trying to deliver on in this coming year.

The positives to this company are, as I see it, obvious. packaging needs are going nowhere, and while plastic may be on the way out, paper and cardboard are going nowhere and only growing more innovative. Ignoring the cyclicality inherent to any company exposed to the spot prices for this sort of feedstock, Billerud isn't going anywhere and has enough customers and market share to be considered "safe" - at least how I see it.

The market for fibre-based packaging is expected to grow around 2-4% per year going forward, and NA and Europe are going to remain attractive markets for companies like these. NA is viewed as Billerud's largest growth opportunity.

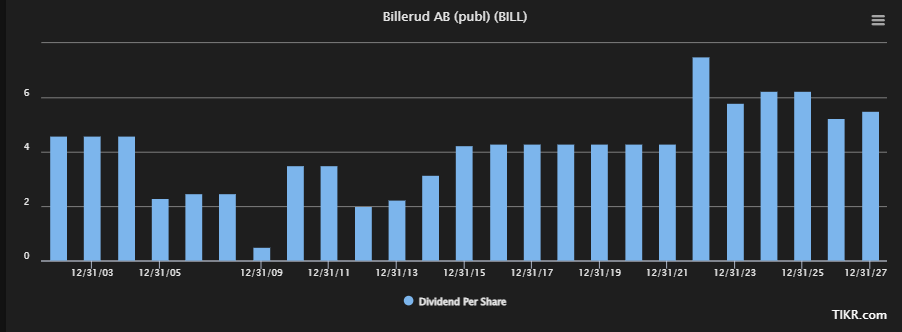

What's more, the company is an attractive dividend payor. 50% of net profit is distributed to shareholders, and the company's dividend has a strong history of stability even in times of high company investment and M&A.

Billerud Dividends (TIKR.com/S&P Global)

{kind=link}

Yes, there is some volatility - but the general direction is good, and you can expect for this to keep growing. The current dividend will likely decline going forward, so a 7-8% yield as we're seeing now, is likely going to be 5-6.5% going forward - but this is still a good yield for the sector.

More importantly, the company recently merged with NA-based Verso. Billerud has secured a 3.5B SEK rights issue. The M&A adds two new mills to the company's already appealing footprint, and the Verso M&A really pushes NA to the forefront, with an expected near-35% of net sales going forward.

{kind=link}

So what is Billerud now?

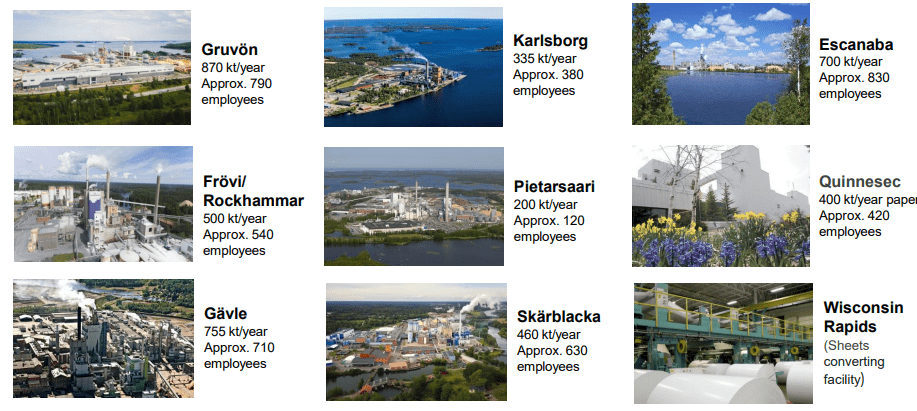

Billerud is a company owning 10 high-quality, modern production units across Europe and NA. It's a world-leading company in superior paper and packaging, employing 5,800 people. It can generate net sales of well over 40-50B SEK and manages volume above 5M kT/year.

{kind=link}

While we're likely to see continued volatility on part of this company going forward, we're also likely to see continued sales, sales growth, demand growth, and plenty of attractive dividends.

This statement of the company as a "qualitative business" leaves me with only one question, as it typically does.

At what price is the company a "BUY"?

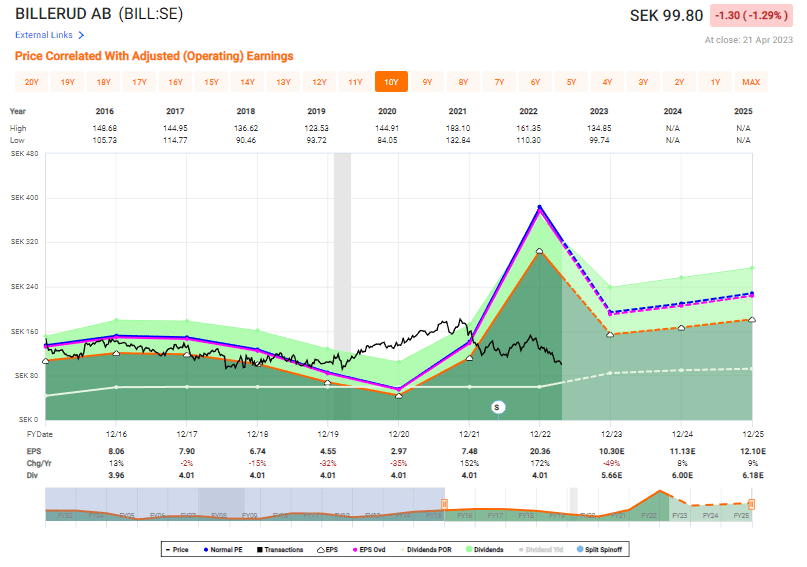

Billerud valuation

As I said earlier in the article, I've generally viewed Billerud as a must-consideration at a double-digit share price. In the past 10 years or so that I've been an active investor, that means I have been able to "BUY" the company exactly two times.

One time was all the way back in 2017-2018.

The other time is now.

Billerud Valuation (F.A.S.T graphs)

{kind=link}

S&P Global's view of the company is simple. 7 analysts follow it, giving it a range starting at 110 SEK and going up to almost 150 SEK, with an average of around 125 SEK, which implies a 24%+ upside here. Billerud plays with packaging giants such as Packaging Corp. ( PKG ), WestRock ( WRK ), UPM ( UPMKY ), Enso ( SEOJF ), Klabin ( KLBAY ), Huhtamäki ( HOYFF ), and others. Many of these companies are already in my portfolio, and the addition of Billerud is to me, a very positive one.

As I said, I could technically sell my stake and still get a decent profit - my cost basis is well below the assignment price, or the current price. But at this juncture, I'm very happy to be able to own Billerud at double digits. I've actually gone ahead and written a whole new set of cash-secured puts at strikes of 87-92 SEK/share. Should the share price reach such levels, I'll be thrilled to take advantage of this and expand my position to maybe 3-4% in a very short time.

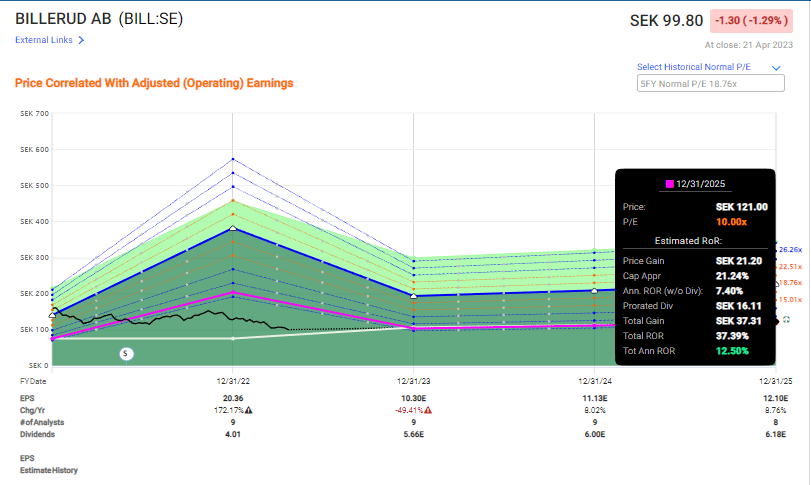

The upside here is phenomenal. Billerud typically trades at a valuation of around 18-19x. That's technically above where we want to see a company in this volatile industry - so let's lower that to 15 just to be safe. However, the normalized P/E even with a very normal EPS here is below 9x P/E. Even if we just assume 10-11x P/E, that's a potentially market-beaten RoR under current forecasts.

Billerud Upside (F.A.S.T graphs)

{kind=link}

Again, that's a 10x P/E. If you're willing to start expecting a range of 15x P/E you're playing with annualized RoR starting at double-digit 12.5% for 10x and going up to almost 30% per year, or close to triple-digits until 2025E.

And that's with an assumption of a 49% EPS drop followed by relatively low growth rates.

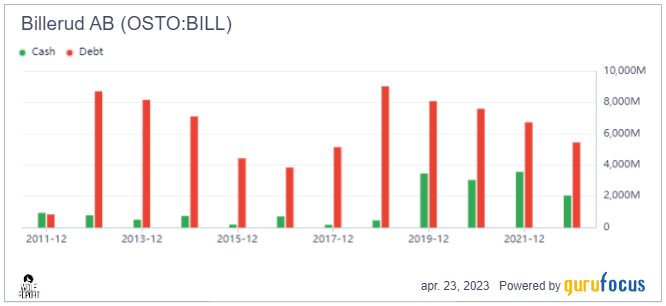

Even using a low growth rate of only 3-5% on a reverse DCF model, simple modelling gives us implied share prices well north of 200 SEK per share - and remember, this company has traded as high as 175 SEK/share back in 2021. So there's plenty of upside potential to consider here. The debt isn't all that bad either. The worst of the debt was assumed by the company back in 2018, and since that time, company leverage has actually gone down, while cash has stayed remarkably strong.

Billerud cash/debt (GuruFocus)

{kind=link}

Both on a high and more granular level, the positives by far outweigh any potential negatives for this company. A Piotroski F-Score marks the company at 8/9. It's a highly unlikely manipulator, and every single one of its historical valuation ratios, starting with PB, P/E, P/S, RevShare, and yield, are close to or at 2-10 year lows.

Risks?

They do exist - but they're mostly macro-related. Billerud as a business is exposed to plenty of cyclicality in the industry due to the feedstock. Also, packaging and pulp/paper companies are notoriously up and down during times of economic uncertainty. Thirdly, and perhaps most seriously, this company has a history of not having the most communicative or "best" in class management. There have been plenty of switches for the past decade. I like the current iteration - capable seemingly better than we've seen - but it's worth keeping an eye on to make sure that goals are achieved and that there is no uncertainty.

Nearly every indicator is calling to us here that this company is significantly undervalued. Billerud is also in the high 70th or low 80th percentiles in profit metric when it comes to the forest industry overall. In Gross margins, it's in the 93rd percentile. In terms of comps/peers UPM, Enso, Holmen, and Klabin are larger - though Klabin is not by much, and is likely to be overtaken by Billerud going forward. That makes Billerud, Holmen, Enso, and UPM as well as Huhtamäki some of the companies I would want to be owning. And the funny thing is, with the addition of Billerud, I now own non-trivial stakes in all of them.

And at very attractive price points as well.

So while you may not have heard of Billerud, or may ask yourself if this sort of company is one you'd want to be owning, my very clear message to you, and my firm initial stance and thesis on this company here is "YES" and "BUY".

Here are the details of my initial thesis for Billerud.

Thesis

- Billerud is a very solid packaging/forestry company with assets and sales in both NA and Europe. It's top-tier in terms of margins and profitability, and after its recent M&A, I believe it's in a position than ever before. At the right price, the combination of packaging resilience and dividend payouts makes Billerud an absolute "must-have" to me.

- My current PT comes to a conservative 10-12x P/E, which implies a 125-130 SEK share price - I go to 127.5/share.

- That makes the company a "BUY". I was recently assigned 3000+ shares at a cost basis of ~97 SEK, I'm buying the company in my corporate account, and I'm going deeper when possible.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

Billerud AB: My Firm Initial Stance Is A Buy